American Tower (NYSE:AMT) is a buy for the dividend growth investor and total return investor. American Tower is one of the largest providers of wireless communications services and is a growth investment that should be in all tech portfolios because of the expanding demand for 5G wireless streaming capability. The quarterly dividend was just increased to $1.08/Qtr. or a 6.8% increase. That’s 31 quarterly increases in a row. Buy the correction you shall (Master Yoda).

{kind=link}

Source: AMT website

I use a set of guidelines that I codified over the last few years to review the companies in The Good Business Portfolio (my portfolio) and other companies that I am considering. For a complete set of guidelines, please see my article “The Good Business Portfolio: Update to Guidelines, August 2018“. These guidelines provide me with a balanced portfolio of income, defensive, total return, and growing companies that hopefully keeps me ahead of the Dow average.

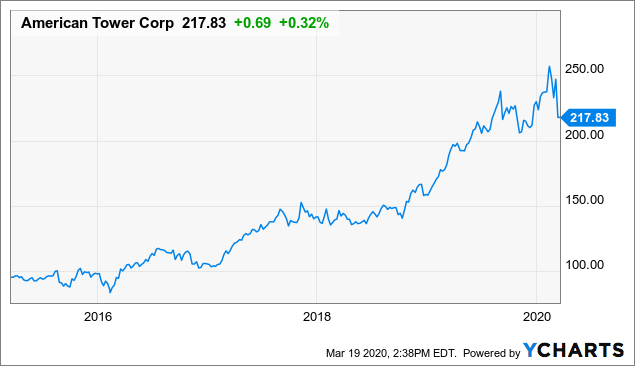

When I scanned the five-year chart, American Tower has a good chart going up and to the right in a steady, strong slope for four of the five years with a small pause in 2015 when the market was a bit negative. Recently, the AMT price has gone down with the market correction but not as much as the market. This correction creates a buying opportunity for a great growing business at a discount price.

Data by YCharts

Data by YCharts

American Tower is being reviewed in the following topics below.

- The Good Business Portfolio Fundamentals

- Company Business

- Conclusions

- Portfolio Management Highlights

Good Business Portfolio Fundamentals

The Good Business Portfolio Guidelines are just a screen to start with and not absolute rules. When I look at a company, the total return is a crucial parameter to see if it fits the objective of the Good Business Portfolio. My total return guideline is that total return must be greater than the Dow’s total return over my test period. American Tower beats against the Dow baseline in my 51-month test compared to the Dow average. I chose the 51-month test period (starting January 1, 2016, and ending to date) because it includes the great year of 2017 and 2019, and other years that had a fair and bad performance. The great American Tower total return of 170.34% compared to the Dow base of 29.20% makes American Tower a great investment for the total return investor that also wants some increasing income. Looking back five years, $10,000 invested five years ago would now be worth over $28,000 today. This gain makes American Tower an excellent investment for the total return investor looking back, which has future growth as the United States and worldwide economies need more of the company’s communications services as the streaming of content continues to grow.

Dow’s 51-Month total return baseline is 29.20%

|

American Tower does meet my dividend guideline of having dividends increase for 8 of the last ten years and having a minimum of 1% yield. American Tower has a below-average dividend yield of 1.8% and has had increases for eight years, making American Tower the right choice for the dividend growth investor. The dividend was last increased in March 2020 for an increase from $1.01/Qtr to $1.08/Qtr or a 6.8% increase. The five-year average payout ratio is moderate, at 53%. After paying the dividend, this leaves cash remaining for increasing the business of the company by developing new additions to the company’s services and adding bolt-on companies like Eaton Towers in Africa.

I also require the CAGR going forward to be able to cover my yearly expenses and my RMD with a CAGR of 7%. My dividends provide 3.3% of the portfolio as income, and I need 1.9% more for a yearly distribution of 5.2%, plus an inflation cushion of 1.8%. The three-year forward S&P CFRA CAGR of 10% exceeds my guideline requirement. This tremendous future growth for American Tower can continue its uptrend benefiting from the continued strong growth in the United States and worldwide streaming capability but may be mitigated by the coronavirus short term.

