jetcityimage

Thesis

BP p.l.c. (NYSE:BP) reported a robust Q2, increased its distribution, and a further stock repurchase to the delight of investors as it benefited from robust oil and gas prices.

We also highlighted in our July update that BP was likely at a bottom and could stage a short-term rally. Therefore, we aren’t surprised that much of its near-term upside was captured pre-earnings, as the market correctly anticipated a solid Q2.

However, BP had pulled back from its post-earnings uplift and could also form a potential bull trap (indicating the market denied further buying upside decisively). While not validated yet, we urge caution as ongoing selling pressure in Brent crude could impact BP’s performance moving forward. We also believe Henry Hub natural gas prices could have peaked, potentially impinging on its forward operating results.

Therefore, we urge investors to be patient and not chase the rally. Accordingly, we reiterate our Hold rating on BP.

Solid Q2 Delighted BP’s Investors

BP reported an incredible Q2 that saw a record replacement-cost profit of $8.45B, up 202% YoY, well above the consensus estimates of $6.8B. Furthermore, it also reported an operating cash flow of $10.86B, up 100.8% YoY, as it benefited tremendously from record oil and gas prices.

The company also raised its distribution by 10% and announced another $3.5B stock repurchase program. Notably, the company’s confidence is predicated on its ability to drive performance with a $40 per barrel cash balance point. CEO Bernard Looney accentuated (edited):

We want to maintain a strong balance point. We want to anchor on that $40. That means that this quarter, given the fact that the company is running well, and the outlook for the environment, we are able to raise the dividend by 10%, and do so while maintaining a $40 oil price breakeven. The first call in our financial framework is our dividend. And we talk about it being a resilient dividend, which means that we want to protect that dividend given our experience of having to cut it just 2 years ago. So we’re very focused on making sure that our investors and our owners can rely on that dividend. And therefore, we believe that it remains prudent to maintain a $40 breakeven price in light of the fact that prices are much, much higher today. (BP FQ2’22 earnings call)

But Watch Out What’s Next After A Record Quarter

BP revenue change % and adjusted EBIT margins % consensus estimates (S&P Cap IQ)

The consensus estimates (bullish) indicate that Q2 could be BP’s peak revenue growth before falling dramatically through FY23. Notwithstanding, BP’s robust operating model should continue to undergird its profitability. Therefore, we are not concerned about near-term risks impacting its capital allocation policies.

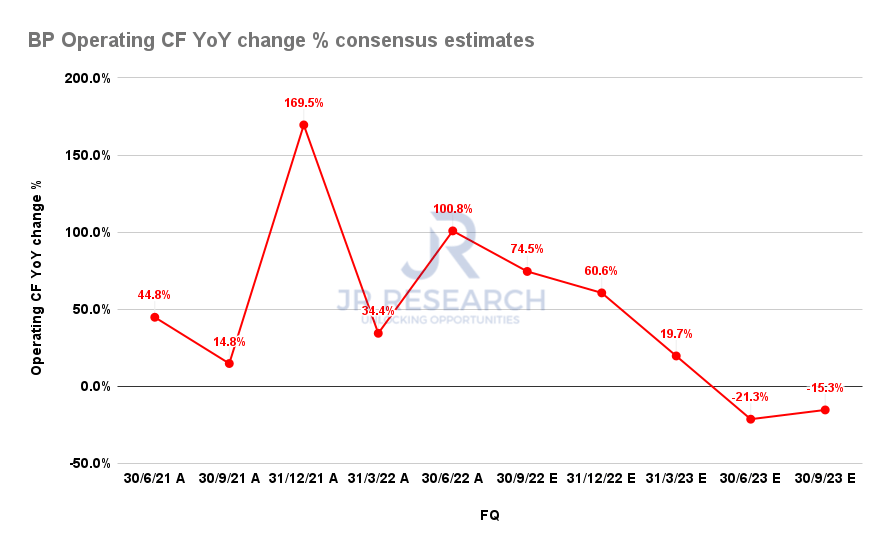

BP operating cash flow change % consensus estimates (S&P Cap IQ)

Furthermore, BP’s operating cash flow growth is projected to moderate further. While we don’t expect it to impact its dividend policy, we believe the Street is modeling for a marked fall in oil and gas prices moving ahead.

We noted that Brent crude and Henry Hub natural gas futures are in backwardation, with Aug 2026 prices well below the pricing of the current contracts, particularly for natural gas. We also discussed in a recent EQT Corporation (EQT) article, positing that natural gas prices have likely topped out. BP also cautioned in its filings (edited)

Decreases in oil, gas or product prices could have an adverse effect on revenue, margins, profitability, and cash flows. If these reductions are significant or for a prolonged period, we may have to write down assets and reassess the viability of certain projects, which may impact future cash flows, profit, capital expenditure, and the ability to work within our financial framework and maintain our long-term investment program. (BP 10-K)

Is BP Stock A Buy, Sell, Or Hold?

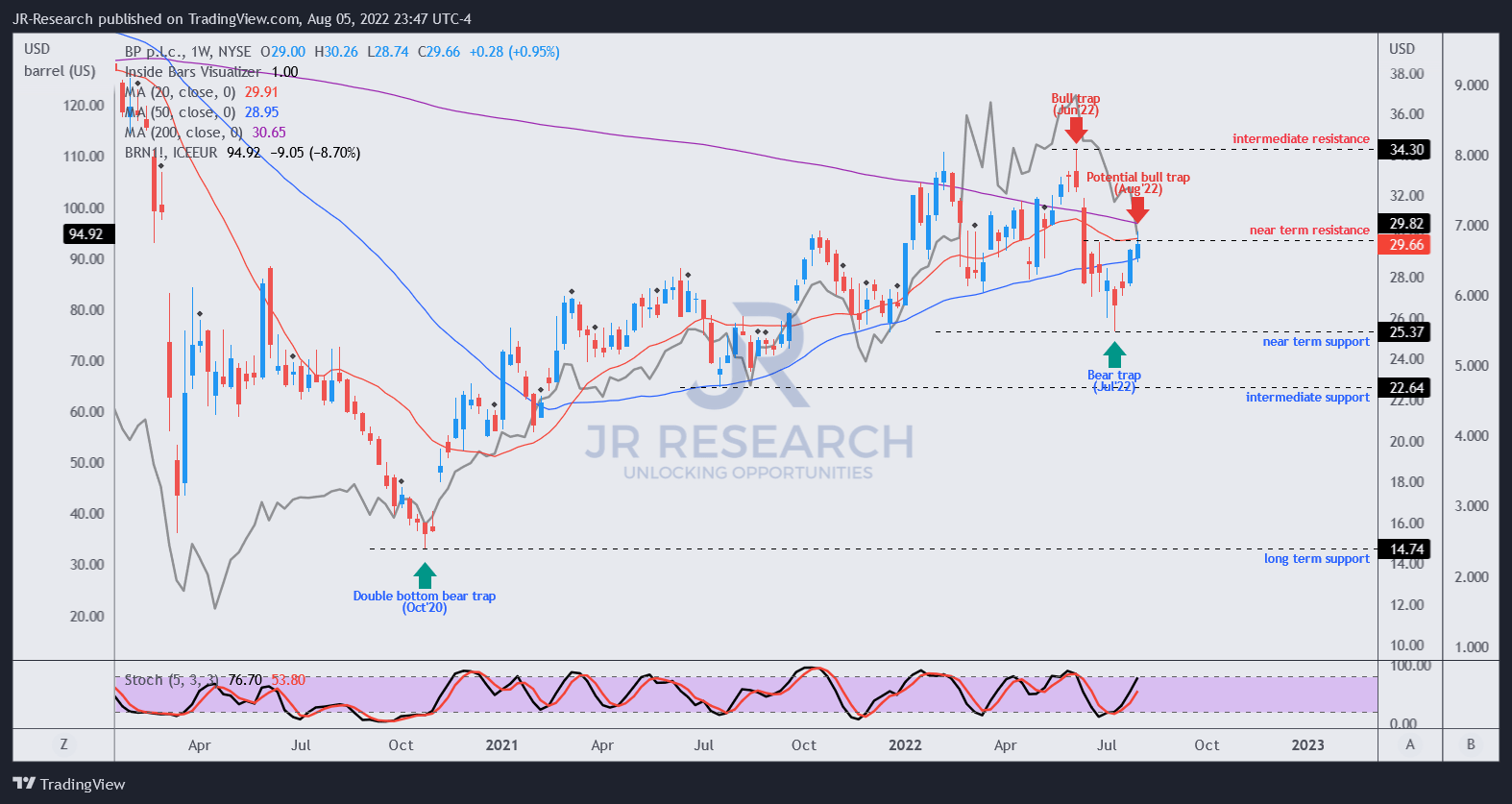

BP price chart (weekly) (TradingView)

Our price action analysis suggests that the near-term upside from its Q2 performance is likely reflected, given the run-up in July. It has also outperformed the Brent crude (gray line overlay), as the market anticipated a robust Q2 release.

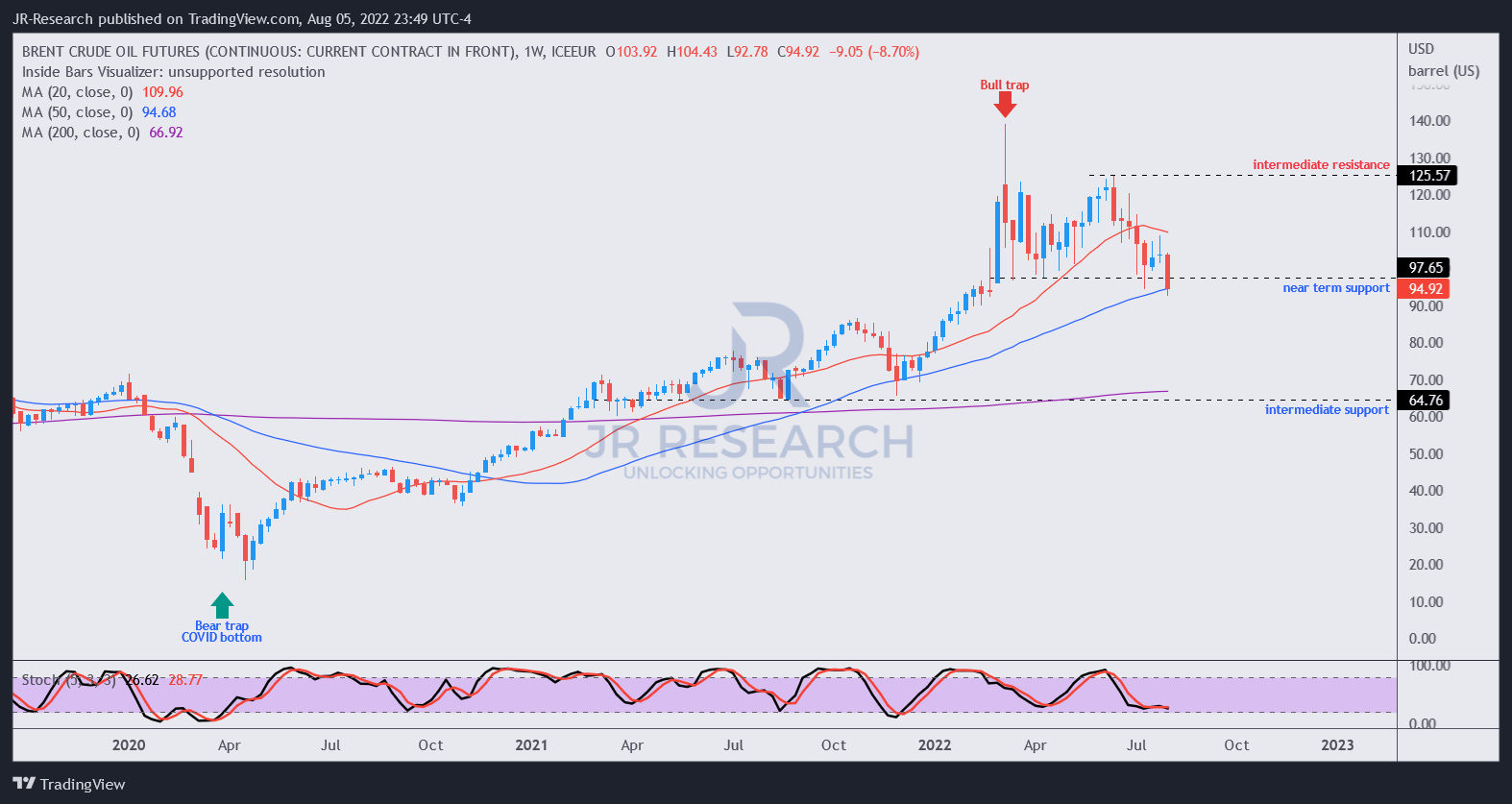

Brent crude price chart (weekly) (TradingView)

Brent crude is also at a critical juncture, as it’s testing its near-term support. It nearly gave up all its post-war gains as the market renewed its focus on recessionary themes and demand destruction. Citi (C) also cautioned in a recent commentary, as it emphasized (edited):

It means the market is no longer expecting tightness ahead, it’s expecting things to loosen up. It’s supply purely playing against demand. More supply and less demand for oil typically mean prices would fall. This is something that needs to concern companies while it is something very pleasant for consumers. – Insider

However, Brent crude could still stage a bear trap (indicating the market rejected further selling downside resolutely) over the next couple of weeks. Therefore, a short-term rally could follow if a bear trap is validated.

However, we continue to urge caution for investors considering chasing the current rally in BP, given its price action and valuation (discussed in our previous article).

As such, we reiterate our Hold rating on BP.

Be the first to comment