piranka

Investment Thesis: In spite of continued improvements in churn and ARPU rates, I take the view that the stock could see limited upside on a short to medium-term basis.

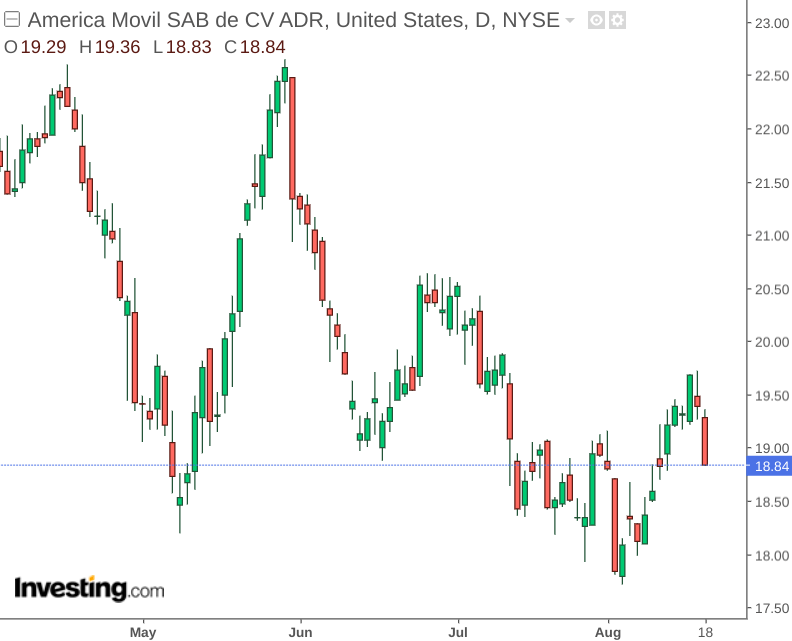

In a previous article back in May, I made the argument that while America Movil (NYSE:AMX) has shown strong performance to date – the stock could see some pressure going forward as a result of intensifying competition across the 5G space as well as a weakening of the Mexican peso relative to the dollar.

Since then, the stock has seen significant downside:

Investing.com

The purpose of this article is to assess whether America Movil could see renewed upside from here – particularly taking recent performance into account. Please note that figures cited from America Movil’s financial reports are provided in Mexican pesos.

Performance

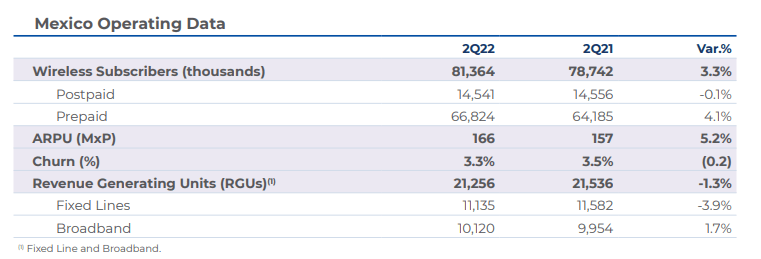

When looking at operating data for Mexico – we can see that while there was a slight decrease in postpaid wireless subscribers from Q2 2021 to Q2 2022 – this was outweighed by a 4.1% increase in prepaid subscribers. Additionally, churn saw a 0.2% decrease along with a 5.2% increase in ARPU (average revenue per user).

America Movil: Q2 2022 Financial and Operating Report

When examining the company’s income statement – while net income saw a slight fall of 0.3% compared to the same six-month period in 2021 – this was driven in significant part by lower foreign exchange losses last year. Over the same period, EBIT was up by 5% – driven by a 3.9% rise in service revenue.

America Movil: Q2 2022 Financial and Operating Report

From a balance sheet standpoint, the company has seen a slight decrease in its quick ratio (as measured by cash and cash equivalents plus accounts receivable all over total current liabilities) – but the company’s cash levels remain stable overall.

| December 2021 | June 2022 | |

| Cash and cash equivalents | 156383 | 150756 |

| Accounts receivable | 212977 | 210479 |

| Total current liabilities | 534013 | 544449 |

| Quick ratio | 69.17% | 66.35% |

Source: Figures sourced from America Movil Q2 2022 Financial and Operating Report. Quick ratio calculated by author.

Moreover, S&P Global Ratings (SPGI) recently upgraded the company’s credit rating to A-/Stable.

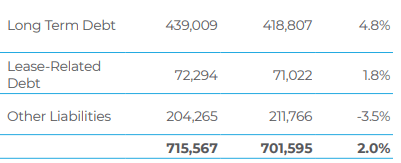

With that being said, America Movil did see its long-term debt rise by 4.8% from December 2021 to over 439 billion pesos:

America Movil Q2 2022 Financial and Operating Profit.

In this regard, investors might become cautious of the stock if long-term debt must continue to rise in order to generate further revenue growth.

