Central Bank Watch Overview:

- Market pricing for the BOC and RBA has been dragged forward in recent weeks, with both central banks now expected to raise rates in the first half of 2022.

- Meanwhile,the outlook for the RBNZ is extremely aggressive, with rates markets expecting nearly five 25-bps hikes before mid-2022.

- Retail trader positioning suggests that the near-term outlook is bearish for the trio of major commodity currencies.

Markets Expecting Policy Shifts

In this edition of Central Bank Watch, we’re examining the rates markets around the Bank of Canada, Reserve Bank of Australia, and Reserve Bank of New Zealand.

The RBNZ is expected to be the most aggressive of the bunch, with the fastest hiking cycle of the post-Global Financial Crisis currently priced in by rates markets – incidentally, an environment that may prove difficult for the New Zealand Dollar.

Elsewhere, the RBA is contending with the market breaking its yield curve control (YCC) policy even as Australian economic data has disappointed. Meanwhile, disappointing Canadian economic data hasn’t deterred markets from pulling forward BOC rate hike odds.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

Bank of Canada is Done with QE

The BOC zeroed out its QE program at its October meeting, much to the surprise of markets which were only anticipating a halving of asset purchases. In turn, with the BOC warning on inflation pressures, traders have pulled forward rate hike odds from 2Q’22 to 1Q’22. There is still room for BOC rate hike odds to rise further, though that may need to wait until Canadian economic data reverses its recent trend of disappointment: the Canada Citi Economic Surprise Index has dropped from +58.6 on October 25 to +22.3 today.

Bank of Canada Interest Rate Expectations (November 11, 2021) (Table 1)

Ahead of the BOC meeting, rate hike markets were pricing in a 101% chance of a 25-bps rate hike by April 2022 (100% chance for a 25-bps rate hike; 1% chance for a 50-bps rate hike). Now, with inflation pressures continuing to ratchet higher across developed economies – for which Canada is not immune – rates markets are expecting March 2022 for the first rate hike (100% chance for a 25-bps rate hike, 31% chance for a 50-bps rate hike).

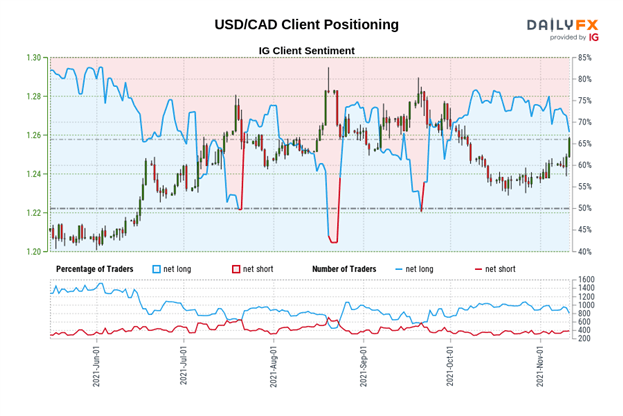

IG Client Sentiment Index: USD/CAD Rate Forecast (November 11, 2021) (Chart 1)

USD/CAD: Retail trader data shows 64.87% of traders are net-long with the ratio of traders long to short at 1.85 to 1. The number of traders net-long is 18.78% lower than yesterday and 21.73% lower from last week, while the number of traders net-short is 3.92% higher than yesterday and 15.36% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests USD/CAD prices may continue to fall.

Yet traders are less net-long than yesterday and compared with last week. Recent changes in sentiment warn that the current USD/CAD price trend may soon reverse higher despite the fact traders remain net-long.

Reserve Bank of Australia’s Quandary

The RBA is continuing its asset purchase program at a run-rate at A$4 billion per week through February 2022, but after allowing Australian government bond yields to shoot higher at the end of October, the central bank decided to abandon is 0.10% target for the AGB due April 2024. The RBA’s patience may prove warranted, as the Australian economy isn’t rebounding as quickly as anticipated as the country emerges from lockdowns: Australia lost -46.3K jobs in October and the unemployment rate jumped from 4.6% to 5.2%.

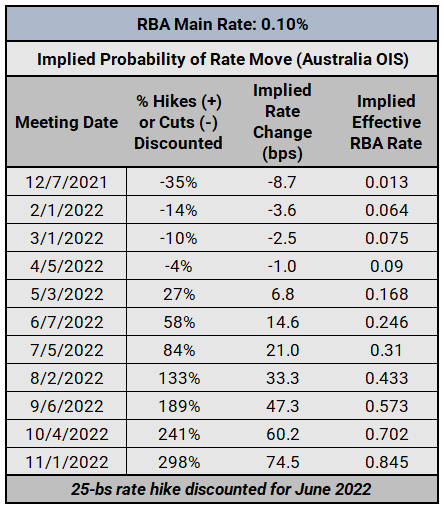

RESERVE BANK OF AUSTRALIA INTEREST RATE EXPECTATIONS (November 11, 2021) (TABLE 2)

After the RBA’s QE program ends in February 2022, rates markets are expecting the central bank to act quickly thereafter to start raising rates (regardless of where inflation rates may be). In the short-term, rate cuts odds have deepened – in mid-October, there was a 29% chance of a 25-bps cut by December 2021, now there is a 35% chance – but markets are now expecting the first RBA rate hike to arrive in June 2022 (58% probability).

