wildpixel

Volatility and change had been the watchwords of my life. – Chris Gardner

The VictoryShares US Large Cap High Div Volatility Wtd ETF (NASDAQ:CDL), a $400m sized fund, run by Victory Capital Management, tracks a portfolio of large-cap, dividend-paying U.S. stocks that exhibit low volatility. Here are a few reasons why this product may be pursued at this juncture.

Why CDL?

CDL does well to infuse fundamental parameters alongside risk control to select its high-yielding stocks, quite unlike a few exchange-traded fund (“ETF”) alternatives that tend to be quite myopic in incorporating only specific disciplines during stock selection. Often, while pursuing only a dividend-yielding portfolio, you run the risk of ending up with names that don’t generate meaningful earnings. CDL negates this risk as the stocks under consideration are required to have generated positive net earnings across the previous 12 months.

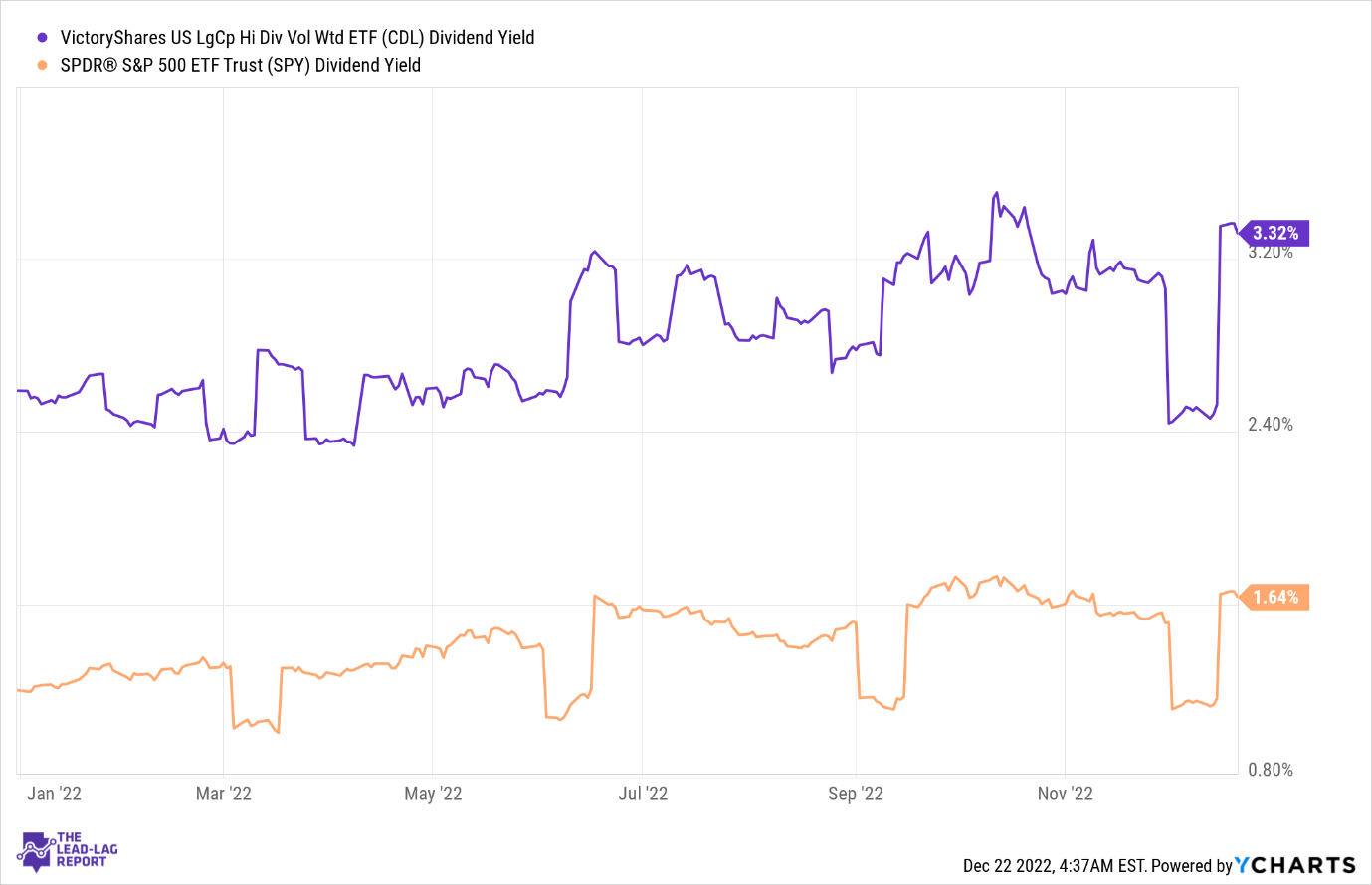

Speaking of yields, you’d be interested to know that this large-cap product currently offers a figure that is twice as good as what you get from the SPY. This superior differential could come in handy in the face of strong drawdowns.

