PonyWang

Advanced Micro Devices, Inc. (NASDAQ:AMD) has grown by leaps and bounds over the last 2 years, benefiting directly from the heightened demand for computing products across the globe. But the chipmaker seems to be heading towards a speed bump. Latest channel sales data reveals that major computing parts and peripherals companies saw their sales decline during April, May, and June. Some of these companies happen to be AMD’s direct channel partners, which suggests that the chipmaker may also be revenue-challenged in the near future. Let’s take a closer look at this data and what it means for investors.

Speed Bump in The Making

Let me start by saying that AMD isn’t a vertically integrated company. Its silicon engineers design the chip architectures which are then fabricated by third-party foundries such as Samsung, Taiwan Semiconductor and GlobalFoundries. Some of the considerations for picking these contract manufacturers are production yield, volume, cost, node process and its stability. Anyway, once the silicon is out, they’re packaged in the form of usable GPUs and distributed globally by companies such as Gigabyte, MSI, ASUS, TUL Corporation and ASRock. Some of these companies also manufacture and distribute other peripherals such as motherboards and networking devices, which are essential for the functioning of AMD’s CPUs.

The point I’m trying to make here is that AMD has lots of third-party channel partners and vendors. By tracking the monthly sales figures for AMD’s key partners, we can get insights about how the company’s upcoming quarters might be looking like. For instance, if the chipmaker’s channel partners continue to grow rapidly, then it would indicate that its partners are flush with orders and AMD will eventually experience that growth as well. Conversely, a slowdown in the sales momentum for these suppliers would point to an impending slowdown for AMD. So, we at Business Quant developed a tool to track monthly sales data for 1200+ such Taiwan-listed firms for exactly this purpose.

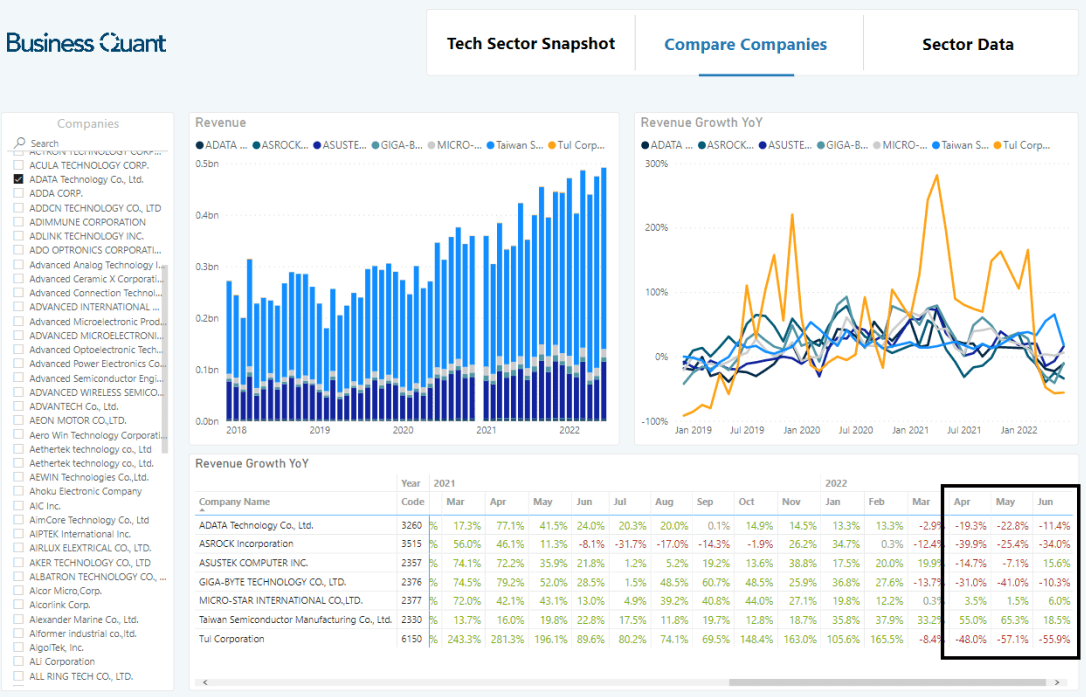

Note in the table below how many of these firms have been reporting sales declines consistently every month, starting from March. Before we dive deeper, let’s make one thing clear. TUL Corporation manufacturers GPUs exclusively for AMD, amongst other peripherals. On the other hand, MSI, ASRock and Gigabyte have a wide product portfolio, consisting of laptops, networking gear and computing peripherals for AMD as well its competitors. Taiwan Semiconductor (TSM) is a semiconductor chip manufacturer that caters to AMD as well as its competitors. ADATA Technology, on the other hand, is usually brand agnostic.

BusinessQuant.com

Basically, these companies aren’t pure-plays and their business isn’t exclusively with AMD. But having said that, the ongoing sales decline across many of these firms, in spite of easing semiconductor shortages, suggests:

- The industry demand for computing products may have waned off, and/or;

- ASPs (average selling prices) have been plummeting (like here) which may be fueling the sales decline, and/or

- This entire slowdown is just a transitory weakness.

