The Global X Q1 China Sector Report can be viewed here. The report provides macro-level and sector-specific insights across the eleven major economic sectors in China’s equity markets.

Summary

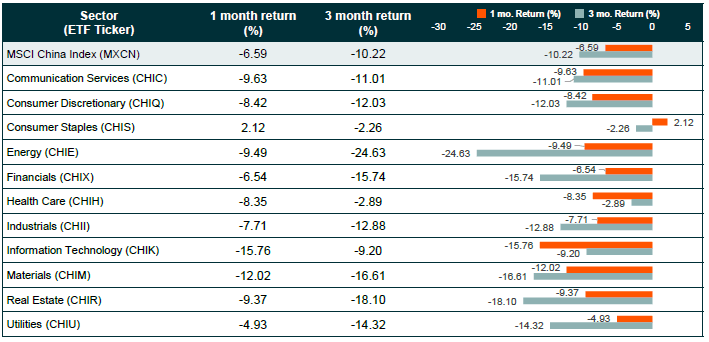

In the first quarter of 2020, the spread of COVID-19 in China led the authorities to introduce a slew of measures to control it. These included travel bans, business closures and quarantines that substantially disrupted normal activity and have clearly taken a heavy toll on China’s economy. All 11 Global Industry Classification Standard (GICS) sectors in China generated negative returns in Q1 2020. The Consumer Staples, Healthcare and Information Technology sectors outperformed the benchmark Broad China Index (MSCI China Index).1

{kind=link}

Source: Bloomberg as of Mar 31, 2020

Performance shown is past performance, based on the NAVs of the underlying sector ETFs and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. To view standard performance each of the funds, please click on the links available under “Related ETFs” below this post.

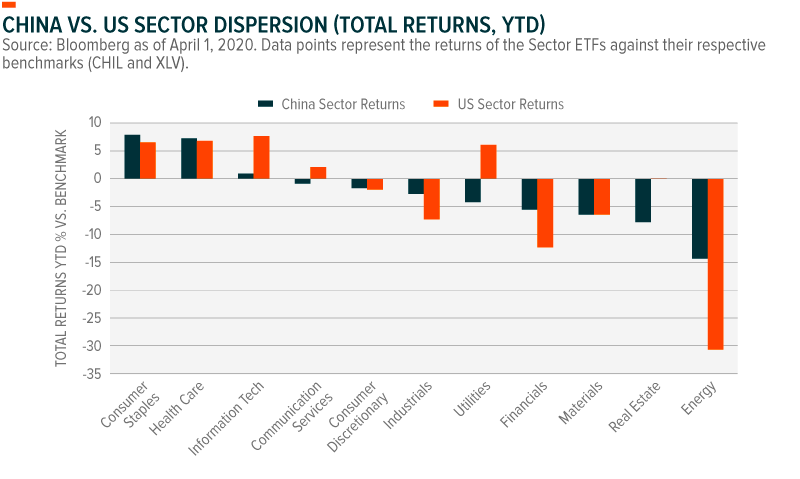

China and US Sectors Show Similar Dispersion at End of Q1

With global efforts to contain the spread of COVID-19, and the ensuing economic and equity market impact, both Chinese and US equity markets turned downwards. In Q1 2020, the S&P 500 Index fell -19.6%, while the MSCI China Top 50 Select Index fell -11.5%.2 Across both markets, each of the eleven major economic sectors performed negatively, but on average China Sectors outperformed US Sectors by roughly 9.6%.

Notably, the dispersion of sector returns in China this quarter were narrower than in the US – opposite to historical trends. This result could be due to greater oil price sensitivity in the US as well as strong intervention by the Chinese government to support its economy amid the COVID-19 outbreak.

Note: Average refers to a simple average of the individual sector returns of the MSCI China Sector and MSCI China Large Cap indexes, as well as the S&P 500 and S&P U.S. Select Sector indexes.

Comparing and Contrasting US and China Sector Performance

At the individual sector level, we saw similarities between China and the US with both countries sharing the same top three performing sectors (Health Care, Consumer Staples, and Information Technology) and substantial overlap among the underperformers.

Such parallels between the US and China are rare and likely tied to the global nature of this quarter’s main market-driving forces, which are the global COVID-19 pandemic and an oversupply of oil resulting from the ongoing OPEC-led price war.

In the chart below, we show the performance of Global X ETFs that are designed to track China’s 11 GICS sectors relative to CHIL, a large cap ETF tracking the 50 largest stocks in China, which is down 13.3% YTD.3

Performance shown is past performance, based on the NAVs of the underlying sector ETFs and does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold, may be worth more of less than their original cost and current performance may be lower or higher than the performance quoted. To view standard performance each of the funds, please click on links available under “Related ETFs” below this post.