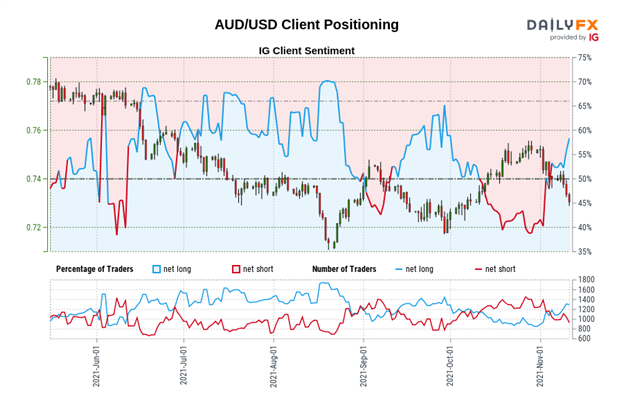

IG Client Sentiment Index: AUD/USD Rate Forecast (NOVEMBER 11, 2021) (Chart 2)

AUD/USD: Retail trader data shows 60.58% of traders are net-long with the ratio of traders long to short at 1.54 to 1. The number of traders net-long is 16.19% higher than yesterday and 24.98% higher from last week, while the number of traders net-short is 16.32% lower than yesterday and 20.85% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests AUD/USD prices may continue to fall.

Traders are further net-long than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger AUD/USD-bearish contrarian trading bias.

RBNZ Looks Aggressive

In the wake of the October RBNZ meeting, when the main rate was increased by 25-bps to 0.50%, rates markets continue to suggest a more aggressive RBNZ on the horizon. But this may constitute an issue for the New Zealand Dollar, insofar as the market is already expecting many more rate hikes over the coming months; the impact is priced-in, meaning the New Zealand Dollar won’t necessarily benefit when the rate hikes arise. Conversely, if the RBNZ doesn’t adhere to the aggressive pricing timeline, then the Kiwi could suffer.

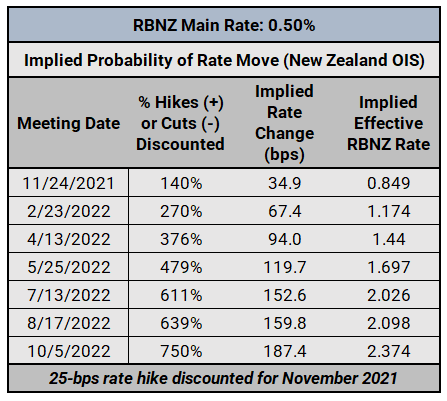

RESERVE BANK OF NEW ZEALAND INTEREST RATE EXPECTATIONS (NOVEMBER 11, 2021) (Table 3)

After the October RBNZ meeting, New Zealand overnight index swaps were pricing in a 91% chance of another 25-bps rate hike before the end of the year. Rate hike odds have jumped in recent weeks, and there is now a 140% chance of a hike at the last meeting of the year in a few weeks (100% chance of a 25-bps rate hike; 40% chance of a 50-bps rate hike). With five 25-bps rate hikes priced-in through mid-2022, this would be the most aggressive rate hike cycle by any major central bank in the post-Global Financial Crisis era.

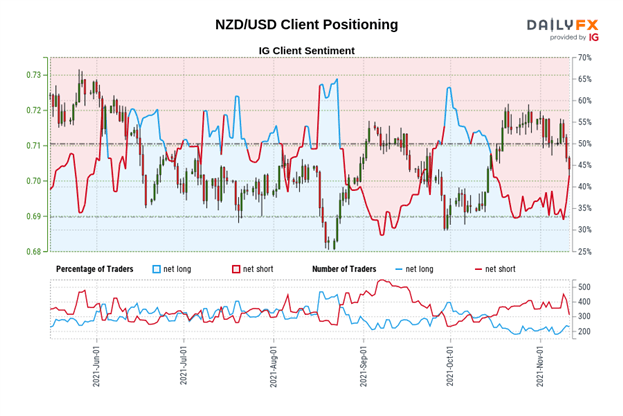

IG Client Sentiment Index: NZD/USD Rate Forecast (NOVEMBER 11, 2021) (Chart 3)

NZD/USD: Retail trader data shows 43.05% of traders are net-long with the ratio of traders short to long at 1.32 to 1. The number of traders net-long is 14.54% higher than yesterday and 25.00% higher from last week, while the number of traders net-short is 0.29% lower than yesterday and 12.24% lower from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests NZD/USD prices may continue to rise.

Yet traders are less net-short than yesterday and compared with last week. Recent changes in sentiment warn that the current NZD/USD price trend may soon reverse lower despite the fact traders remain net-short.

— Written by Christopher Vecchio, CFA, Senior Strategist

Be the first to comment