sshepard

Earnings Estimates Q4 2022

Analysts expect Bank of America Corporation (NYSE:BAC) to earn $.7687 per share in Q4, a decline from Q3 earnings of $.81, and $.82 in Q4 2021 when the bank’s Provision expense was -$482 million.

Q4 2022 Provision likely will be roughly in line with the $900 million reported in Q3 2022.

BAC EPS Est (Seeking Alpha, YCharts)

Analyst Ratings

Street analysts rate BAC “Outperform” with a composite score of 2.22. None of the 27 analysts following the stock rate it a Sell or Underperform.

BAC Investment Outlook Street (YCharts)

Seeking Alpha analysts during the past 30 days are more bullish on BAC than the Street, giving BAC a composite score of 2.06. However, two analysts rate the bank Underperform.

BAC Investment Outlook Seeking Alpha (Seeking Alpha)

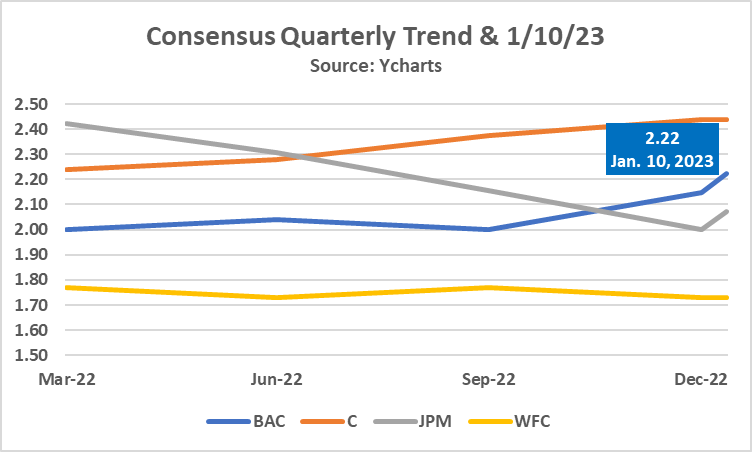

The BAC consensus rating of 2.22 is moderately less favorable than JPMorgan Chase & Co (JPM), and significantly less favorable than Wells Fargo & Co (WFC). Only Citigroup Inc (C) among the four big banks has a lower analyst composite score than BAC.

Consensus (YCharts)

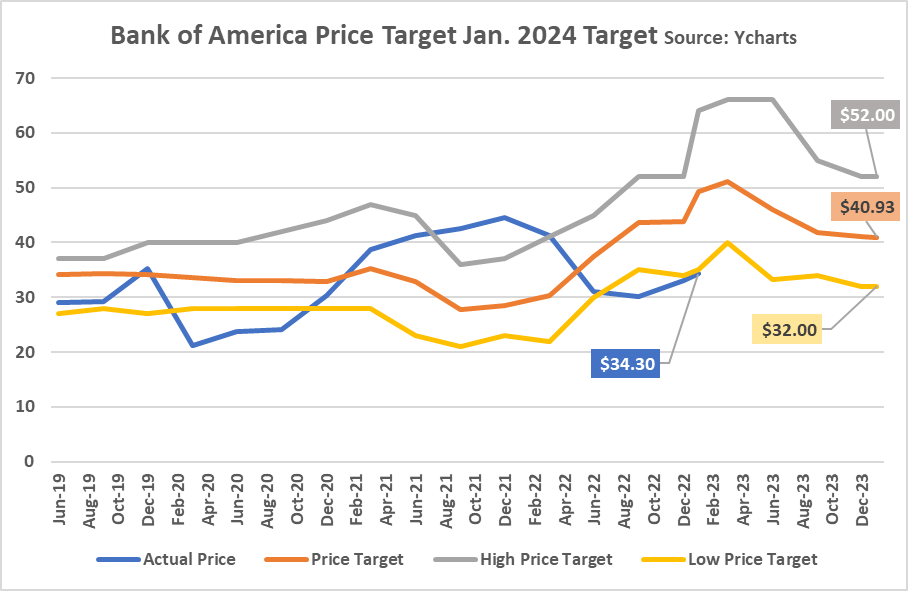

Price Target

Consensus Price Target for BAC a year from now is $40.93, a 19% jump from January 10 close. The range in price targets is a low of $32 and high of $52.

