Scott Olson

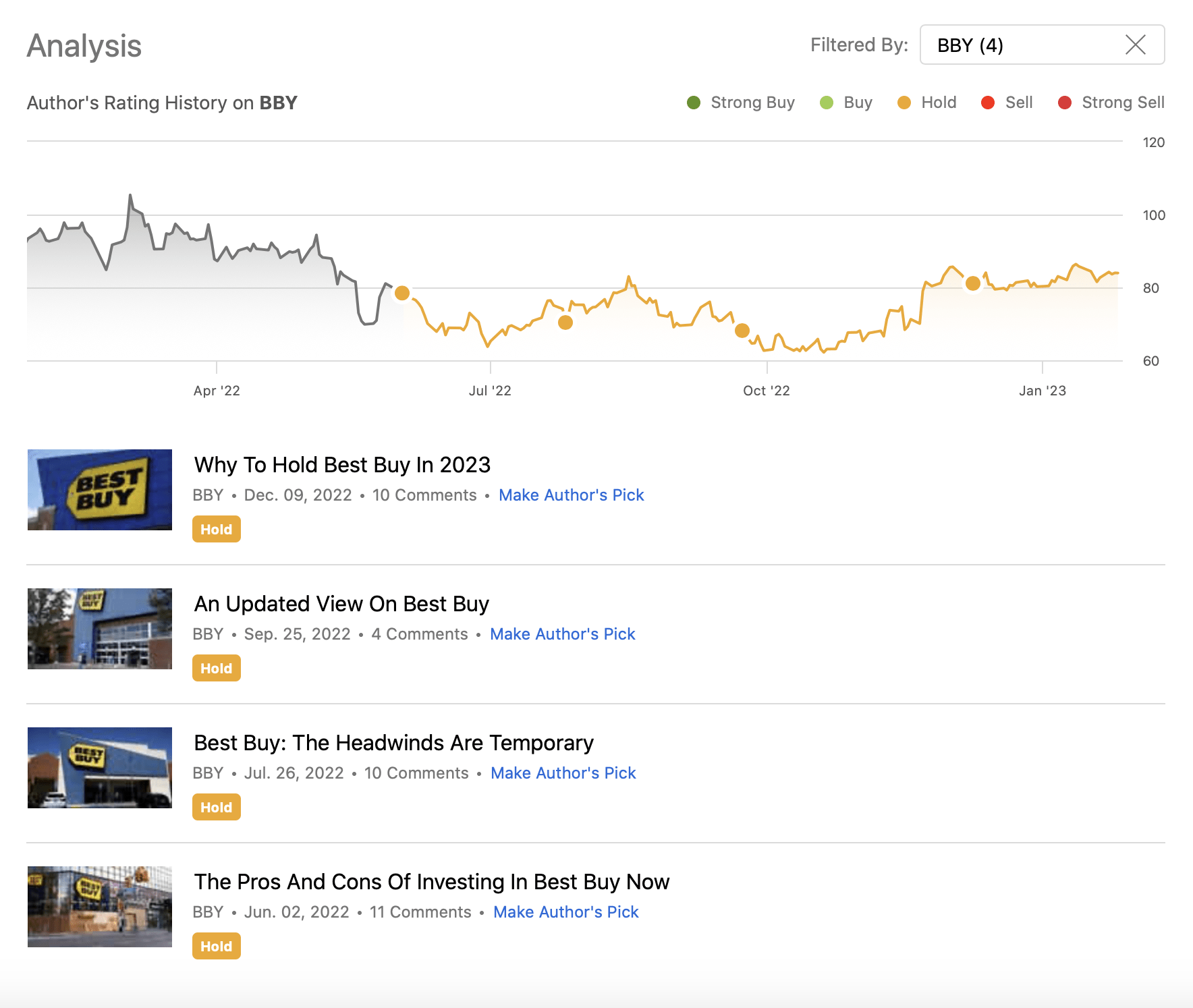

Best Buy Co., Inc. (NYSE:BBY) retails technology products in the United States and Canada. In 2022, we have published four articles on the firm, rating Best Buy’s stock as “hold” each time.

Analysis history (Seeking Alpha)

Today, we are going to take a look at Best Buy’s business from a different perspective. We will be examining the profitability and the efficiency of the firm, and its development over the past years, to understand: is it now a good time to start buying?

We will be primarily looking at the return on equity (ROE) and its change over time. We will decompose this ratio into three parts, namely into the net profit margin, the asset turnover and the equity multiplier.

