cagkansayin/iStock via Getty Images

Introduction

As equities fall and as bonds fall, investors and in particular, retirees have the challenging task of scouring the world for reliable yields. Some sectors such as mREITs present high yields to the tune of 13.94%, but at the cost of meaningful capital erosion such as a 30.39% decline in 2022, which ultimately makes them value destructive investments.

It is reasonable to believe that high quality yields coming from sectors that also have strong relative strength are more sustainable. This makes Chord Energy Corporation (NASDAQ:CHRD) an attractive option.

Thesis

I am bullish on CHRD due to 3 key reasons:

- Lack of O&G upstream capex makes E&P players relative outperformers

- CHRD is returning value to shareholders

- CHRD is printing consistent volumes outperformance with low variation.

Lack of O&G upstream capex makes E&P players relative outperformers

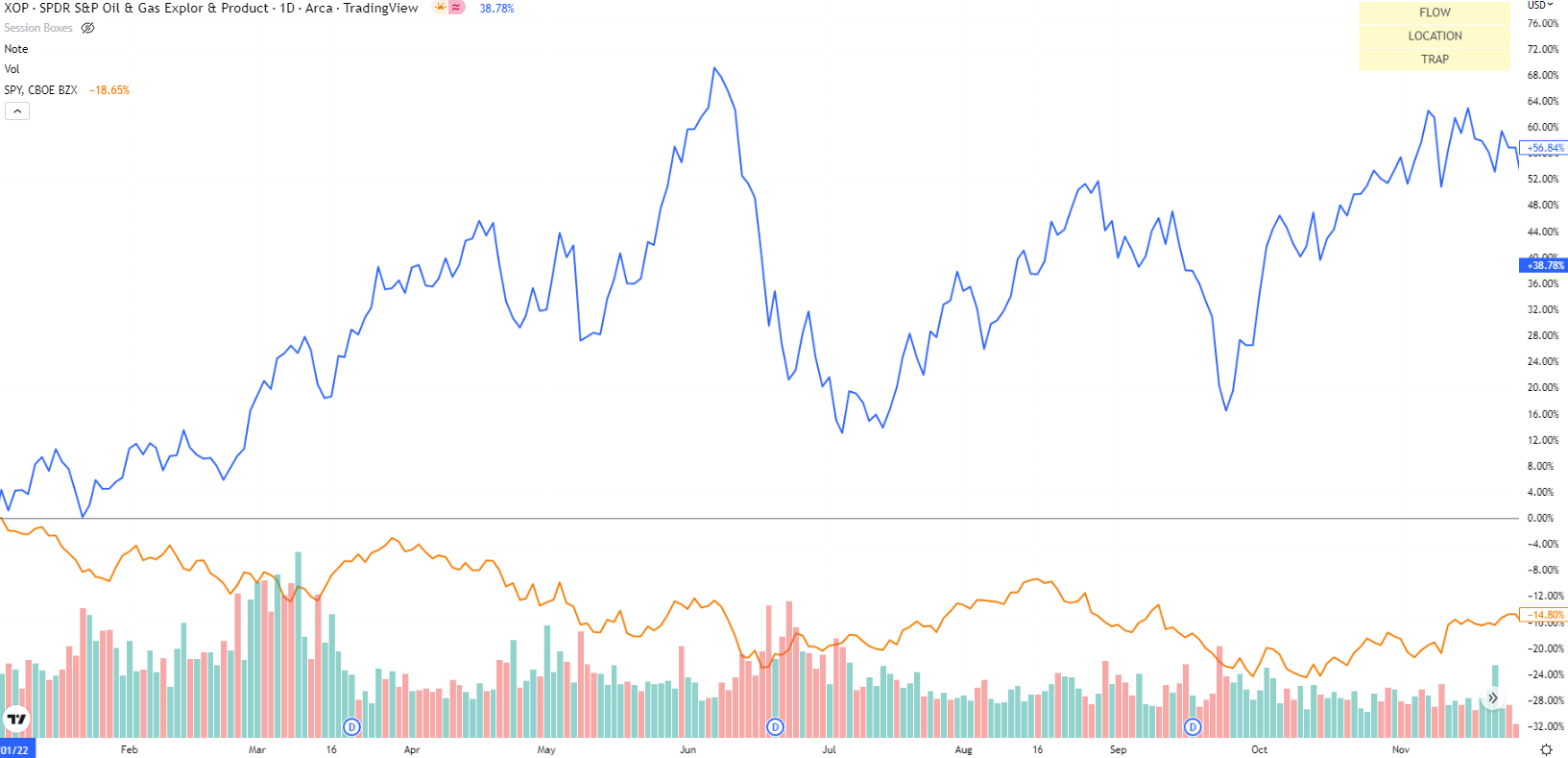

The O&G upstream industry has outperformed the S&P 500 (SP500) by a massive 71.64% in 2022, as evidenced by the performance the S&P Oil & Gas Production ETF (XOP):