YCharts

Ultimately, the final 100 stocks chosen are then weighted twice a year (in March and September) based on the standard deviation of daily price changes over the last 6 months; needless to say, stocks with a lower volatility quotient receive higher weights in CDL’s tracking index. I believe pursuing a portfolio of low-risk stocks could be particularly useful considering the environment we’re in.

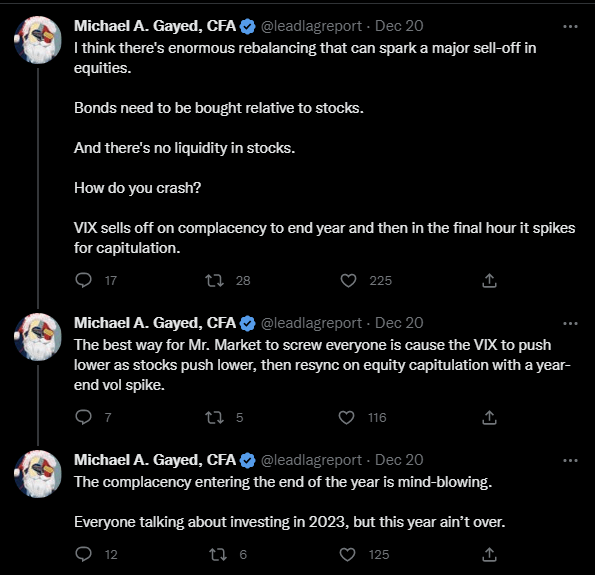

If you’ve been following some of my recent commentary on the timeline of The Lead-Lag Report Twitter account, you’d note that I’ve expressed some concerns about the relative complacency with which retail investors have been going about their business as we close the year. With the VIX sliding to the sub-20 levels, the retail cohort ostensibly believes that it’s safe enough to take off their seatbelts, but this false bravado could leave them with egg on their face when we potentially witness a volatility spike by the end of the year.

Twitter

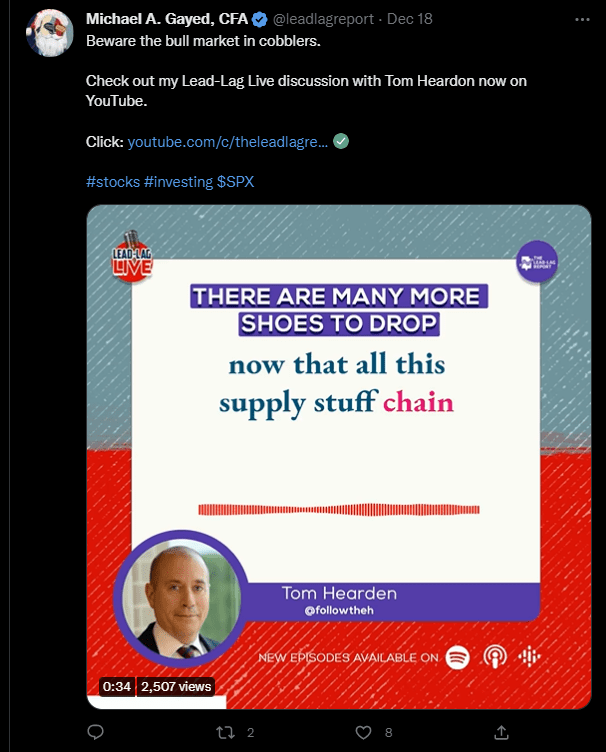

Tom Hearden, in a discussion on Lead-Lag Live, has noted the impact of tax-loss selling as we close the year, but he also thinks that next year a lot of equities are unlikely to get a free pass as valuation standards will be scrutinized with even greater discernment.

Twitter

For instance, a lot of companies have gotten away with using bloated adjusted EBITDA numbers, which have largely been propped up by dodgy non-cash variables such as stock-based compensation. In a recessionary environment, the market will have little time for names that rely heavily on this.

