adaask

Both Enbridge (NYSE:ENB) and Kinder Morgan (NYSE:KMI) are high-yield investment grade midstream businesses with very strong cash flow profiles.

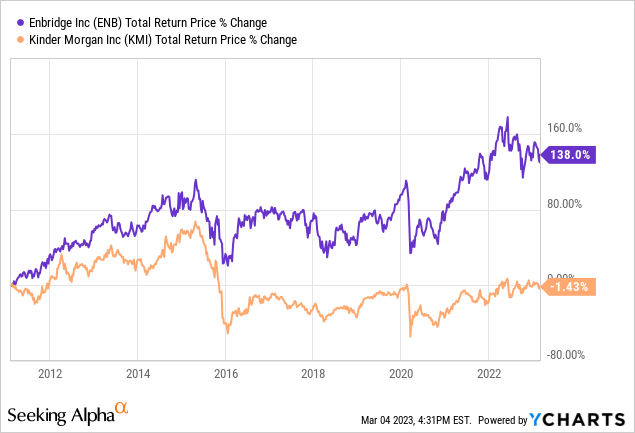

ENB has significantly outperformed KMI over time:

Furthermore, ENB has grown its dividend for 28 consecutive years, while KMI had a nasty dividend cut back in 2016 and has only been able to gradually grow its dividend in recent years.

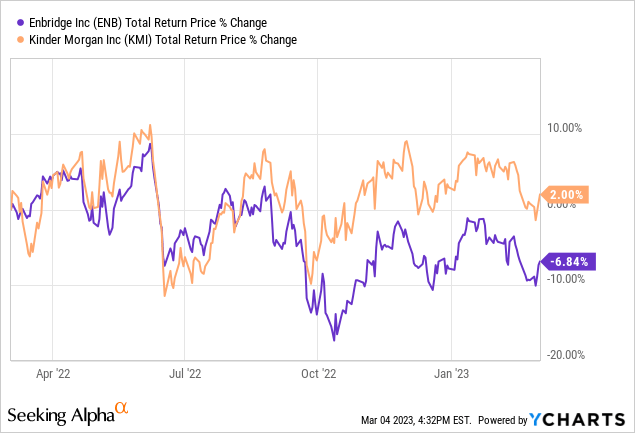

That said, KMI has meaningfully outperformed ENB over the past year and remains meaningfully cheaper on an EV/EBITDA basis.

In this article, we will compare them side by side and offer our take on which one is a better buy right now.

Enbridge Vs. KMI: Business Model

ENB’s business model features an exceptionally stable cash flow profile, with 98% of its cash flow linked to contracts that are unaffected by commodity price fluctuations, and 95% of its cash flow supported by investment-grade counterparties.

The company’s large and diversified asset portfolio provides several advantages, including economies of scale, growth investment opportunities, protection against individual asset, commodity, or geographic concentration risk, and a vital role in North America’s energy value chain.

ENB owns the second-longest natural gas transmission pipeline network in the U.S., North America’s largest natural gas distribution business, and longest crude oil pipeline network. Furthermore, the company is expanding its renewable power business to comply with Canadian environmental mandates, which provides another avenue for long-term growth.

For KMI’s part, the overwhelming majority of its counterparties are investment grade, which provides the company with a very steady cash flow stream in different macroeconomic environments. Its reliable cash flows stem from the company’s competitive advantages and the durability of its contracts, as 88% of its EBITDA is generated from long-term contracts that are resistant to commodity price fluctuations, such as take-or-pay and/or fee-based contracts. Furthermore, an additional 6% of its EBITDA is hedged, while only 6% is susceptible to commodity price sensitivity.

On top of that, KMI has a prominent presence in mission-critical midstream infrastructure. For example, KMI owns the largest CO2 transportation business, the largest independent refined products transportation business, the largest independent terminal business, and the largest natural gas transmission business in North America. In addition, KMI serves almost all of the country’s major gas supply and demand regions by transporting approximately 40% of all U.S. natural gas and 50% of its LNG.

