piranka/E+ via Getty Images

In this modern era, big data is big business. But there has come to be so much data that many companies may struggle to find out what is useful and what isn’t. One company dedicated to helping customers collect and better understand their data is BigBear.ai (NYSE:BBAI). Recent financial performance at the company’s top line has been rather positive. Long term, this trend looks set to continue. But the firm’s bottom line is mixed and largely unattractive. That makes it difficult to value the enterprise and increases the risk of owning the stock to some extent. At the end of the day, while growth is impressive, it’s not enough to more than offset the negatives, leading me to rate the company a ‘hold’ prospect at this time.

A niche player in big data

According to the management team at BigBear.ai, the company focuses on using artificial intelligence and machine learning to help customers, mostly governments, to make better decisions. Its various products and services are provided through a modular, cloud-based platform that helps customers to address three phases of data-driven decision making.

The first of these is data curation. The company collects, normalizes, and integrates historical and real-time data from various sources, including its own proprietary data collections, customer proprietary data, and third-party data, in an attempt to create more accurate insights for clients.

This data is then distilled in order to identify information that would be considered relevant that involves a customer’s operating environment. Examples of data collected include tracking data, geopolitical events, public sentiment, stock market price changes, and more.

The next category the company focuses on is analysis. This is delivered on its platform and involves the interpretation of curated data. Using storytelling techniques, the company then works to make predictive analytics more accessible and actionable for the relevant decision-makers they are working with.

During this phase, the company relies tremendously on artificial intelligence and machine learning, as well as mathematical models like tensor completion, ultimately leading the firm to enrich and mine data in a way that becomes incredibly valuable to customers. The last component of this is guidance. On this part, the company provides goal-oriented advice that allows customers to make their own desired outcomes and to then determine what actions would be best in response to those preferences.

On top of all of these activities, the company also provides consulting services to design, customize, deploy, operate, and support their own solutions for both federal and commercial customers.