I think a $40 number is reasonable for reasons I will note below.

An examination of the next chart may erode investor confidence in analyst Price Targets. Since 2019, the analyst community’s crystal balls have been extra fuzzy as their misses are material. In fairness, Covid created absolute havoc not only for the world, but bank analysts as well who struggled with the wild jump in Provision expense in 2021 and reversals in 2022.

BAC Price Target (YCharts)

My Thoughts Ahead of January 13 Earnings Report

During the past 30 days, I have added BAC and Bank of America Preferred (BAC.PL) shares at <$32 and <$1200, respectively. If the Q4 earnings report proves favorable as I expect, my purchase price cap for BAC common will move to $<35.

I will not repeat the major points from my “Bank Poised to Breakout” September 2022 BAC article, instead urging investors to read CEO Moynihan’s comments at the December 6 Goldman Sachs US Financial Services Conference.

Moynihan’s December comments, together with insights learned from the bank’s Q3 earnings call, caused me to change my view of the bank’s prospects from Buy to Strong Buy.

Because Moynihan’s comments at the Goldman conference were so revealing, I believe investors should expect to learn the following on January 13:

- Steady, durable deposits at $1.9 trillion, which amounts to $500 billion in “excess deposits,” per Moynihan.

- Funding costs at the lowest range of the big banks as loans remain close to 50-55% of deposits. Perhaps the most stunning number from the Moynihan comments at Goldman: BAC has only $30 billion in CDs in a $1.9 trillion deposit base. Moynihan said, “we don’t need the funding.”

- BAC is adding 1 million new checking account relationships a year.

- Customer retention and satisfaction appear stable.

- Expenses (~$15.3 billion/quarter) which have run 2% year-over-year, will increase moderately because of inflation, but operating leverage is expected to continue its favorable trend.

- There appears to be a freeze on hiring (needs to be confirmed), with the bank targeting a headcount target of 205,000 versus current 215,000. No layoffs.

- Investment in technology continues to increase, up 15% from 2020.

- Real estate usage cut from 130 million square feet in 2010 to 70 million today.

- Moynihan expressed concern about the overall state of office real estate in the US. Related, he noted that the bank is a conservative commercial real estate lender, with CRE loans at ~6% of the total loan book.

- Loans are expected to show mid-single digit Y/Y growth. 92% of commercial loans $s are investment grade.

- Securities/Investments remain short-term and exclusively “risk-free” US-backed. The bank is avoiding duration risk, though open in mid-2023 to extending maturities in mortgage-backed securities.

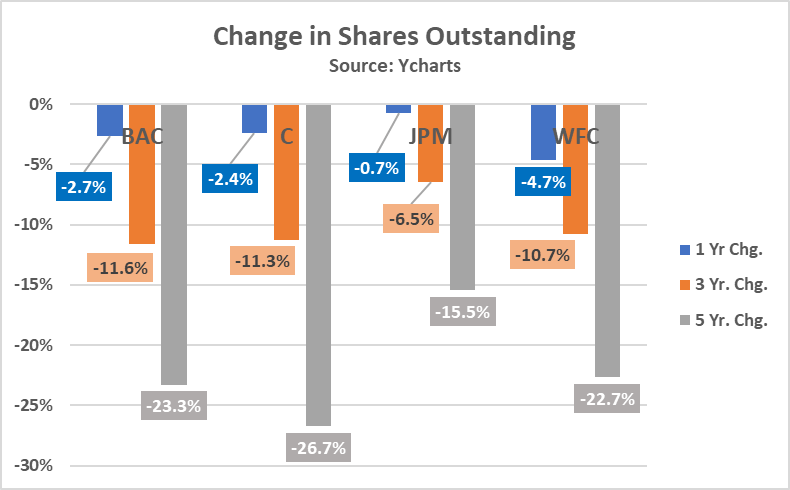

Share Repurchases: Looking for More Insight

At both the Goldman and the Q3 earnings calls, Moynihan spoke to capital adequacy, free cash flow, and share repurchases. Investors should learn more details on January 13.

Moynihan said in October, “you should expect that buybacks will continue to increase”.

Specifically, I would like to know total repurchases in Q4, if any?

