piranka/iStock via Getty Images

Elevator Pitch

I am of the view that Apple Inc. (NASDAQ:AAPL) is a better buy as compared to Advanced Micro Devices, Inc. (NASDAQ:AMD). I previously wrote about AAPL and AMD in earlier articles published on February 24, 2022 and January 31, 2022, respectively. My analysis finds that Apple is in a better position to maintain or expand its current valuation multiples as compared to AMD. Recent speculation about lower iPhone SE production for AAPL is not a major worry, and I see the potential introduction of hardware subscriptions as a key re-rating catalyst for Apple’s shares.

AMD And Apple Stock Key Metrics

Recent developments for AMD and Apple deserve attention, and it is relevant to evaluate certain key metrics disclosed for these two companies in the past few months.

On February 24, 2022, AMD revealed that the company’s “board of directors approved a new $8 billion share repurchase program.” As of the date of this announcement, AMD also still had $1 billion remaining from its prior share buyback authorization announced in May 2021. The new $8 billion share buyback program is quite significant representing approximately 4.6% of AMD’s market capitalization, and it is usually good when companies return more capital to their shareholders.

But things are not as straightforward as it sounds on paper. AMD’s new share repurchase program is likely initiated with the purpose of offsetting the dilution associated with the recent acquisition of Xilinx. In the February 24, 2022 announcement, AMD also acknowledged that it intends to buy back more of its own shares with the aim of both “offsetting dilution from stock issuances and reducing share count over time.”

Two weeks prior to the share buyback announcement, AMD confirmed on February 14, 2022 that the company’s takeover of Xilinx has been completed. Based on my estimates, AMD’s shares outstanding (excluding the effects of any share repurchases) will increase by approximately +35% as this transaction is entirely funded by the issuance of shares.

In my previous January 31, 2022 update for AMD, I noted that the company’s “growth for FY 2022 could be diluted as a result of the Xilinx deal.” My view is supported by the work of other sell-side analysts as well. A February 11, 2022 sell-side report (not publicly available) titled “Updated XLNX Accretion Analysis Ahead of the Deal Close” published by Raymond James Financial (RJF) estimates “about $0.43 of dilution to 2022 earnings” for AMD. This is because the dilution effects of the increased share count “exceeds the accretion from adding Xilinx earnings (which has grown at a slower rate vs. AMD).”

Although the $8 billion new share repurchase program will help to partially offset the dilution effects relating to the Xilinx acquisition, this deal will still have a negative impact on AMD’s short-term financial performance.

Separately, the most notable metric relating to Apple is the company’s estimated (or speculated) production volume for its key products.

On March 28, 2022 Seeking Alpha News published an article citing a Nikkei Asia report which claimed that Apple “is cutting 20% of its planned iPhone SE output for the next quarter (2Q 2022 in calendar year terms).”

In my opinion, I think that there are three reasons why investors shouldn’t be unduly worried even if such speculation about AAPL’s iPhone SE production cut turns out to be true.

Firstly, it could be simply a case of Apple prioritizing the production of specific key products over others, as it did in the past. In my prior November 12, 2021 article on Apple, I analyzed why AAPL “reduced the production of iPads” in consideration of “long lead times for iPhone 13″ and expectations of weaker demand for iPads.”

Secondly, iPhone SE should not account for a meaningful proportion of Apple’s sales. Analysts from IDC estimate that the recently launched iPhone SE 3 could possibly contribute a modest 10% of the company’s total shipments for iPhones.

Thirdly, my analysis of Apple’s historical quarterly revenue in recent years suggests that the company’s revenue is typically higher in the second half of the calendar year vis-a-vis the first half. This is likely attributable to the launch of the new iPhone flagship model in September/October and holiday season purchases. As such, Q2 2021 is not a peak season for Apple’s product sales, so even if production falls below expectations, this shouldn’t be a major concern.

In the subsequent sections of the current article, I touch on the historical share price performance and the outlook for both AMD and Apple.

Does AMD Or Apple Perform Better?

Apple’s shares have performed much better than AMD in 2022 thus far.