Author – SEC EDGAR Data

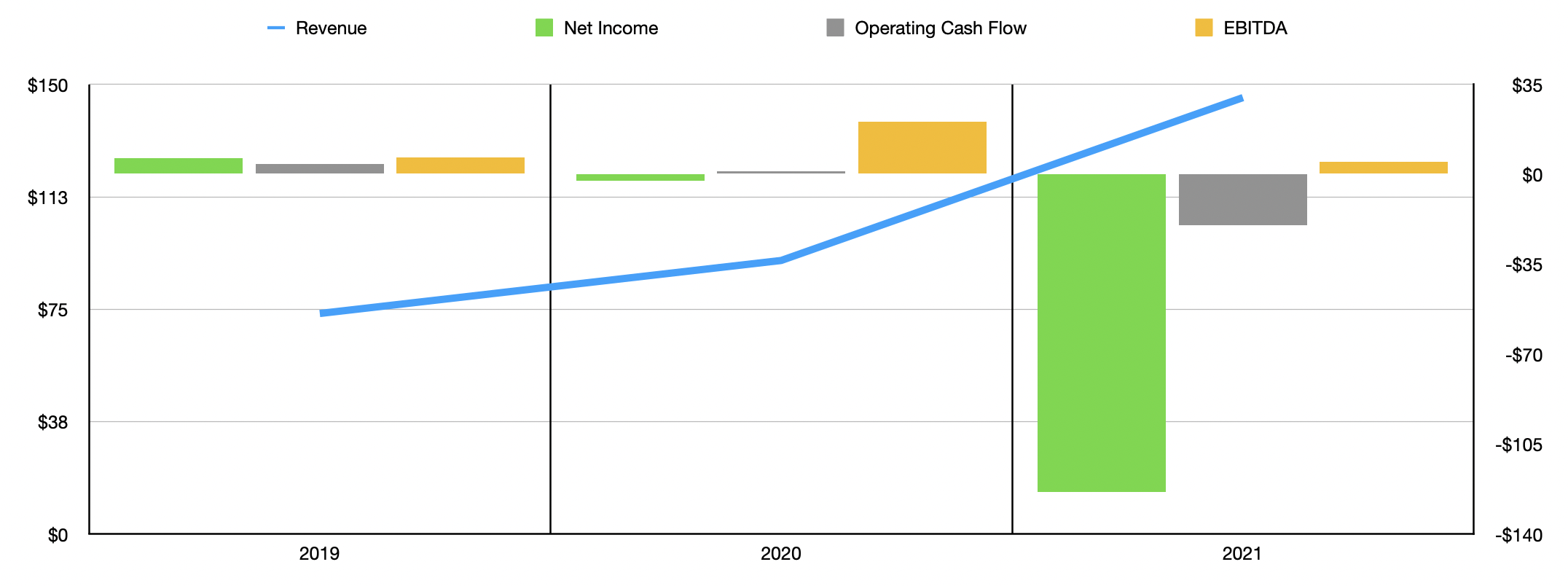

Over the past few years, financial performance for the company, at the top line, has been rather impressive. Between 2019 and 2021, for instance, the company saw revenue increase, climbing from $73.6 million to $145.6 million. The composition of revenue for the business has also changed during this time frame. For instance, during the firm’s 2021 fiscal year, an impressive 49% of revenue came from sales of their own software solutions. This compares to just 1% of sales that this accounted for back in 2016. Another interesting source of business for the company has been offering the ability of its own data scientists and software engineers to co-locate on the premises of its customers and, while there, to develop solutions for those customers. This is most common when the company works with government organizations.

Financially speaking, performance for the company has been rather mixed in recent years. Revenue growth has been consistently positive, but the same cannot be said of its bottom line. Net income for the company was $6.25 million in 2019. Then, in 2020, the company lost $2.55 million before generating a significant loss of $123.55 million. This is not the only area where the business worsened year after year. Operating cash flow for the firm went from $4.12 million in 2019 to negative $19.78 million last year. Even if we adjust for changes in working capital, the net outflow for the business was in the amount of $17.71 million in 2021. The only profitability metric that has been rather volatile has been EBITDA. This went from $6.54 million in 2019 to $20.51 million, on a pro forma basis, in 2020 before dropping to $4.85 million last year.

