Sean Gallup/Getty Images News

An unprecedented emphasis has been placed on outpacing inflation. The repercussions of inflation outpacing wage growth and the return on invested capital have detrimental ramifications. If earned income or the return of capital from investments doesn’t keep pace with rising prices and escalated costs of living, inflation can significantly decrease purchasing power, which could correlate to depleting savings accounts, retirement portfolios, or increased debt levels. The impacts of rampant inflation can become catastrophic unless an individual is well hedged in a portfolio allocation that can outpace inflation.

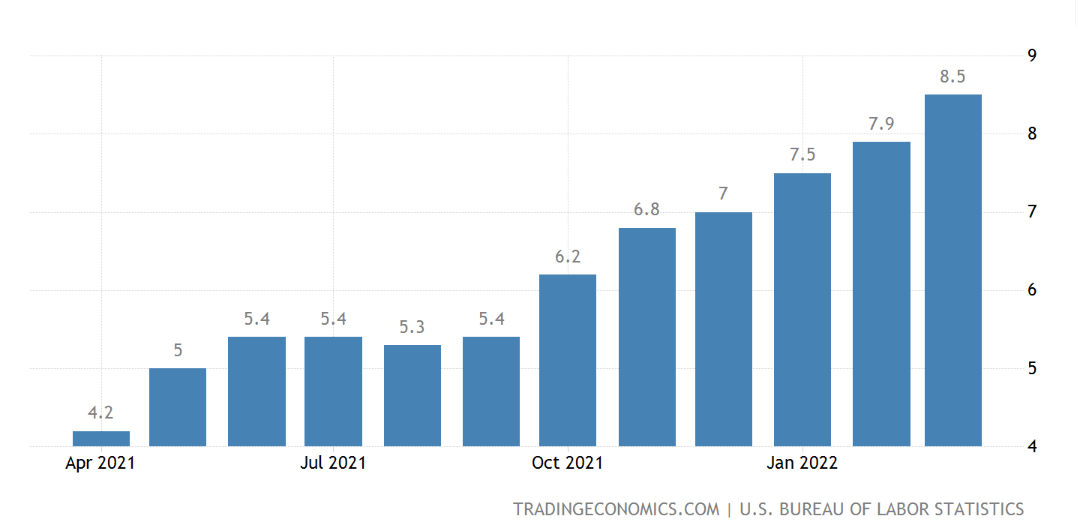

Today inflation has accelerated to 8.5%, which is the highest level on record since December of 1981. Energy prices increased 32%, while food prices jumped 8.8%. It’s imperative that people conduct a deep financial analysis of their investments and adjust to the new market dynamic, as cheap capital simply isn’t available to companies. Most companies face rising operating costs, declining sales volumes, and shrinking margins as they fail to pass rising costs on to the consumer. During inflation, many cost-conscious consumers shop with a heightened sense of awareness as they look to squeeze every penny out of the dollar. This can mean switching from name-brand items to store brands or eliminating expenses from their monthly budgets.

Trending Economics

From an investment standpoint, conventional wisdom indicates that investors should allocate their capital toward resilient consumer defensive businesses that can utilize economies of scale and high pricing power. Companies that fall into these parameters have a greater ability to pass rising costs onto the consumer without incurring declining sales volumes. Traditional investment tendencies are to invest in dividend-paying businesses because their financials are stable and predictable while also adding gold as hedges against inflation.

A dollar today will not buy the same value of goods in 2032, the same way the dollar’s purchasing power has changed since 2012. Throughout history, inflation has occurred within market economies, and the only two ways to stay ahead of inflation are to grow your income quicker than inflation rises or by investing in asset classes that can outperform during periods of high inflation. The world has morphed into a global economy as pricing power, and global market reach should be considered when looking for investible assets that can outpace inflation. When it comes to investments, the bottom line is that for every $10,000 of invested capital, you need to finish the year exceeding $10,850 to outpace the current rate of inflation (8.5%). This can come from capital appreciation, dividends, or a combination of both.

