Thurtell

A Quick Take On Array Technologies

Array Technologies (NASDAQ:ARRY) reported its Q3 2022 financial results on November 8, 2022, beating revenue and EPS estimates.

The firm is a manufacturer of ground-mounting systems for large-scale solar energy projects.

Management has adjusted downward its expected adjusted earnings in 2022 and the company faces a variety of market uncertainties.

I’m on Hold for ARRY in the near term.

Array’s Overview

Albuquerque, New Mexico-based Array was founded to develop integrated ground-mounting systems, including steel supports, electric motors and electronic controllers called single-axis trackers.

BloombergNEF said that about 70% of all ground-mounted solar energy projects in the U.S. built during 2019 used tracker systems.

Management is headed by Chief Executive Officer Kevin Hostetler, who has been with the firm since April 2022 and was previously CEO of Rotork and CEO of FDH Infrastructure Services.

The company’s primary offerings include:

-

DuraTrack HZ v3 – hardware system

-

SmarTrack – machine learning module

Array Technologies’ Market & Competition

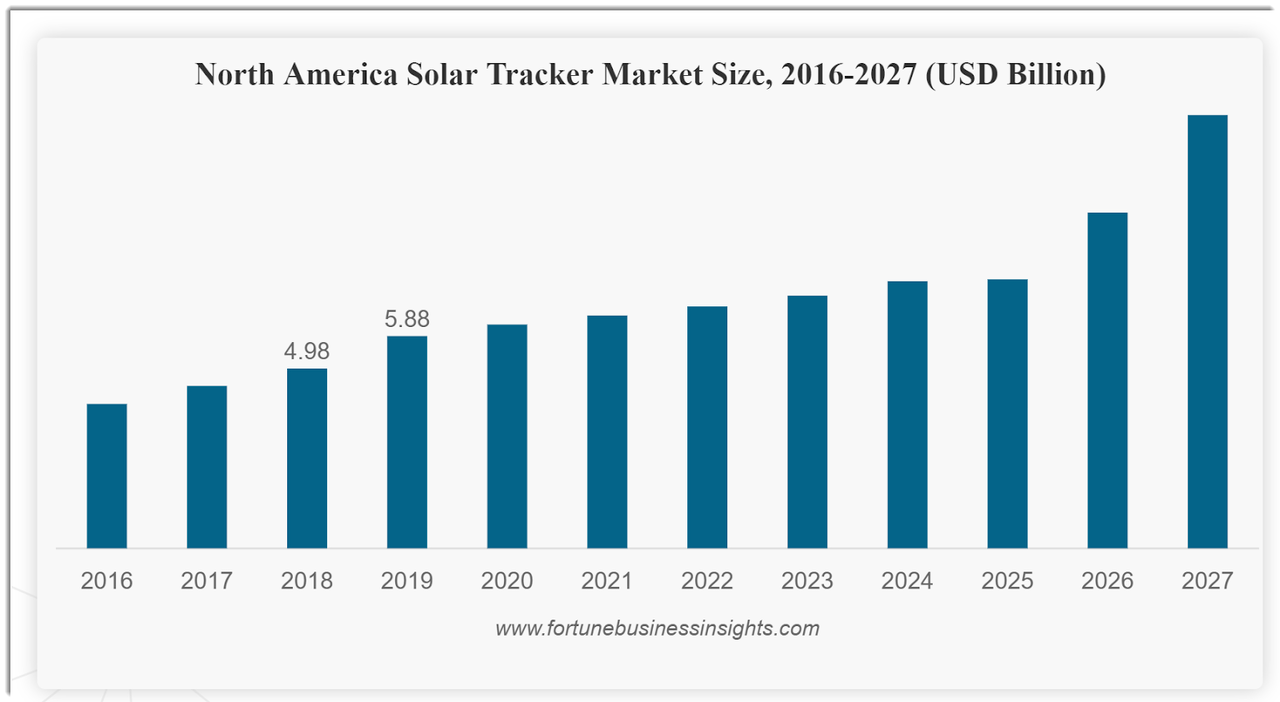

According to a 2020 market research report by Fortune Business Insights, the global market for solar trackers was an estimated $9.3 billion in 2019 and is expected to exceed $22 billion by 2027.

This represents a forecast CAGR of 12.6% from 2020 to 2027.