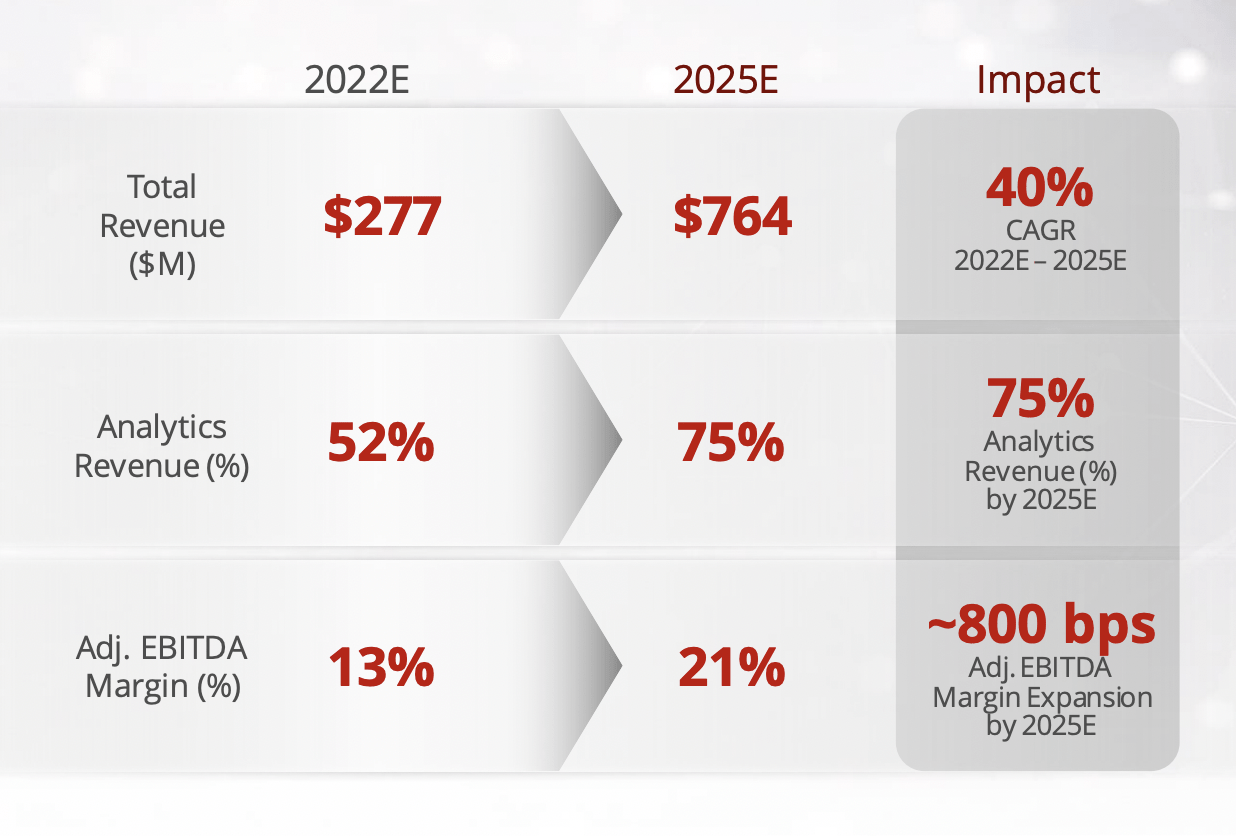

When it comes to the company’s 2022 fiscal year, this pattern of growing revenue but uncertain profits is likely to continue. According to management, sales for the company should come in at between $175 million and $205 million, of which only $20 million will come from commercial operations, with the rest attributable to government agencies. That represents an increase of 30.5%, at the midpoint, compared to what the company generated in 2021. While this does represent a nice increase year over year, it does fall far short of the $277 million management forecasted when they released an investor presentation back in September of last year. This faulty forecast does bring significant doubt to the company’s ability to grow its revenue to $764 million by 2025 like management said they believed they could.

BigBear.ai

The only guidance management gave when it came to profitability was that it claimed that EBITDA would be positive, but it provided no details as to how positive it might be. We do know that, when management forecasted originally for the firm to generate $277 million in revenue for the year, their plan was for an EBITDA margin of about 13%. If that same margin were to apply to what the company should now generate, then a reading of about $24.7 million is not unrealistic. We do know that net debt is just $24.68 million, which stacks up against the company’s market capitalization of $1.40 billion. But without some reliability on its bottom line, you can’t really value the business. The most generous attempt would be to assume that the same margin would apply to the company’s revised view of revenue this year. However, that would translate to an EV to EBITDA multiple of 57.7. And again, this is the generous, conservative scenario. Of course, if the company can achieve rapid growth, this multiple could come down. For instance, matching the 2025 targets management set forth in September of last year would bring the EV to EBITDA multiple of the firm, by that time, down to 8.9. But as we have seen already, there is substantial doubt about the firm’s ability to do so.

BigBear.ai

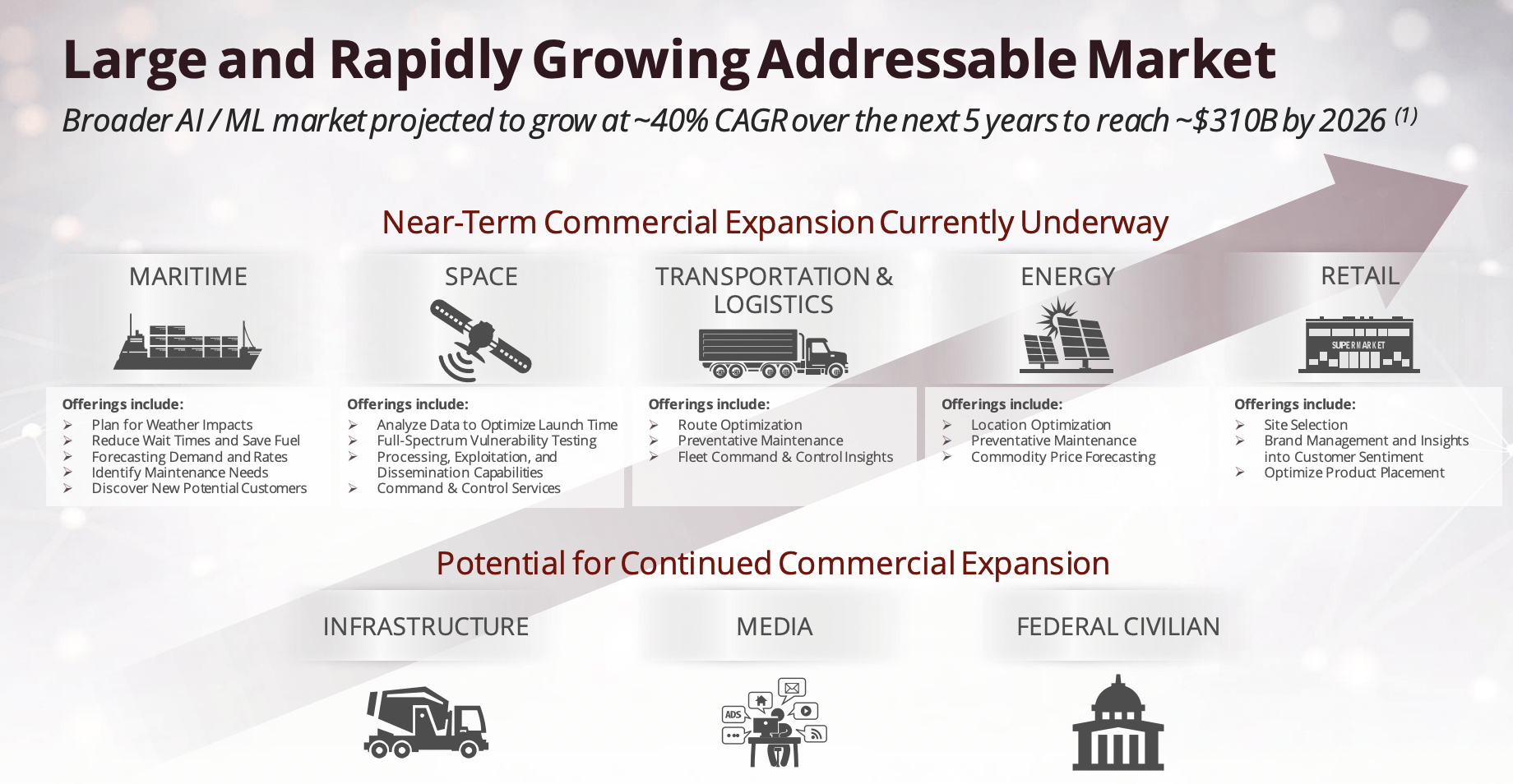

At the end of the day, investors in this company aren’t really buying into it for its valuation. They’re buying into it for its growth potential. Certainly, the market opportunity for the company is significant. At present, the company estimates that it operates in a total addressable market of roughly $72 billion. However, that market is forecasted to grow at a rate of about 40% per year, eventually hitting $310 billion by 2026. In that vein, the company has done well to grow its backlog. But much of this seems to be focused on multiple years worth of contracts. I say this because while backlog ended the most recent fiscal year at $465.7 million, the revenue increase this year relative to last year is not reflective of a significant portion of that being realized in 2022.

Takeaway

Based on the data provided, BigBear.ai may be doing well to grow its top line. But the company is virtually impossible to value given its uncertain and largely negative bottom line results. Even if we are generous, shares of the firm look rather pricey. This is true especially if we compare the multiple of the company to its revenue growth. Investors seem to be more focused on the broader market prospects for the firm. It is certainly possible the company could achieve tremendous long-term growth by appropriately targeting this space. But all things considered, it just does not appear to be a great opportunity at this time.

Be the first to comment