LukaTDB

Bank of Hawaii Corporation (NYSE: BOH) has seen a lot of macroeconomic downturns. Its recovery and rebound, are a testament to its reliance and growth potential. True to its promises, it is regaining its footing after some slippages in the last two years. It appears more enticing and conservative to hedge the blows of economic uncertainties. Revenues and margins are more stable and consistent with its asset-sensitive Balance Sheet. Its liquidity position remains stellar with its stable cash balances and financial leverage. So, it is no wonder that it can sustain its branch openings and dividend payments. In turn, the stock price adheres to sound fundamentals while remaining reasonable.

Company Performance

For over a century, Bank of Hawaii Corporation had been through crests and troughs. Economic downturns had a massive impact on many banks, and BOH was never an exemption. Even so, it managed to get through them. In the last two years, another crisis disrupted its flourishing operations. The pandemic limited its potential as interest rates fell to almost zero. It was logical since its loans were more interest-sensitive. Despite all these, it remains the largest bank in the state, with many shareholders living in the area. It is also one of those with the largest deposits in the state. It has become more conservative amidst the influx of willing borrowers in the last two years. Now, its prudence is paying off as it expands amidst inflation.

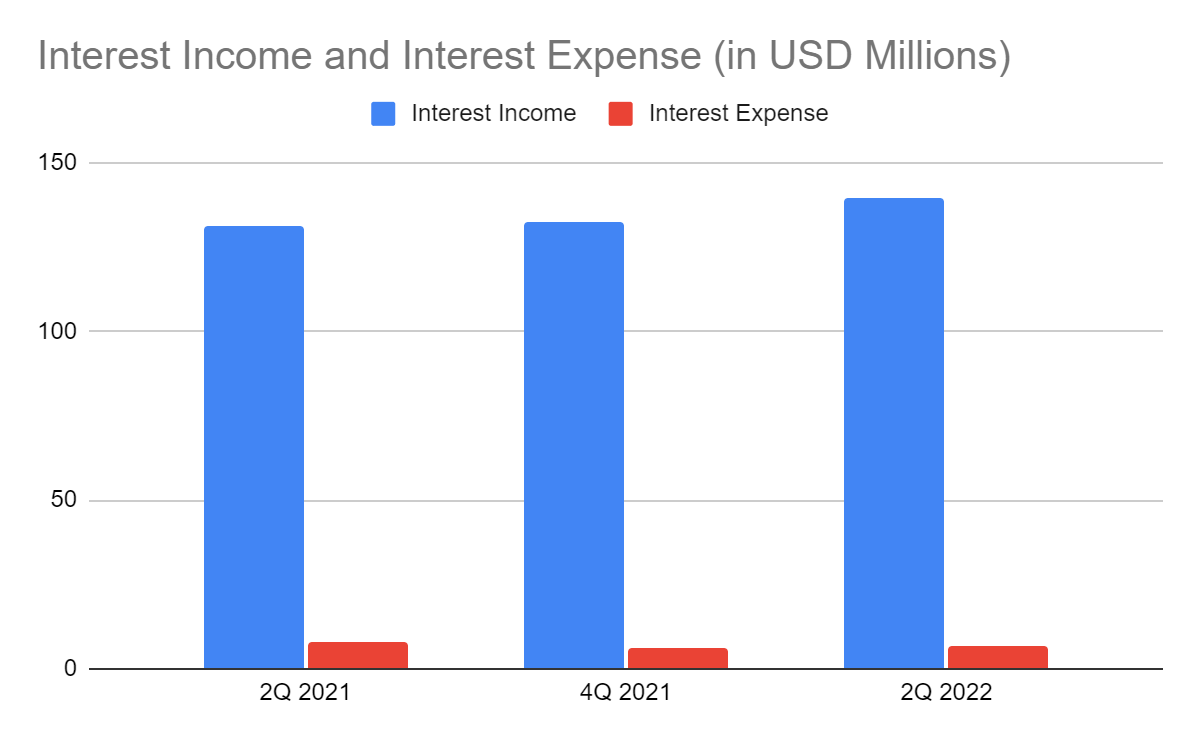

Its interest income amounts to $139.56 million, a 7% year-over-year growth. Thanks to its conservative loan balance to capitalize on the rising interest rates. Its loans are more responsive to interest rate changes. A massive bulk of loans are from mortgages and home equity. Commercial and industrial loans are also interest-sensitive. So, the growth in loans is driving higher interest income. Both loan segments are larger today. But, its increased focus on more secure loans, such as commercial loans is vital for its stability.

Its investment decisions are also wise, allowing it to derive more dividend income. Its securities are decreasing their appeal and value amidst the interest rate hikes. It is reasonable since higher interest rates affect mortgage-backed securities. Even so, its asset-sensitive Balance Sheet is working better in a high-interest environment. Its assets are well-positioned with a strong capital base and liquidity. It shows its impressive asset quality. In fact, ROAA is 1% vs 0.97%, showing it yields more returns today. ROAE is 18% vs 15% in the comparative quarter. Deleveraging is another core strength of the company. Borrowings are lower than in the comparative time series. It has a partial offsetting impact on the decrease in deposits. As such, interest expenses are lower at $6.7 million vs $7.9 million despite the interest rate hikes.

Interest Income and Interest Expense (MarketWatch)

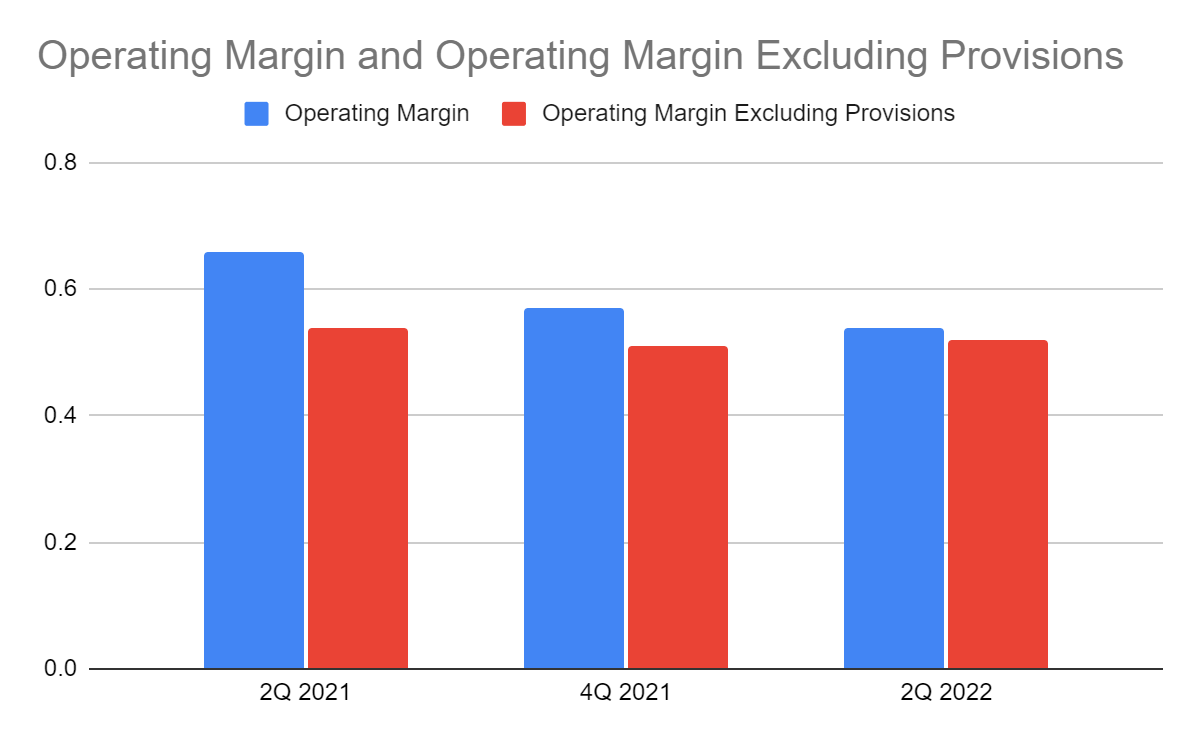

Despite its robust performance, the company remains conservative to remain liquid. I will discuss more of its Balance Sheet in the succeeding part. With its high-yielding assets and well-managed borrowings, its revenues and expenses are stable. Its net interest margin without credit loan provisions is 95% vs 94% in 2Q 2021. Its non-interest segment remains stable so its operating margin without provisions of 52%.

