bruev/iStock via Getty Images

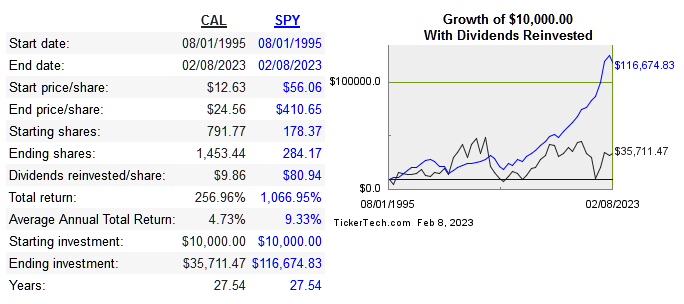

Caleres Inc. (NYSE:CAL) is the parent company of Famous Footwear and a portfolio of other clothing and apparel brands. It’s been publicly traded since 1981, and was originally founded in 1878. The total store count is 876 as of the last 10-Q. Below is the long term share price performance:

dividendchannel

The global footwear market is estimated to grow at 4% till 2030. This figure looks different if we break down the low end of the market versus the highly discretionary side of the shoe market. Lower priced shoes are a staple, but the rate of purchase can certainly slow during a recession. Next we’ll compare metrics with CAL’s peers:

|

Company |

Revenue 10-Year CAGR |

Median 10-year ROE |

Median 10-Year ROIC |

EPS 10-Year CAGR |

FCF 10-Year CAGR |

|

CAL |

1.3% |

10.3% |

6.5% |

20.3% |

22.3% |

|

14.6% |

13.8% |

11.1% |

28.7% |

n/a |

|

|

4.8% |

20.3% |

16.7% |

16.9% |

7.1% |

|

|

0.6% |

9.9% |

9.2% |

7.6% |

6.9% |

|

|

5.7% |

8.7% |

8.7% |

23.5% |

28.3% |

|

|

4.7% |

13.9% |

13% |

-1.3% |

-0.1% |

Capital Allocation

The company takes a mixed approach when it comes to allocating capital. Dividends have been paid since the late 80’s, but stays constant for years at a time, so definitely no dividend growth strategy being run here. Share count has slowly decreased over the past few years but I don’t think this will be a significant driver of EPS if the rate is kept as it has been.

They’ve made relatively few acquisitions along the way so I also wouldn’t expect this to be a significant driver of returns.

Risk

Fundamentally the company is below average in terms of returns on capital. They do however have fairly consistent free cash flow, and have never let debt get out of control. Keep in mind that CAL has never had an operating margin higher than 8%, and that margin is quite volatile itself. The company has been relatively flat over the past decade but it hasn’t wasted money since then.

The company is in good shape financially and can probably weather a recession mainly due to not using excess leverage. The biggest risk is paying what looks like a cheap price for a stock that could easily drop lower, which brings us to the valuation next.