The main drivers for this expected growth are a continued effort by countries to reduce their carbon emissions through increasing renewable energy sources.

Also, the near term has seen a reduction in activity due to the Covid-19 pandemic’s effects on supply chains. However, below is a chart indicating the historical and projected growth rate of the solar tracker market in North America:

N. America Solar Tracker Market (Fortune Business Insights)

Major competitive or other industry participants include:

-

Nextracker

-

PV Hardware

-

Artech Solar

-

UNIRAC

-

RBI Solar

-

FTC Solar

Array Technologies’ Recent Financial Performance

-

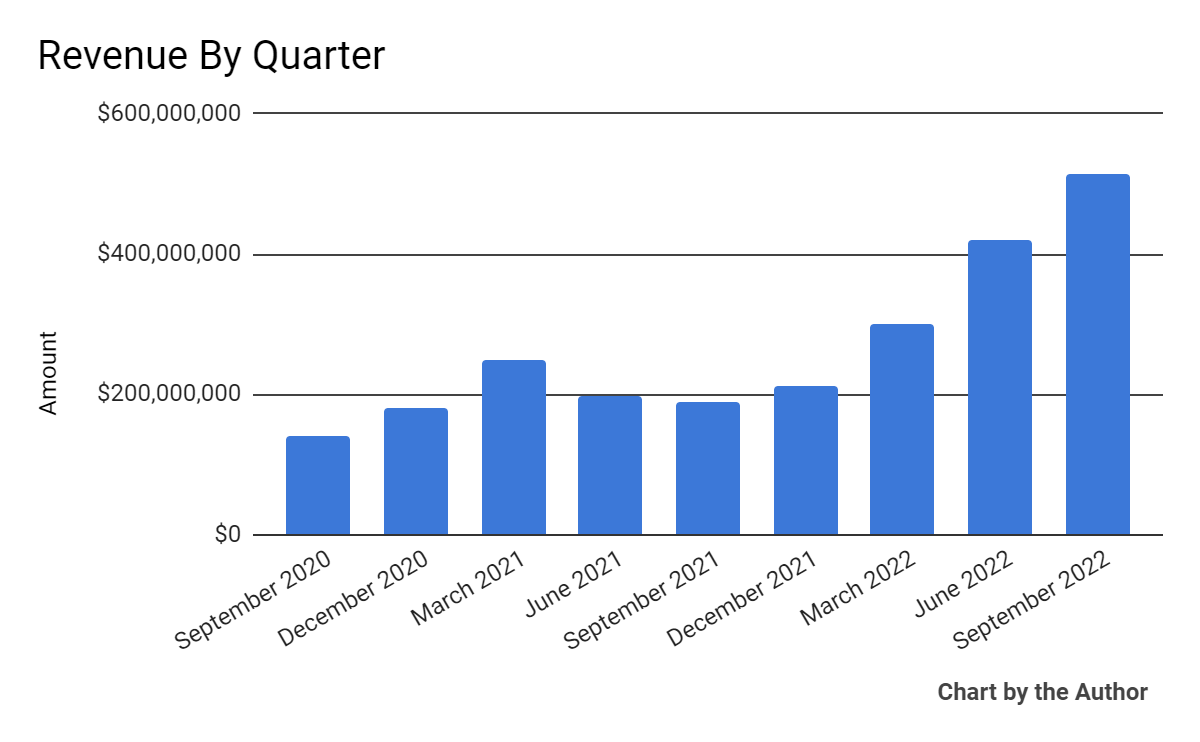

Total revenue by quarter has grown substantially in recent quarters:

Total Revenue (Seeking Alpha)

-

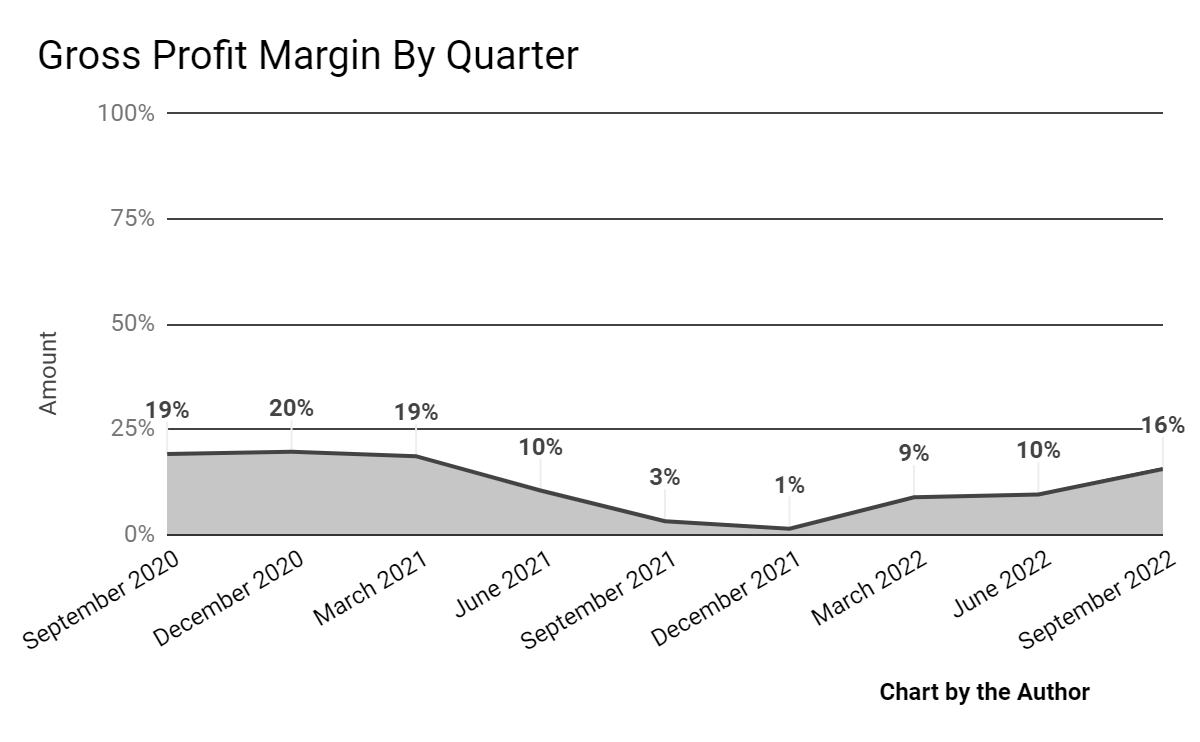

Gross profit margin by quarter has varied according to the following chart:

Gross Profit Margin (Seeking Alpha)