There’s also a lot of disparity around expectations around interest rates, which could trigger further volatility. The Fed wants to believe that it won’t hike rates until 2024, but the Fed futures market disagrees and is already pricing in quarter-point cuts in Q3 and Q4.

Adding to the uncertainty, you also have to consider some of the unwelcome developments from the land of the rising sun, where the yield curve control policy was loosened. There are suggestions that Japan may be less enthusiastic about buying U.S. treasuries, which could be a massive blow for that asset class that has only recently begun exhibiting its traditional risk-off qualities. All in all, this stop-gap nature of treasury movements is unwelcome and could likely only spur another bout of volatility in the financial markets.

Already this year, when the VIX rose by 25%, we’ve seen the S&P 500 Index (SP500) give up 17% of its market cap. Interestingly enough, CDL has been relatively flattish through all the turmoil. Investors who’ve followed my work over the years would recollect that I place a lot of importance on strategies or products that can help preserve capital in a down cycle, and CDL could be one of those names.

Also note that even though CDL has outperformed the benchmark index this year, the former can be picked up at a forward P/E of just 12.1x, which translates to a ~33% discount relative to the latter’s corresponding multiple.

Risks

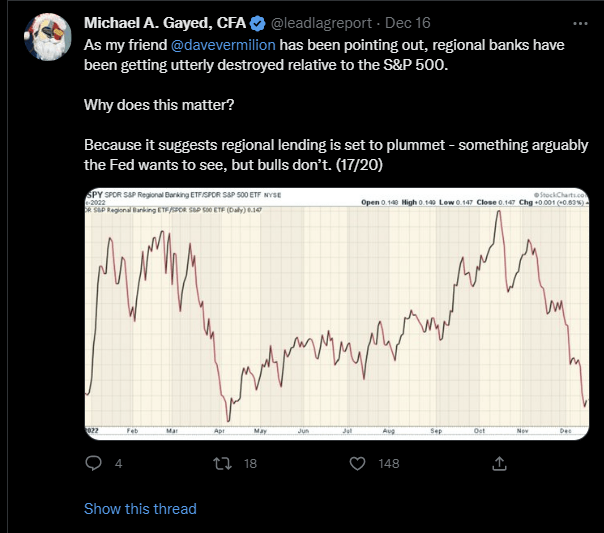

If there’s one aspect of CDL that isn’t ideal, it’s that the financial sector accounts for the largest share of the portfolio. As noted in the leaders-laggers section of The Lead-Lag Report, financials have been on something of a downtrend since late November, and I don’t believe this is just a short-term pivot.

Twitter

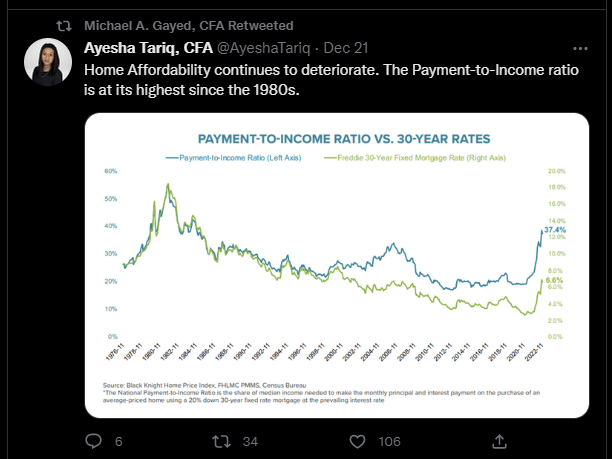

As noted in a tweet on the Lead-Lag Report timeline, loan growth trends don’t look too great in the face of a recession, and you also have to worry about potentially higher credit costs given the sizeable exposure of banks to the housing market. As noted by a Lead-Lag Live guest, Ayesha Tariq, payment-to-income ratios are currently hovering at uncomfortable levels. All in all, Fitch Ratings expects potentially higher loan loss provisions to weigh adversely on the earnings of these financial companies.

Twitter

Anticipate Crashes, Corrections, and Bear Markets

Anticipate Crashes, Corrections, and Bear Markets

Sometimes, you might not realize your biggest portfolio risks until it’s too late.

That’s why it’s important to pay attention to the right market data, analysis, and insights on a daily basis. Being a passive investor puts you at unnecessary risk. When you stay informed on key signals and indicators, you’ll take control of your financial future.

My award-winning market research gives you everything you need to know each day, so you can be ready to act when it matters most.

Click here to gain access and try the Lead-Lag Report FREE for 14 days.

Be the first to comment