Operating Margin and Operating Margin Without Provisions (MarketWatch)

Macroeconomic Factors

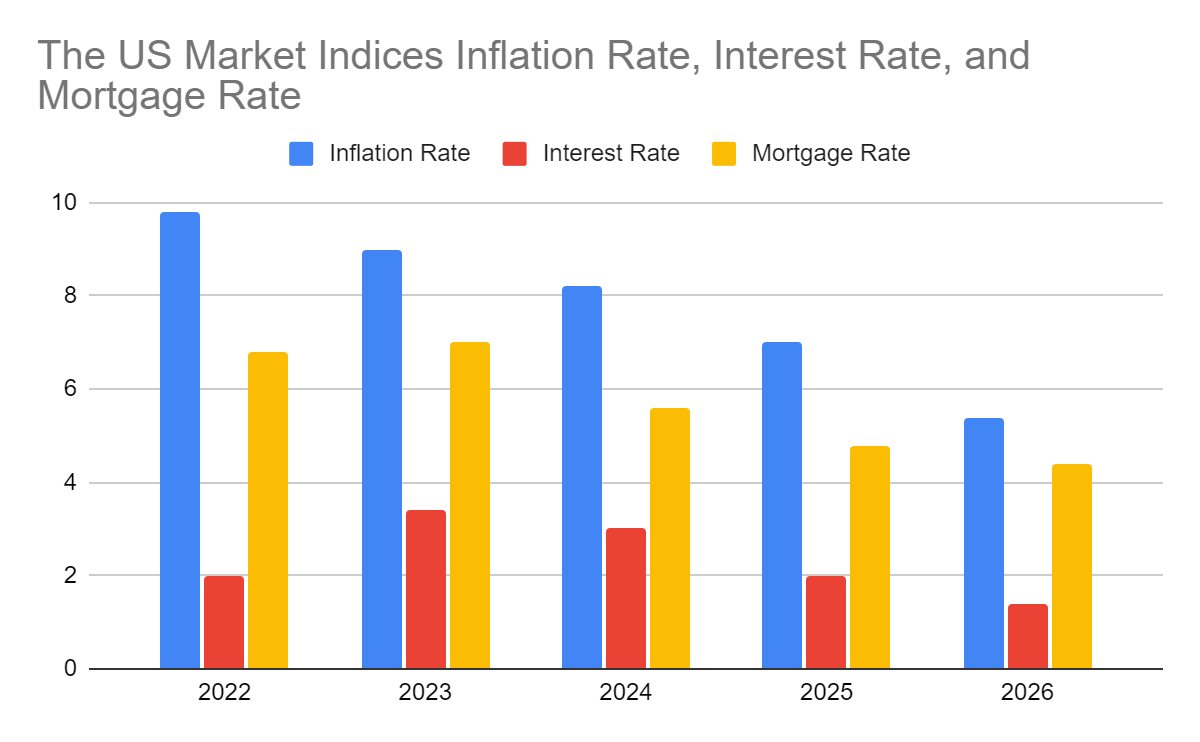

Bank of Hawaii Corporation faces more external pressures as the economy reopens. The high-inflation environment has become more evident in the second quarter. In June, it had another all-time high at 9.1%. The pent-up demand and the disturbances in Europe are the primary driving forces. The supply chain disruptions also raise prices. To make it simple, the US economy sees a combination of pent-up demand and shortages. So, it raised the price further in the first half. But now, inflation seems to be going into a summer lull as it stays lower at 8.5%. Inflation may be affecting the demand elasticity as more consumers adjust their spending. Even so, I still project the inflation rate to reach 9.6%, given the uncertainty. In the following years, I expect the pandemic fears to subside. I expect the economy to be more flexible, so inflation may decrease from 9% to 5.2%. It is still higher than pre-pandemic levels, which is still logical.

The interest and mortgage rates are going in the same direction. A series of hikes are expected to stabilize inflation. Also, the Fed has already raised 75 basis points in June. It may speed up in the second half as shortages become more evident, raising prices further. So, the interest rate may peak at 3.4% this year. It is already higher than the previous estimations. Meanwhile, the mortgage rate is at 5.7%, which is already higher than the estimation of 5.1-5.3%. With that, analysts expect it to be even higher at 7%. But in the following years, I expect them to have a gradual decrease as inflation may become lower. Although higher than pre-pandemic levels, they may become more stable.

Inflation Rate, Interest Rate, and Mortgage Rate (Author Estimation, Barron’s, and Forbes)

Fortunately, BOH is working better in the high inflation environment. It capitalizes on higher interest and mortgage rates to generate more returns. Its interest-sensitive assets are generating more returns except for its securities. But, its stable deposits and borrowings enhance its risk tolerance and capital preservation. Currently, it continues to take the lead in Hawaii as its primary market. SMEs are also bouncing back, one of the primary markets. The housing and automobile boom persists despite the slight decrease in spending. Transactions are more client-facing with improved digital capabilities. It allows it to manage its operating capacity and cater to more customers. It is also in line with its expansion and enhanced user experience.