Looking Forward

Over the past quarter – investors seem to have shied away from America Movil not only due to concerns about inflation going forward but also as a result of a weakening peso lowering the company’s overall earnings growth.

However, wireless subscribers have continued to grow, and the company has been seeing improved churn and ARPU rates.

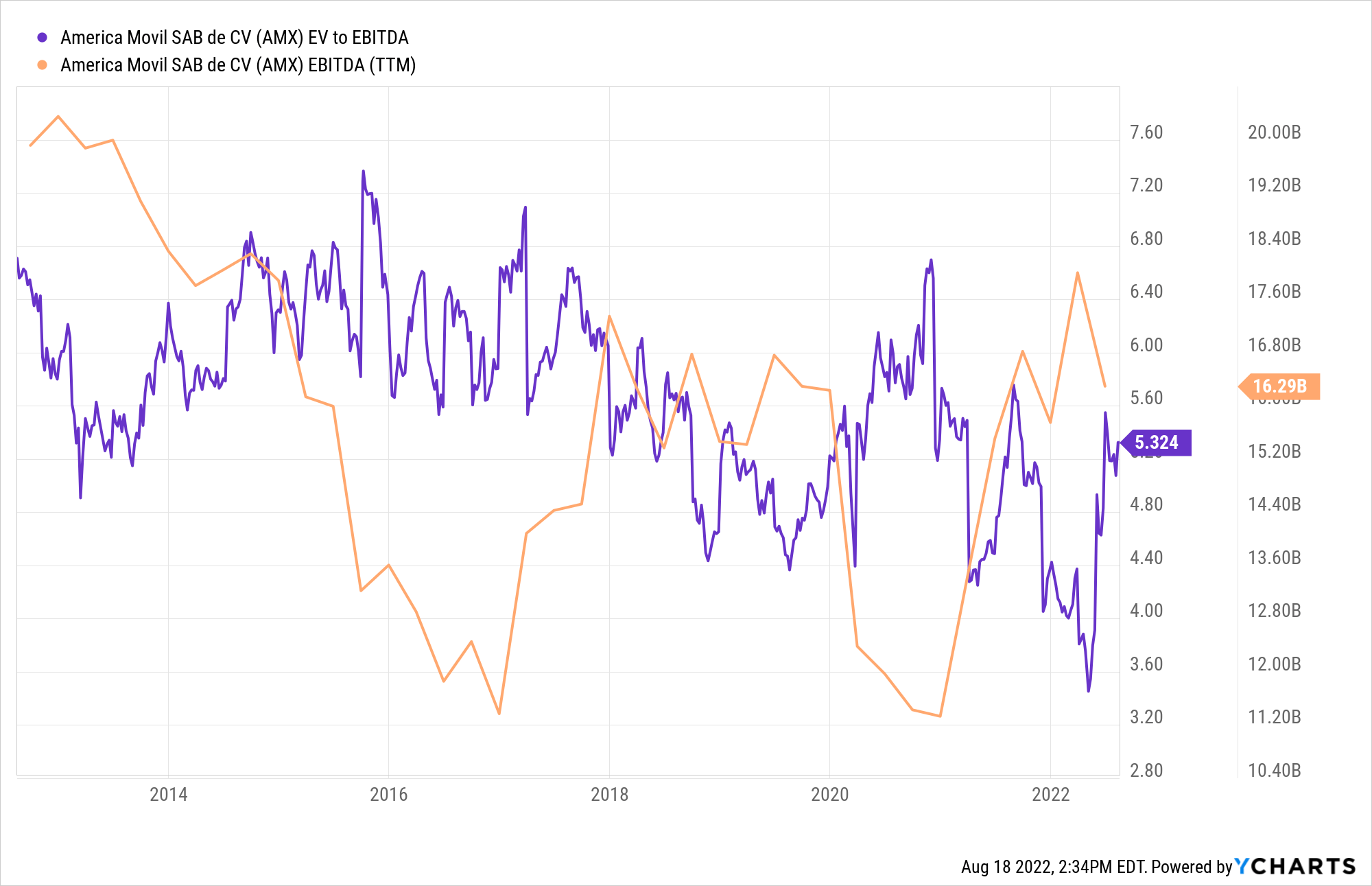

From an earnings standpoint, we can see that on a 10-year basis – the company has seen its EV/EBITDA ratio trending downwards – while EBITDA has steadily climbed back to levels seen between 2018 to 2020.

YCharts.com

While I anticipate that a rebound in peso strength relative to the dollar could reignite investor interest in this stock – investors are also likely to want to see a reduction in long-term debt levels.

Conclusion

To conclude, America Movil has continued to show growth across important metrics such as churn and ARPU. However, growth in long-term debt and foreign exchange losses as a result of a weaker peso relative to the dollar could continue to be concerning. I take the view that the stock could see limited upside in the short to medium-term.

Be the first to comment