-

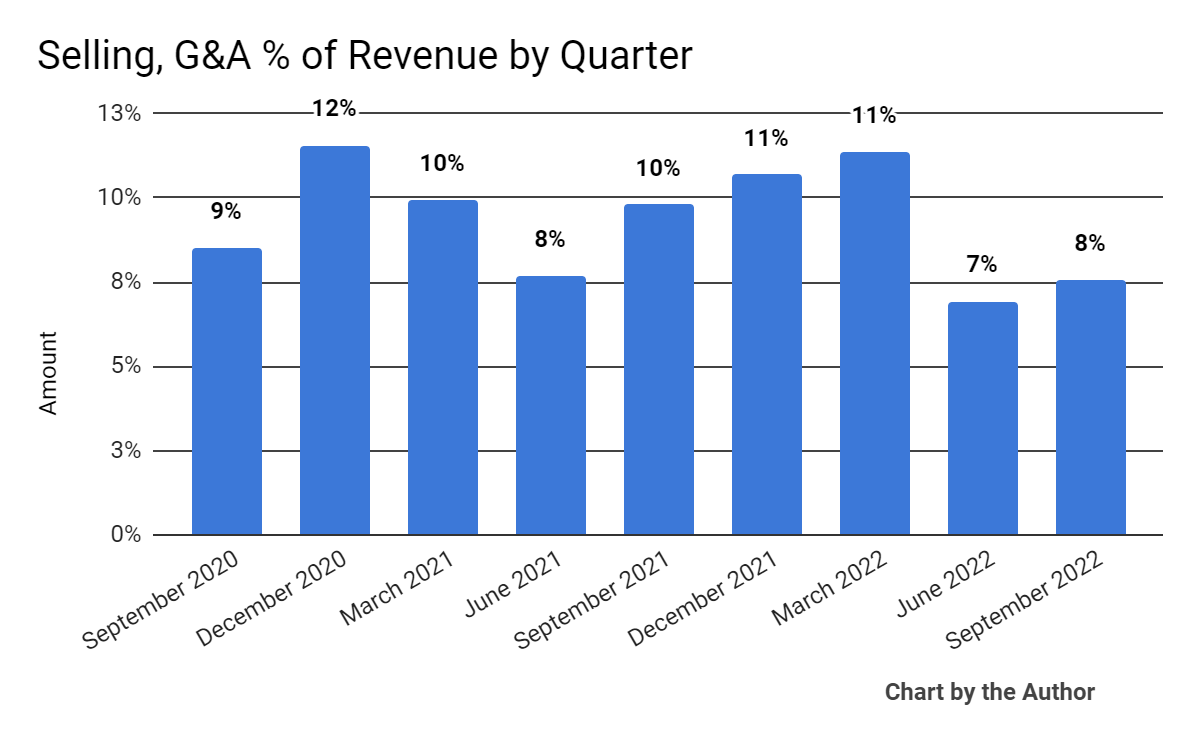

Selling, G&A expenses as a percentage of total revenue by quarter have trended lower in recent quarters:

Selling, G&A % Of Revenue (Seeking Alpha)

-

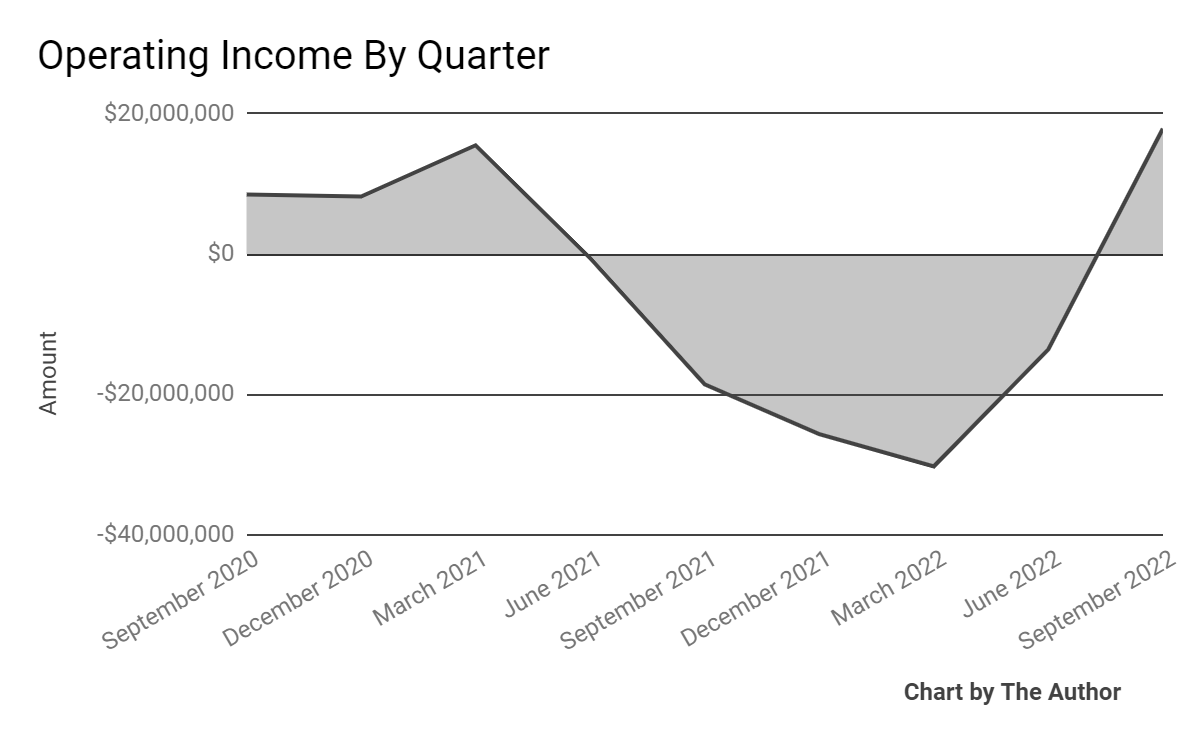

Operating income by quarter has fluctuated materially, as the chart shows below:

Operating Income (Seeking Alpha)