Why Bank of Hawaii Corporation May Remain Sturdy

The performance of BOH appears to be more robust this year. Its rebound is more sustainable, matched with its expansion. It continues to diversify and improve the quality of its asset-sensitive portfolio. It has a better liquidity position and risk tolerance. The uptrend in the C&I and mortgage segment allows it to take advantage of higher rates. Also, its enhanced digital market presence may help it capture and keep more clients.

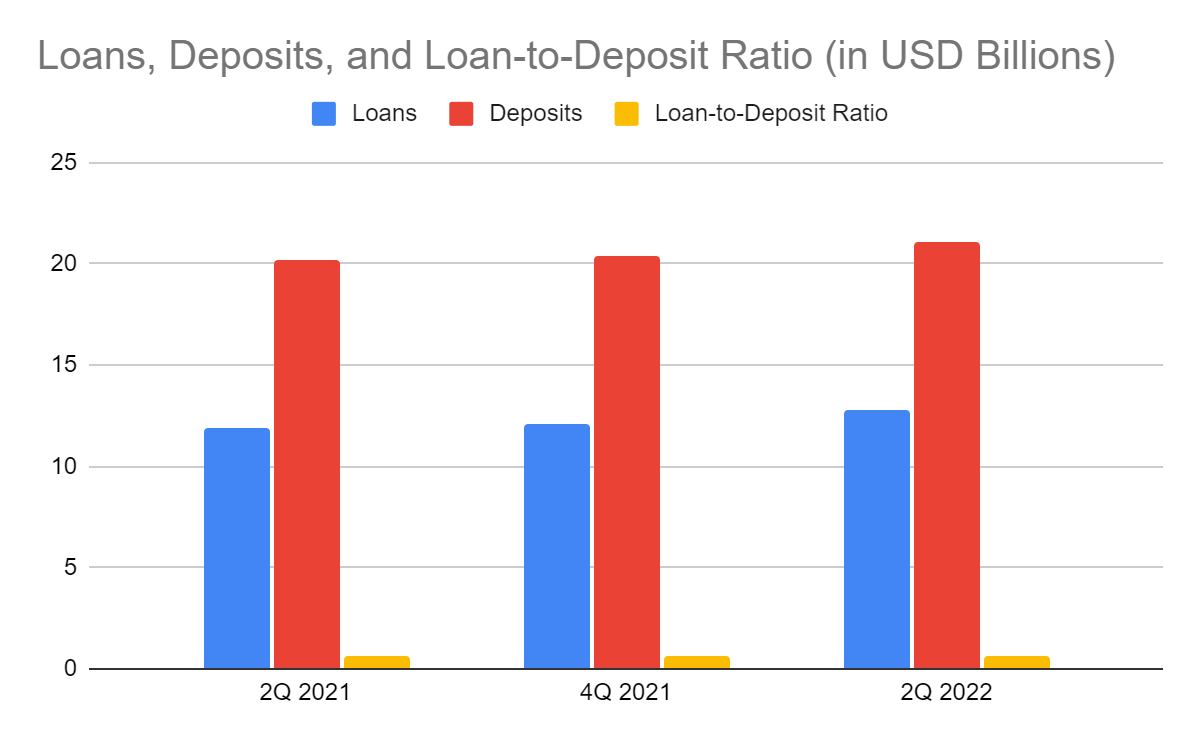

It also enjoys its high-yielding loans, especially mortgage and housing equity loans. As such, it is logical for it to take advantage of the situation and raise its loan volume. Even better, it has an excellent liquidity position with a loan-to-deposit ratio of only 61%. It is way lower than the average ratio of 70-90%, making it more conservative. It has more room to loan out to more borrowers without risking its liquidity. Also, its loan provision is 1.16%. Although it is lower than the comparative quarter, it remains ideal for banks of its size. Likewise, deposits are higher but stable, which is ideal in a high-interest environment.

Loans, Deposits, and Loan-to-Deposit Ratio (MarketWatch)