China Sector Outperformers

In China, the best performers this quarter were Health Care (NYSEARCA:CHIH), Consumer Staples (NYSEARCA:CHIS), Information Technology (NYSEARCA:CHIK), and Communication Services (NYSEARCA:CHIC). Relative to the benchmark CHIL, and their US counterparts, these sectors all outperformed. Such performance was mainly negative because of the ongoing COVID-19 crisis. But sectors in China fared better on average than in the US because of China’s progress in containing the outbreak and strong policy support to stabilize markets. While the Consumer Staples and Health Care sectors contributed most to MSCI China Index’s performance, Consumer Staples was the only sector that contributed positively to the Index’s monthly performance.

Greater demand for food, cleaning supplies and personal products led to outperformance in the Staples sector. Beijing also extended individual Income Tax (IIT) cuts implemented in 2019, designed to increase overall spending by individuals, while local governments distributed prepaid vouchers to encourage consumption. Consumers prioritizing basic goods purchases boosted the sector, as did economic activity, which picked up at the end of March when the lockdown began to ease.

Info Tech and Communication Services companies also performed well on a relative basis, as these sectors include firms providing the software behind video games, teleconferencing, and tele-education, as well as semiconductor firms and IT service providers – which helped keep people connected while they stayed at home.

Firms in the Health Care sector received praise from Beijing for their efforts on the frontlines combating COVID-19 and received support for aggressive R&D investments focused on containing and eliminating the outbreak. Health Care tech and biotech companies, as well as medical equipment and suppliers, were all encouraged by Chinese authorities to help respond to the outbreak of COVID-19.

Health Care Technology firms like Alibaba (NYSE:BABA) and Ping An (OTCPK:PIAIF), as well as medical software provider, Winning Health Technologies, stepped in to facilitate tele-medicine doctor visits and consultations during the outbreak and containment of COVID-19 in China, and are among China’s best performers YTD. Ping An’s Good Doctor telemedicine platform, for example, became so popular that the user base increased nine-fold from December 2019 to January 2020 alone.

These firms provided critical services, rapidly responding to provide necessary supplies and equipment, ramped up R&D investments, and helped solidify the emerging role technology is playing in China’s health care space with the online distribution of goods and telemedicine services.

China Sector Underperformers

As COVID-19 continued to spread across China in Q1, China’s Consumer Discretionary (NYSEARCA:CHIQ), Energy (NYSEARCA:CHIE), Real Estate (NYSEARCA:CHIR), Utilities (NYSEARCA:CHIU), Materials (NYSEARCA:CHIM), and Financials (NYSEARCA:CHIX) sectors, all underperformed the broader Chinese markets (NYSEARCA:CHIL).

The Energy sector was hit hardest over the last quarter, as overall demand fell because of reduced travel and manufacturing resulting from the COVID-19 outbreak, and a supply glut of oil and coal flooded the market. As a net importer of oil, lower prices could become a net positive for Chinese industry. However, in the near-term, China’s Energy sector – which is dominated by coal producers – will face headwinds related to an oversupply of coal and a gradual shift away from coal as a primary energy source.

In the Real Estate sector, developers were hit hardest, while operating companies performed well despite the economic headwinds, as projects stalled, and workers stayed at home. More than 100 real estate companies filed for bankruptcy in the first two months of the year due to a cash crunch as sales fell 36% from the same period last year.

Conclusion

COVID-19 and ongoing price wars between some of the world’s biggest oil producers may affect performance across China, but individual sectors are uniquely impacted. Macroeconomic drivers, policy stimulus, and economic integration can all affect sector divergence. As China becomes an increasingly critical economy for global markets, investors may increasingly consider sector investing in China that reflect nuanced and targeted approaches to invest in the world’s second largest economy.

1. Bloomberg, as of Mar 31, 2020.

2. Ibid.

3. Ibid.

Carefully consider the Fund’s investment objectives, risks, and charges and expenses before investing. This and other information can be found in the Fund’s summary or full prospectuses. Please read the prospectus carefully before investing.

Global X Management Company LLC serves as an advisor to Global X Funds. The Funds are distributed by SEI Investments Distribution Co. (SIDCO), which is not affiliated with Global X Management Company LLC or Mirae Asset Global Investments. Global X Funds are not sponsored, endorsed, issued, sold or promoted by MSCI, nor does MSCI make any representations regarding the advisability of investing in the Global X Funds. Neither SIDCO, Global X nor Mirae Asset Global Investments are affiliated with MSCI.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment