imaginima/E+ via Getty Images

Boston Properties (NYSE: NYSE:BXP) is a developer and owner of Class-A office properties in the USA. The company concentrates on six markets: San Francisco, Los Angeles, New York, Seattle, Boston, and Washington, DC. It is structured as a Real Estate Investment Trust (REIT) that manages, acquires, and develops office properties in its chosen areas. The company’s portfolio includes 196 properties and over 50 million square feet of real estate.

ycharts.com

In this article, I will show that even though the company’s value may rise in the next 12- 18 months, as a long-term position, Boston Properties is not the best option in its sector, and this stock receives a neutral position in my book.

Office Real Estate Market

Since the beginning of the COVID 19 pandemic, demand for office space has been down considerably. Over the past few months, governments have lifted restrictions, and businesses have begun to allow their employees to get back to work.

Even though restrictions have been lifted, there is still uncertainty about what the future holds for office REITs’. Unlike home and apartment REITs, the developments that Boston Properties hold are not a necessity for society to function. People need homes to live in, not offices to do work in. This leaves uncertainty about the future and makes a usually stable market have a higher short-term beta than expected.

One of the advantages of office REITs is that they usually have long-term lease agreements which provide stable cash flow. However, purchasing or developing these large properties is becoming increasingly expensive. With supply chain issues looming, projects typically go overtime and over budget and reduce profit and cash flow. This lowers the company’s return on investment and decreases profitability.

I feel that the value of the properties that Boston Properties holds will underperform compared to the rest of the market. The core cities that the company holds are not in strategic locations, and the American mass migration from California, New York, and other cold, traditionally democratic states to states like Texas, Georgia, and Florida, which have much better tax rates and business opportunities. Real estate prices are determined by two primary factors: supply vs demand and location. As demand decreases, especially for office properties in highly taxed areas, revenue could decrease for Boston Properties and force rents down, thus, decreasing the earnings. Boston Properties needs expansion into untapped south-eastern markets to grow shareholder value.

Boston Properties CEO Owen Thomas fought back against similar claims telling CNBC in early March:

“Companies are saying, ‘Look, we don’t want to work from home. We want to have our people in a physical office, and so we’re going to go to the cost and the expense of leasing something in the suburbs on a short-term basis so we can put them all together”

Whether he is right or not remains to be seen. But there is no doubt that the company is on the defensive at the moment.

Solid Financials

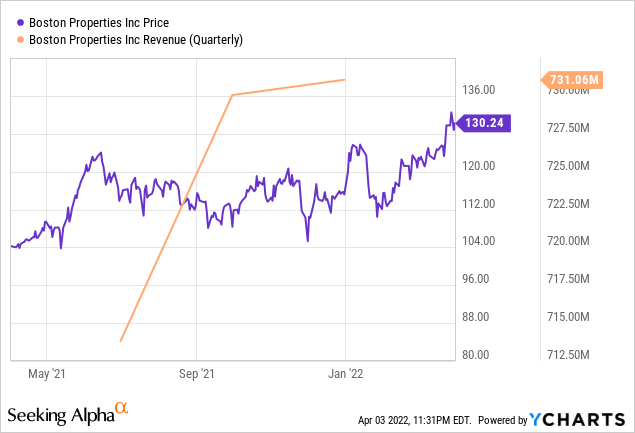

Boston Properties held a P/FFO of 18.65 in 2021 and a forecast P/FFO of 16.56 in 2021. This is roughly in line with what is expected in the industry, with the overall sector forward P/FFO being 16.47. While this does not detract from Boston Properties as an investment, it certainly does not paint a picture of a company with tremendous value to be found at current prices. They are forecast for 3.04 billion dollars in revenue in 2022 (4.50% growth) with an average EPS of 0.67. These metrics show that stable growth is expected; however, the long-term revenue outlook is foggy as the company is trying to transition the type of real estate that it buys from pure office real estate to media centers and life science buildings.

ycharts.com

As stated in my thesis, I do not despise the outlook of the company. BXP’s dividend pays $3.92 per share (about 3.10%) per year, much lower than the average REIT available on the market. Many REITs’ can pay a healthy 4-6 percent dividend yearly, with some rising to the 8-10 percent mark. Investors won’t have to look far to get a better overall return in the short and long term.

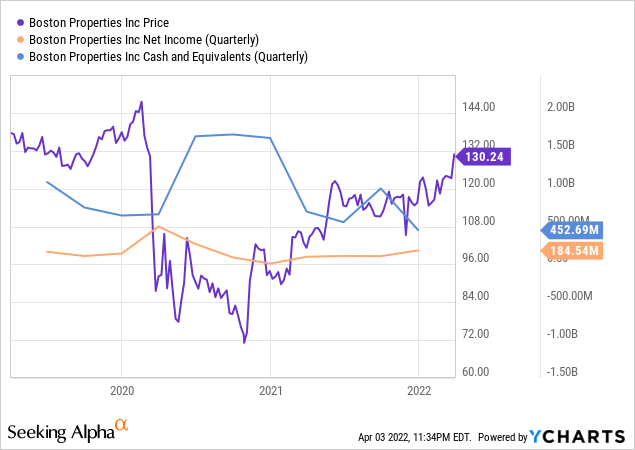

BXP’s earnings actually declined in 2021, even though many other sectors and companies inside the real estate sector saw massive growth. The company’s 2021 profit was 505 million dollars, considerably lower than 850 million in 2020 and lower than pre-pandemic levels in 2018 and 2019, which were 582 and 521 million, respectively. This is a huge red flag when investing in a REIT; this may show that they are investing in areas and property types that are quickly losing demand. The instability of the company’s earnings, as well as the fact that any REIT must pay out 90% of its taxable income, could be worrying for some investors if there is a market downturn because the company may not have enough cash on hand to deal with headwinds effectively. There are many companies in the real estate sector with better cash flow, better dividends, and a better market, making BXP undesirable at current prices.

ycharts.com

BXP’s total debt to total assets ratio is 59.67, a very high number even for a REIT. This puts pressure on their business to find clients to rent their offices long-term because they do not have much equity in their properties. Also, REITs with less equity cannot maneuver as well in times of financial crisis and are more prone to default. The company’s cash and short-term investments are down over 70% in 2021; there will be no significant investments in the near future to take the BXP to the next level. While this metric is not critical, it can give insight into the company’s short-term direction and possible pitfalls. The best companies to invest in have plenty of cash flow not just for emergencies but also to take advantage of opportunities that may arise in their markets.

Risks

When any company changes direction, it carries an element of risk and takes lots of cash to execute. Specifically, mistakes are expensive in the real estate market because once development plans are made, and the first concrete is poured, the job must continue until completion. Even the purchase of already built buildings can be risky as demographics change and other corporations change how they do business. In many ways, Boston Properties is at the mercy of other businesses and what they want to do with their employees. Personally, I would prefer an investment in companies that proactively get business rather than reactively try and create it.

Future Growth and Takeaways

Boston Properties is a solid company, it trades at a P/FFO in line with its competitors, and stable growth is expected in the short term. However, in the long term, BXP may face issues with finding customers, increasing revenue, and managing debt. Year over year, the company’s revenue has decreased and is not recommended as a good long-term hold with better options available on the market. In order to succeed, Boston Properties will have to begin investing in southern regions of the US – states like Florida and Texas, where people and ultimately jobs are flooding in greater numbers every year. Investment in those areas will be critical for solid margins and good cash flow in the future. This cash flow could be used to increase and maximize their dividend and provide further shareholder value. This shareholder value is critical as more investors flock to apartment and condo REITs over business entity and office real estate REITs.

Be the first to comment