JHVEPhoto/iStock Editorial via Getty Images

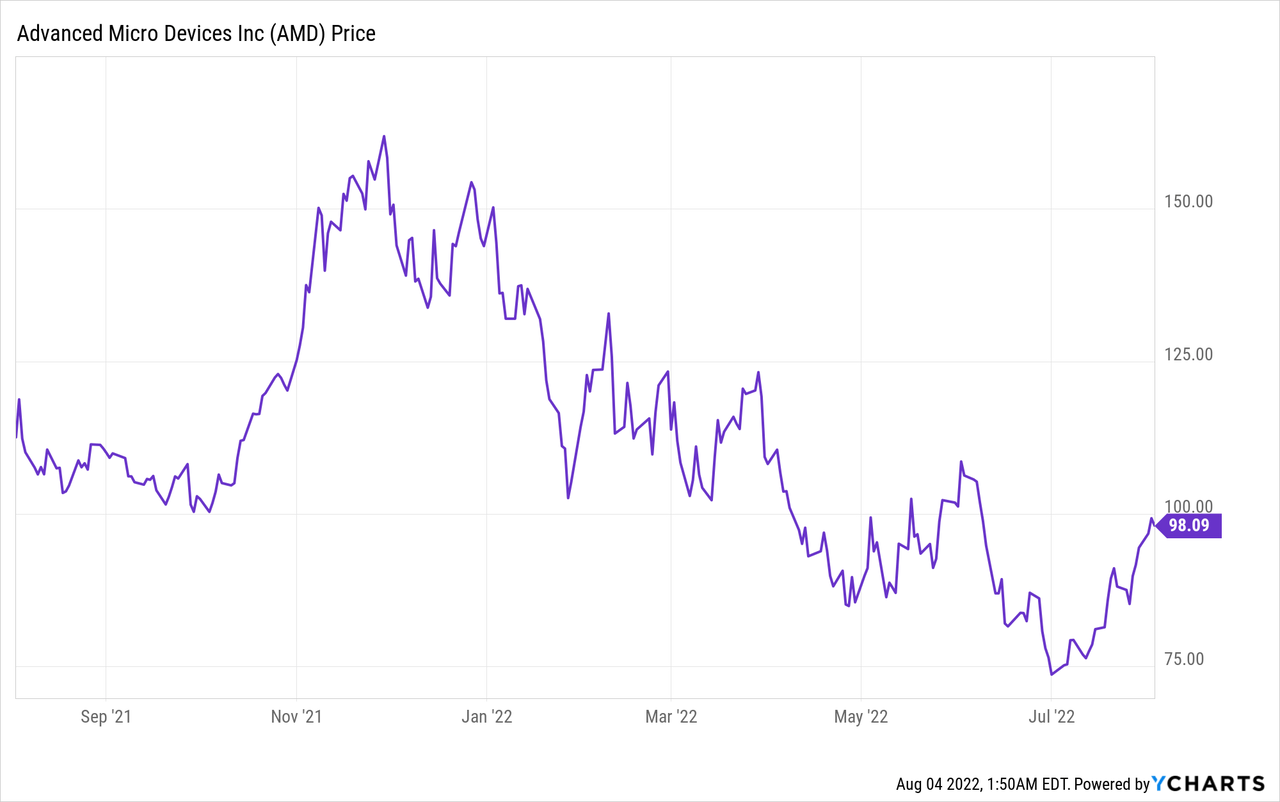

Advanced Micro Devices (NASDAQ:AMD) is a leading provider of high performance semiconductor chips. The company has generated tremendous growth over the past few years and in the quarter ending June 2022, results continued to shine. Despite this, the stock price has been butchered by ~51% between November 2021 and July 2022. This mainly driven by the high inflation and rising interest rate environment. However, over the past month, the stock price has actually popped by ~33% as the market saw an opportunity to capture, “Growth at a Reasonable Price”. AMD is still undervalued intrinsically and relative to historic multiples, let’s dive into the business model, financials and valuation for the juicy details.

Business Model

AMD has a $135 billion total addressable market across its four main business segments:

- Data Center – $50B TAM

- PCs – $40B TAM

- Embedded – $29B TAM

- Gaming – $16B TAM

AMD TAM (Investor presentation 2022)

This market opportunity is forecasted to expand, thanks to growing technologies such as Hyperscale Cloud, Supercomputing, 5G, Self Driving Vehicles, Simulation (Metaverse) and even IoT (Internet of Things).

