Justin Sullivan

Thesis

During the trailing twelve months, Broadcom (NASDAQ:AVGO) has distributed about $15 billion to shareholders, as compared to a market capitalization of less than $240 billion. In general, Broadcom is looking like a ‘value’ opportunity, trading at cheap multiples. This is surprising, however, as an analyst could easily argue that Broadcom is also a ‘growth’ company, as during the past 5 years Broadcom expanded revenues by a CAGR of close to 19%. Personally, I value AVGO stock with a residual earnings model and calculate a fair implied share price of $692.65. AVGO is a ‘Buy’.

For reference, Broadcom’s stock has also performed well in recent years, with the share price increasing by about 117% over the past five years, as compared to again of slightly less than 40% for the S&P 500 (SPY). The company’s one year forward P/E ratio is also materially below the respective valuation of the industry median, which suggests that the stock is undervalued compared to its peers.

Seeking Alpha

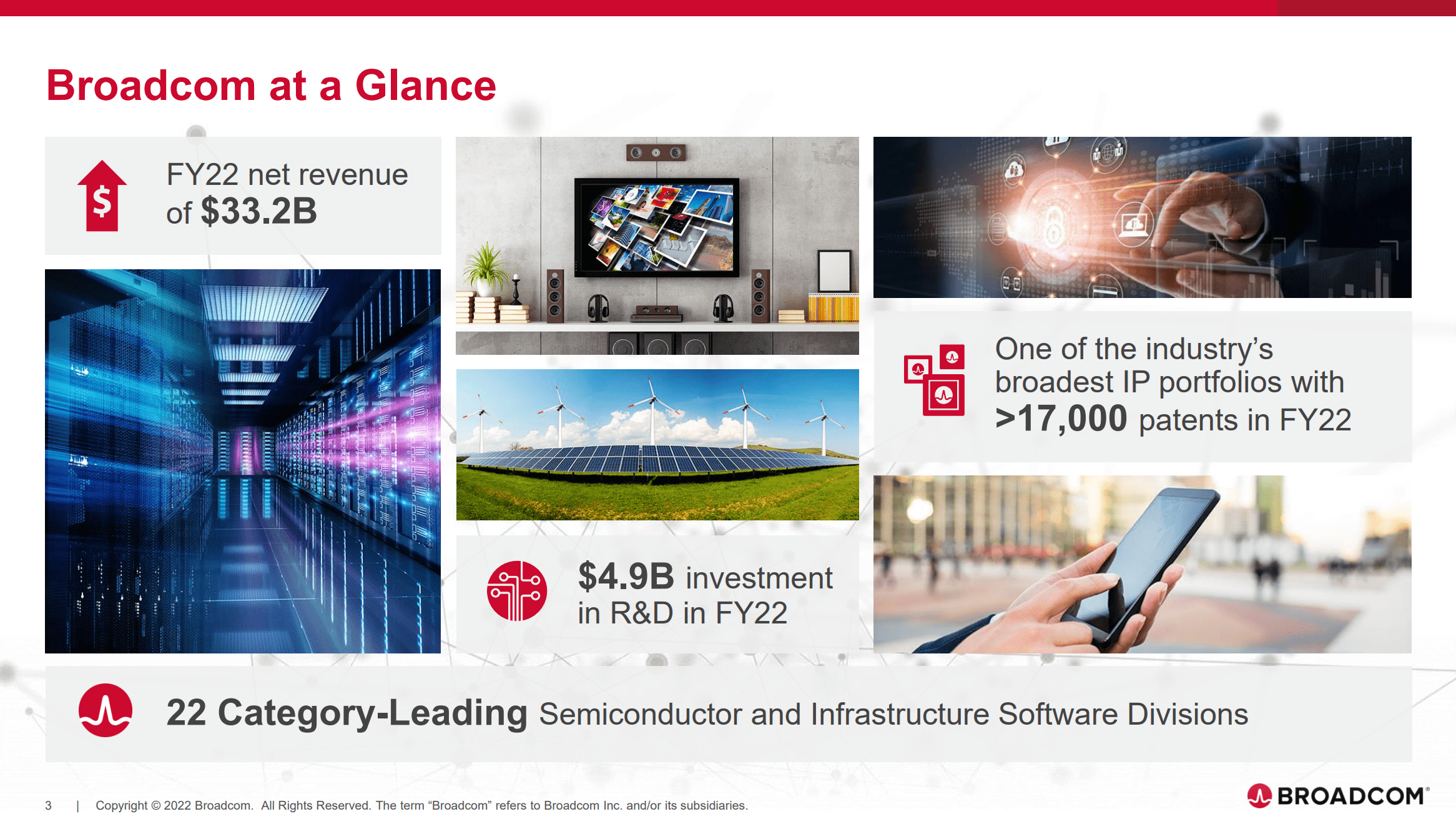

About Broadcom

Broadcom is a technology company that specializes in semiconductor and infrastructure software solutions. With that frame of reference, the company operates in three main segments: Semiconductor Solutions, Infrastructure Software, and IP Licensing. The Semiconductor Solutions segment provides a range of products that include solutions for analog and digital semiconductor devices. In addition, Broadcom also offers modules for various applications in context of data centers, networking, software defined infrastructure, as well as broadband and wireless communication. Broadcom’s Infrastructure Software segment provides solutions that help to manage and automate data center, enterprise, and service provider networks. The IP Licensing segment licenses intellectual property related to wireless and wired infrastructure and networking technologies.

Broadcom Investor Presentation

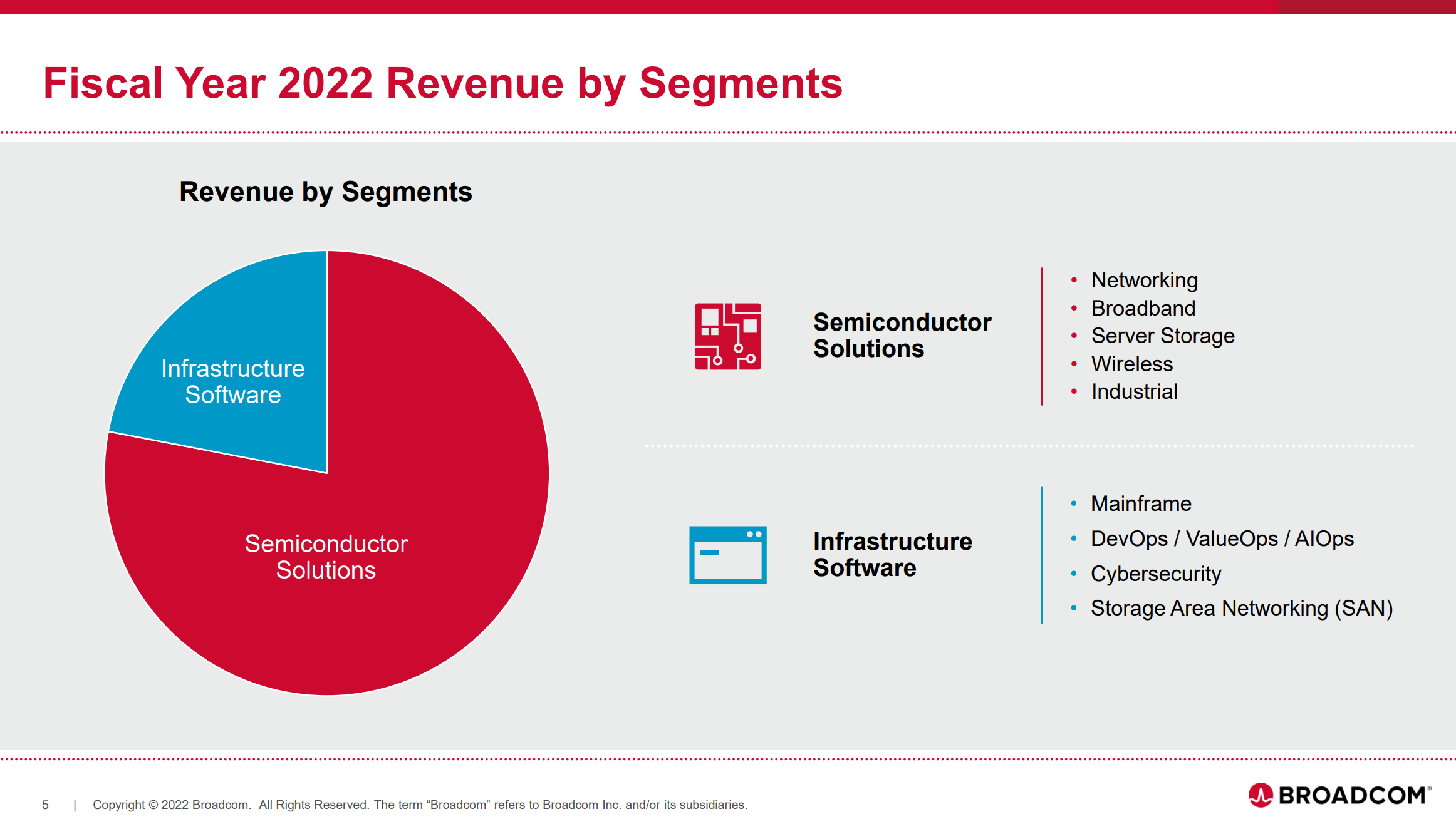

With reference to the introduction section about Broadcom’s product portfolio, it is important to note that semiconductor solutions account for more than three quarters of Broadcom’s total revenue exposure.

Broadcom Investor Presentation

Attractive Macro Tailwinds Support Business Fundamentals

A key argument for investing in Broadcom is anchored on the company’s attractive exposure to secular growth drivers: Broadcom’s fundamentals are levered to an increasing demand for data, which is further supported by the increasing adoption of the Internet of Things, 5G, and cloud computing. This is creating a need for more sophisticated and efficient semiconductor and infrastructure software solutions, which Broadcom is well positioned to provide. The company has a strong portfolio of products and a track record of innovation and development, which gives it a competitive advantage in the market.