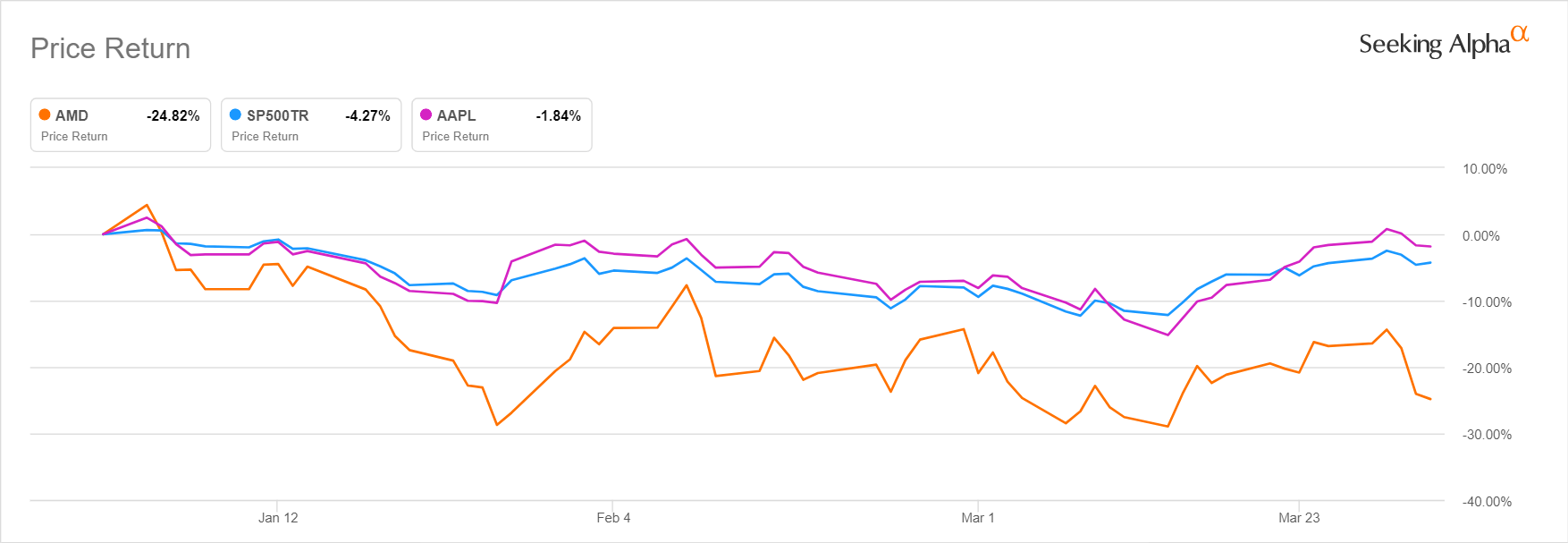

2022 Year-to-date Stock Price Performance For AMD And Apple

Seeking Alpha

Apple’s stock price decreased by -1.8% in 2022 year-to-date, which is even better than the -4.3% decline for the S&P 500 over the same period. In contrast, AMD’s share price has already fallen by -24.8% in the first three months or so of this year.

One factor that accounts for AMD’s inferior share price performance vis-a-vis Apple is that the short-term negative effects of the recent Xilinx acquisition might be a greater concern for investors as compared to the potential reduction in production volumes for Apple, which I explained earlier.

Another factor is that the valuation de-rating for AMD has been much more severe. Notably, Apple and AMD are currently valued by the market at consensus forward next twelve months’ normalized P/E multiples of 28.0 times and 26.8 times, respectively based on S&P Capital IQ data and their last traded share prices as of April 1, 2022. But AMD traded at 47.9 times forward P/E at the beginning of 2022, while the market valued AAPL at a more reasonable forward P/E of 32.0 times as of January 3, 2022.

Is AMD Or Apple’s Market Capitalization Growing Faster?

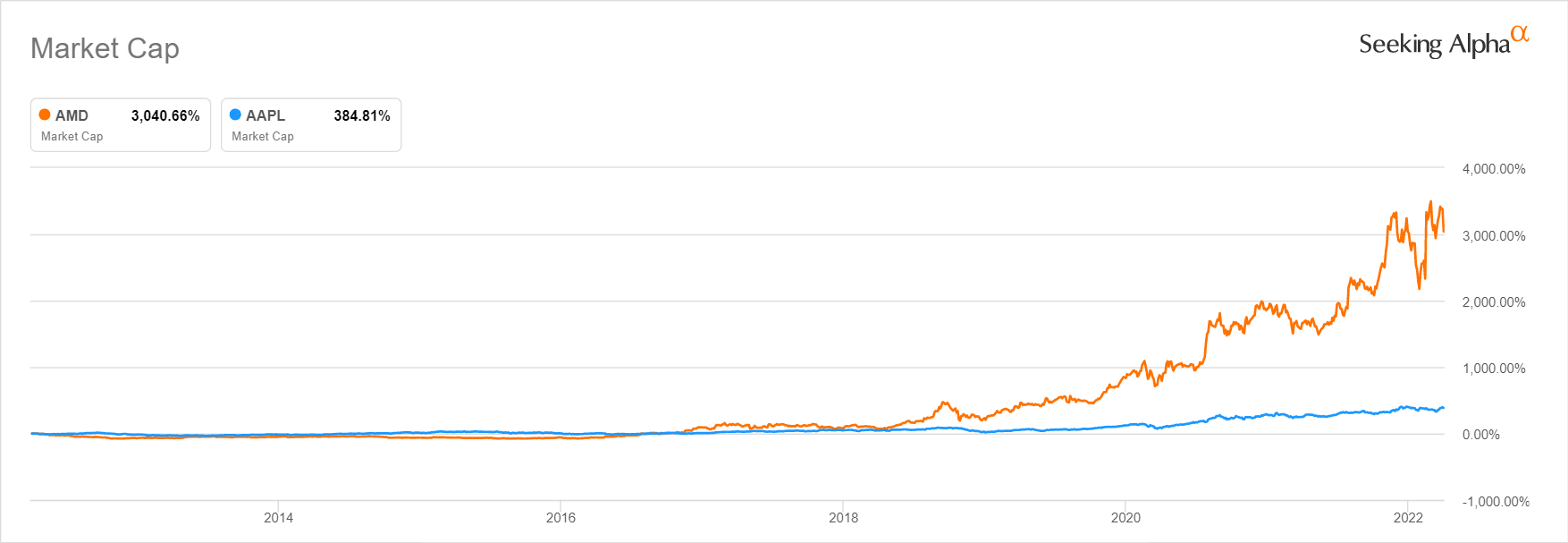

AMD’s market capitalization has been growing much faster than that of Apple in the past 10 years. This holds true, even if one does the same comparison for the one-year, three-year and five-year periods.

The Relative Growth In The Market Capitalizations Of AMD And Apple In Percentage Terms For The Past Decade

