Leks_Laputin/iStock via Getty Images

The Apple & AVGO Investment Thesis

As termed by Miguel de Cervantes in the novel, Don Quixote, “it is the part of a wise man to keep himself today for tomorrow, and not venture all his eggs in one basket.” This quote is critical to our discussion today, attributed to Apple’s role (AAPL) in Broadcom’s (NASDAQ:AVGO) topline thus far.

In particular, we reckon the generative AI hype may help to divert some of the AAPL-related headwinds away, though it is uncertain how AVGO aims to replace the lost revenues. This was because the Cupertino giant commanded 20% of the semiconductor company’s revenues in FY2022 and FY2021 at $6.64B and $5.49B, respectively, as declared by the company here.

It was due to this fact that AVGO stock was negatively impacted by -8.7% in the days after supposedly losing a key AAPL contract in December 13, 2019 and announcing its intentions to sell the RF unit in December 18, 2019. The same pessimism also occurred on January 9, 2023 when Bloomberg reported that the smartphone maker might replace AVGO’s Wi-Fi and Bluetooth chips from 2025 onwards.

However, it is unclear how AAPL intends to replace these chips, due to the reported difficulty in producing its own modem chips currently manufactured by Qualcomm (QCOM). Particularly, the former has expected a major switch only from 2024 onwards, despite acquiring Intel’s (INTC) modem business for $1B in FQ4’19.

It appears that manufacturing these chips are not as easy as it seems, especially since QCOM’s 5G modem offerings prove superior to its competitors. While Samsung (OTCPK:SSNNF)(OTCPK:SSNLF) also produces its own 5G chipsets, Exynos 2200, the South Korean company opts to use QCOM’s Snapdragon 8 Gen 2 in its flagship Galaxy S23 Ultra 5G, amongst others.

The reason is perhaps due to Snapdragon 8 Gen 2’s reported improvements in the Geekbench 6 multi-core benchmark by up to +39.6% and in the iGPU – FP32 Performance by +110.9%. Therefore, it is no wonder that SSNNF has made the switch for its 2023 releases, against 2022’s Galaxy S22 on Exynos 2200.

In the same vein, AVGO released the “World’s First Wi-Fi 7 Ecosystem Solutions” in April 12, 2022. Analyst Ming-Chi Kuo from TF International Securities had speculated that AAPL might potentially adopt the former’s Wi-Fi 6E chipset in iPhone 15 by late 2023. Over the next few years, the analyst also posited that the Cupertino giant might eventually adopt AVGO’s Wi-Fi 7, due to the shift in AAPL’s focus to 3nm processors through 2025.

The same had been highlighted by Hock Tan, CEO of AVGO, in the recent FQ1’23 earnings call:

Our relationship, our strategic engagement continues very much the same as it has for the last multiple years and we see that to continue in a fairly predictable stable manner. (Seeking Alpha)

Either way, AAPL seemed determined to design its own chips moving forward, with its A- and M-series processors already replacing INTC’s SoC since 2017 and 2020, respectively. We reckon these factors may naturally keep AVGO on its toes over the next few years.

Perhaps this was why AVGO had chosen to diversify its conventional hardware/ infrastructure software offerings by acquiring VMware (NYSE:VMW) for $61B in cash and stock, since the latter specialized in complex enterprise software solutions.

While we remain uncertain about the hefty price tag at this time of economic downturn, there may be excellent synergy in software integrations and operating efficiencies moving forward, attributed to Hock Tan’s multiple M&A successes thus far.

Particularly, once the merger is completed, AVGO’s software offerings will be tucked under VMW’s cloud-native architecture, allowing massive opportunities for collaborations between their hardware and software offerings. We reckon these may serve as tailwinds for further innovation, cementing the company’s offerings as one of the best-in-class semiconductor suppliers.

This diversification is highly strategic as well, due to the immense impact of PC demand destruction on INTC’s top/ bottom lines and stock prices thus far. The company had to break its streak of eight consecutive years of dividend growth, largely in part due to the drastic -20.2% YoY impact on the top line and -59.6% YoY on the bottom line in FY2022. This was unsurprising, since PCs (Client Computing) comprised an overwhelming 51.5% of the company’s revenues in FY2021, prior to the PC headwinds.

The same had been discussed in our previous Nvidia (NASDAQ:NVDA) article here, attributed to the company’s sustained innovation in the data centers, AI, IoT, gaming, and automotive industries, amongst others. In our opinion, these efforts justified its premium valuations, while expanding its strategic leadership in multiple end markets while mitigating future demand destructions.

Therefore, we remain highly confident in AVGO’s progress, while being particularly interested in Hock Tan’s future plans for VMW once the merger is completed by the end of 2023, assuming that all regulatory approvals are obtained.

Beyond VMW, we reckon the company may actively seek new opportunities to support its top and bottom line growth as well, in preparation of AAPL’s likely eventual departure. Particularly, the ChatGPT hype may support the stock’s upward rally, due to the notable $800M (+300% YoY) top-line contribution in FY2023, attributed to the “exponential demand from its hyperscale customers.”

In the long-term, the market growth for global generative AI is massive as well, with Brainy Insights projecting a market expansion from $8.65B in 2022 to $188.62B by 2032, at an accelerated CAGR of 36.1%. This suggests AVGO’s excellent tailwinds for innovation and growth through the next decade, as highlighted by Hock Tan, CEO of AVGO:

We are seeing a very strong and a strong sense of urgency among our customers especially in the hyperscale environment to be – to not miss out – not to be late in this trend… We are in early innings and which is why we think we have time to come up — to start to work on even a new generation of switches in Ethernet that are — specifically designed dedicated to these kind of workloads, which are very different from the normal workloads that we see today traditionally in data centers and we have to address that. Don’t forget generative AI is still early stage. (Seeking Alpha)

Nonetheless, we must also advise investors to proceed with caution here, since the $800M sum is minimal compared to AVGO’s FY2022 revenues of $33.2B and FQ2’23 guidance of $8.7B. Combined with the fully booked lead time of 50-weeks, the immediate contribution from generative AI may not be significant enough to support the current market optimism.

So, Is AVGO Stock A Buy, Sell, or Hold?

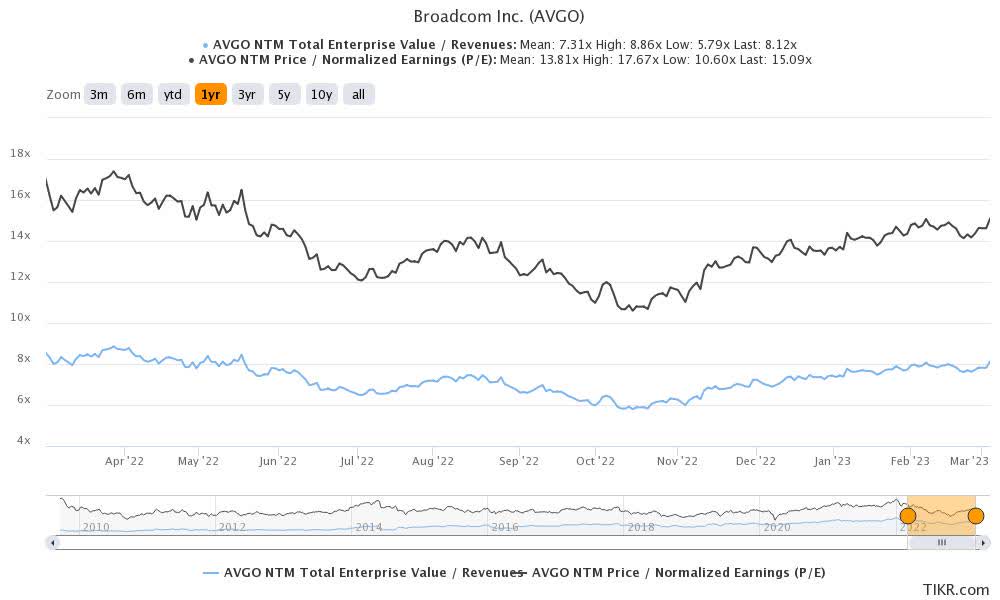

AVGO 1Y EV/Revenue and P/E Valuations

S&P Capital IQ

AVGO is currently trading at an EV/NTM Revenue of 8.12x and NTM P/E of 15.09x, higher than its 3Y pre-pandemic mean of 5.72x and 13.06x, respectively. Otherwise, it is still higher than its 1Y mean of 7.31x and 13.81x, respectively.

Based on its projected FY2024 EPS of $44.27 and current P/E valuations, we are looking at a moderate price target of $668.03, suggesting minimal upside potential from current levels.

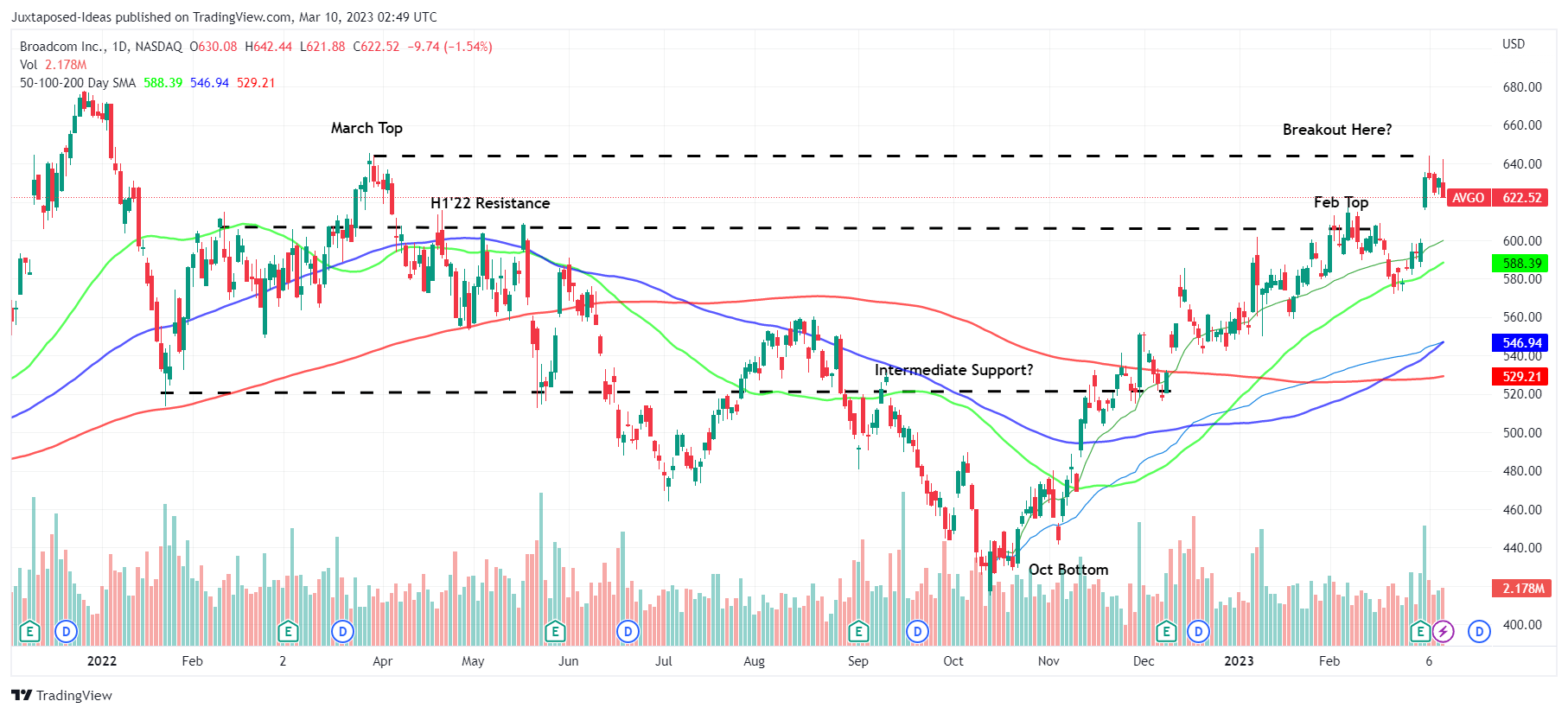

AVGO 1Y Stock Price

Trading View

This lack of potential upside is unsurprising, due to the tremendous surge AVGO has enjoyed by +45.7% from its October bottom to $622.52 at the time of writing. The stock had also broken through its previous resistance levels to test another top, implying more volatility in the short term.

Combined with the rising peak and trough movements over the past few months, we reckon it may be more prudent to rate AVGO as a Hold here. Chasing the stock at these levels may not be sustainable for long-term portfolio growth, especially driven by the recent AI hype.

Keen investors may have to be patient and wait for another retracement to the mid $500s at its previous support levels, for an improved margin of safety to our price target.

Be the first to comment