ROE decomposition (investopedia.com)

Return on Equity

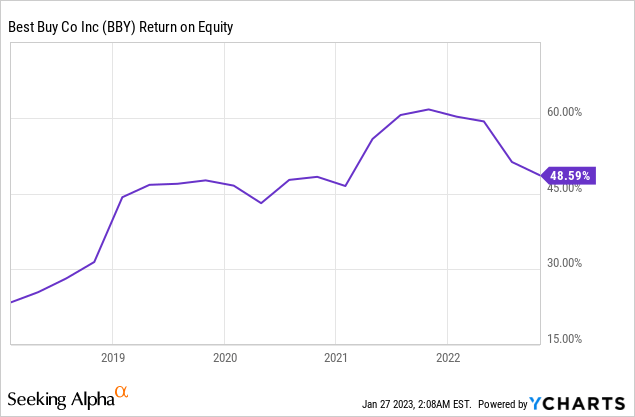

ROE is an important measure of financial performance and it is often used to gauge the corporation’s profitability and its efficiency of generating profits. Normally an improving or stable return on equity is preferred.

In general the company’s return on equity has been trending upwards since 2018. However, in the second half of 2022, it has seen a slight decline, which we believe can be explained by the challenging macroeconomic environment, including poor consumer sentiment and rising raw material and freight costs.

To understand better what is really behind this trend, let us look at the three components highlighted above.

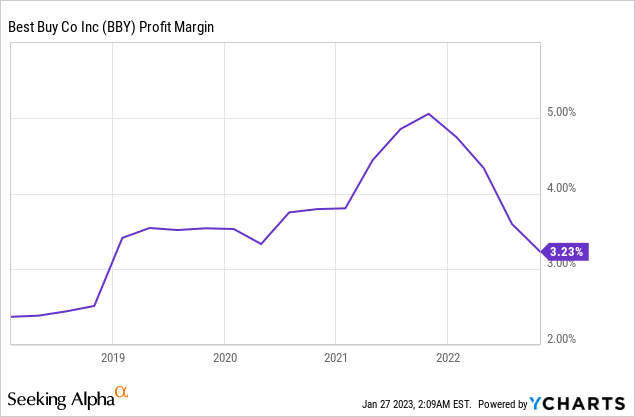

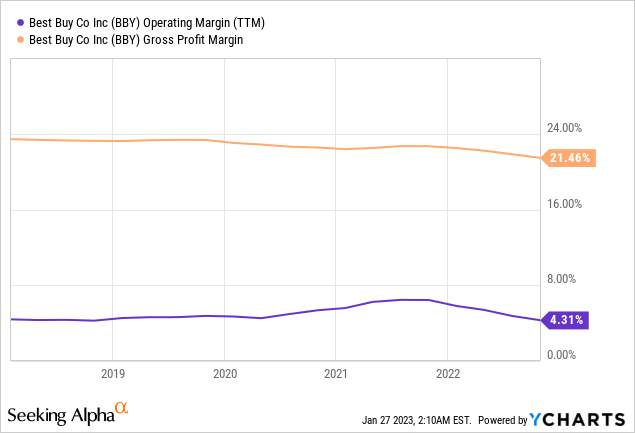

Net profit margin

In 2022, profit margin has been sharply declining, which we believe is the primary driver of the ROE decline as well.

Net profit margin can be significantly influenced by the macroeconomic environment. Due to the geopolitical tension in the Eastern European region energy prices have skyrocketed in 2022. Inflation and the substantial demand for increasing wages have also put an upward pressure on the costs.

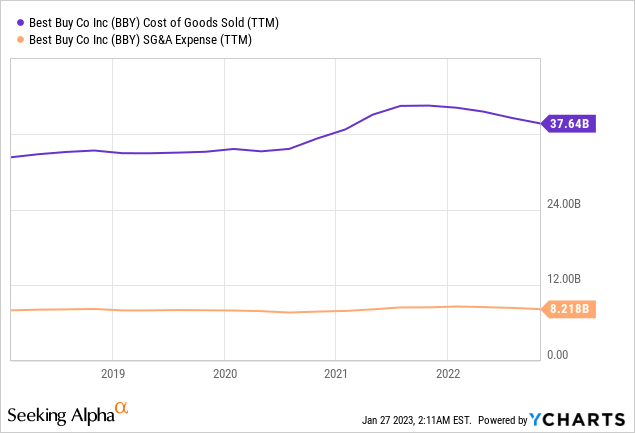

Costs

These in turn have not only led to a contraction of the net profit margin, but also the gross- and operating margins.

So what do we expect going forward?

Energy and fuel prices have moderated over the second half of 2022, which we believe is likely to have a positive impact on BBY’s margins in the coming quarters. Further, inflation readings have appeared also favourable in the past months, which may also benefit the firm.