Relative Performance of XOP vs S&P500 (Trading View, Author’s Analysis)

This has been mostly due to energy deficits triggered by geopolitical tensions leading to higher prices without offsetting supply. So far, upstream O&G players have been reluctant to invest in capacity expansions and thereby ease out the supply situation. This cautionary expansion stance is being adopted as the industry has faced a large amount of criticism for expansion from government and ESG evangelists.

CHRD is returning value to shareholders

In its Q3 FY22 investor presentation, Chord Energy Corporation management stated its intention to return more than 75% of its free cash flow (“FCF”) to shareholders. The reinvestment rate for the business is low at 36%, which corresponds to maintaining current levels of production to slightly growing production. The company does not intend to opt for major capex expansion plans.

My previous analysis on the O&G sector has posited the view that upstream capex expansions will eventually occur, as the world is heading towards a large energy deficit situation. Indeed, there is traction amongst private E&P companies in upstream capex already.

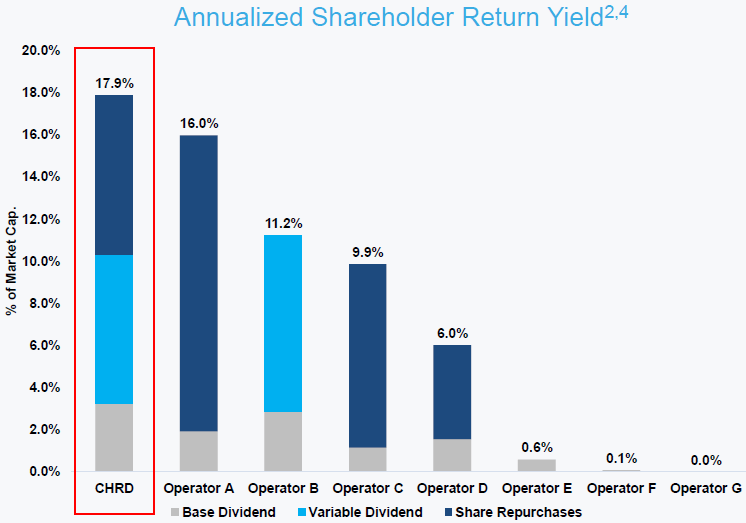

Now when a new wave of capex expansions occur, shareholders in companies that are late adopters of the expansions trend will see higher returns in the near term as they won’t be spending on capex. I believe this is the case for Chord Energy Corporation, as evidenced by the fact that it has proven its commitment to being one of the leaders in returning value to shareholders:

CHRD Annualized Shareholder Return Yield vs Peers (CHRD November 2022 Presentation)

Key peers include Civitas Resources (CIVI), Callon Petroleum Company (CPE), Enerplus Corporation (ERF), Magnolia Oil & Gas Corporation (MGY), Matador Resources Company (MTDR), PDC Energy (PDCE) and SM Energy Company (SM).

As can be seen in the graphic above from Chord Energy Corporation’s Q3 FY22 Investor Presentation, CHRD has the highest annualized shareholder return yield compared to peers with 17.9% of its market capitalization value flowing back to shareholders via a mix of dividends and share repurchases.