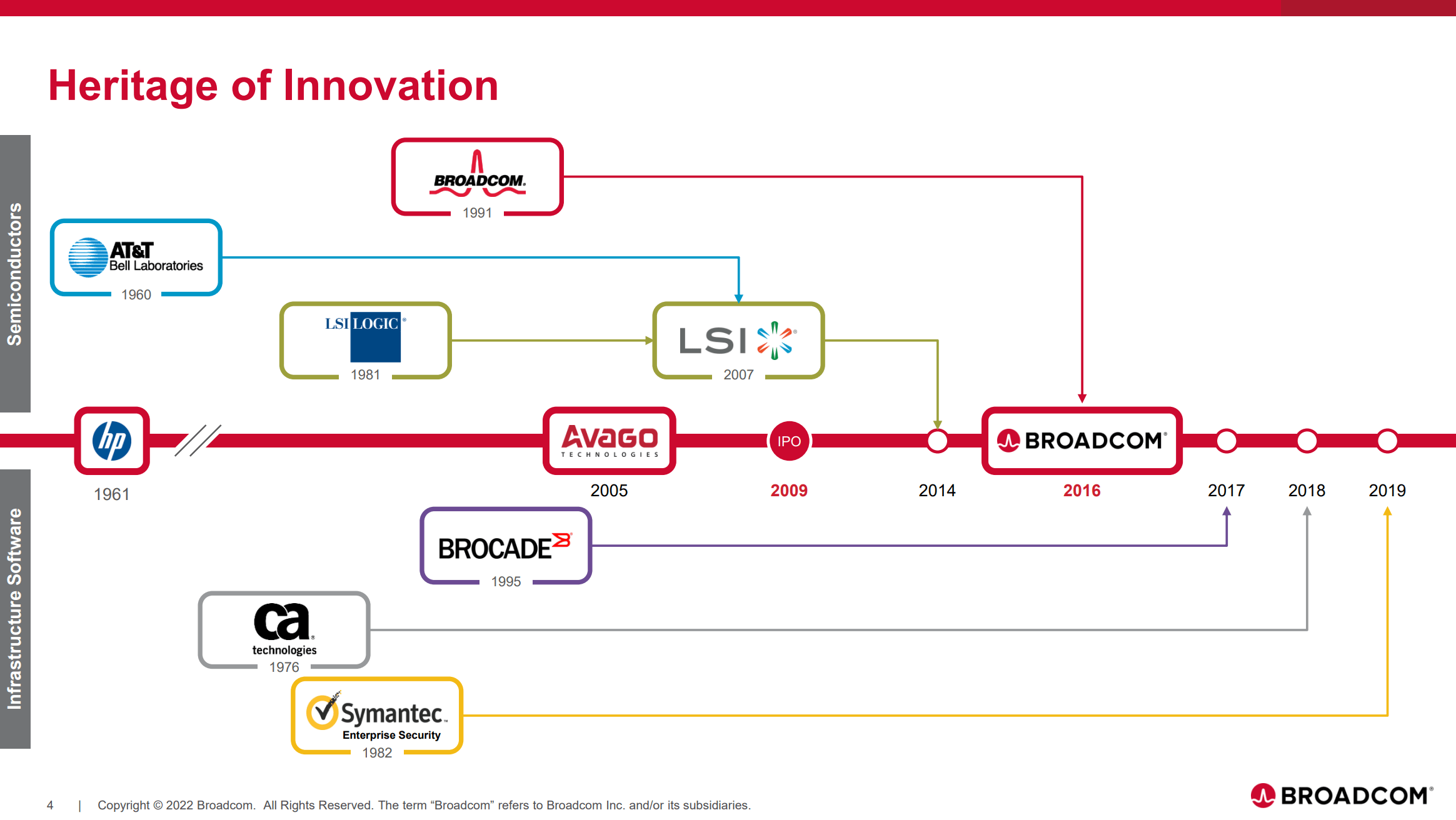

Another driver of Broadcom’s growth is the trend towards industry consolidation. With the increasing complexity of technology and the need for economies of scale, companies are looking to merge or acquire other companies to gain access to new markets, technologies, and customers. With that frame of reference, Broadcom has a history of making successful strategic acquisitions, as highlighted below:

Broadcom Investor Presentation

Likely closing in late 2023, Broadcom is also set to acquire VMware (VMW) for $61 billion. This strategic move is poised to strengthen Broadcom’s offerings of vital infrastructure solutions for cloud. With regards to financials, the acquisition is estimated to add an ~$8.5 billion of incremental EBITDA to Broadcom’s profitability.

It’s a Growth and Value Company

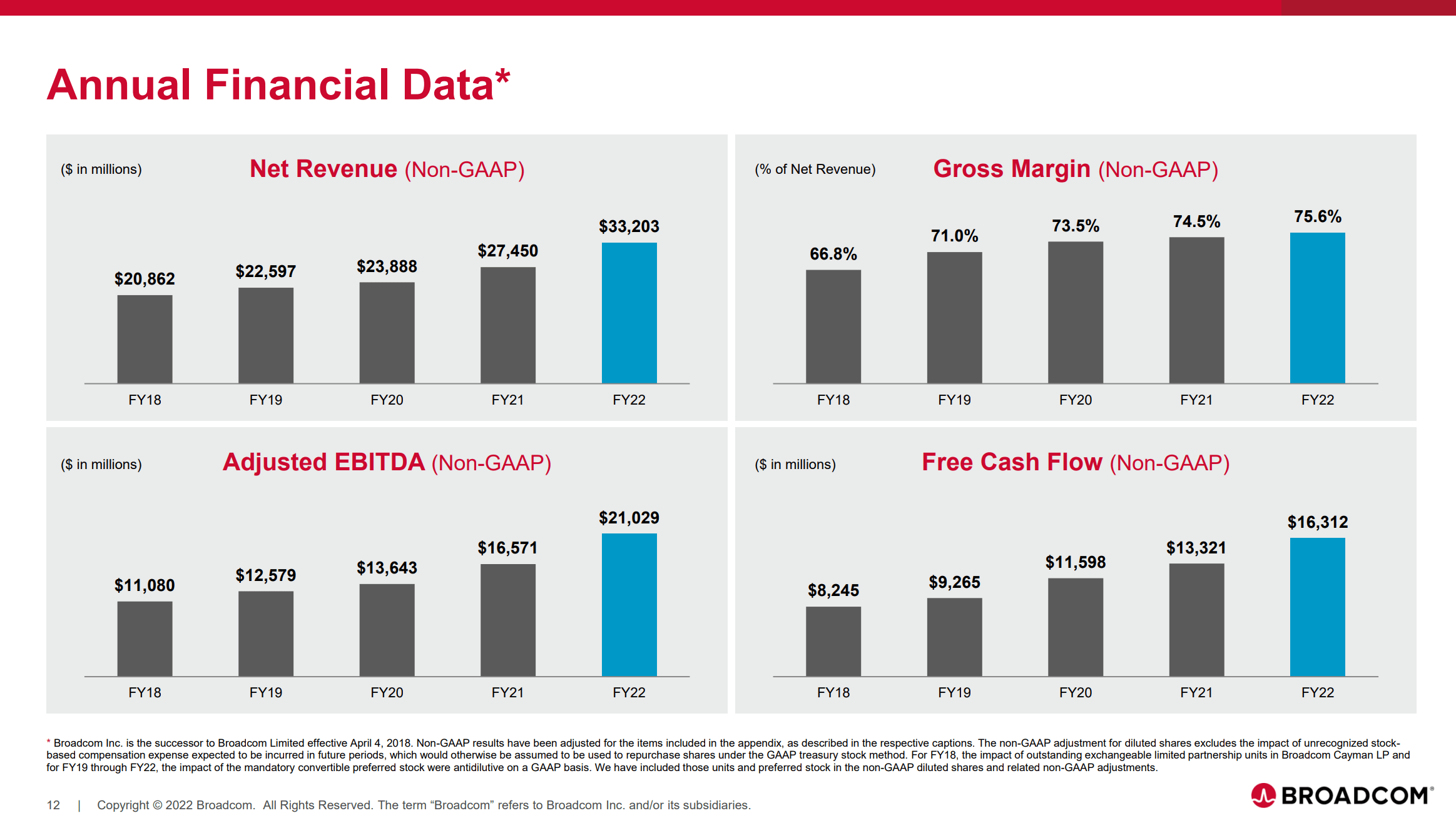

Reflecting on Broadcom’s secular growth tailwinds, it is no surprise that the company’s financial performance has been very strong in recent years, with steady revenue growth and value accumulation. In fact, during the past 5 years, Broadcom’s revenue expanded by a CAGR of close to 19%, jumping from $17.6 billion in FY 2017 to $33.2 billion in FY 2022. Over the same time period, Broadcom’s operating profits have more than tripled: expanding from $5.5 billion to $14.3 billion.