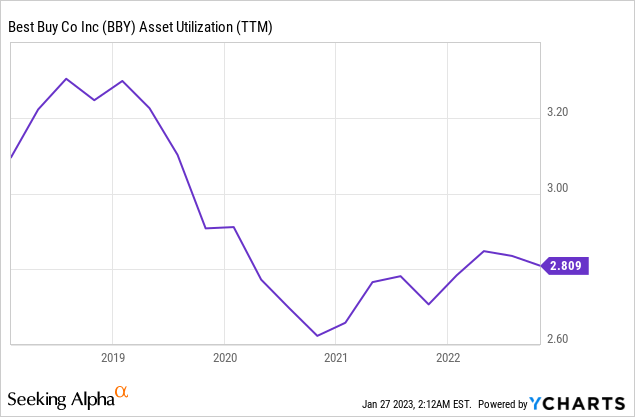

Asset turnover

The asset turnover ratio (or sometimes called asset utilisation) measures the value of a company’s sales or revenues relative to the value of its assets. It shows how effectively the company is using its assets to generate sales. Generally, we would like to see this ratio trending upwards or staying flat.

However, the asset utilisation of BBY has declined substantially compared to pre-pandemic levels. We would like to see this measure improving before upgrading our rating to “buy”. But going forward, we are actually expecting an improvement. The improving macroeconomic environment, especially the improving consumer sentiment, may fuel demand for discretionary, durable goods. When the consumer sentiment improves, people are more willing to spend on non-essential items, which can benefit BBY’s financial performance in the coming quarters.

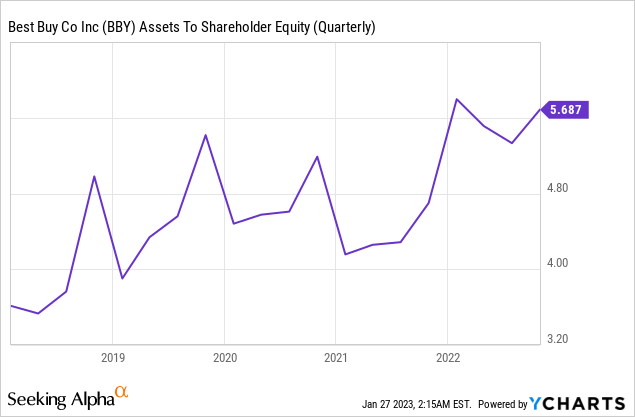

Equity multiplier

The last part of the three step decomposition of the ROE is the equity multiplier, which is simply the ratio of assets to shareholder equity. A higher ratio indicates more leverage, meaning that the firm is using a larger amount of debt to finance its assets.

The reason why ROE remained relatively high, despite the declining net profit margin, was the increasing leverage. In some cases increasing leverage can be beneficial, but we do not believe that this is the case for BBY right now.

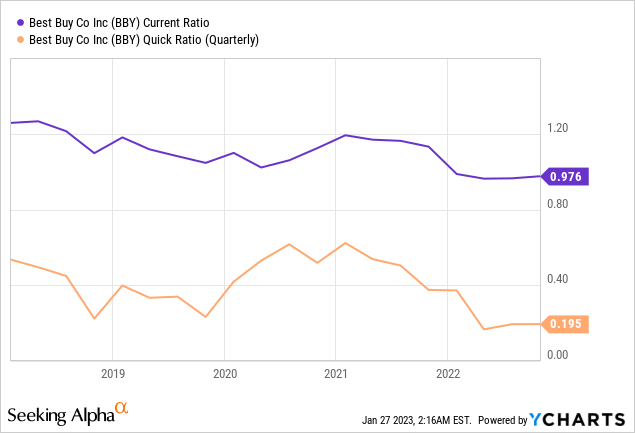

To explain why, we will look at the current- and quick ratios.

The current- and the quick ratios are liquidity ratios, indicating whether the firm has enough current assets to meet its current liabilities. We would ideally like to see both of these above 1. In reality, both of these are below 1 and have been exhibiting a generally declining trend.

Such a trend indicates that the firm’s ability to meet its current liabilities is decreasing, along with its financial flexibility. During downturns and challenging macroeconomic environments, we prefer when the firms have sufficient flexibility in order to be able to deal with unexpected situations. This we do not see in BBY’s case.

To sum up

It is definitely a good sign that ROE has been trending upwards, despite the macroeconomic challenges. While the net profit margin and the asset turnover have been negatively impacting the measure in the past quarters, we expect both of these ratios to improve in 2023, due to the improving consumer sentiment and the moderating raw material prices. At the same time, the increasing leverage is not particularly appealing, as both liquidity ratios have fallen below 1.

To reflect also on our previous writings:

- The firm remains attractive from a dividend payment and share buyback point of view.

- The valuation remains attractive, according to the traditional price multiples and the Gordon Growth Model.

In general, we are more bullish on the stock than in 2022, however we would like to see our assumptions about the improving macroeconomic environment materialise and the above highlighted measures improving before we would issue a “buy” rating.

For these reasons, we maintain our previously established “hold”.

Be the first to comment