Technology Trends (investor presentation 2022)

AMD is a strong category leader across three of its four main segments, which include Data Center, PCs and Embedded. NVIDIA (NVDA) battles AMD as a leader in Gaming GPUs and also with a strong data center offering. The two previously planned to merge, which would have created an unstoppable chip company, but this was halted by “regulatory challenges”.

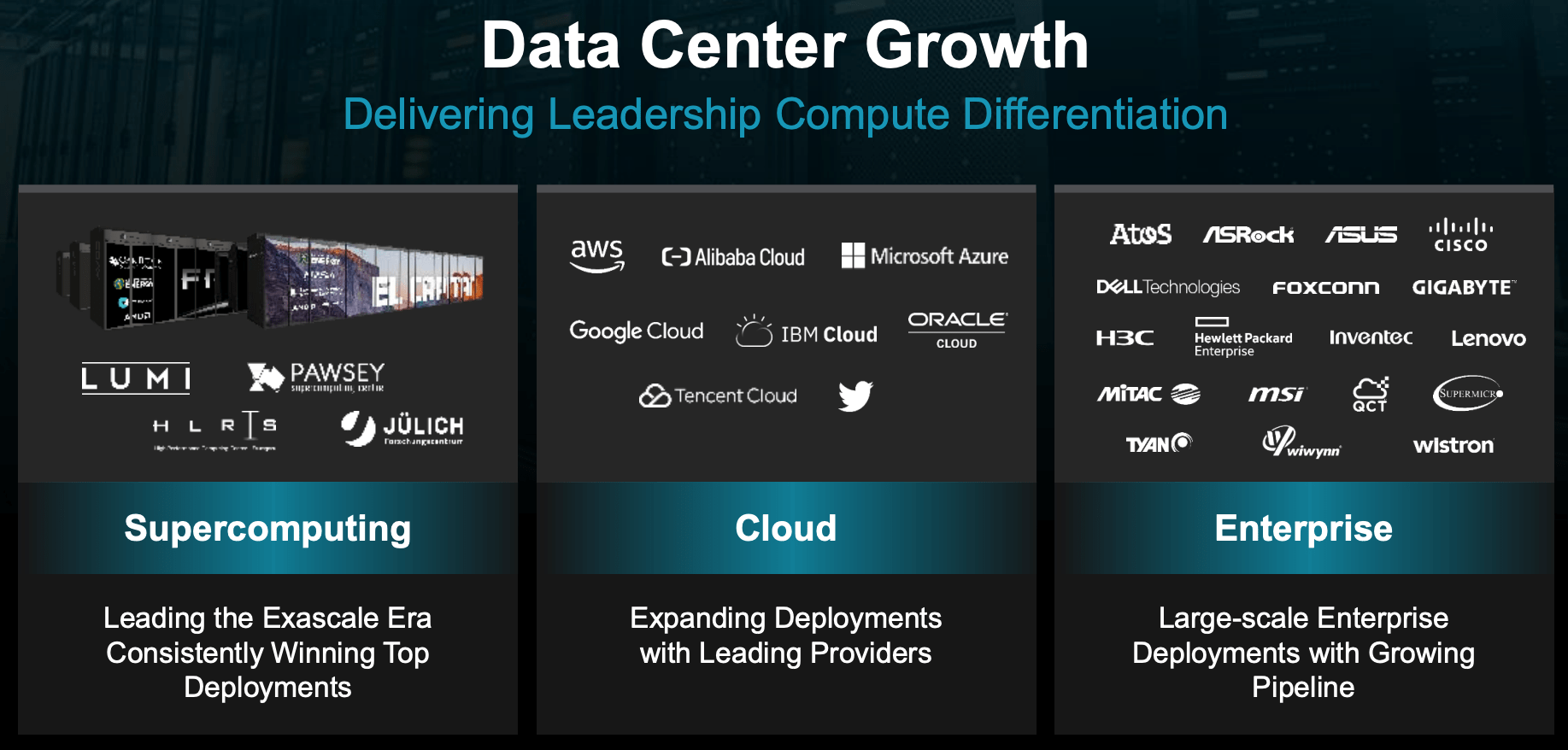

AMD’s Data Center server processors are best in class. It’s AMD EPYC are the “World’s highest performance server processor”. This offers greater performance than the competition across high performance computing (HPC), cloud and enterprise workloads. Its chips are already deployed across the three major cloud providers’ infrastructure such as AWS, Microsoft Azure and Google Cloud. In addition, AMD’s chips can be found in the Chinese cloud leader facilities, such as those run by Tencent Cloud and Alibaba Cloud. In the recent quarter, Microsoft