This establishes the fact that things aren’t smooth sailing for AMD’s channel partners of late. But this begs the question – what does is mean for AMD and its shareholders?

Understanding the Ramifications

See, if AMD’s channel partners are seeing declining ASPs or sales volumes, then they’re naturally going to cut back on inventory orders which is likely to reflect as a slowdown in AMD’s growth momentum. So, for now, I’m anticipating the chipmaker’s management to issue a rather soft guidance for Q3 in its upcoming earnings call which is scheduled for next week. This slowdown would be contrary to what many of us have been anticipating of late.

Secondly, I don’t see AMD’s sales being adversely hit in Q2 at least. Fact of the matter is that channel inventory fluctuations usually take several weeks to fully unravel, especially in the hardware industry. Usually, companies sign minimum inventory purchase obligations, spanning from end retailers, to distributors, assembly and packing firms and even fabrication plants which reduces fluctuations. Considering that this channel sales slowdown started to appear in March, I reckon the financial impact in AMD’s books is likely to start showing sometime in its mid-Q3 (July/August time frame).

But this does not necessarily project a doomsday picture for AMD. This might just be transitory weakness as average selling prices across GPU and CPU SKUs normalize. The recent meltdown in cryptocurrency prices have prompted the community of crypto miners to dump their parts in large numbers, which has contributed to this price normalization. Also, Nvidia (NVDA) and AMD are a few months away from launching their next-generation SKUs on newer process nodes. So, the demand could be temporarily subdued as consumers, like yours truly, withhold their purchases and wait for these big releases.

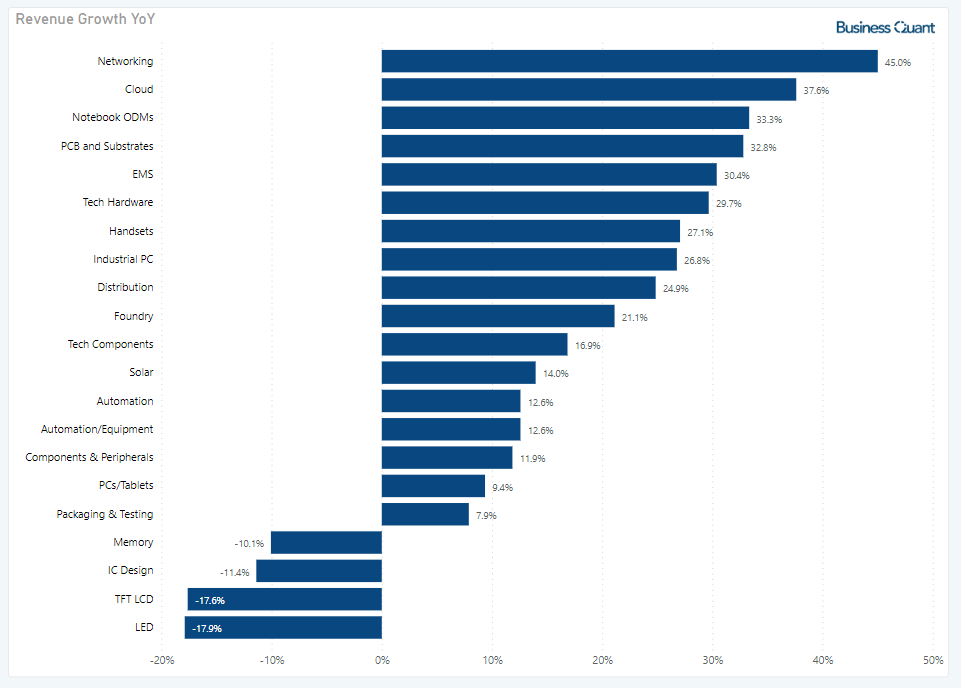

Lastly, I’ll clarify that there isn’t a sales meltdown across the entire technology hardware supply chain. Several industries, such as notebooks, datacenter devices, foundries, and computing peripherals amongst others, have experienced robust sales growth during June. This leads me to believe that the slowdown is transitory in nature and that it’s specific to AMD as well as its direct peers.

BusinessQuant.com

Having said that, AMD’s shares are attractively valued compared to many of the other rapidly growing semiconductor stocks at the time of this writing. This means the stock seems to have little downside potential from current levels, but is likely to rally ferociously upon the absence of bad news or posting positive news. So, I believe that any potential price corrections in AMD represent a buying opportunity for investors with a multi-year time horizon.

BusinessQuant.com

Investors Takeaway

Rather than presenting conjecture, I wrote this article with a data-driven approach. Although I’m bullish on AMD over the longer run, latest channel sales data suggests the company is heading towards a minor speed bump. So, investors who don’t have the appetite for portfolio drawdowns may want to avoid the stock for the time being. But patient investors with a long-term time horizon may want to accumulate AMD’s shares on potential price corrections. The chipmaker is attractively priced at current levels and has several catalysts at play that are poised to catapult its growth (as I detailed here).

Be the first to comment