ipopba

Anavex Life Sciences (NASDAQ:AVXL) has been on my radar’s periphery over the past year or so due to the company’s potential blockbuster Alzheimer’s candidate, ANAVEX 2-73. I avoided moving the ticker higher up on my watch list until the company reports the complete data set from ANAVEX 2-73. However, the company’s Q1 2023 earnings report revealed a nice beat on EPS and a robust cash position. In addition, the company publicized that they “plan to submit the data for publication and peer-reviewed medical journal in the near term,” which appeared to trigger a buying frenzy with AVXL hitting its “highest level since early December.” I am not one to buy into the hype, but ANAVEX 2-73’s data looks promising and should hold up against Biogen’s (BIIB) and Eisai’s (OTCPK:ESALY) (OTCPK:ESALF) Leqembi. Therefore, we could be looking at a potential blockbuster drug in the coming years. Seeing that AVXL’s market cap is under $1B, I think the ticker is a prime candidate for the Compounding Healthcare “Bio Boom” Portfolio and should be near the top of my watch list.

I intend to provide a brief background on Anavex and ANAVEX 2-73. In addition, I discuss why AVXL is a prime Bio Boom candidate. Furthermore, I point out a few downside risks that investors need to be aware of. Finally, I reveal my plans for initiating a starter position in the near term.