Azure has deployed AMD Instinct MI200 accelerators for large-scale Artificial Intelligence (AI) training, which is another great endorsement of the company’s leading technology.

AMD Data Center offering (Investor Presentation 2022)

AMD’s offering is also widely deployed across enterprises such as Cisco, Dell, Hewlett-Packard Enterprises (HPE), Asus, Lenovo and more. The AMD powered Frontier Supercomputer has recently surpassed the exaflop barrier and achieved industry recognition.

Management has made it a strategic priority to become the “New Data Center Leader” and they aim to do this through leveraging their best-in-class technologies, continued innovation and executing on a consistent roadmap.

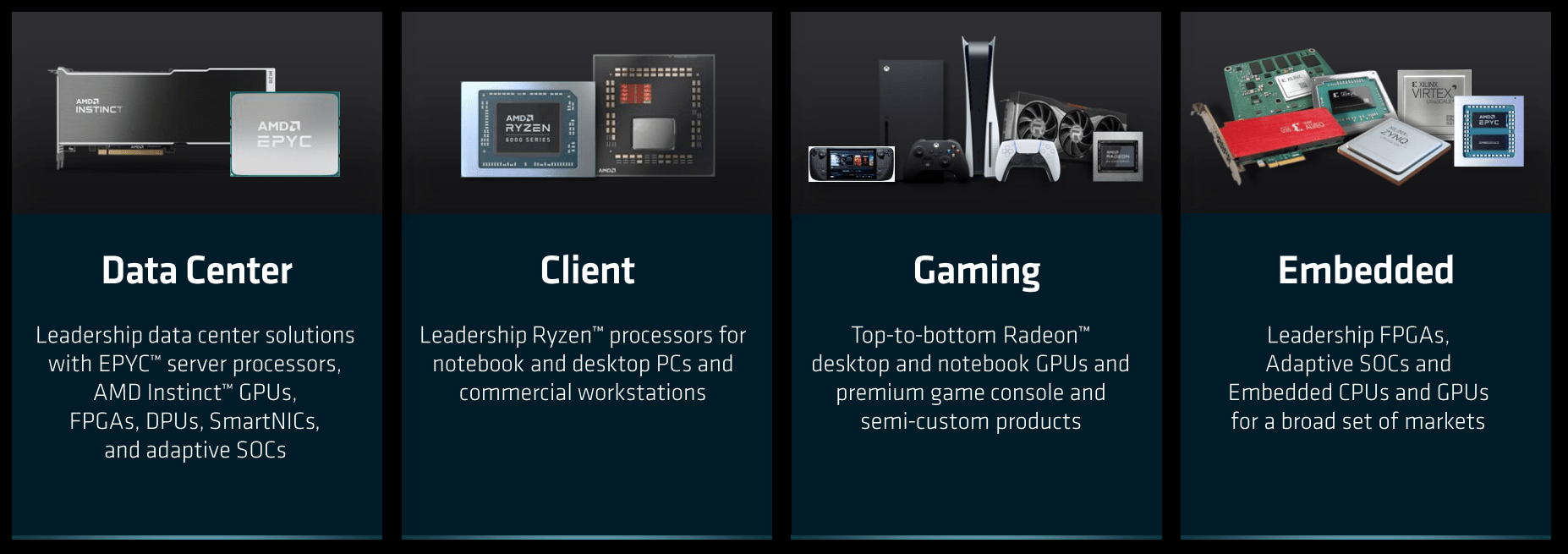

In the Gaming segment, AMD’s Zen 2 chips are used in the PlayStation 5 and the Xbox Series X/S. For client PCs, AMD’s Ryzen Processors edge Intel in the value and power consumption department and offer very close performance in other areas.

AMD products (Investor presentation 2022)

The main reason AMD offers much more efficient consumption when compared to Intel is because of its smaller 7nm (nanometer) chips. Intel has fallen behind after struggling to execute on the latest 7nm chip designs. Meanwhile, AMD has already announced an even smaller 5nm chip, which will be the “world’s first” of this size and is expected to arrive in the fall of 2022.

AMD Zen 5nm (Investor Presentation 2022)

Growing Financials

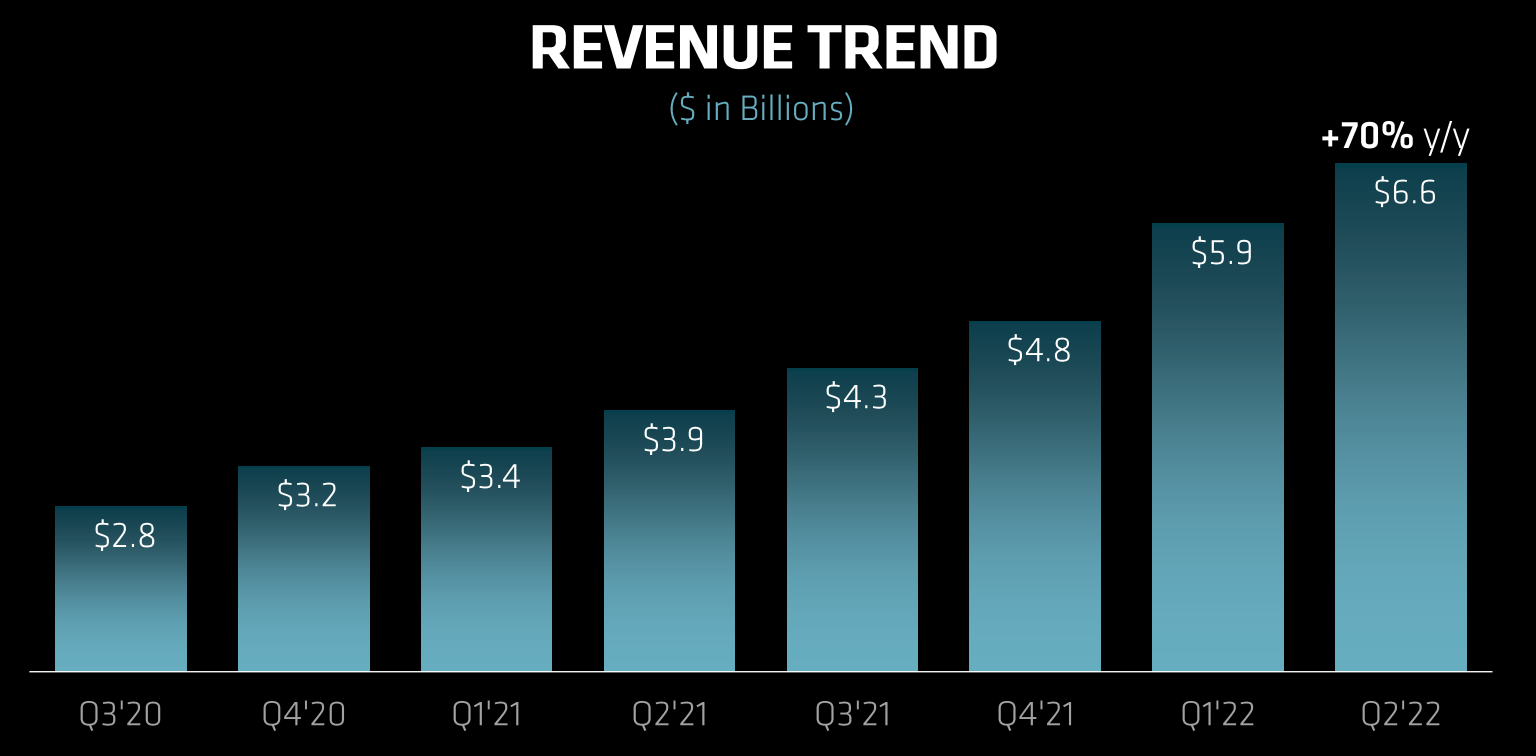

AMD announced strong earnings for the second quarter of 2022. Total revenue was $6.6 billion, up a blistering 70% year over year.