Enbridge Vs. KMI: Balance Sheet

ENB enjoys a very robust financial position, as indicated by its BBB+ credit rating. Moreover, the vast majority of its debt has fixed interest rates and is not due until the 2030s, 2040s, 2050s, 2060s, and even 2080s, further emphasizing the company’s financial stability. Additionally, ENB’s leverage ratio of 4.7x falls within the lower half of its target debt/EBITDA range (4.5x – 5.0x), and its cash flow is very steady, with diversified assets underpinning it. Taken together, these factors imply that ENB is exposed to minimal to no financial distress risk for the foreseeable future.

KMI concluded the year 2022 with its lowest year-end net debt level since 2014. Moreover, KMI possesses a robust investment grade credit rating of BBB from S&P with a stable outlook. Furthermore, its net debt to EBITDA ratio is much lower than its long-term target of 4.5x. As a result, this suggests that KMI has the ability to increase its leverage ratio to take advantage of attractive opportunities as they arise.

Both companies are in excellent financial shape and face minimal risk of financial distress in the short term. Furthermore, the management teams of both companies imply that their balance sheets will continue to strengthen over time.

Enbridge Vs. KMI: Dividend Outlook

ENB’s and KMI’s investment-grade balance sheets, strong asset portfolios, and cash flow growth profiles indicate that both companies’ dividends should be secure for many years to come. Moreover, they are projected to increase their dividends at low to mid-single digit rates, and they have very strong coverage ratios based on DCF per share metrics.

Analysts project that KMI will grow its dividend at a 2.6% CAGR through 2027 while its DCF per share is expected to grow at a 3.2% CAGR over the same period. ENB is forecasted to grow its dividend at a 3.7% CAGR through 2026 while its DCF per share is expected to grow at a 2.6% CAGR over the same period.

While KMI has a stronger DCF/share growth profile, ENB has more robust dividend per share growth projections over this period. This is likely due to the fact that KMI has a pretty strong commitment to its share buyback, where it is likely to deploy a relatively greater portion of its retained cash flow than ENB is, while ENB will likely allocate more of its retained cash flow to dividends than KMI will.

Enbridge Vs. KMI: Catalysts And Risks

Any volatility in the energy industry is unlikely to present significant risks for both companies in the short to medium term, as they have a low-risk profile with commodity price insensitivity built into their cash flow profiles.

If the energy sector experiences long-term growth, the companies can benefit from higher contract fees and more opportunities for organic growth. They may also pursue growth through strategic acquisitions.

However, in the unlikely event of a much more rapid energy transition than is expected, both companies may encounter challenges such as reduced contract fees, excess network capacity, and limited opportunities for growth investment.

Enbridge Vs. KMI: Valuation

Based on the data below, we see that KMI is cheaper relative to ENB on both a comparative and historical basis based off of EV/EBITDA. KMI is also cheaper on a P/DCF basis. That said, ENB offers a slightly higher dividend yield.

| Metric | ENB | KMI |

| EV/EBITDA | 12.15x | 9.47x |

| EV/EBITDA (5-Yr Avg) | 12.55x | 10.18x |

| P/2023E DCF | 9.62x | 8.25x |

| Dividend Yield | 6.7% | 6.4% |

Investor Takeaway

When deciding between ENB and KMI, investors should consider that both companies have low-risk profiles, strong asset portfolios, and secure income yields. While ENB is in a slightly stronger financial position, KMI has a lower valuation. ENB has a better track record of dividend growth, while KMI has a superior per share growth profile with a cheaper valuation. Investors can choose between the slightly higher quality of ENB or the lower valuation of KMI, or both.

It is important to note that ENB is based in Canada and subject to tax withholding on dividends, whereas KMI is based in the United States. Investors should consider the tax and currency exchange implications when making their decision.

Although neither ENB nor KMI is currently our top investment choice for the midstream component of our portfolio at High Yield Investor, we still view both companies as attractive investment opportunities and rate them as Buys. Holding both in a well-diversified, low-risk, dividend-focused portfolio may be a prudent strategy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment