Andrei Berezovskii

While chip rival Intel Corporation (INTC) reported a horrible Q4 2022 quarter last week, Advanced Micro Devices, Inc. (NASDAQ:AMD) investors shouldn’t sweat the weak numbers. The smaller chip company reports earnings this week (Tuesday 1/31 after the close), and investors shouldn’t expect a great quarter or strong guidance for 2023. Regardless, my investment thesis remains ultra-Bullish on AMD due to potential market share gains when the PC inventory correction inevitably ends in the next few quarters.

PC Inventory Correction Hitting Hard

A big part of the weak results from Intel is an ongoing inventory correction. The chip giant reported Q4’22 revenues of $14.0 billion and guided to a massive collapse in Q1’23 revenues to a range of ~$11.0 billion.

In the chip sector, a big key to quarterly revenues is end-user demand versus chip shipments. Intel is guiding towards end-user consumption far exceeding chips shipped to customers in the impacted period.

Intel provided some rather bullish commentary on actual PC demand in 2023 suggesting the market demand is around 275 million units. On the Q4’22 earnings call, CEO Pat Gelsinger made these following comments on PC demand:

In the PC market, we saw a further deterioration as we ended calendar year 2022. In Q3, we provided an estimate for the calendar year 2023 PC consumption TAM of 270 million to 295 million units. Given continued uncertainty and demand signals we see in Q1, we expect the lower end of that range is a more likely outcome.

The PC sector was trending towards annualized sales in this range prior to Covid. A major issue facing Intel is that the PC ecosystem is digesting inventories at a fast clip (emphasis added):

Near term, the PC ecosystem continues to deplete inventory. For all of calendar year 2022, our sell-in was roughly 10% below consumption with Q4 under shipping meaningfully higher than full year, and Q1 expected to grow again to represent the most significant inventory digestion in our data set. While we know this dynamic will need to reverse, predicting one is difficult.

AMD Impact

The impacts on AMD are very hard to determine. The smaller chip company had already cut a lot of the PC sales from the Q3 numbers and Q4 guidance limiting any similar financial hit again.

Also very importantly, AMD pre-announced a warning for Q3’22 on October 6. The management team issued a warning very close after the quarter end and would unlikely now wait a full month to report a bad quarter for Q4.

When reporting Q3’22 results, AMD guided to the following Q4’22 expectations:

- Revenue – ~$5.5 billion +/- $300 million, flat sequentially.

- Gross margin – ~51%.

The real big unknown is whether AMD would feel any need to provide preliminary updates on 2023. The company hasn’t guided to 2023 numbers, making this the biggest risk to the investment story going into the Q4’22 earnings report on January 31 after the market close.

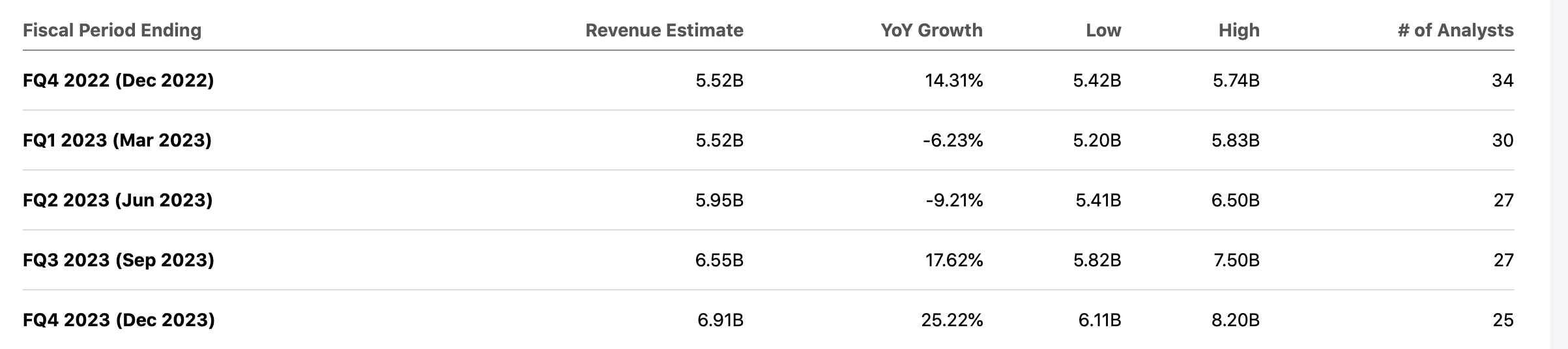

Analysts currently forecast 2023 sales of $25 billion with the following quarterly estimates:

Source: Seeking Alpha

AMD provided a lot of guidance suggesting the PC inventory correction would end by the start of 2023. The analyst estimates support this thesis, with Q1’23 revenues targeted sequentially flat during a typically seasonally slow period, but the company faces a scenario where this appears exceptionally difficult to achieve.

If AMD generates Q1’23 revenues of $5.5 billion and builds on those numbers throughout the year, the stock is off to the races. If not, investors should quickly understand a weak March quarter refreshes the numbers and provides an easy hurdle in the year ahead.

