Nattakorn Maneerat/iStock via Getty Images

After the bell on Thursday, we received fiscal first quarter results from BlackBerry (NYSE:BB). The software and services firm has been under pressure recently as the market has fled many tech names, especially those with little growth and no profitability. Unfortunately for investors, the company’s latest results were mostly a repeat of the same old song, yet another period where we wait for a brighter future.

As usual, the headline results looked tremendous. Q1 revenues of $168 million came in more than $8 million ahead of the street, but there are two major asterisks here. First, BlackBerry reported licensing revenues of $4 million, whereas the street expected almost nothing as guidance for this segment called for near zero revenues here during this fiscal year. The second thing to remember is that management’s extremely weak guidance at the March report caused estimates to plummet. It’s not too hard to jump over the expectations bar when you guide so low that analysts basically put the bar on the ground.

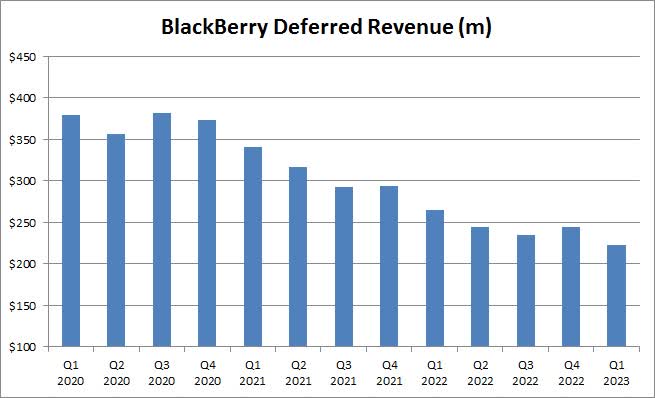

Going into that Q4 report nearly three months ago, the street was looking for more than $187 million in fiscal Q1, so this top line beat was mainly driven by the average sales estimate falling by nearly $30 million. This was the lowest revenue number reported by BlackBerry since John Chen took over more than 8.5 years ago. The near term won’t be helped by the fact that the deferred revenue balance continues its long term downward trend, as seen below. The portion of these revenues expected to be recognized in the next 12 months now stands at $190 million, down $18 million over the past year and $59 million over the past two years.

BlackBerry Deferred Revenue (Company Earnings Reports)

On the bottom line, the company’s adjusted loss was a nickel per share. Like the revenue side, this number beat due to reduced estimates that were calling for a 4 cent loss going into the previous quarter’s report. BlackBerry’s true GAAP loss was much worse, as the company continues to adjust away numerous expenses that other firms out there consider ordinary business. Investors will also be disappointed that Cybersecurity gross margins dipped by 4 percentage points over the prior year period, despite higher revenue, and IoT margins were only flat.

Perhaps the most concerning part of the report was that some key metrics continue to weaken. While competitors like CrowdStrike (CRWD) continue to show massive growth in annual recurring revenues (“ARR”), BlackBerry’s total ARR is actually shrinking. Cybersecurity ARR dipped another $13 million in the period and is down $30 million from Q1 2022, while IoT ARR is only up $8 million in the past 12 months. The Cybersecurity Dollar-Based Net Retention Rate declined another 3 percentage points to 88% in Q1, and stood at 94% in the year ago period. Perhaps the only good news was that the QNX royalty backlog has risen from $490 million to $560 million in the past year, but this revenue will take years to fully recognize. On the flip side, the percentage growth in the number of vehicles reportedly using QNX dipped when compared to previous years.

For the quarter, BlackBerry burned through $43 million in cash, ending the period with a net cash balance of $356 million. That balance will drop when the company pays off its $165 million litigation segment. There will be a cash inflow if the currently agreed to patent deal goes through, although a majority of that expected initial payment would be needed to pay off the company’s debt that matures in late 2023. The notes can be converted to stock, but shares currently trade a bit below the $6 conversion level, so no conversion would happen at this price.

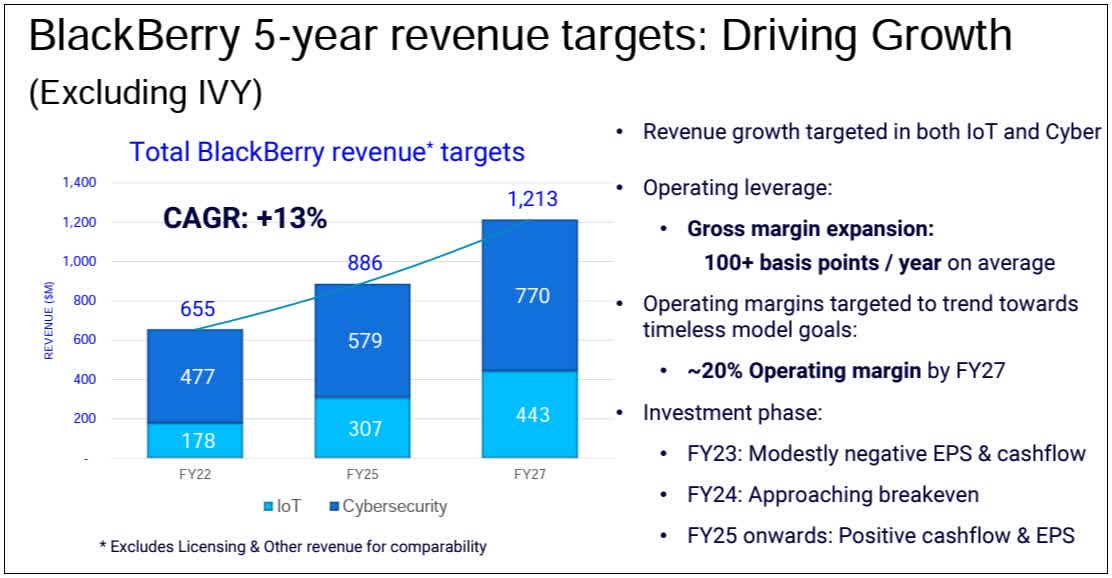

The main criticism I’ve had over the years is that this management team loves to talk about growth in one or two segments, or for the future, but at the expense of total sales. The graphic below shows the company’s five-year plan, where it is hoping to be back over $1.2 billion in revenues, excluding Ivy, by fiscal 2027. While that looks like great growth from where we are now, it basically means a flat decade for total company sales. Let’s not forget that when John Chen took over nearly a decade ago, this company was doing that much in revenue every quarter. He was looking to grow sales from there, but eventually had to give up on the hardware business a few years after he was supposed to fix it, which wasted precious time and resources.

BlackBerry Future Targets (Company IR site)

Given what we’ve seen in recent years, it is not a guarantee that these revenue targets will eventually be hit, as management has continually lowered expectations year after year. In the past year alone, for example, the average street revenue estimate for the current 2023 fiscal year has gone from more than $954 million to less than $690 million. A basic reiteration of guidance on the conference call likely won’t provide any meaningful upside to estimates anytime soon.

As for BlackBerry shares, they closed Thursday at $5.37, but were down a couple of percent in after-hours trading. Going into the report, the average price target on the street was $7, but that number was down more than a dollar over the past year. I don’t see too many reasons for analysts to change their numbers in a big way on this report, but there might be some targets trimmed a little due to overall market weakness and multiple contraction in this sector thanks to rate hikes and quantitative tightening.

In the end, it was another uninspiring quarter from BlackBerry. The company announced its lowest revenue figure under John Chen, only beating estimates that were significantly reduced. While the company keeps talking about this bright future, we’ve been hearing that from this management team for a decade now, and key internals have not shown any improvement. Since John Chen took over, the stock is down 15% while the NASDAQ is up about 177%, as the ultimate scorecard here continues to look quite bad.

Be the first to comment