Over the previous year, inflation has risen 102.38%, increasing from 4.2% to 8.5%. Nobody has a crystal ball, and there are too many variables and unknown factors to accurately predict how far inflation will rise or how quickly it will subside. The 2021 fiscal year is a great benchmark because inflation was 7% in December. I want to pick companies with the following characteristics:

- Revenue growth outpaced the combination of cost of revenue and total operating expenses

- 3-year track record of increasing net income

- Gross profit margin that exceeds 50%

- Profit margin that exceeds 25%

- Sideways capital expenditure expense with increasing cash generated from operations leading to increased Free Cash Flow

- More cash on hand than total liabilities

These qualifications eliminate almost every individual equity in the market, as only a handful of companies can meet these criteria. I believe Alphabet (NASDAQ:GOOGL) is the best-positioned stock to outpace inflation.

It’s Time For A New Type Of “Conventional thinking” Or “Conventional Wisdom”

Yes, it’s true that during inflation and even a recession, people will always need to buy food, pay their electric bills, and utilize real estate space. Aspects of technology need to be added to the conventional wisdom around recession-proof or inflationary stocks. Nobody is getting rid of their cell phones; companies will still advertise, individuals will still consume content, and everyone is going to use search engines. It’s not 1980 anymore, and the 1980 mentality around what sectors will do well during periods of inflation needs to be updated.

Alphabet is a collection of businesses. The most well-known is Google, which gets broken out into two segments: Google Services and Google Cloud. Within Alphabet’s ecosystem of businesses, they own Android, Chrome, Gmail, Google Drive, Google Maps, Google Photos, Google Play, and YouTube, just to name a few. Alphabet has built world-class advertising technologies for advertisers, agencies, and publishers to power their digital marketing businesses. Millions of companies have reached their audience and grown their businesses through Alphabets advertising solutions.

Here are some statistics that illustrate Alphabet’s dominance.

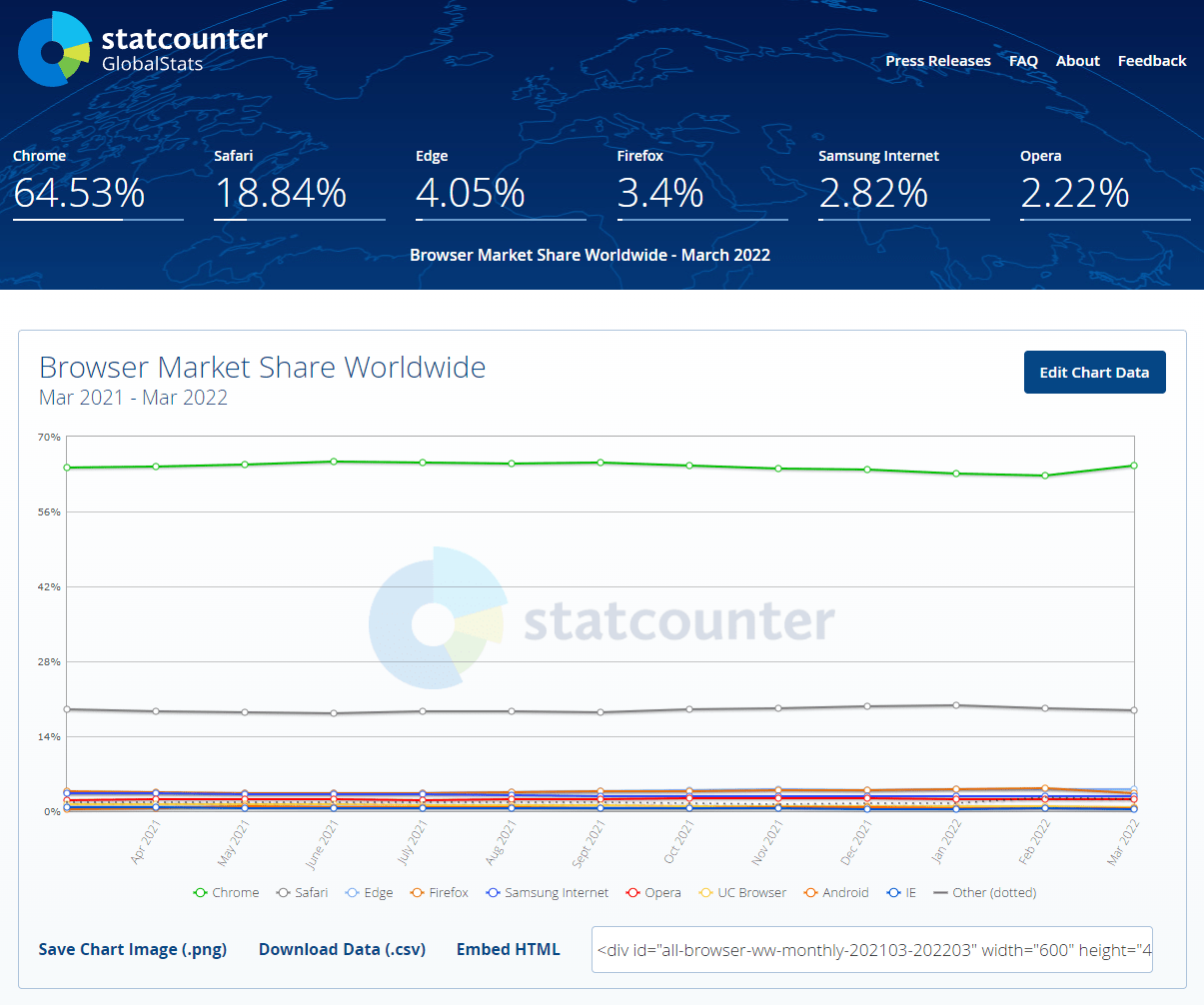

Google Chrome has 64.53% in browser market share globally, with Safari coming in 2nd place with 18.84%.

statcounter

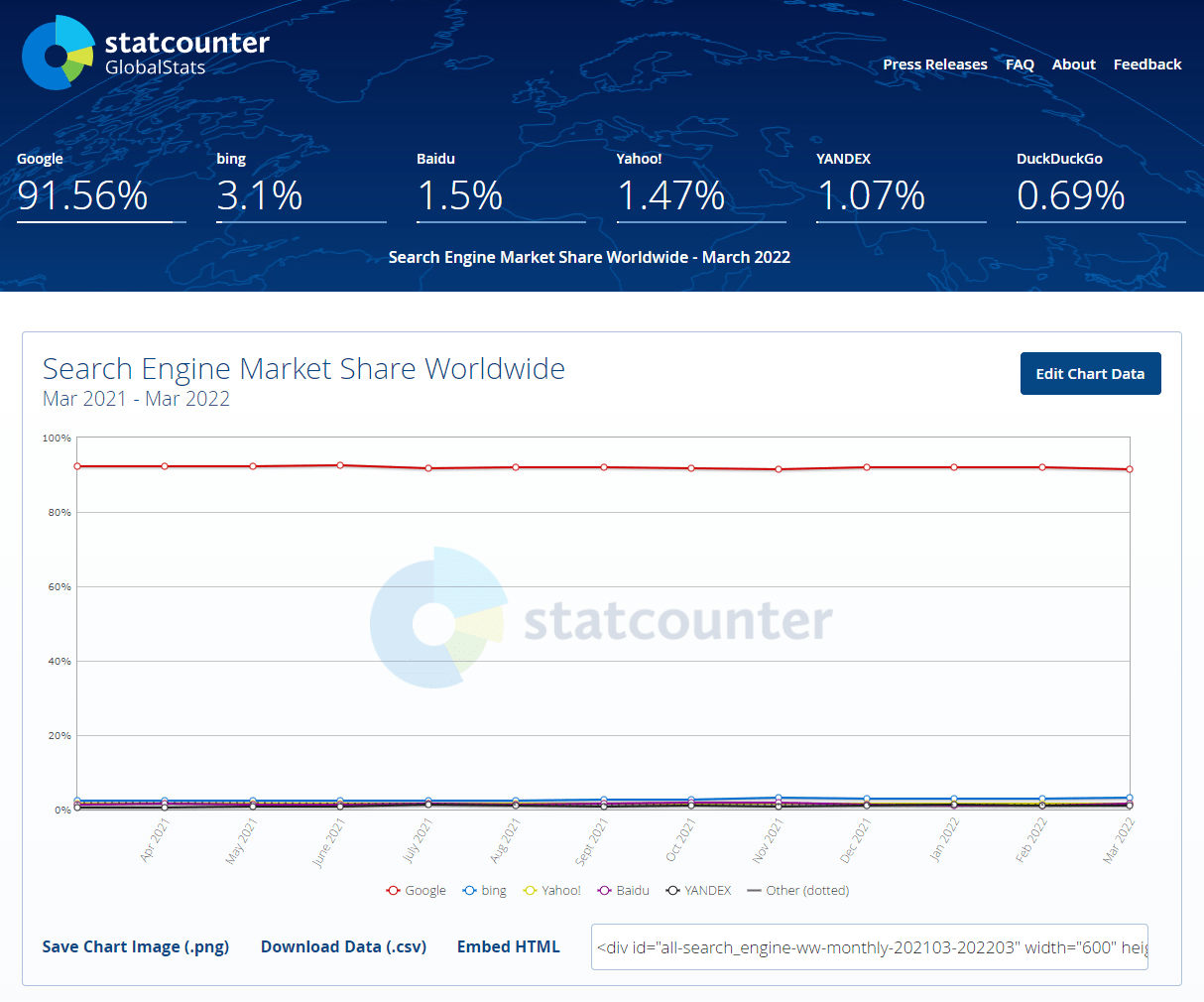

Google has 91.56% of the search engine market share worldwide, while Bing comes in 2nd with 3.1%.

statcounter

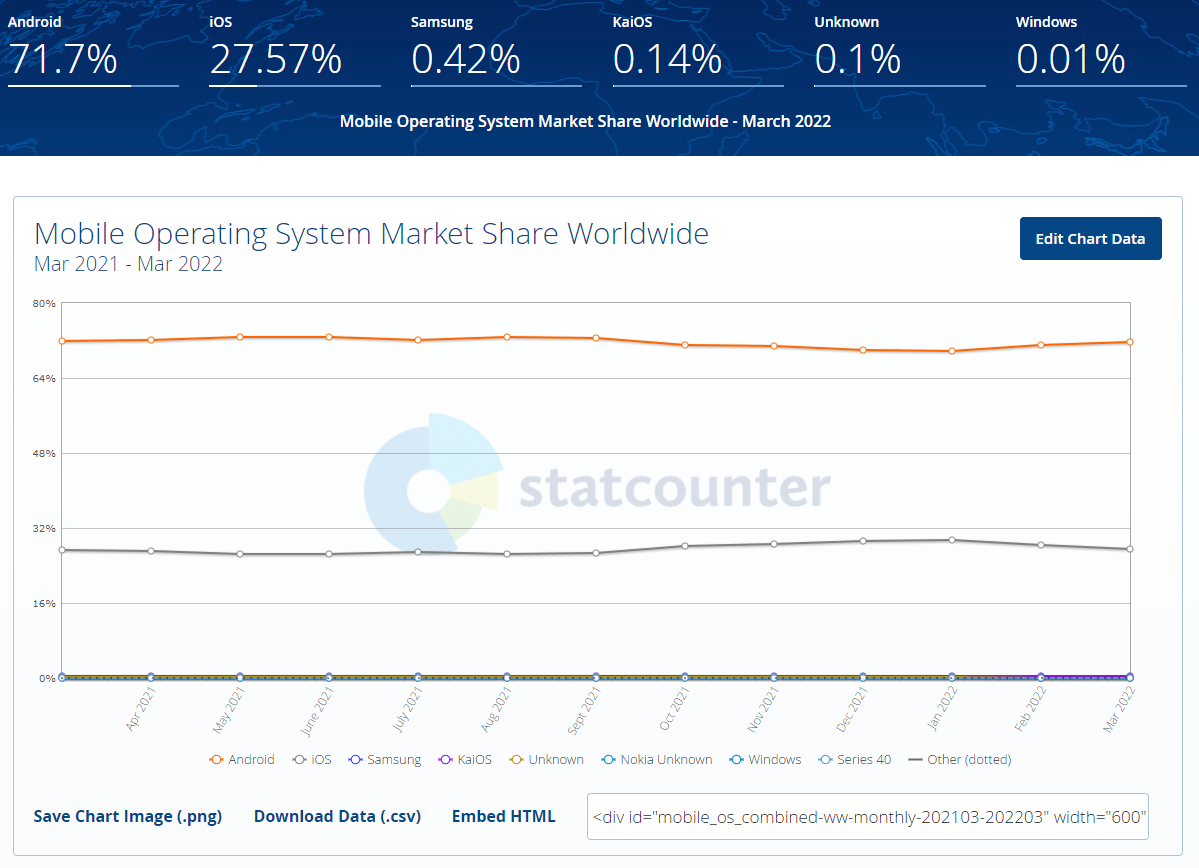

Android, which Alphabet owns, has 71.7% of the global mobile operating system market share (smartphones), while iOS from Apple (AAPL) accounts for 27.57%.

statcounter

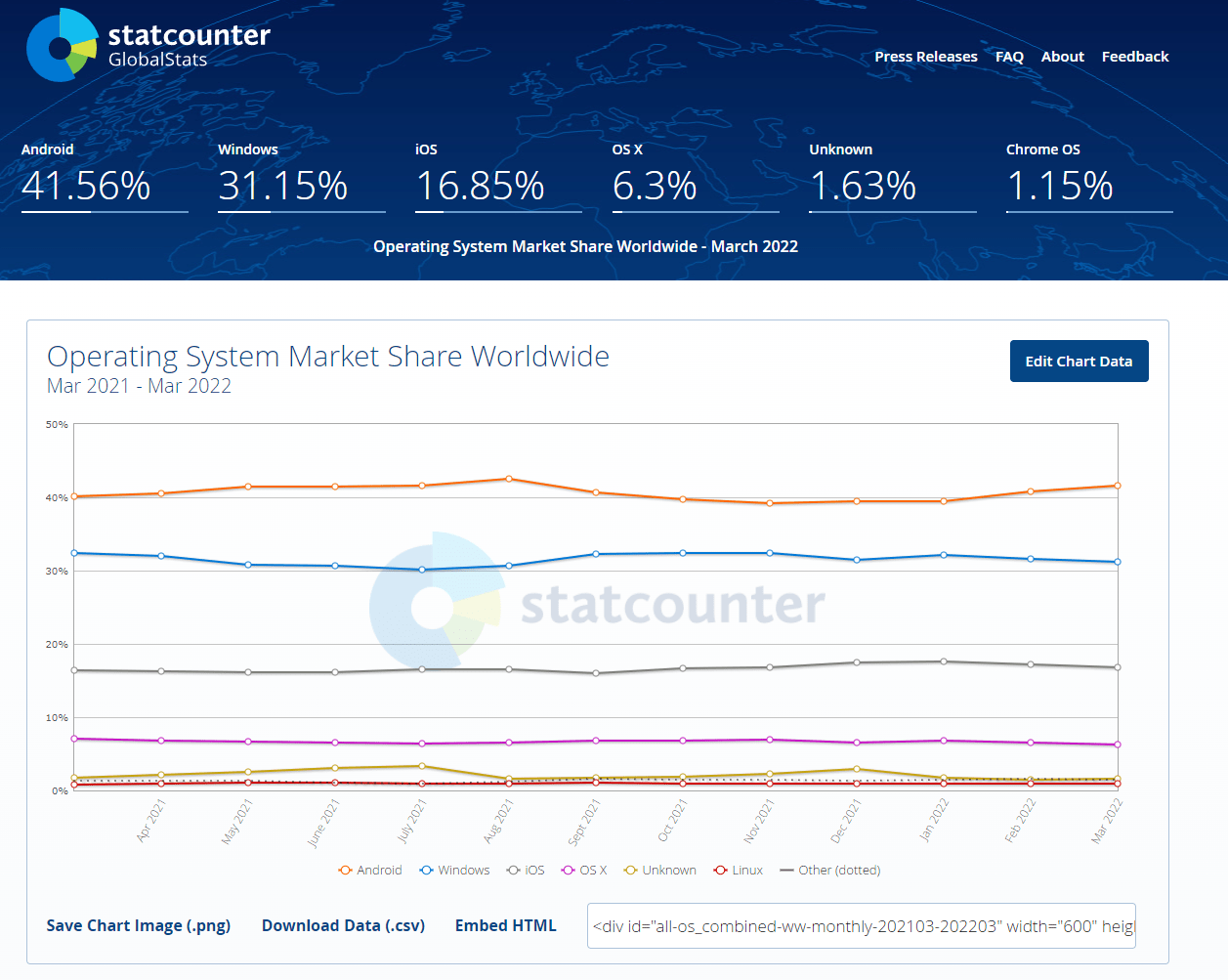

When all platforms are taken into consideration, including computers, tablets, and smartphones, Android has 41.56% of the global operating system market share, while Windows from Microsoft (MSFT) comes in 2nd with 31.15%, and iOS comes in 3rd with 16.85%.

statcounter

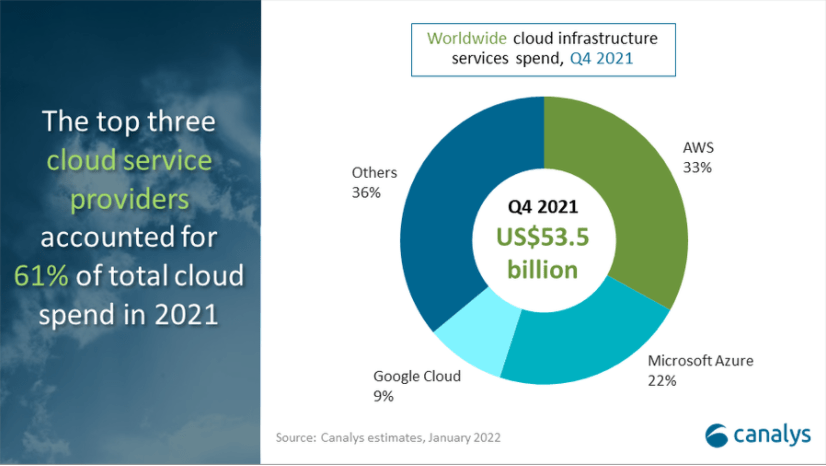

As an honorable mention, Google Cloud has 9% of the worldwide cloud infrastructure spend, which places them in 3rd place behind Azure from MSFT with 22% and AWS from Amazon (AMZN) with 33%. This is significant because YOY Google Cloud has increased its revenue by 47.07%, and over the next 8 years, the worldwide cloud infrastructure spend is expected to increase to $1.55 trillion. If Google Cloud can maintain a 6.5% market share in 2030, it would place Google Cloud’s revenue at $100.75 billion.

Canalys

Technology is embedded into society, and Alphabet owns and operates the 3rd largest cloud infrastructure platform and the most used browser, search engine, mobile operating system, and overall operating system. It doesn’t matter if we experience higher inflation, a recession, or even a depression; these products from Alphabet will be used by billions of people daily.

Alphabet’s Financials Have Dominated Throughout 2021 As Inflation Rose To 7%

Alphabet, hands down, has one of the best sets of financials of any publicly-traded company.

Income Statement

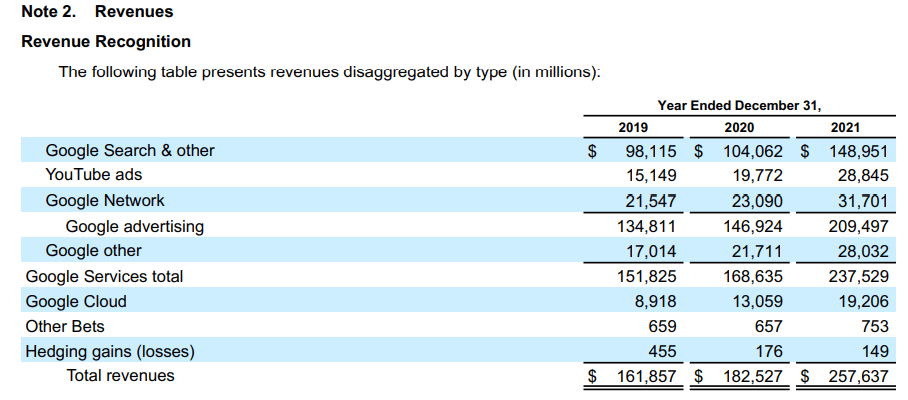

Alphabet has increased its revenue by $75.11 billion (41.15%) YoY from $182.53 billion to $257.64 billion. Search saw a 43.14% ($44.89B) increase YoY, while YouTube ads revenue increased 45.89% ($9.07B) YoY, and Google Cloud grew by 47.07% ($6.15B) YoY.

Alphabet 10-K

Growing a company’s revenue isn’t enough because growth without profits equals irrelevancy. I want to make sure a company isn’t just spending its way to a better price to sales ratio so the revenue growth needs to exceed the growth in the cost of revenue and total operating expenses. In 2021 Alphabet’s cost of revenue grew by $26.21 billion while its total operating expenses grew by $11.41 billion. Alphabet’s revenue growth exceeded its overall expense growth by $37.49 billion or 99.65%.

The gross profit margin because it indicates how much of a company’s revenue goes directly to producing it and how strong the moat around their business is. If you read Warren Buffett and the Interpretation of Financial Statements on page 34 of the Kindle edition, it says:

As a very general rule (and there are exceptions): Companies with gross profit margins of 40% or better tend to be companies with some sort of durable competitive advantage. Companies with gross profit margins below 40% tend to be companies in highly competitive industries, where competition is hurting overall profit margins (there are exceptions here, too).

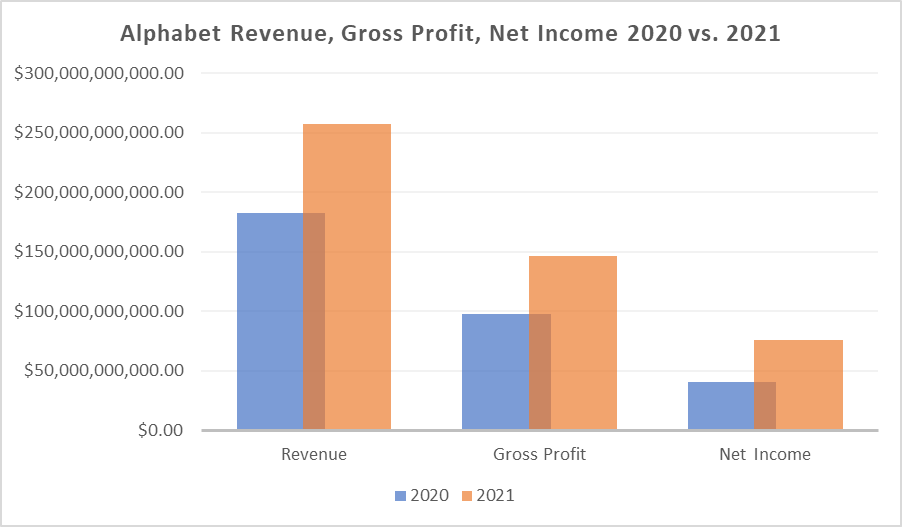

Alphabet’s gross profit grew by 50% ($48.90B) in 2021 to $146.7 billion. This places Alphabet’s Gross Profit margin at 56.94% ($146.698 / $257.637), which is significantly larger than the Oracle of Omaha’s magic number of 40%.

Generating profits is more important than ever during periods of inflation, as the next economic cycle is often a recession. Having a solid war chest and the ability to generate profits can be the difference between relevancy or chapter 11. In 2021 Alphabet operated its own cash machine as it generated $76.03 billion in net income. This was an 88.81% YoY increase ($35.76B) during a period when inflation ran rampant. Alphabets 2021 net income number isn’t a fluke as it increased YoY sequentially over the previous three years. This also puts Alphabet’s profit margin at 29.51%. Almost 1/3rd of every additional dollar in revenue goes directly to the bottom line, and Alphabet increased its revenue by $75.11 billion in 2021.

