The NASDAQ Stock Exchange headquarters in New York, JHVEPhoto/iStock Editorial via Getty Images

About Atlis Motor Vehicles

www.atlismotorvehicles.com

ATLIS Motor Vehicles, Inc. (NASDAQ:AMV) was formed as a Delaware corporation on 11/9/16 and is based in Mesa, Arizona. ATLIS is a vertically integrated, mobility technology company developing products that will power work. The Company is working toward production of an electric vehicle technology platform for heavy and light duty work trucks for individual and fleet use in agriculture, service, utility, and construction industries, amongst others. To meet the towing and payload capabilities of legacy diesel-powered vehicles, ATLIS has developed proprietary battery technology and a modular system architecture capable of scaling to meet the specific needs of the all-electric vehicle. – Source: Company

Stock performance

Seeking Alpha

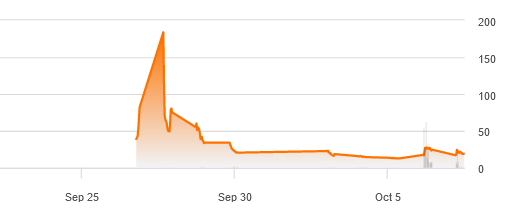

As the above chart shows, AMV’s stock price has mimicked a roller coaster ride since it began trading on the NASDAQ stock exchange on 9/27/22 via a Regulation A filing. The high/low price range of $243.99/$12.05 as of 10/7/22 underscores the extreme volatility of this speculative stock. Prior to 10/6/22 AMV was thinly-traded, due at least in part to issues some shareholders experienced in trying to dispose of their shares. Although Atlis CEO Mark Hanchett recently apologized to “about 20,000” AMV investors, I believe that this will be of little solace to those who incurred a financial loss because of this debacle. In my view, AMV suffered reputational damage as a result of this gaffe which may trigger SEC scrutiny and/or a shareholder lawsuit. The 10/6/22 volume of 5,733,600 was 2,130% higher than its average daily volume of 269,200 prior to 10/6/22 which is strong evidence of day-trading activity. Based on AMV’s recent trading pattern, I believe that continued downside price pressure is on the horizon.

SEC caveats

The SEC has warned investors about the risks of investing in Regulation A securities offerings and advised investors to be aware of investment research websites or articles that seem to provide unbiased commentary on stocks, as they may be a part of an undisclosed paid stock promotion. Nanalyze has bluntly stated that Regulation A and equity crowdfunding securities offerings should be avoided like the plague because “they’re a funding option for firms that institutional investors don’t want any part of.” I second that motion in a New York minute.

AMV capitalization

Atlis Motor Vehicles

Atlis Motor Vehicles

The above offering circular indicates that AMV has focused on unsophisticated investors, many of whom patronize reddit.com 24/7/365 and post such drivel that AMV is the “Best non-Chinese IPO!” This level of hyperbole is reminiscent of infomercial king Ron Popeil and his trademark mantra “But wait, there’s more!” And there is more. Atlis has also engaged the services of startengine.com and this attention-getting headline “StartEngine Retail Investors See 137,000% Return After Atlis Motors AMV) IPO” will increase interest in the site and make Shark Tank’s Kevin (“Mr. Wonderful”) O’Leary proud. Only in America, right? However, as AMV attempts to transition from a Main Street to a Wall Street investor base they will need to develop a new and sophisticated capitalization strategy to be successful, which in my view will be a heavy lift.

AMV balance sheets, income statements, and cash flow statements data

Key takeaways from my review of AMV’s three core financial statements are as follows:

SEC

SEC

As shown above, as of 6/30/22 AMV’s cash balance decreased by $2,508,096M, or 79.7% YTD.

SEC SEC

As shown above, as of 6/30/22 AMV had a working capital deficit of $639,993 ($1,207,877-$1,849,079) compared to a working capital balance of $2,727,706 ($3,436,741-$709,035) as of 12/31/21. In addition, as of 6/30/22 AMV had a current ratio of 0.65 compared to a current ratio of 4.85 as of 12/31/21.

SEC

SEC

As shown above, as of 6/30/22 AMV had a YTD net loss of $36,977,689 compared to a net loss of $11,201,341 YoY which represents an increase of $25,776,348 or 230.1%.

SEC SEC

SEC

SEC

As shown above, as of 6/30/22 AMV’s sole source of cash YTD was from sale of securities in the amount of $8,881,902 from their Regulation A and crowdfunding campaigns. Since net cash used from operating and investing activities during this time period totaled $11,389,998 ($11,330,613) + $59,385), there was a YTD decrease in cash of $2,508,096 as of 6/30/22.

Financial pro formas

As a former CPA with significant audit experience, this going concern qualification contained in AMV’s audited financial statements for the year ended 12/31/21 is a serious issue for me. Until this situation is remediated, Atlis is likely to be hamstrung in their efforts to obtain sufficient additional funding. Based on the company’s YTD 2022 cash burn rate, and expected capital expenditures in the near-term at this time it appears that AMV may face a liquidity crisis sometime in 2023. The next 10-Q filing may provide some meaningful insight into their present capitalization and clarify their path forward for the remainder of 2022.

Bulls vs. bears

The crux of this debate is whether AMV’s can achieve profitability based on the company’s claim that they can do so within six years with additional capitalization of $370M. The bull case is largely based on company website data and links to media coverage of the company which readers may access here. AMV’s aspirational agenda includes an innovative subscription model which I believe may be the wave of the future. The bulls also are counting on the company’s ability to sell AMV XT at a base price of $45,000, which would be considerably less than the $68,575 base price of the Rivian (RIVN) R1T. In my view, the ability to produce a 15-minute charging capability would be an instant game-changer for the company as they would have the opportunity for a multi-million licensing deals with other vehicle manufacturers. Under this scenario AMV would be on the radar of the industry giants as a compelling takeover.

The bear case is that AMV will be unable to execute their business plan given the financial firepower of their competitors in the EV light and heavy truck sector. They point out that the company has made several representations in the past which have not reached fruition and have not delivered on several key development timetables. They argue that the current valuation is prohibitively inflated since AMV is a pre-revenue developmental stage company and Wall Street has no appetite at present for money-losing companies. I am from Missouri on this one as I consider Atlis to be a “show me” stock not worthy of investment consideration at this time. As always, the devil will be in the details.

Conclusion

Based on the foregoing financial and operational analysis, Atlis Motor Vehicles, Inc. faces Hurricane Ian-like headwinds going forward and has no clear path to profitability. In my view what Mark Hanchett, AMV’s CEO and Founder has characterized as an “ambitious business plan” is fanciful. I believe that it unlikely that the company will be able to achieve profitability within six years with additional capitalization of $370M. In addition, AMV has a remote chance of attracting any funding from institutional sources given their suboptimal financials and relying on Regulation A and Regulation CF sources for the significant capital necessary is simply untenable. In my view, the bottom line is that at this time the risk/reward tradeoff favors the bear thesis. As a result, in my opinion, the AMV (self-professed) “team of outlaws” has an uncertain future and is on the road to nowhere.

Be the first to comment