Also, I would like more insight about current capital ratios given the attention this topic is getting with a new head of the Fed Stress test. Moynihan implied in December that the bank has met or exceeded key capital ratios that could constrain buybacks if not otherwise achieved.

Below are the most current numbers I have on share count for the four big banks as of the date of each bank’s most recent 10-Q. Repurchases will be a hot topic on the upcoming earnings calls for all four banks.

Share Count (YCharts)

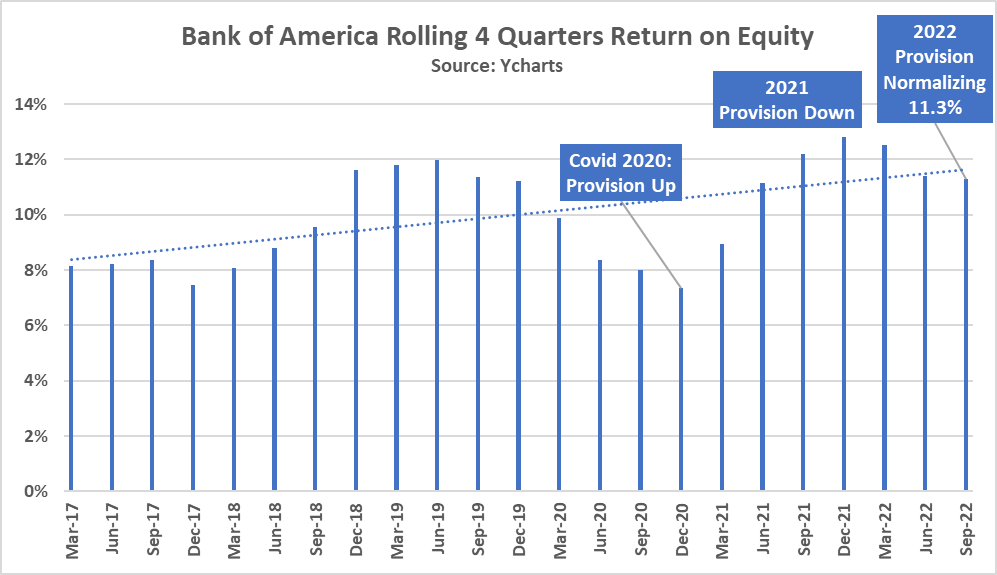

Key Number: ROE

Investors who have read my work for a while know that I prefer High-Quality banks, which I define as banks that consistently and reliably generate returns on investor equity greater than the bank’s cost of capital.

I expect BAC to generate ~11% ROE over the next of couple years. The Q4 earnings report will be a key check point.

Here is the recent trend. As noted, I take ROE numbers for 2020-2021 with a grain of salt given the wild fluctuations in Provision.

BAC ROE Rolling 4 Quarters (YCharts)

Risks

Moynihan started his Goldman presentation with the bank’s economic forecast which calls for the economy falling into a moderate recession (-1.5 to -2%) in 2023. BAC currently forecasts for the economy to get back on track during Q4.

BAC expects unemployment to hit 5% to 5.5% this year, which will have an impact on credit performance.

Moynihan says, “US consumers are in good shape,” but also noted that BAC consumer payments slowed to 5% Y/Y compared to 11% earlier in the year. (I interpret this comment to mean the Fed is getting what it wants: a slowdown.)

BAC expects credit to deteriorate, with 5 and 30-day delinquencies up from earlier in the year but still below pre-Covid 2019 numbers.

Moynihan expressed confidence that the bank will weather a weaker economy since management “built the company for that (business cycle) purpose.”

BAC sees evidence that consumers are being “more careful” and “cautious,” with credit line usage shrinking.

Investment Banking activity is down ~30% across the US (if I followed Moynihan’s math) for not only BAC but the industry; the bank is maintaining share.

Sales & Trading activity will be a big focus on January 13 given the uncertainties associated with market volatility.

Caveat

The foregoing is my opinion which I share for the purpose of getting feedback and questions that challenge my ideas and assumptions.

Every investor needs to do his/her own due diligence before investing as well as determine their risk profile. I am risk-averse, preferring to invest in the nation’s best banks which reliably earn returns exceeding cost of capital.

Be the first to comment