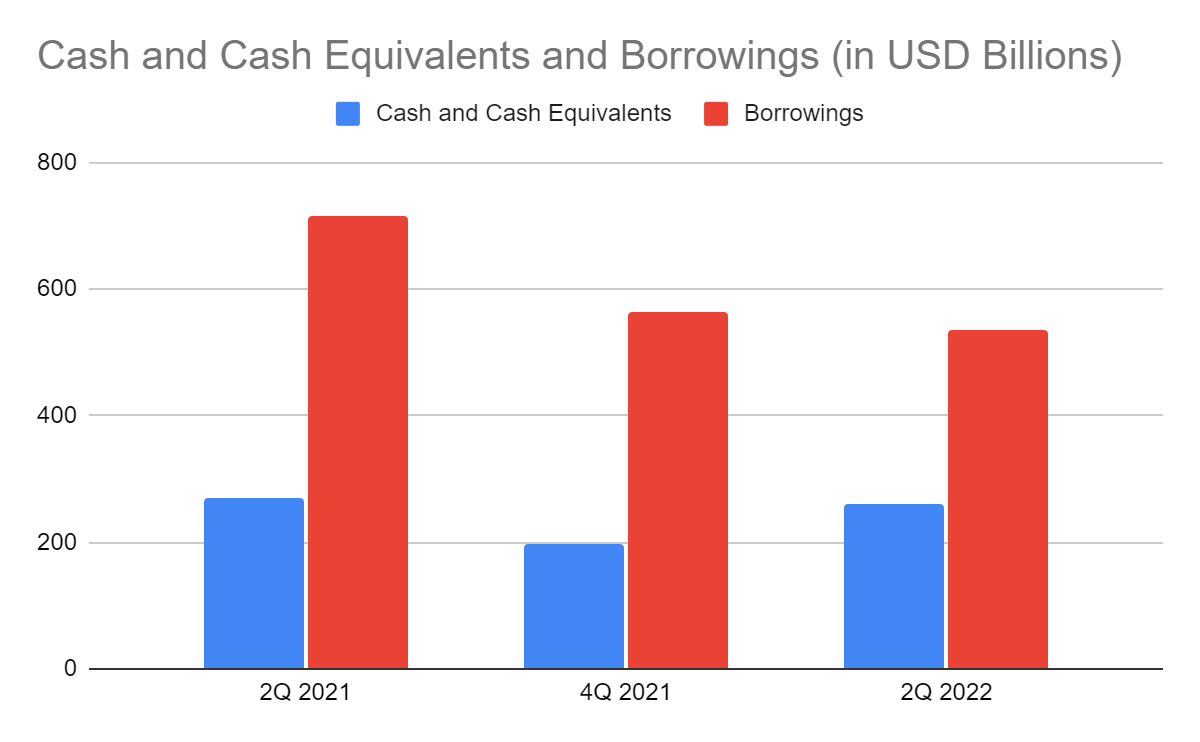

Meanwhile, cash and investments comprise 41% of the total assets, so it is very liquid. Its cash levels are stable, allowing it to sustain its operations. Deleveraging is another attribute of its impressive liquidity. The total borrowings today are 26% lower than in 2Q 2021. So, the percentage of cash and cash equivalents to borrowings is 49% vs 38% in 2Q 2021. Its Net Debt/EBITDA is only about 1.4x, so the bank earns enough to cover its borrowings.

Cash and Cash Equivalents and Borrowings (MarketWatch)

Given its stellar Balance Sheet, BOH is well-positioned against economic disruptions. It can sustain its current size and expansion while remaining liquid and viable. In fact, it made another branch open in the state, increasing its operating capacity.

Stock Price Assessment

The stock price of Bank of Hawaii Corporation has been in a sharp uptrend in the last two months. It is already the same as the price at the start of the year, making it reasonable. At $84.03, it is 17% higher than the most recent dip. But, it still appears reasonable at an earnings multiple of 14x. Its Price-to-Cash Flow Ratio is 10.47.

Even better, the company is consistent with its dividend payments. Although dividend growth was not sustained in some years, payments were continuous. Even at the height of the pandemic, dividends were still paid and did not decrease. Its dividend yield of 3.29% is higher than the average of the S&P 400 at 3.04%, making the stock price reasonable. To assess the stock price better, we will use the DCF Model and the Dividend Discount Model.

DCF Model

FCFF $310,000,000

Cash $261,000,000

Borrowings $536,000,000

Perpetual Growth Rate 4.8%

WACC 9%

Common Shares Outstanding 40,183,000

Stock Price $84.03

Derived Value $96.17

Dividend Discount Model

Stock Price $84.03

Average Dividend Growth 0.08368335533

Estimated Dividends Per Share $2.80

Cost of Capital Equity 0.1168347881

Derived Value $90.0844144 or $90.08

Both models show the potential undervaluation of the stock price. The stock price may have a 7-12% upside. The stock price also appears reasonable and attractive.

Bottomline

Bank of Hawaii Corporation moves in line with the economic pattern of Hawaii. It has an impressive positioning of its asset-sensitive portfolio. It has adequate capacity to sustain its current size, expansion, and dividend payments. Also, the stock price is still reasonable with potential undervaluation. The recommendation is that Bank of Hawaii Corporation is a buy.

Be the first to comment