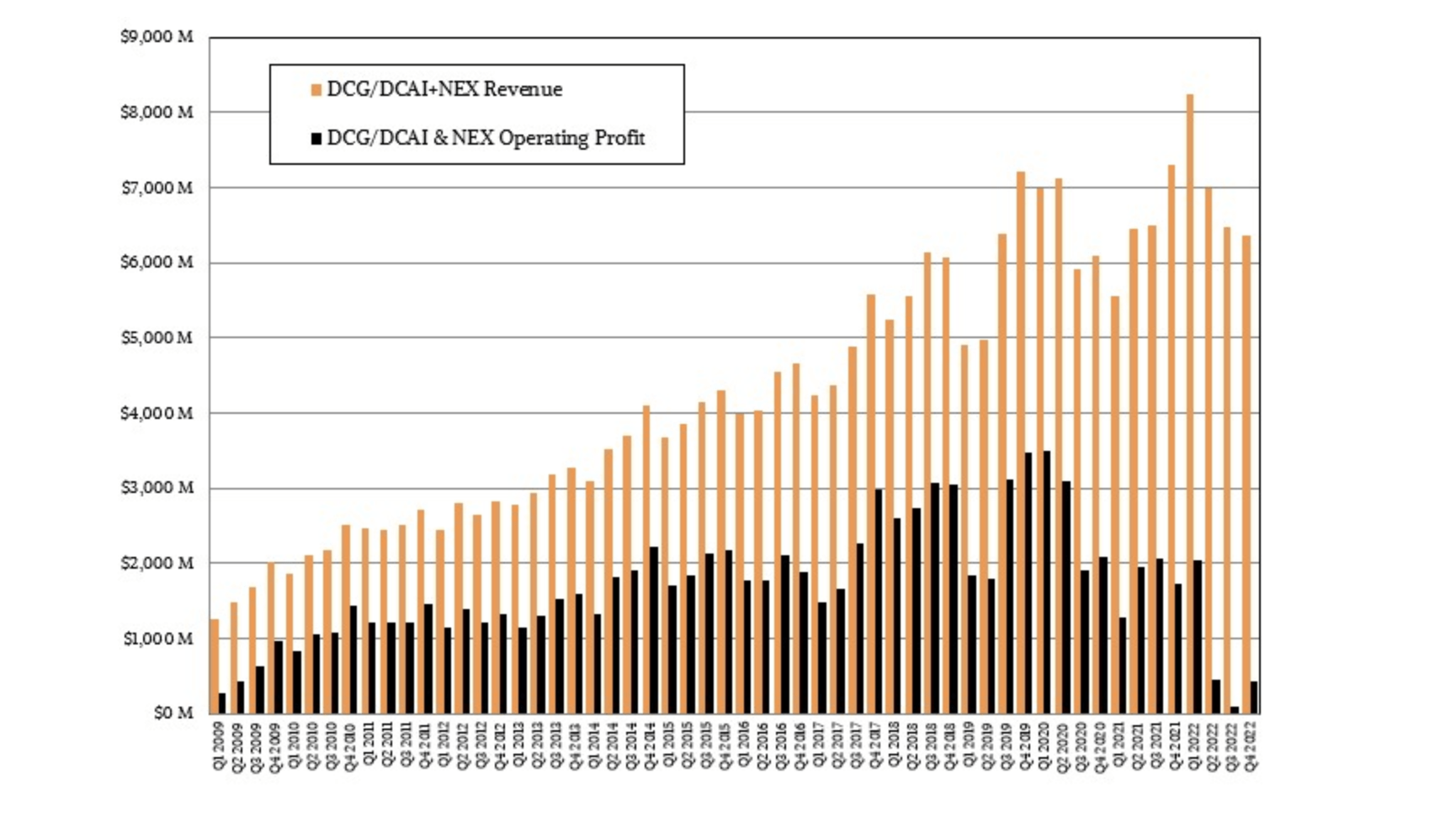

Investors can be confident AMD isn’t losing any market share here. The server market remains strong, with the Genoa CPU chip forecast to continue grabbing share from Intel. The chip giant was able to report Q4’22 data center group revenues were still solid at $4.3 billion and NextPlatfrom estimated “real data center” revenue still sits above $6 billion and in line with numbers for the last 4+ years.

Source: NextPlatform

Though, the amount was down from the prior year levels. Intel has generated $6+ billion in quarterly data center revenues since the 2018/19 period. During this period, the chip giant has completely lost all of their operating profits in the sector likely due to AMD offering better price/performance forcing Intel to cut prices.

The quarterly numbers are relatively high considering AMD has stolen a large amount of market share the last couple of years. The market should expect AMD to report a quarter approaching $2 billion in server revenues.

The problem facing Intel is that one isn’t sure how much of the guidance is AMD just taking data center market share with the Genoa CPUs and new segmented options. After all, Intel pointed to weakness in the enterprise and China segments where AMD isn’t as strong yet.

Takeaway

The key investor takeaway is that no pre-announcement from AMD is a positive sign, but investors should expect weak guidance for at least Q1’23. The chip company should continue taking market share in the data center space with billions still left at Intel to capture.

Advanced Micro Devices, Inc. stock only trades at 21x 2023 EPS targets, but remember these numbers are greatly impacted by weak demand currently. Our base case research on AMD predicts the chip company will generate normalized EPS in the $5 to $6 range and the stock is very cheap at only $72 here.

Be the first to comment