JuSun

It’s hard to go too wrong when buying value, especially when it comes to cash rich businesses that have economic moats. In these cases, it’s a good reminder for the Mohnish Pabrai saying that goes: “heads you win, tails you don’t lose too much”.

This brings me to Bristol-Myers Squibb (NYSE:BMY). It’s been a while since I last visited the stock in October of 2021, and the stock has produced a market beating total return of 33%, far surpassing the 15% decline of the S&P 500 (SPY) over the same timeframe.

BMY remains fairly inexpensive at the current price of $73 with a low forward PE, especially after the recent drop from the $80+ level. In this article, I highlight why BMY is a good value at present for potentially strong total returns, so let’s get started.

Why BMY?

Bristol Myers Squibb is a well-renowned large-cap pharmaceutical company, with $47 billion in annual sales. Over the years, it’s pivoted its business towards higher-margin specialty drugs, and was transformed by its acquisitions of Celgene in 2019 and MyoCardia in 2020. This pushed BMY further into the specialty pharma segment, with namely first-in-class cardiovascular, oncology and immunology drugs.

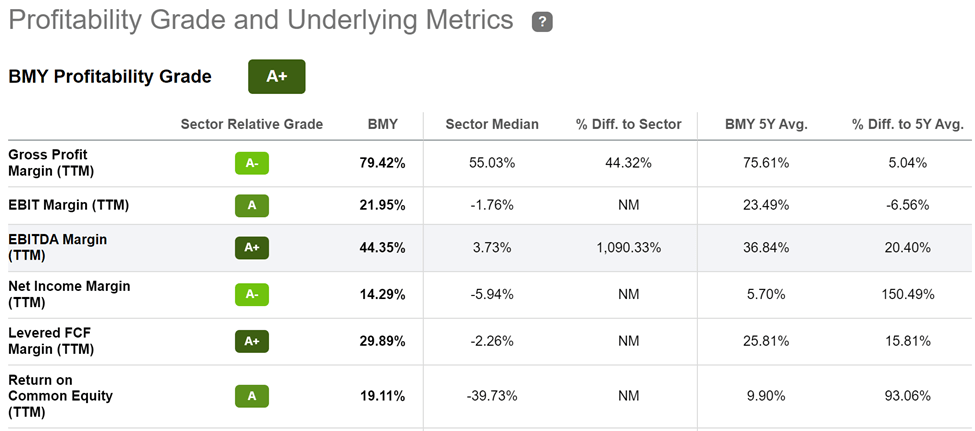

As one would expect from a moat-worthy pharmaceutical company, BMY is a cash-rich business with high margins due to its robust R&D platform, built-up knowledge base, and a number of drugs on patent protection. This is reflected by BMY’s A+ profitability grade.

As shown below, BMY has impressive EBITDA and Net Income margins of 44% and 14%, respectively over the trailing twelve months, sitting far above the median for the overall pharma industry.

BMY Profitability Grade (Seeking Alpha)

This is not to say that BMY is without risks, however, as total revenue declined by 3.4% YoY during the third quarter, due to FX headwinds as a result of a strong US dollar and generic competition for Revlimid, which is BMY’s multiple myeloma drug. This was, however, partially offset by strong growth in BMY’s in-line and new product portfolio, which saw 13% YoY growth on a constant currency basis.

Looking forward, BMY should be able to replace lost sales from Revlimid with growth in new drugs and its pipeline. This includes the launching of 9 new medicines over the past year, including the approval of 3 first-in-class drugs that management expects to see over $4 billion in annual sales. Management highlighted the efficacy and potential from these 3 new medicines during the last conference call:

We delivered 3 key new products this year: Opdualag, Camzyos and Sotyktu. Each is a first-in-class asset, and these products have the potential to contribute meaningfully to our growth.

Opdualag marks the second approved I-O combination that we delivered. Its strong launch continued during the quarter, furthering our leadership in delivering innovative cancer treatments to patients well into the next decade.

We’re also encouraged with the progress we have made towards building our foundation for Camzyos as a specialty cardiovascular medicine. We are seeing increasing numbers of patients initiating therapy, and their feedback has been very positive. David will provide more details on the launch in a moment.

Sotyktu has been approved with a label that reflects its profile, and as an oral of choice medicine for moderate-to-severe plaque psoriasis. We are very encouraged by the early days of this launch and see significant benefit to these patients with this important new option.

Meanwhile, BMY is well-positioned from a balance sheet standpoint to continue its strong track record of innovative drug development. This is reflected by its strong A+ credit rating from S&P. It also has a high cash and short-term investments balance of $9.0 billion and carries a very safe net debt to EBITDA ratio of 1.5x.

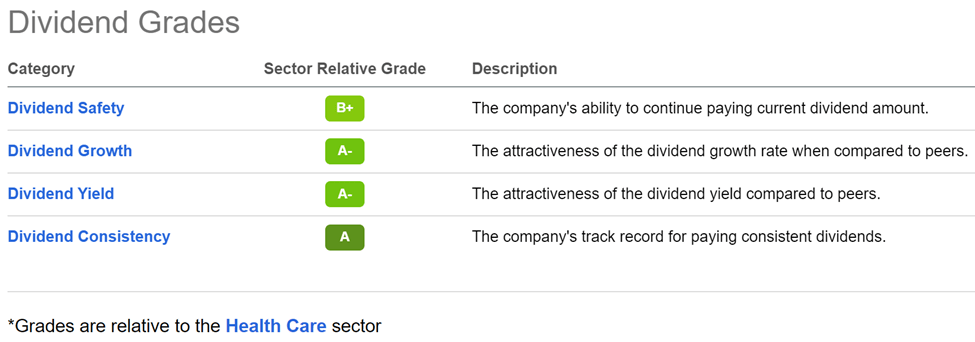

Importantly, while BMY’s dividend yield of 3.1% isn’t particularly high, it is nearly double that of the S&P 500’s current 1.6% yield and comes with a very safe 28% payout ratio. Management recently raised the dividend by 5.6%, and it comes with A and B grades for safety, growth, yield, and consistency, as shown below.

BMY Dividend Grades (Seeking Alpha)

Lastly, BMY remains attractive at the current price of $73 with a forward PE of just 9.6x. Analysts have a rather conservative price target of $80 which could still mean a double-digit total return. The low PE also implies that BMY can get a respectable 10.4% earnings yield on share repurchases alone.

Management highlighted its commitment to debt reduction and opportunistic share reductions through its accelerated share repurchase program during the last conference call:

We remain committed to continued debt reduction. In the quarter, we repaid $2.8 billion of debt, and we remain committed to returning capital to shareholders. We executed a $5 billion ASR earlier this year, and have $9.5 billion remaining in our share via authorization, and we will continue to be opportunistic on share repurchases.

Investor Takeaway

Overall, Bristol-Myers Squibb remains an attractive option for investors looking to capture its high margin business at a low valuation. It has a number of promising new drugs that could drive meaningful growth. It also has a strong balance sheet with low leverage and ample cash on hand to fund development and opportunistic share repurchases. Considering all the above, I find BMY to be a Buy for potentially strong long-term returns.

Be the first to comment