Broadcom Investor Presentation

With such strong growth it is surprising that Broadcom also offers a strong ‘value’ argument. With a P/E of about x14, AVGO is valued at an industry discount of almost 30%. Moreover, investors should consider that Broadcom is offering a TTM equity yield of almost 7%. During the past 4 quarters, the company has completed approximately $15.5 billion of shareholder distributions, $7 billion in form of dividends and $8.5 in form of share buybacks.

Residual Earnings Model

To estimate a company’s fair implied valuation, I am a great fan of applying the residual earnings model, which anchors on the idea that a valuation should equal a business’ discounted future earnings after a capital charge. As per the CFA Institute:

Conceptually, residual income is net income less a charge (deduction) for common shareholders’ opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company’s capital.

With regard to my AVGO stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal ’till 2025. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise.

- To estimate the capital charge, I anchor AVGO’s cost of equity at 10%.

- For the terminal growth rate after 2025, I apply 3.25%, which is approximately one percentage point above the US’s estimated long-term nominal GDP growth (conservative in my opinion).

Given these assumptions, I calculate a base-case target price for AVGO of about $692.65 a share, which implies that AVGO could be undervalued by as much as 21.5%.

Analyst Consensus EPS; Author’s Calculation

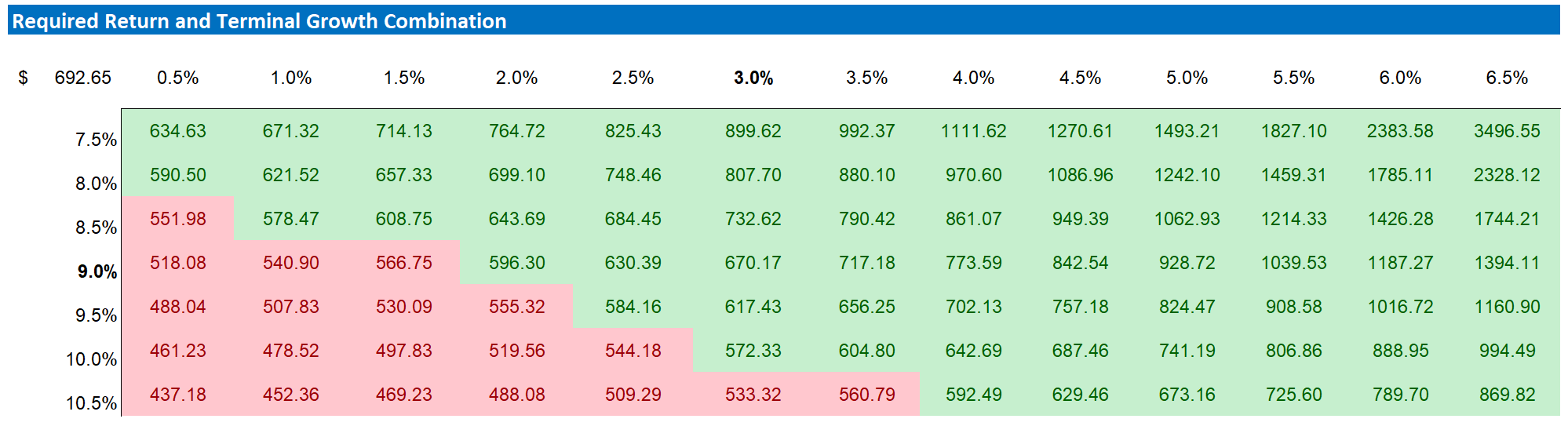

My base case target price does not calculate a lot of upside. But investors should also consider the risk-reward profile. To test various assumptions of AVGO’s cost of equity and terminal growth rate, I have constructed a sensitivity table.

Analyst Consensus EPS; Author’s Calculation

Conclusion

With a recent history of almost 20% of compounded annual revenue growth, paired with an equity yield of close to 7%, I view AVGO as a growth and value stock alike. And the company looks undervalued: Personally, I value AVGO stock with a residual earnings model and calculate a fair implied share price of $692.65. AVGO is a ‘Buy’.

Be the first to comment