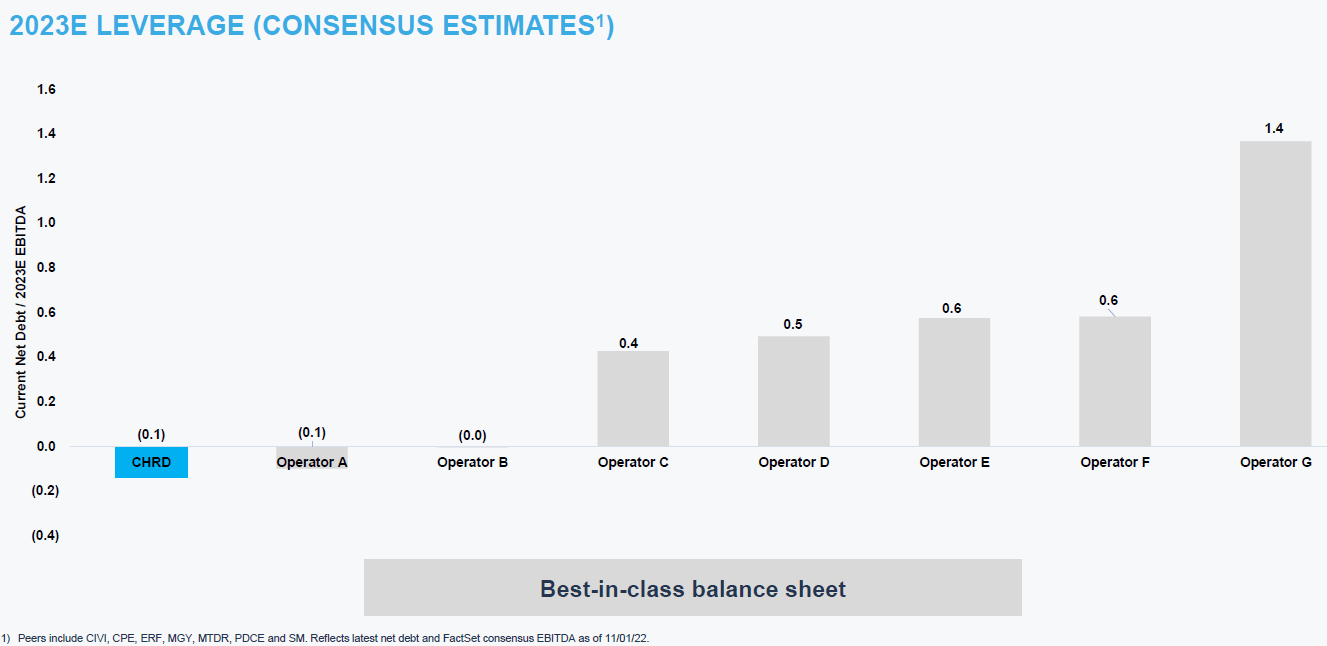

Note that this is accompanied by lower financial leverage risk as well, since consensus estimates put CHRD in a net cash position with the lowest leverage levels among its peers:

CHRD Leverage vs Peers (CHRD November 2022 Presentation)

Thus, investors looking for sustainable yields arising from sectors that have relative strength in the market should find Chord Energy Corporation a prime candidate for their portfolios.

CHRD is Printing Consistent Volumes Outperformance With Low Variation

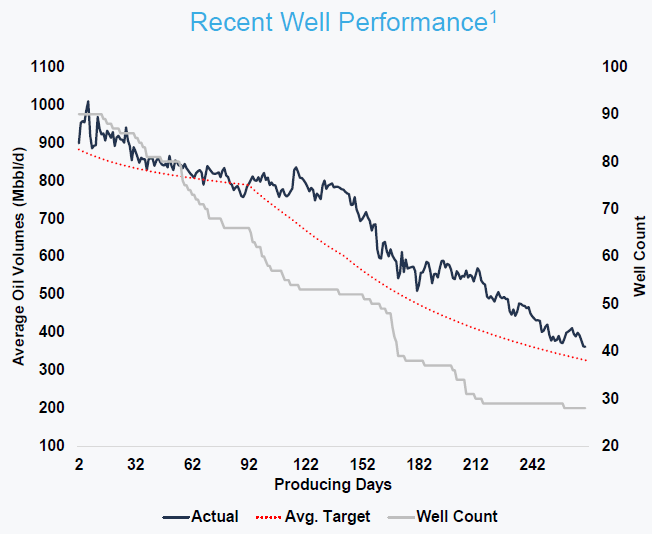

CHRD has consistently out-delivered in volumes across its O&G wells:

CHRD Well Performance (CHRD November 2022 Presentation)

Moreover, CFO Michael Lou commented in the Q3 FY22 earnings call that a large driver of this is the fact that the basins they operate in are mature and hence yield greater predictability. This would lead to lower variation in volume performance; an attractive feature when the main play is focused on consistent milking of assets for shareholder return.

Furthermore, management has indicated that they expect this momentum to continue:

…we’ve got a lot of activity in the fourth quarter.

All this suggests to me that the underlying earning assets are in a very healthy and predictable run-rate situation, which improves the resiliency and quality of the shareholder yields.

Technical Analysis

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post, which explains how and why I read the charts the way I do, utilizing principles of Flow, Location and Trap.

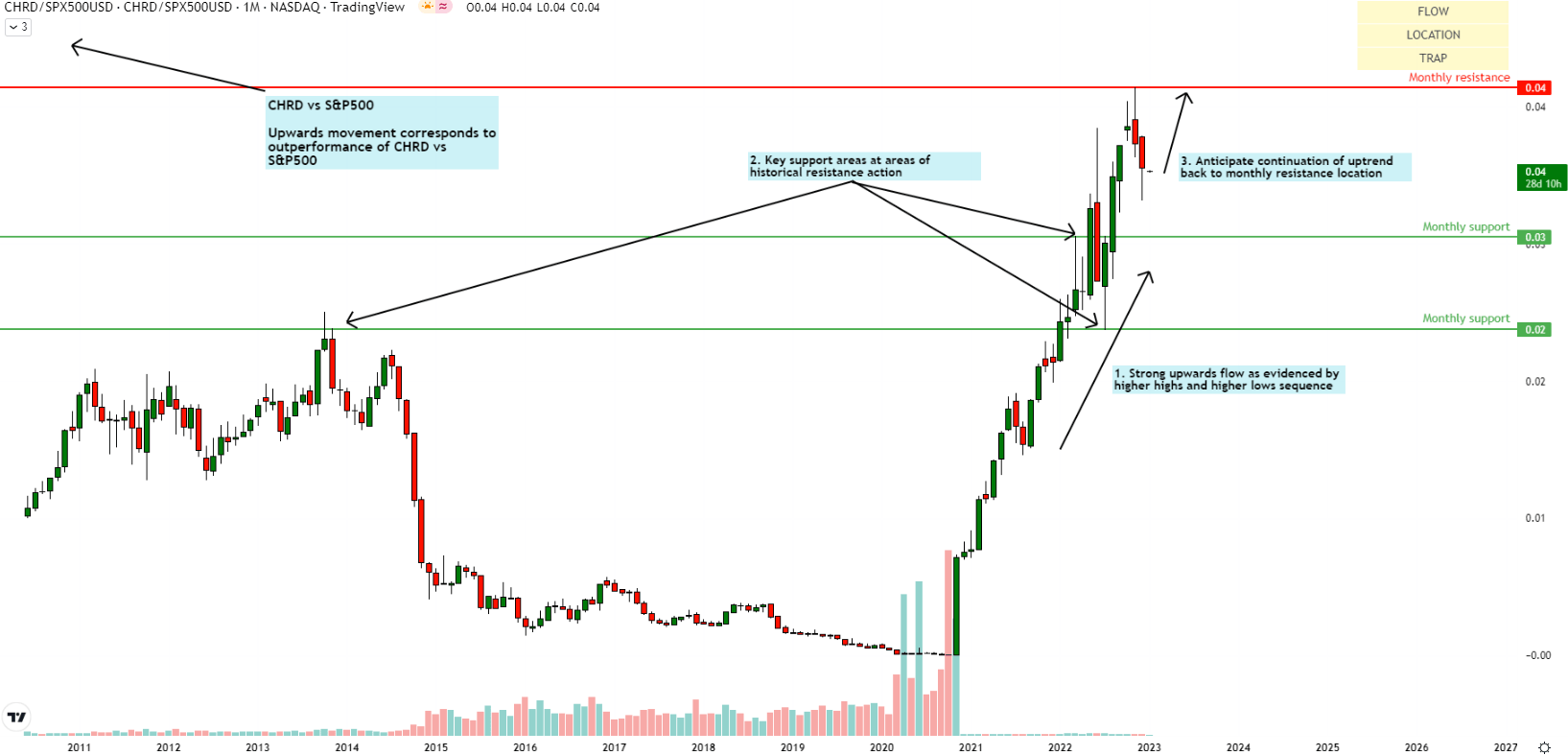

Relative Read of CHRD vs SPX500

CHRD vs SPX500 Technical Analysis (TradingView, Author’s Analysis)

CHRD/SPX500 is in a very strong uptrend, suggesting outperformance over the S&P 500 (SPY, SPX). I do not see any signs of trend slowdown, which I deem to have happened when prices make an equal low amid an uptrend. So far, there have been consecutive higher lows. Thus, I anticipate the trend movement to continue at least back up toward the monthly resistance.