Background on Anavex Life Sciences

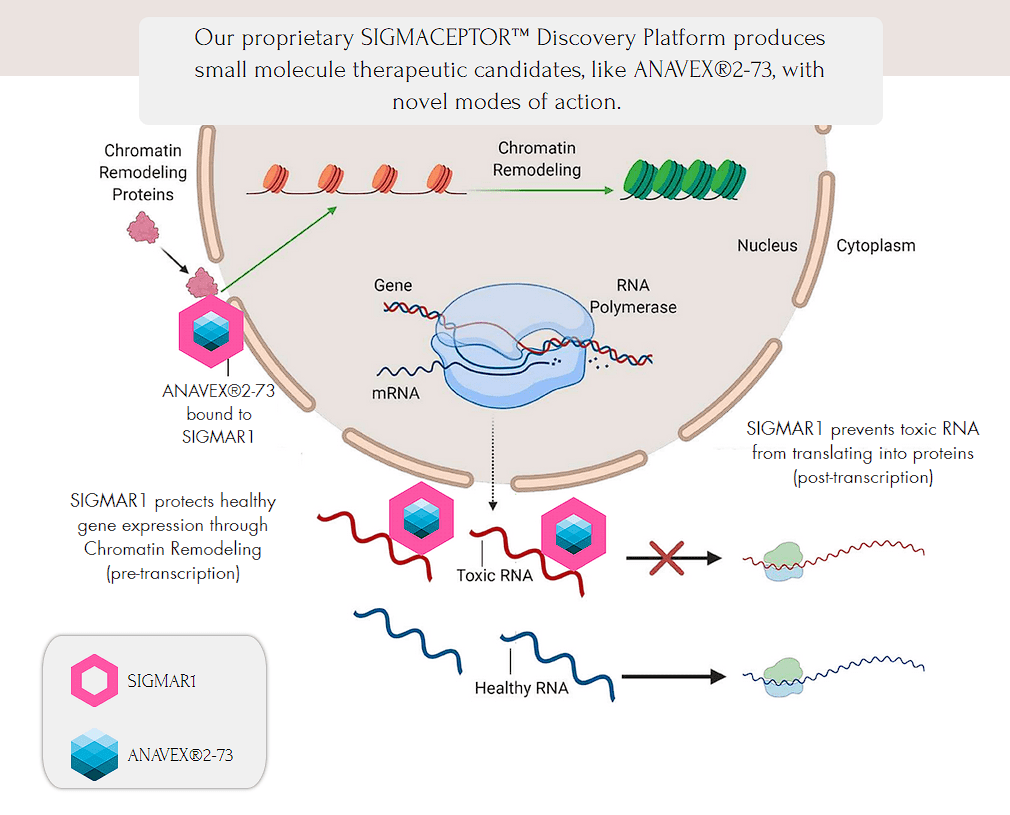

Anavex Life Sciences develops novel small-molecule treatments for CNS diseases, including Alzheimer’s, Parkinson’s, Rett syndrome, and other rare diseases. The company is taking aim at the upstream Sigma-1 receptor “SIGMAR1”, using their “SIGMACEPTOR” platform, which has the ability to have the patient’s own immune system to combat some of the worst CNS conditions. This is achieved by using one of the company’s SIGMAR1 agonists, which activates SIGMAR1, thus, reducing cellular stress around RNA gene transcription. Looking at the figure below, we can see how ANAVEX 2-73 can help promote healthy gene expression, and also help prevent toxic RNA from translating into proteins.

Anavex SIGMACEPTOR Platform (Anavex)

SIGMAR1 is essential to neuronal homeostasis due to its participation in moderating glutamate levels, preserving endoplasmic reticulum function, and regulating calcium. By activating SIGMAR1, the body can perform neurogenesis, diminish reactive oxygen species accumulation, subdue neuro-inflammation, and amends Aβ toxicity. Moreover, SIGMAR1 also stimulates autophagy that degrades amyloid-beta precursor proteins, in so doing regulating Aβ production.

ANAVEX has decided to take advantage of the sigma receptor’s ability to be a viable target for an assortment of CNS conditions and has generated several pipeline candidates that are addressing some of the worst neurological diseases.

ANAVEX 2-73 Pipeline (Anavex)

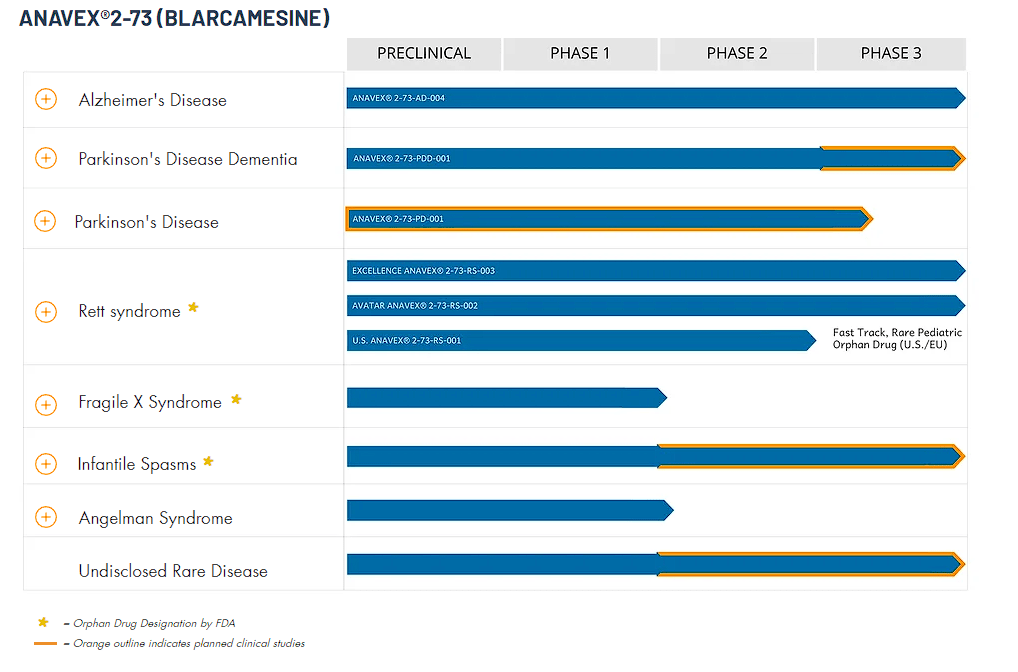

The company’s pipeline includes ANAVEX 2-73 a SIGMAR1 agonist in an oral once-daily drug currently targeting several indications including neurodegenerative such as Alzheimer’s, as well as neurodevelopmental diseases, such as Rett syndrome.

So far, ANAVEX 2-73 has performed well in pre-clinical work that supports ANAVEX 2-73 as a platform drug for Alzheimer’s disease, Parkinson’s disease, Rett syndrome, as well as epilepsy, infantile spasms, Fragile X syndrome, Angelman syndrome, MS and tuberous sclerosis complex “TSC”. Of note, ANAVEX 2-73 showed encouraging data in mouse models for Rett syndrome. For Parkinson’s, their Phase II proof-of-concept trial produced statistically significant improvements in the CDR computerized assessment system analysis to demonstrate its ability to help cognitive performance. As a result, the drug received several FDA and EMA designations including fast track and rare pediatric orphan drug, which help expedite the regulatory process and provide market exclusivity.

In Alzheimer’s disease, ANAVEX 2-73 is moving closer and closer to a potential approval thanks to strong clinical data that hit co-primary and key secondary endpoints for patients with early Alzheimer’s disease in their AD-004 Phase IIb/III trial.

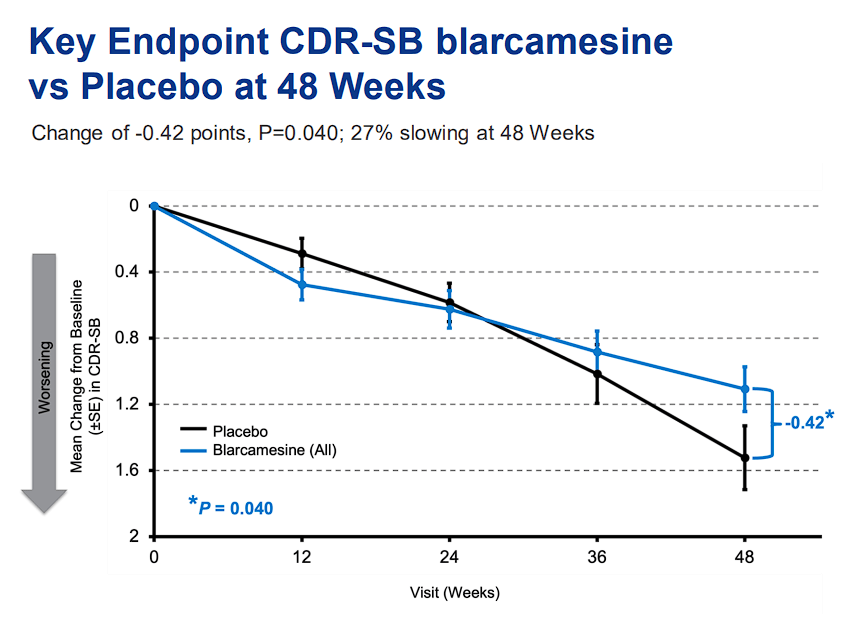

ANAVEX 2-73 vs Placebo in CDR-SB Test “Clinical Dementia Rating” (Anavex)

The data showed that ANAVEX 2-73 slowed the decline of cognition and function in patients with early Alzheimer’s disease over 48 weeks with patients showing 84% more likely to improve cognitively over placebo. In addition, patients who were administered ANAVEX 2-73 were 167% more likely to improve function over placebo, and reduced clinical decline of cognition and function by 27%. In terms of safety, ANAVEX 2-73 was generally safe and well tolerated.

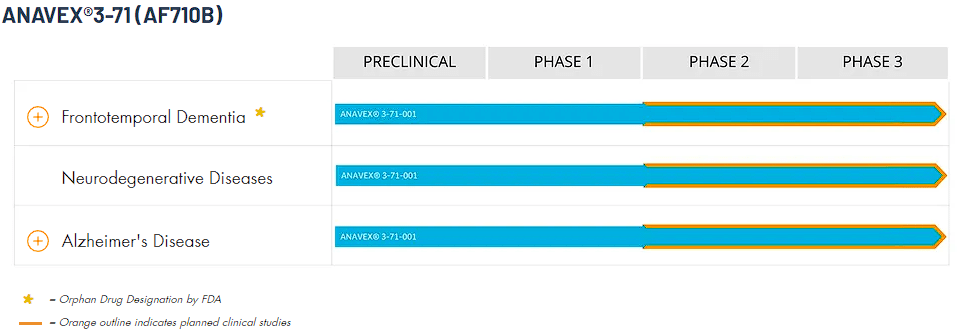

ANAVEX 3-71 is another SIGMAR1 activation drug, however, it has a unique mechanism of action due to its ability of M1 muscarinic allosteric modulation, which is expected to boost neuroprotection and cognition in Alzheimer’s disease patients. The company believes ANAVEX 3-71 will be operative in very small doses in protein-aggregation-related disease by combating cognitive deficits, amyloid and tau pathologies, and mitochondrial irregularities, as well as improving inflammation. The company’s initial Phase I trial of ANAVEX 3-71 hit its primary and secondary endpoints of safety, with no serious adverse events or dose-limiting toxicities being reported. The company is looking to pit ANAVEX 3-71 up against schizophrenia, FTD, and Alzheimer’s disease in respective registration trials.

ANAVEX 3-71 Pipeline (Anavex)

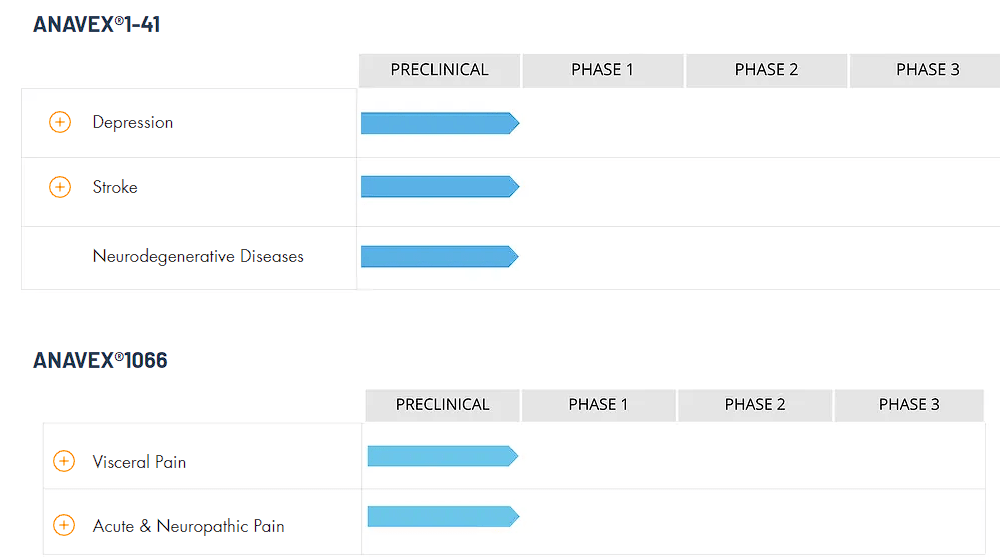

ANAVEX 1-41 is a sigma-1 agonist that has performed well in pre-clinical tests displaying the potential to safeguard nerve cells from degeneration or death. In addition, ANAVEX 1-41 was able to inhibit the expression of caspase-3, thus, helping reduce the apoptosis of cells in the hippocampus, which is linked to the pathogenesis of neurodegenerative and neurodevelopmental diseases as well as depression and stroke.

Anavex Preclinical Pipeline (Anavex)

ANAVEX 1066 is a sigma-1/sigma-2 ligand that is intended for the treatment of neuropathic and visceral pain. ANAVEX 1066’s pre-clinical work showed its ability to address pain at a rapid rate and remained substantial for two hours.

The company’s other pipeline candidate is ANAVEX 1037 for the treatment of prostate and pancreatic cancer. ANAVEX 1037 is believed to have a high affinity for SIGMAR1 and an adequate affinity for sigma-2 receptors as well as sodium channels. ANAVEX 1037’s pre-clinical studies revealed antitumor prospects to discriminately induce selective apoptosis of cancer cells without disturbing healthy cells and possibly inhibit metastasis, reduce angiogenesis, and thwart tumor cell proliferation.

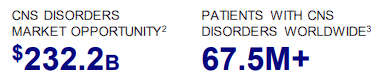

If all goes well, the company will be the trailblazer in SIGMAR1 therapeutics and a leader in CNS treatments to address the 67.5M+ patients with CNS disorders that generate a roughly $232.2B market opportunity.

Anavex CNS Disorder Market Opportunity (Anavex)

In terms of cash, Anavex reported they finished their Q1 with ~$143.6M in cash and equivalents, which they believe is adequate to fund operations and clinical programs beyond the next four years.

Bio Boom Candidate

The Bio Boom Portfolio comprises healthcare companies that are typically not profitable and are very speculative, however, they present considerable upside because of a potent impending catalyst, estimated revenue growth, or a potential turnaround. Usually, these are small to mid-cap companies with volatile tickers that will permit frequent trading opportunities to help generate considerable profit while growing a “house money” position over time. These tickers are traded provided they are still in play or until the company graduates to the “Bioreactor” growth portfolio.

I believe AVXL does have a number of Bio Boom features that indicate outstanding upside potential from these current prices. First and foremost, I believe AVXL is trading at a markdown for its projected revenues. The company is looking to enter a massive market with incredible growth potential in the coming years and decades.

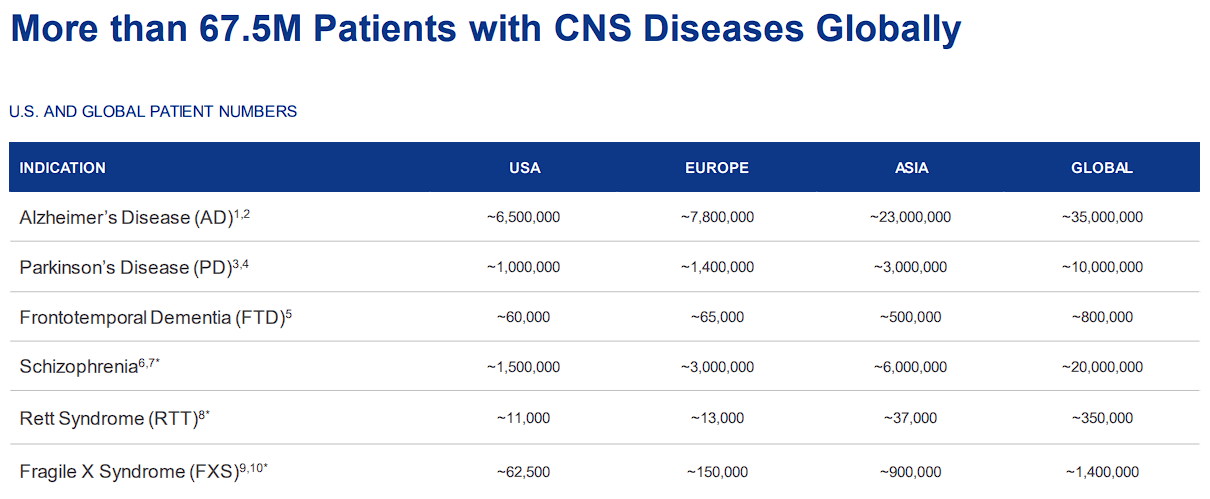

Anavex CNS Disorders Approximate Patient Populations (Anavex) Anavex CNS Market Growth Estimates (Anavex)

So, the company should report incredible growth even if they only get one of their candidates on the market.

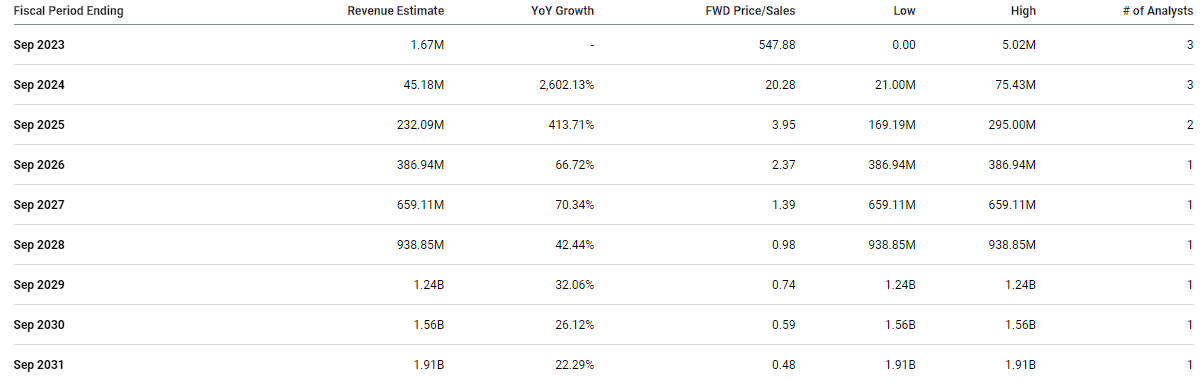

In fact, the Street expects Anavex to report significant revenue starting in 2024 and will experience strong double-digit and even triple-digit growth for the remainder of the decade and clear $1.5B in 2029.

Anavex Analyst Annual Revenue Estimates (Seeking Alpha)

AVXL’s market cap is about $916M, so that would be approximately 0.59x forward price-to-sales. Considering the industry’s average price-to-sales is 4x-5x, we can say AVXL is trading at a discount for its forward revenue estimates. If AVXL was to be priced in line with its peers, we could see the shares trading around $77 per share in several years. Surely, the company will almost certainly have to complete some method of dilution, and we don’t know if Anavex will ever hit these projections. Still, these figures do show AVXL’s upside potential, which is a vital characteristic of a Bio Boom ticker.

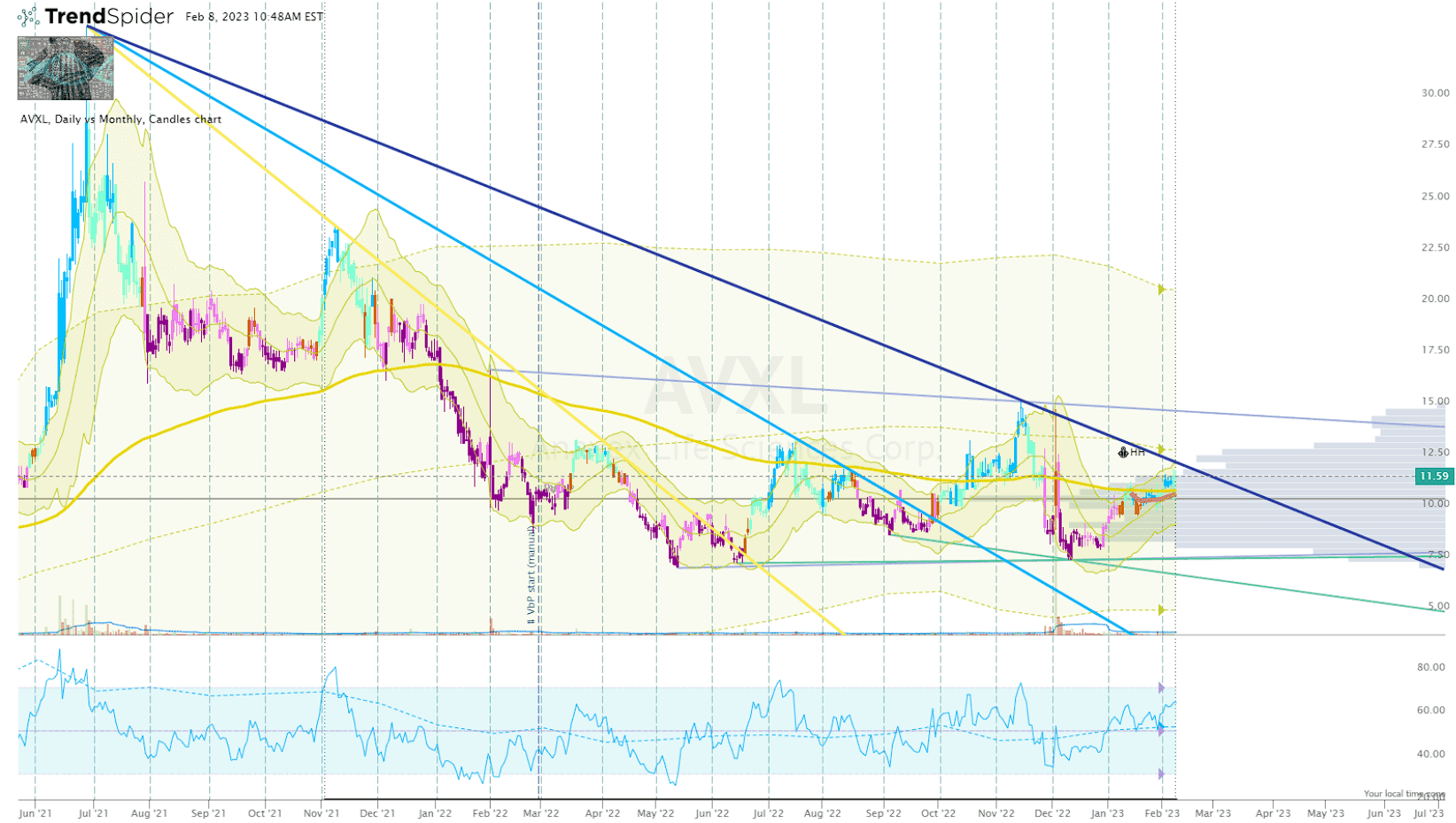

Another characteristic to contemplate is the ticker’s indecisive state on account of the market-wide sell-off and investors waiting for additional data. AVXL has been trading in a choppy manner for almost a year after an eight-month nose-dive from its high in the middle of 2021. The choppy trading does smooth out to form a nice base and a double-bottom to set up a potential reversal move in the coming months.

AVXL Daily Chart (Trendspider)

The share price is approaching another downtrend ray from its all-time high, which could be the last big hurdle before a potential breakout move to get above $15 per share. This could provide an opportunity to book significant profit and move the position to a “house money” status.

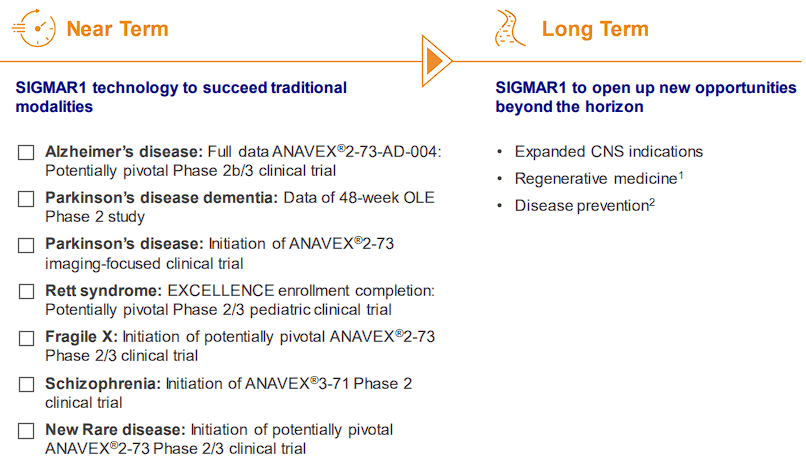

In addition, to the valuations and technical analysis, AVXL also has near-term and long-term catalysts that can help showcase Anavex’s intriguing platform technology and impressive pipeline.

Anavex Near-Term and Long-Term Catalysts/Opportunities (Anavex)

Looking at the figure above, we can see that Anavex will be able to showcase their ability to treat a plethora of CNS indications and have several programs moving toward commercialization in the near future.

The additional data from their placebo-controlled Phase IIb/III Alzheimer’s disease trial should provide us with more biomarkers and endpoints. Most notably, the company is expected to report some data from MRIs of the brain, which is a very important marker showing brain atrophy. In addition, we will see some other key measurements such as quality of life, sleep quality, and other behavioral measures, which are correlated with Alzheimer’s pathology. The company expects to “try to do this as soon as possible because we want to share that also with the agencies in the FDA in Europe,” but they did not provide guidance on a timeline in the conference call. The company should have the data to approach the FDA to determine their course of action, and hopefully, provide investors with a rough timeline for possible approval.

Will ANAVEX 2-73 be approved?

Well, Leqembi received accelerated approval centered on its amyloid-clearing ability, despite some significant safety after 3 deaths have been reported that may be associated with the drug. Meanwhile, ANAVEX 2-73 throttled cognitive decline by 45% with an ADAS-Cog score of 28.75, vs Leqembi’s score of 24.45. In addition, ANAVEX 2-73 had superior efficacy at 48 weeks in patients who were in more advanced stages of the disease. Indeed, we don’t know for certain if ANAVEX 2-73 will be approved, but the current data suggests it is very likely.

In addition to Alzheimer’s, Anavex expects to provide updates on the Parkinson’s dementia program and data from the Rett syndrome study. Obviously, any positive updates on these programs should validate the company’s platform and have a dramatic impact on the share price.

These catalysts could have a positive impact on the share price as investors appreciate the earnings potential as well as the company’s expertise in a certain area of medicine with a unique platform, a broad pipeline, and a robust cash position do indicate Anavex has solid long-term prospects and perhaps arise as an acquisition target.

Essentially, AVXL has the components to be a budding multi-bagger in the future… a select Bio Boom candidate.

Downside Risk

The obvious downside risks come from regulatory decisions and competition. Although I am bullish on the company’s chances with regulators, it is possible that ANAVEX 2-73 needs additional data before getting the green light. Obviously, this would be a major setback and the share price would be punished for a prolonged period of time. The other concern is competition, which is currently Biogen’s and Eisai’s Leqembi. Indeed, the current data does favor ANAVEX 2-73, but the trial is not a head-to-head study and the trial design is not identical. Most notably, Leqembi’s trial extension kept patients on for 18 months and was able to sustain its ability to slow impairment. ANAVEX 2-73’s trial ended at 48 weeks, so it is possible that Leqembi’s long-term data outperforms ANAVEX 2-73’s long-term data.

Yes, I am aware that ANAVEX 2-73 appears to be more effective and safer than Leqembi at this time. But, the concern is the potential scenario that the full data does not put the argument to rest, and leaves investors with some doubt about the FDA and ANAVEX 2-73’s commercial success. I suspect the market is going to attempt to toy with AVXL, and any sort of doubt could bring an onslaught of selling pressure.

As a result, I am giving AVXL a conviction level of 3 out of 5 at this time.

My Plan

AVXL is currently trading at around $11 per share, which is fairly cheap considering the company’s upside prospects. So, I plan on initiating a small position in the immediate term and will look to grow that position ahead of a potential data publication. My goal is to book some profits at my Sell Targets on a spike in the share price, and perhaps transition my AVXL position into a “house money” state for a long-term investment. This way I will have exposure to AVXL’s upside potential, but the original investment has been removed leaving only profits left on the table.

Be the first to comment