I have a capitalization guideline where the capitalization must be greater than $10 Billion. American Tower passes this guideline. American Tower is a large-cap company with a capitalization of $106 billion. American Tower 2020 projected cash flow at $1500 million is good, allowing the company to have the means for company growth each year. Companies like American Tower have the cash and ability to buy other smaller companies and weather any storms that might come along.

One of my guidelines is that the S&P rating must be three stars or better. American Tower S&P CFRA rating is three stars or hold with a target price of $240, passing the guideline. American Tower’s price is below this target by 15%. American Tower is below the target price at present and has a high forward PE of 27, making American Tower a good buy at this entry point. Considering the potential growth and stability of the company, if you are a long-term investor that wants good increasing future total return growth, you may want to look at this company. Take advantage of the correction and buy a good business at a nice discount.

One of my guidelines is would I buy the whole company if I could. The answer is yes. The total return is secure, and the below-average dividend yearly yield has grown at a high rate over the past five years, making American Tower a great business to own for the growth and the long-term income investor. The Good Business Portfolio likes to embrace all kinds of investment styles but concentrates on buying companies that can be understood, makes a fair profit, invests profits back into the business, and also generates a good income stream. Most of all, what makes American Tower interesting is the increasing long-term demand for streaming capability.

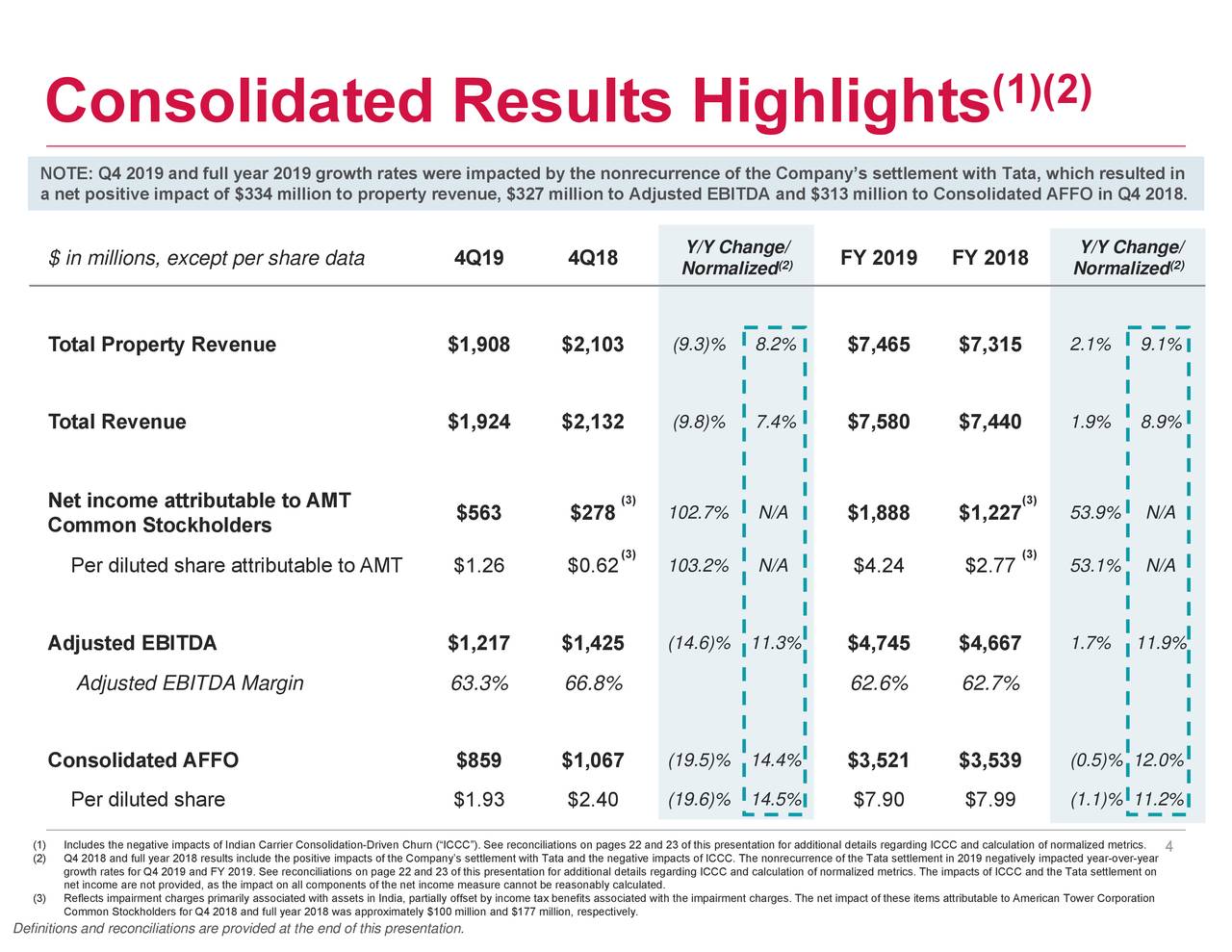

I don’t have a guideline for earnings but look for the earnings of my positions too consistently beat their quarterly estimates. For the last quarter on February 25, 2020, American Tower reported earnings that beat expected by $0.03 at $1.93, compared to last year at $0.62. Total revenue was lower at $1.92 billion less than a year ago by 9.4% year over year and was in line with expected total revenue. This was a mixed report with bottom-line beating expected and the top line decreasing with a decrease compared to last year. The next earnings report will be out April 2020 and is expected to be $2.09 compared to last year at $1.73 a strong increase. The graphic below shows more details on the comparisons between 2018 and 2019.

Source: AMT earnings call slides

Company Business

American Tower is one of the largest developers and providers of wireless communications services in the United States and foreign countries.

As per data from Reuters

American Tower operates as a real estate investment trust (REIT), which owns, operates, and develops multi-tenant communications real estate. ATC’s segments include U.S. property, Asia property, EMEA property, Latin America property, Services, and Other. Its primary business is property operations, which include the leasing of space on communications sites to wireless service providers, radio and television broadcast companies, wireless data providers, government agencies and municipalities, and tenants in various other industries. Its U.S. property segment includes operations in the United States. Its Asia property segment includes operations in India. The EMEA property segment includes operations in Germany, Ghana, Nigeria, South Africa, and Uganda. The Latin America property segment includes operations in Brazil, Chile, Colombia, Costa Rica, Mexico, and Peru. Its services segment offers tower-related services in the United States.

Overall, American Tower is a great business with a 10% S&P CFRA CAGR projected growth as the worldwide economy grows going forward with the increasing need for more streaming capability. I feel this growth rate will be at least 10% because of the 5G implementation. The good earnings and revenue growth provide AMT the capability to continue its growth as the business increases by buying bolt companies like Eaton Towers in Africa and investing in 5G expansion.

From the 4th quarter’s earnings call are a few highlights that show the great growth and opportunities that are the future of American Tower.

- They expect the T-Mobile (NASDAQ:TMUS) and Sprint (NYSE:S) merger to be net neutral to net positive for the company over the mid to long term with the accelerated nationwide 5G coverage requirements associated with this transaction will drive further demand for tower space.

- DISH’s (NASDAQ:DISH) commitment to building a new full nationwide network will add to growth.

- T-Mobile and DISH will help speed the deployment of fast, efficient 5G broadband service to consumers

- They invested around $100 million in green energy solutions, such as advanced batteries, solar installations, and other initiatives, primarily in our African and Indian markets as part of our commitment to reducing fossil fuel usage.

- They expect to continue to make meaningful investments in clean energy and fuel innovation this year, concentrated mainly in India and Africa.

- They constructed a record of more than 4,500 sites in 2019, and we expect to exceed that by around an additional 2,000 sites in 2020.

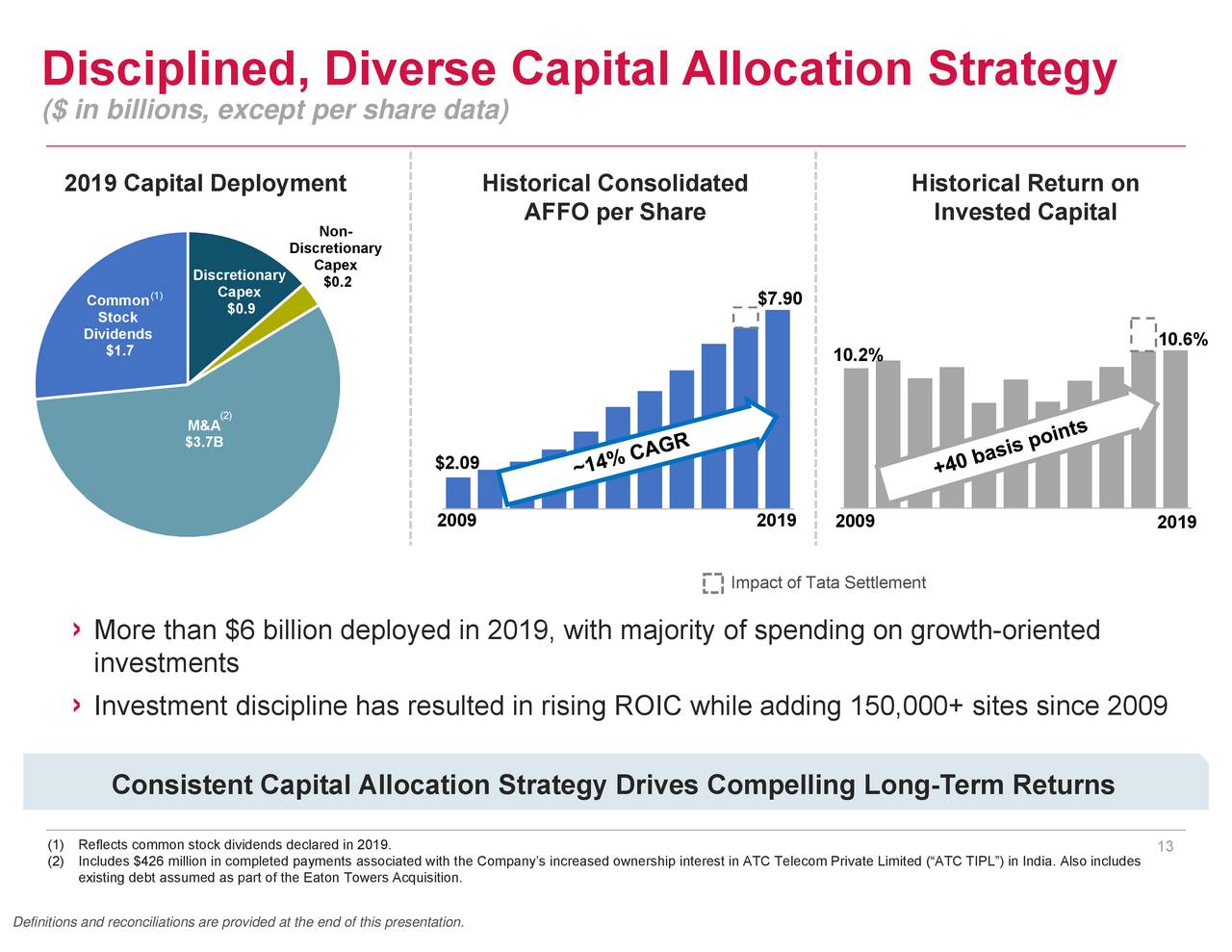

This shows the growth in the 4th quarter that can continue going forward with an increase in top and bottom lines. American Tower has good growth and will continue as the United States population grows with the need for more integrated streaming and phone communications. The growth is being driven by the 5G implementation, which may be balanced by a slowing economy because of the coronavirus. The graphic below shows CAGR from the last major correction in 2009, which may be repeated after this correction turns around.

Source: AMT earnings call slides

Conclusions

American Tower is a good investment choice for the dividend growth investor with its slightly below-average dividend yield but with good dividend growth and a great choice for the total return investor. American Tower is 1.22% of The Good Business Portfolio, and the position will be increased whenever cash is available. If you want a growing dividend income and good total return in the growing computer streaming business, AMT may be the right investment for you.

Portfolio Management Highlights

The five companies comprising the largest percentage of the portfolio are Johnson & Johnson (NYSE:JNJ) at 9.3% of the portfolio, the Eaton Vance Enhanced Equity Income Fund II (NYSE:EOS) at 7.8% of the portfolio, Home Depot (NYSE:HD) at 10.3% of the portfolio, Omega Healthcare Investors (NYSE:OHI) at 9.0% of the portfolio, and Boeing (NYSE:BA) at 7.0% of the portfolio. Therefore, BA, EOS, JNJ, OHI, and HD are now in trim or close to trim position, but I am letting them run a bit since they are great companies.

- On February 4, I trimmed HD to 9% of the portfolio. HD is a great business but needs more foreign expansion to grow even stronger.

- On January 13, I trimmed Danaher (NYSE:DHR) to 1.5% of the portfolio. I like DHR long term, but the next year’s earnings look a bit weak, and I need cash for my RMD.

- On December 5, I wrote covered calls against my Danaher position to collect another premium ($1.54/share December $150). I like DHR, but it’s getting a bit pricey, and the covered calls give me some extra income and some downside protection. On December 19, I closed the position by buying back the calls and made a small profit.

Boeing is going to be pressed to 10% of the portfolio because of it being cash positive on 787 deferred plane costs at $1.3 billion in the third quarter of 2019, an increase from the second quarter. Boeing has dropped in the last ten months because of the second 737 MAX crash, and I look at this as an opportunity to buy BA at a reasonable price. From the latest news on Boeing is a rumor that Warren Buffett is taking a position on BA, maybe he knows a good investment. It now looks like the 737 MAX will not be approved until mid-year, but the FAA has said it could be earlier because Boeing is making good progress, all will depend on the first test flight with the FAA.

JNJ will be pressed to 9% of the portfolio because of its defensive nature in this post-BREXIT world. Earnings in the last quarter beat on the top and bottom line, and Mr. Market did nothing. JNJ in April 2019 increased the dividend to $0.95/Qtr., which is 57 years in a row of increases. JNJ is not a trading stock but a hold forever; it is now a strong buy as the healthcare sector remains under pressure.

The total return for the Good Business Portfolio is ahead of the Dow average from 1/1/2020 to March 13 by 0.7%, which is a small gain above the market loss of 18.8% for the portfolio with BA a strong drag. Each quarter after the earnings season, I write an article giving a complete portfolio list and performance, the latest article is titled ” The Good Business Portfolio: 2019 4th Quarter Earnings and Performance Review“. Become a real-time follower, and you will get each quarter’s performance after the next earnings season is over.

Disclosure: I am/we are long BA, JNJ, HD, EOS, DHR, MO, DIS, V, OHI, TXN, AMT. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Of course, this is not a recommendation to buy or sell, and you should always do your own research and talk to your financial advisor before any purchase or sale. This is how I manage my IRA retirement account, and the opinions of the companies are my own.

Be the first to comment