AMD Revenue (Earnings AMD)

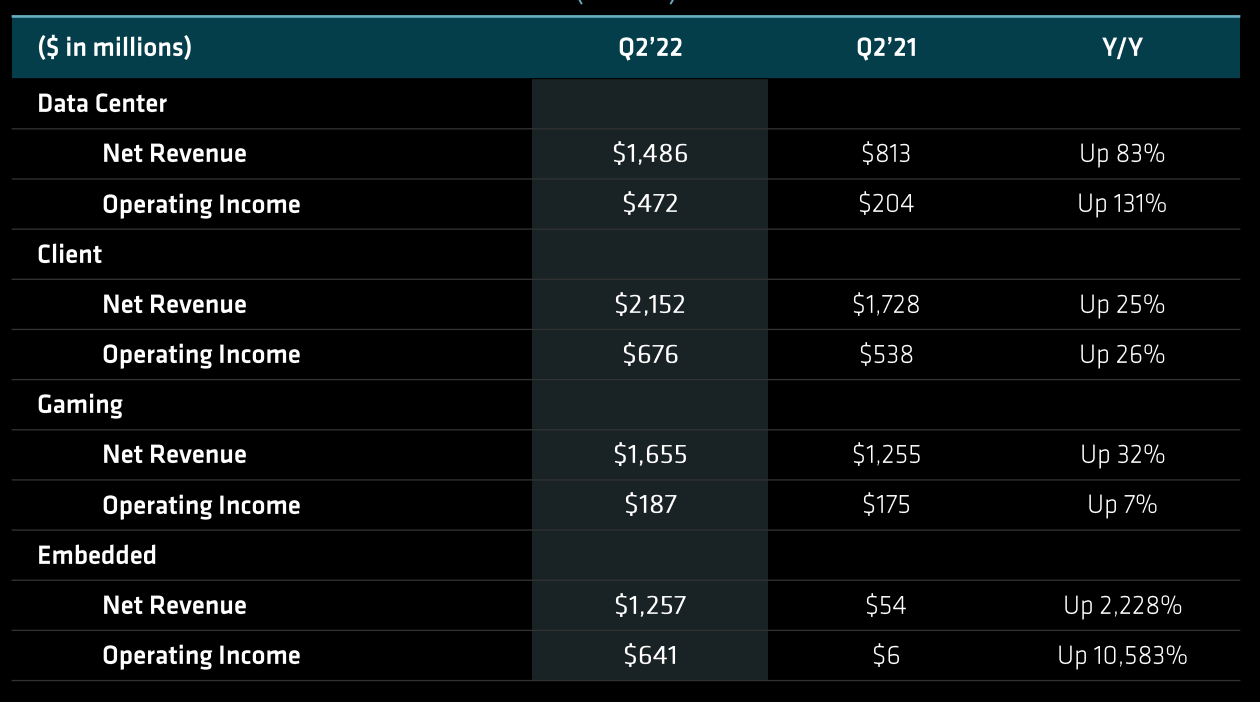

This revenue growth was driven by strong Data Center revenue, up a rapid 83% year-over-year to $1.486 billion at a strong 32% operating margin. This was a result of strong sales of its EPYC Data Center Processors. Client revenue popped by 25% to $2.152 billion, as a result of strong mobile processor sales. Gaming revenue also expanded by 32% to $1.7 billion. This was driven by an increase in semi custom product sales, however, graphics revenue did decline slightly.

Segment Growth (AMD Q2 22 Earnings)

Embedded computing revenue accelerated to $1.257 billion. This increased by an eye-watering 2,228%, but this increase was mainly driven by revenue inclusion from a recently finalized acquisition. AMD acquired Xilinx in an all-stock transaction, the deal was announced in 2020 but finally closed in early 2022. Xilinx is the inventor of the FPGA (field programmable gate array) which is commonly used in aerospace and military applications.

AMD’s gross margin was 46%, which represented a 2% decrease year-over-year. Operating income was $526 million, or 8% of revenue. This was down 37% year-over-year, primarily driven by the amortization of intangible assets related to the Xilinx acquisition. Earnings per share were also affected by the same issue, down $0.27, compared to $0.58 in the prior year. The good news is this is the decline in income related to the acquisition seems to be more of a balance sheet adjustment, as opposed to a decline in “real dollars”. So, I don’t consider this to be a major issue moving forward. Non-GAAP diluted earnings per share actually increased to $1.05, up from $0.63 a year ago.

Earnings per share (AMD Q2 Financials)

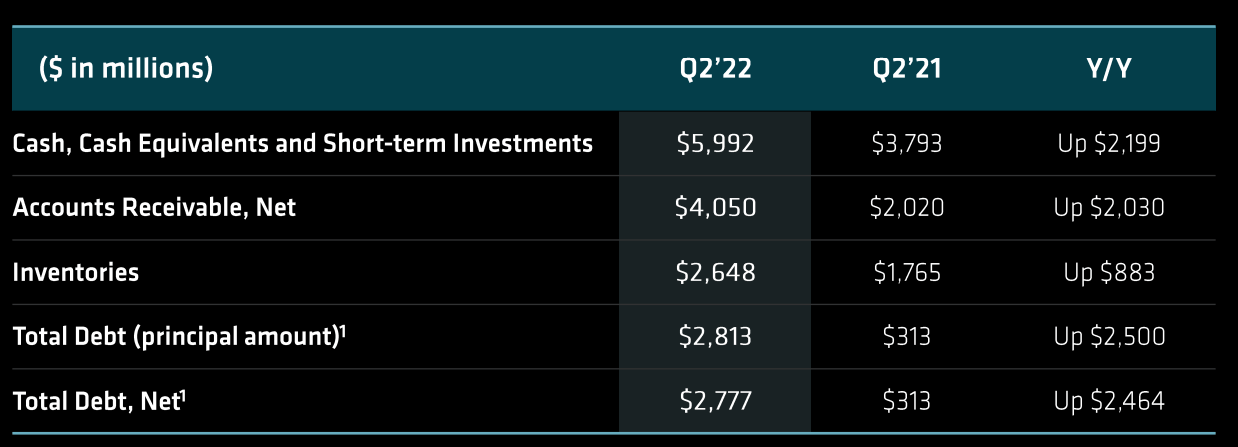

AMD has a robust balance sheet with $5.99 billion in cash and short-term investments. In addition to total debt of ~$2.8 billion, which is manageable due to the strong Free Cash flow of $906 million, up 43% year over year.

AMD Balance Sheet (Earnings Q2)

Tepid Guidance

For the third quarter of 2022, AMD’s management forecasts $6.7 billion in revenue, which would represent a slightly slower growth rate of 55% vs. 70% mentioned prior. Full year revenue is forecasted to be $26.3 billion (+/- $300 million), up approximately 60% year-over-year. These are fantastic numbers, however, AMD’s CEO Su is forecasting slower growth in the PC segment.

“We have taken a more conservative outlook on the PC business, so a quarter ago we would have thought that the PC business would be down let’s call it high single digits,”

“Our current view of the PC business is that it will be down mid-teens.”

Advanced Valuation Model

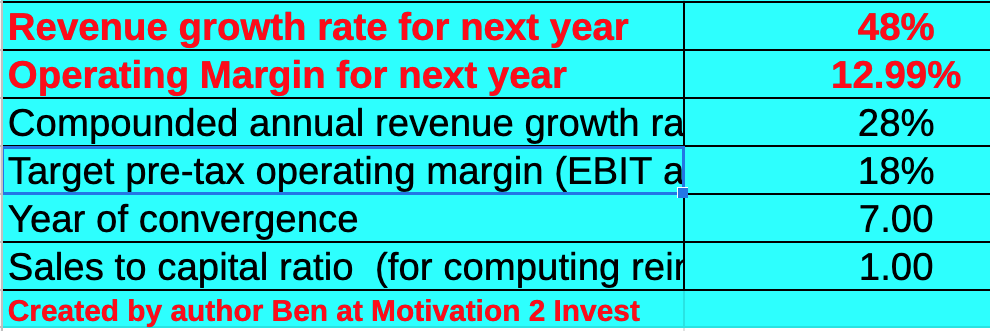

In order to value AMD, I have plugged the latest financials into my advanced valuation model, which uses the discounted cash flow method of valuation. I have conservatively forecasted 48% revenue growth for next year, as the company will be growing its revenue from a larger base. In addition, I have forecasted 28% revenue growth for the next 2 to 5 years. This valuation is driven by expected strength in Data Center segment to continue and strong digital transformation tailwinds.

AMD Stock Valuation 1 (created by author Ben at Motivation 2 Invest)

I have forecasted the company’s operating margin to steadily increase to ~18% over the next 7 years, driven by strong growth in the higher margin cloud segment. These margin numbers include the company’s R&D expenses, which I have capitalized for increased accuracy.

AMD stock valuation 2 (created by author Ben at Motivation 2 Invest)

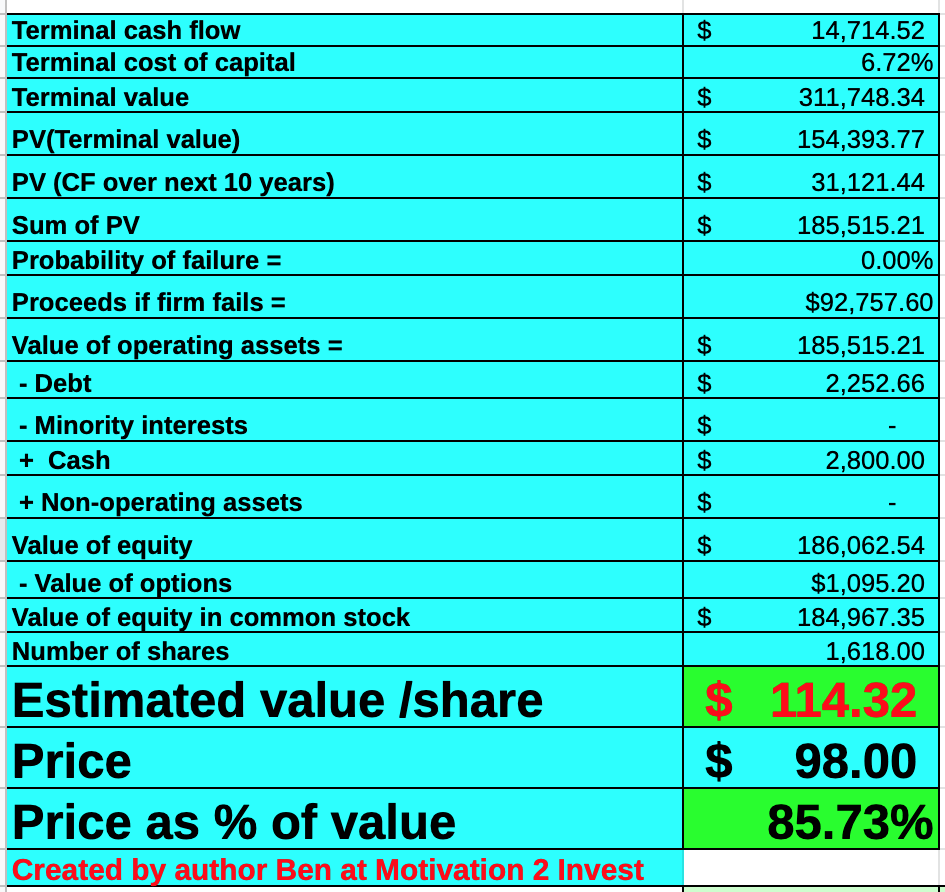

Given these numbers, I get a fair value of $114 per share. The stock is currently trading at $98/share and thus is ~15% undervalued.