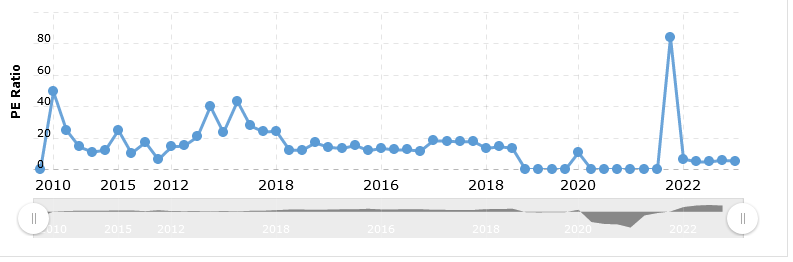

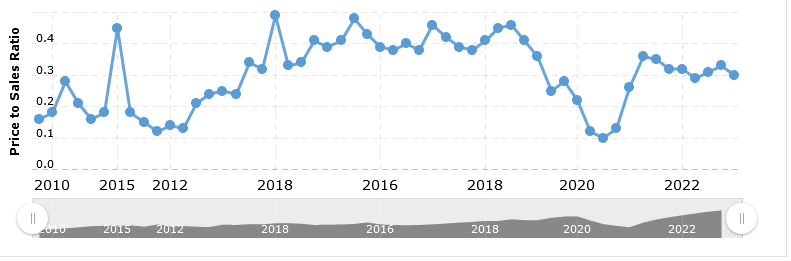

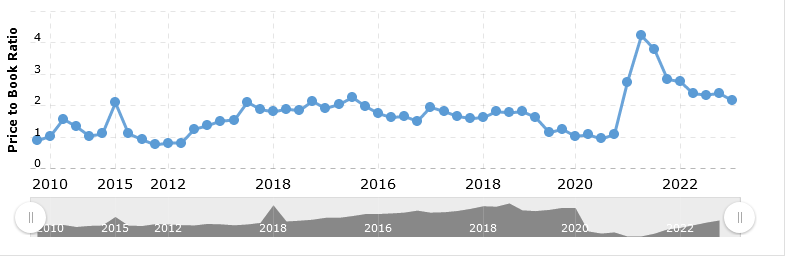

Valuation

First we will compare price multiples with peers, followed by historical multiples for CAL and my DCF model last:

|

Company |

EV/Sales |

EV/EBITDA |

EV/FCF |

P/B |

Div Yield |

|

CAL |

0.3 |

3 |

-36.7 |

2.2 |

1.1% |

|

SKX |

0.9 |

9.4 |

-15.6 |

1.9 |

n/a |

|

FL |

0.5 |

4.6 |

-28.5 |

1.3 |

3.4% |

|

GCO |

0.3 |

4.4 |

-3.1 |

1.1 |

n/a |

|

SCVL |

0.5 |

4.1 |

-24.4 |

1.5 |

1.2% |

|

DBI |

0.3 |

3.6 |

-131.9 |

1.5 |

1.8% |

macrotrends macrotrends macrotrends

Interestingly, the multiples are nearly identical for the industry at large. All have low multiples and negative free cash flow. If a recession is truly on the way, then the whole industry will suffer. I’m not predicting the likelihood of a coming recession or exactly how bad it will affect these companies, but I do think the discretionary nature of many shoe purchases offers us as investors a fair amount of risk for little upside potential in return.

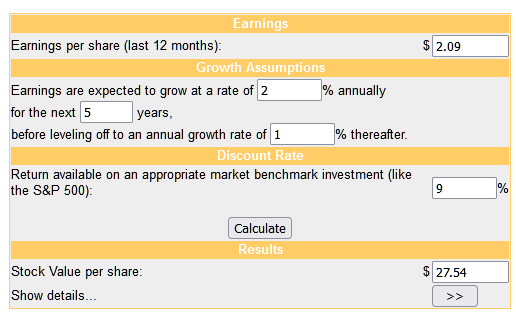

Next is the DCF model:

moneychimp

When an entire industry/sector/geographic region is cheap, I do think it’s worth sifting through to see if any higher quality companies have been caught in the broader downturn and unfairly punished price-wise. In this case I don’t see CAL separating itself from its peers. The stock is cheap for a reason. The company is mature, growth is flat, and a recession is expected by many in the industry. Even if no recession actually happens this year, the potential upside for this company is limited versus a fair amount of uncertainty in a very tough industry.

The current share price would make it undervalued on an intrinsic basis according to my model, but it doesn’t change the uncertainty of tougher economic times ahead. The company certainly isn’t overvalued, but this doesn’t mean a recession won’t drag prices lower. My rating for this stock is a hold.

Conclusion

This company and its peers will always be doing their best during the boom times. Even in those times, CAL does not generate above average returns on capital nor does their operating margin show much stability. This does make them a below average company, but it doesn’t mean they make a lot of bad decisions. The industry is tough already and the macro affects the general direction of the business.

The low multiples now are warranted, but this doesn’t mean they can’t go lower. This is why I will be avoiding Caleres stock. Even at a cheaper price it is still a mature, slow/no growth company that has to contend with mid single digit profit margins on average and limited industry growth.

Be the first to comment