Seeking Alpha

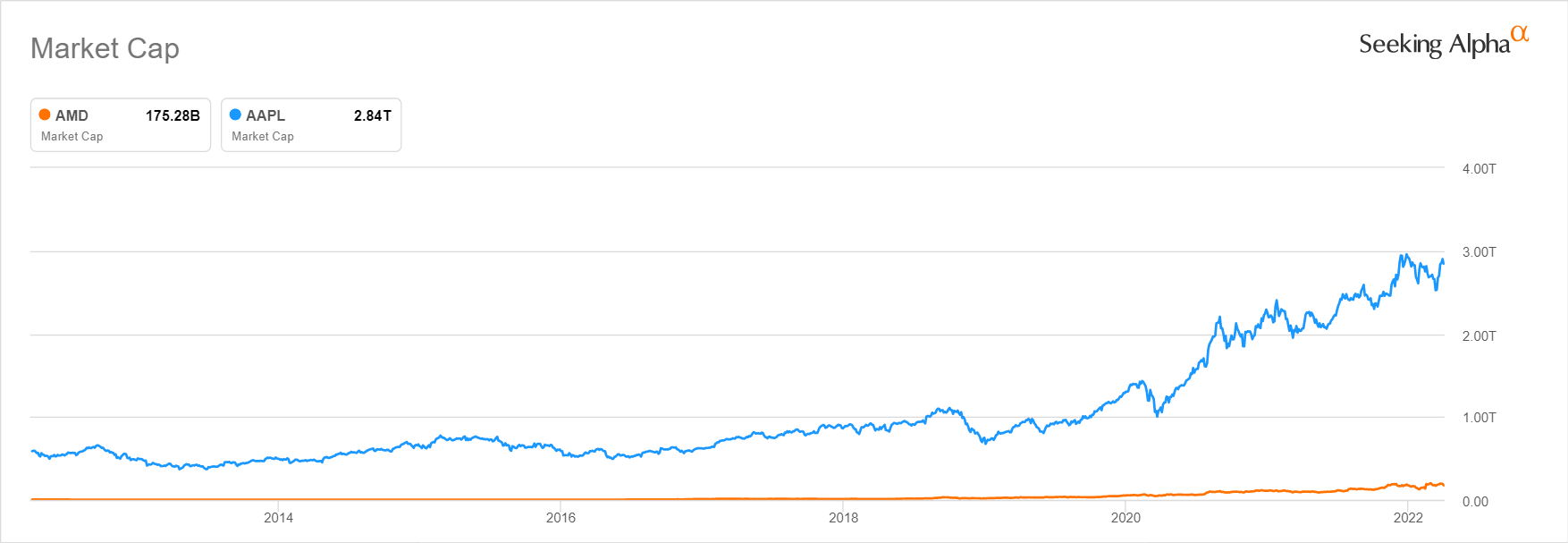

It is a different story, when one compares the market capitalization of the two listed companies in absolute terms. Apple is approximately 16 times as large as AMD with regards to market capitalization.

A Comparison Of The Market Capitalizations Of AMD And Apple In Absolute Terms

Seeking Alpha

Of course, it is the future that matters, rather than what has happened in the past. In the next section, I discuss the outlook and growth prospects for Apple and AMD.

Will AMD Be Worth More Than Apple In The Future?

In my view, it is highly unlikely that AMD’s market capitalization can exceed that of Apple in the foreseeable future. More importantly, I think that Apple’s shares should outperform AMD in the near term.

Sell-side consensus data sourced from S&P Capital IQ data suggests that AMD is expected to generate a normalized net profit of $11.1 billion in fiscal 2026, while Apple is forecast to deliver normalized earnings of $146.6 billion in FY 2026. In other words, this implies that if AAPL is valued by the market at 25 times P/E in 2026, AMD will have to trade at a P/E ratio of 330 times to equal Apple’s market capitalization. This implies that there is a very low probability that AMD will be worth more than Apple in the next five years.

Separately, as I mentioned earlier in this article, both stocks are now trading at forward P/E multiples in the mid-to-high twenties percentage level. For the next one year, I also expect Apple to be valued by the market at a relatively higher P/E multiple than AMD, and do better than the latter in terms of share price performance.

In the case of AMD, there has been a substantial valuation de-rating for high-flying, high-growth tech stocks in recent months, and it will be challenging for AMD to trade back up to 40-60 times P/E levels that it used to trade at in 2020 and 2021. Moreover, the dilutive effects of the Xilinx deal will put a cap on the potential earnings growth for AMD this year.

On the other hand, Apple is well-positioned to continue trading at its current P/E multiples in the high-twenties level, and a further expansion in its P/E multiples to the low-to-mid thirties can’t be ruled out.

Specifically, AAPL’s plans for hardware subscriptions could be a major boost to its valuations. On March 23, 2022, Seeking Alpha News highlighted that Apple “is reportedly working on a subscription plan to make owning iPhones and other hardware, such as Macs, similar to paying a monthly app fee” citing a Bloomberg report. Although Apple has yet to officially release details on this new strategy, this could possibly be a game changer for the company.

Apple’s forward P/E multiple has re-rated significantly from the low-teens levels in the 2017-2019 period to above 20 times in the past two years. A key driver of this positive valuation re-rating has been an increasing proportion of high-margin and recurring revenues in recent years.

If AAPL makes the shift to hardware subscriptions, it could help to lower the financial burden of owning more Apple hardware products. This might translate to higher hardware sales and also increased services revenue. With more consumers owning multiple Apple hardware products, there are also even more “touch-points” for Apple to cross-sell other high-margin services, which supports further valuation re-rating for AAPL.

Is AMD Or AAPL Stock A Better Buy?

AAPL stock is a better Buy than AMD in my opinion. As explained above, I think it is challenging for AMD’s shares to see a positive re-rating any time soon. On the other hand, Apple should be able to maintain or expand its valuation multiples going forward thanks to an increasing proportion of recurring services revenue.

Be the first to comment