Standalone Read of CHRD

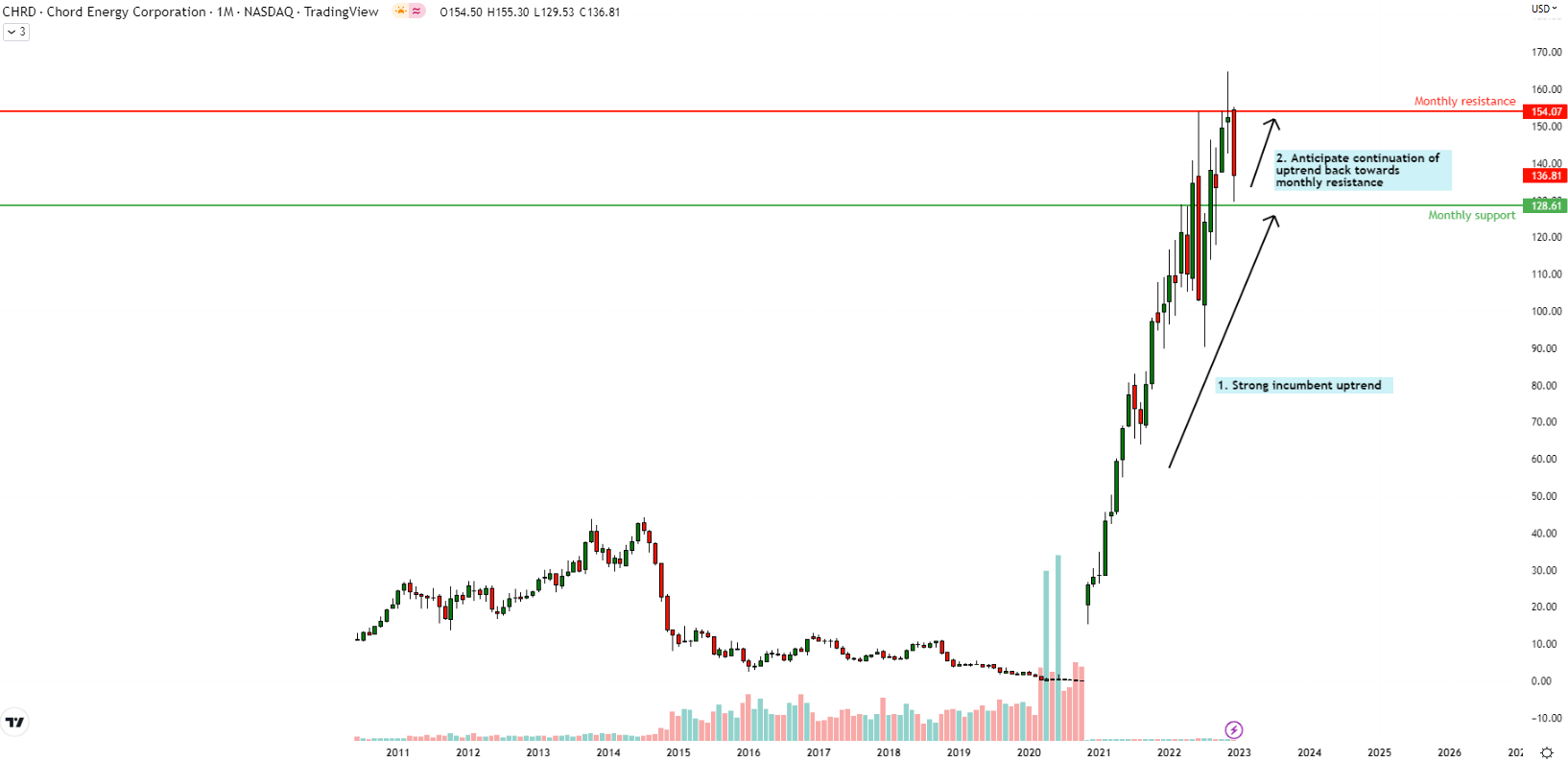

CHRD Technical Analysis (TradingView, Author’s Analysis)

On an absolute basis too, CHRD shows a very strong uptrend without any signs of trend slowdown. Thus, I anticipate a continuation back up towards the monthly resistance at $154.07 as the current pullback ends.

Takeaway & Positioning

I think Chord Energy Corporation is a very solid dividend stock powered by dual tailwinds of elevated O&G prices in an expansion-constrained upstream sector, and consistent, predictable volume production. The company’s top-tier position in return of capital yield makes this stock especially attractive to retirees. The technicals suggest bullishness as well, and I anticipate CHRD to continue outperforming the S&P 500. For these reasons, I rate Chord Energy Corporation a “buy.”

Be the first to comment