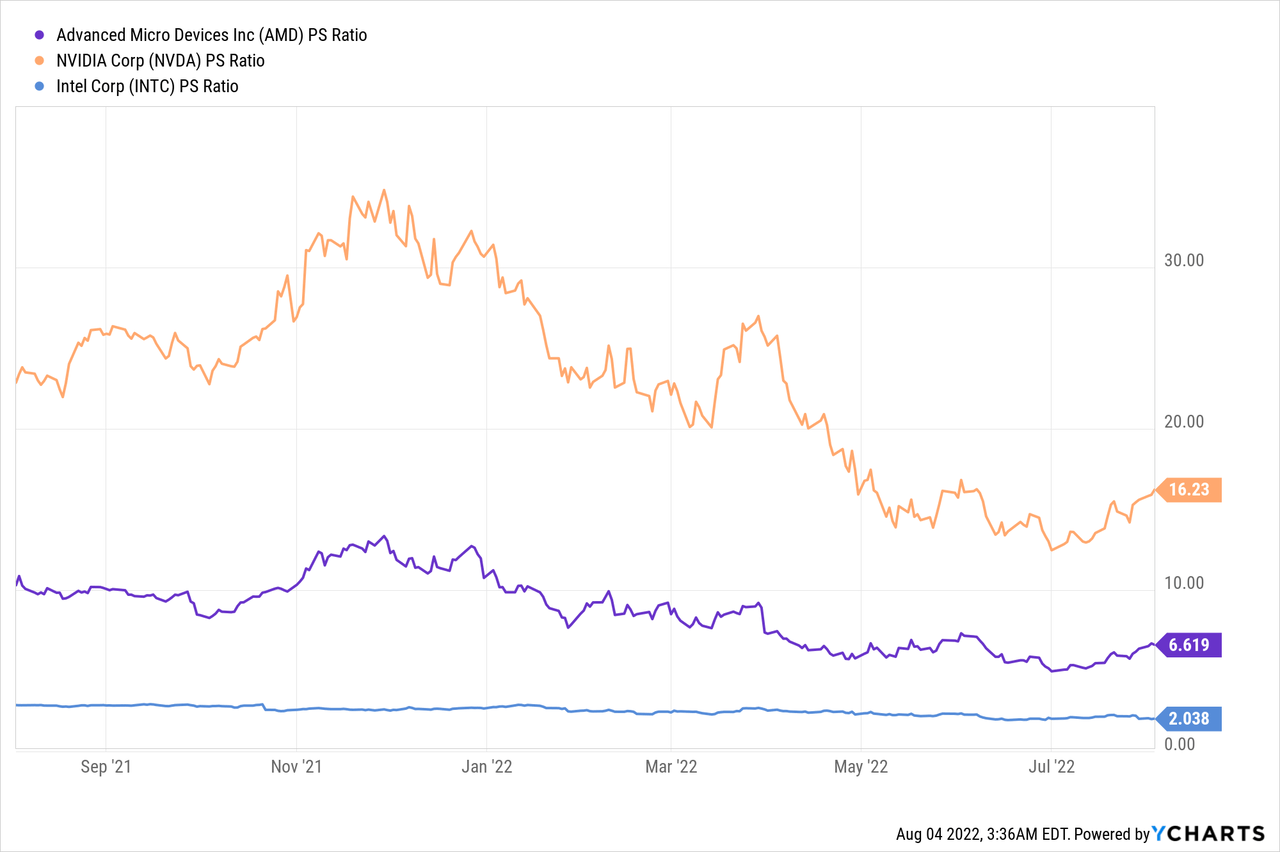

As an extra data point, AMD is trading at a Price to Earning (P/E) (FWD) = 22.86, which is 54% cheaper than its 5-year average. AMD’s Price to Sales Ratio = 6.6, which is cheaper than Nvidia, PS = 16. However, as accepted, it is more expensive than Intel (INTC) which is trading at a low Price to Sales Ratio = 2, due to slower growth and execution issues.

Risks

IT spending Slowdown

The high inflation environment is squeezing input costs for businesses. Meta (META) and many other tech companies have announced plans to slow down hiring. In addition, “Cloud Titans” such as Microsoft (MSFT) and Google (GOOG) (GOOGL) have announced to be extending the life of their server and network assets from four years to six years. Microsoft CFO recently stated:

“Investments in our software that increased efficiencies in how we operate our server and network equipment as well as advances in technology have resulted in lives extending beyond historical accounting useful lives”

Actions such as these will directly impact companies such as AMD, as delayed IT spending will hit its growth rate and many others in the industry.

Final Thoughts

AMD is a tremendous company and true innovator when it comes to technology. The fact that NVIDIA tried to acquire the company (and this was blocked) is testament to the quality of its technology and assets. It has a track record of blistering growth and an outstanding ability to execute, which can’t be said for others such as Intel. The stock is still undervalued and thus this looks to be a great opportunity for the long term. However, I do expect some short term volatility in the next year due to IT spending cutbacks and softer gaming demand.

Be the first to comment