-

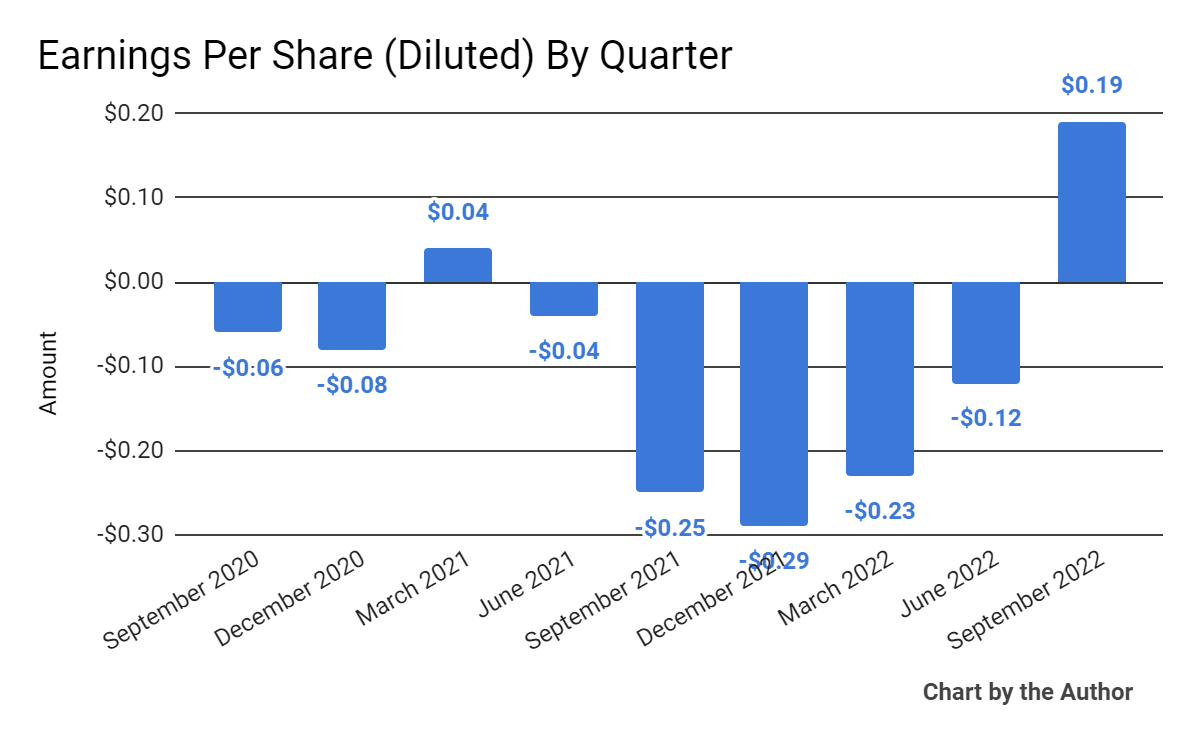

Earnings per share (Diluted) has turned positive in Q3 2022:

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

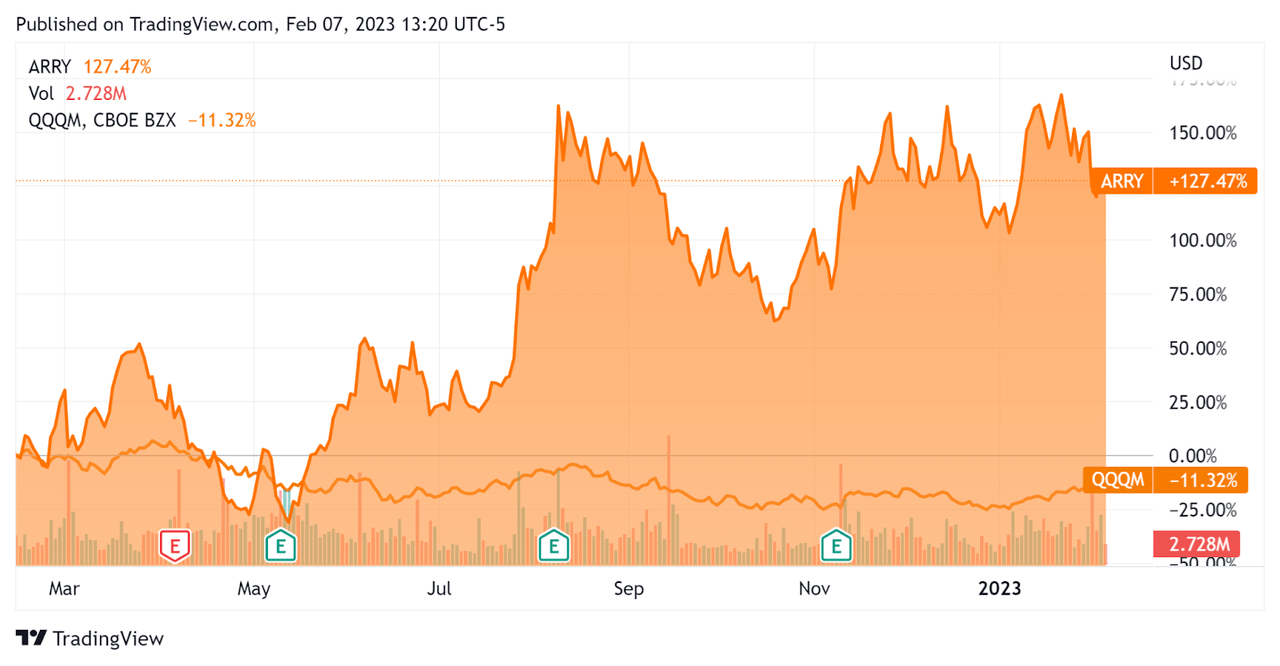

In the past 12 months, ARRY’s stock price has risen 127.47% vs. that of the QQQM Nasdaq 100 Index’s drop of 11.3%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Array Technologies

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

2.7 |

|

Enterprise Value / EBITDA |

119.5 |

|

Price / Sales |

2.0 |

|

Revenue Growth Rate |

78.8% |

|

Net Income Margin |

-0.6% |

|

GAAP EBITDA % |

2.3% |

|

Market Capitalization |

$2,976,702,460 |

|

Enterprise Value |

$3,988,374,530 |

|

Operating Cash Flow |

-$53,327,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.45 |

(Source – Seeking Alpha)

As a reference, a relevant partial public comparable would be FTC Solar (FTCI); shown below is a comparison of their primary valuation metrics:

|

Metric [TTM] |

FTC Solar |

Array Technologies, Inc. |

Variance |

|

Enterprise Value / Sales |

1.3 |

2.7 |

117.5% |

|

Revenue Growth Rate |

-6.8% |

78.8% |

–% |

|

Net Income Margin |

-51.9% |

-0.6% |

-98.9% |

|

Operating Cash Flow |

-$89,530,000 |

-$53,327,000 |

-40.4% |

(Source – Seeking Alpha)

Commentary On Array Technologies

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted the ‘dynamic landscape’ of the U.S. domestic market.

Leadership expects the company will benefit materially from the passage of the Inflation Reduction Act in 2022, but cautioned that the effects from the bill’s provisions will be a long-time in coming as ‘there is still a lot of work that needs to be done by the various governmental agencies tasked with rolling it out to define and clarify critical aspects of the bill before the industry can wholesale shift to the new paradigm.’

As to its financial results, Q3 revenue rose 12% year-over-year on an organic basis, while the firm’s order book ended the quarter at $1.8 billion, an increase of 77% year-over-year.

Gross margin continued its trend higher during the quarter, while adjusted EBITDA increased sharply year-over-year. Note that ‘adjusted’ usually excludes stock-based compensation.

Earnings per share rose sharply into positive territory at $0.19 for the quarter.

For the balance sheet, the firm finished the quarter with cash and equivalents of $62.8 million and total debt of $768.5 million.

Over the trailing twelve months, free cash used was $61.1 million, of which capital expenditures accounted for $7.8 million. The company paid $13.7 million in stock-based compensation in the last four quarters.

Looking ahead, management ‘modestly’ updated its full-year 2022 guidance, with expected revenue of $1.55 billion at the midpoint of the range and adjusted EBITDA of $127 million at the midpoint.

Regarding valuation, the market is valuing ARRY at far higher multiples than faltering FTC solar.

But, a problem ARRY now faces is the recently reported ban on certain solar panel technologies by the Chinese government, which could potentially hamper the firm’s future growth by reducing solar panel availability among its customers.

A potential upside catalyst to the stock could include reduced forex headwinds as well as faster implementation of the IRA.

While ARRY has performed extremely well over the past 12-month period, the company faces a potentially more challenging near-term picture due to various market uncertainties.

As a result, management has prudently adjusted downward its full-year adjusted earnings per share expectations.

Given that outlook, I’m on Hold for ARRY in the near term.

Be the first to comment