Steven Fiorillo / Seeking Alpha

Cash Flow Statement

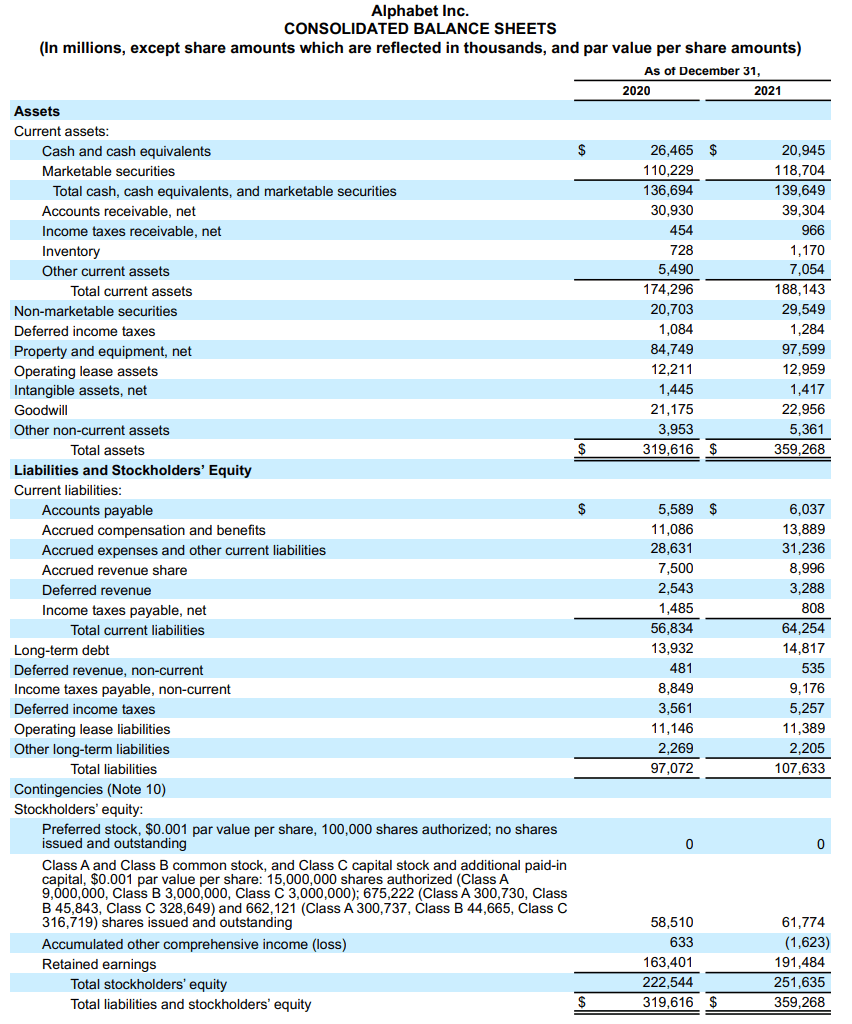

Free Cash Flow (FCF) could be the most underrated and most important financial metric to look at as this is how companies can repay debt, pay dividends, buy back shares, make acquisitions, or reinvest in the business. During inflation, you want to be in companies that not only generate positive FCF, but are growing their FCF. I always want to see a company that can grow its cash from operations while its capital expenditures stay relatively sideways.

Alphabet is an anomaly in this aspect because its annual capital expenditures declined by -499 million over the previous 3 years while its cash generated from operations increased by $43.68 billion (91.06%) to $91.65 billion. In 2021 Alphabet produced $67.01 billion in FCF. When a company generates this type of FCF, it can make almost any acquisition desired or manufacture earnings by repurchasing common shares and directly increasing its EPS.

Steven Fiorillo / Seeking Alpha

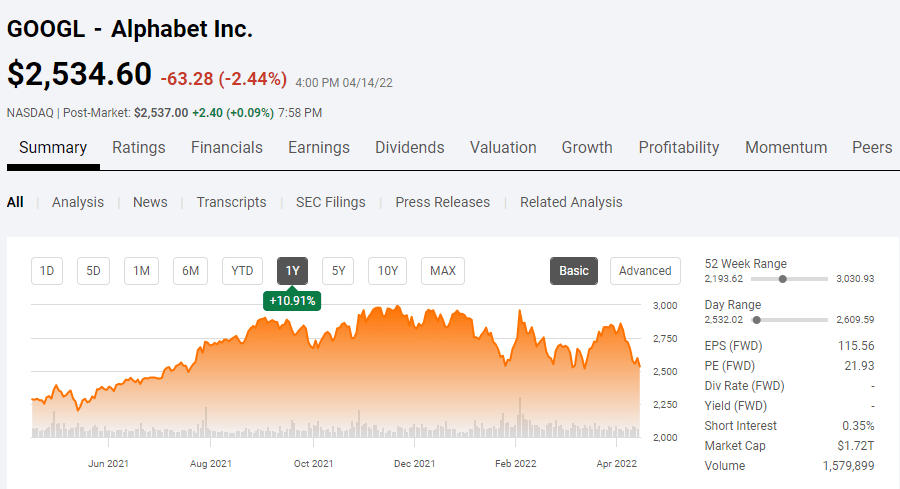

Balance Sheet

Alphabet has one of the strongest balance sheets in the entire market. A balance sheet can make or break a company. In a rising rate environment where inflation is rising, and there is no guarantee that additional costs can be passed onto the consumer, it’s more important than ever to have a fortress of a balance sheet.

Alphabet has $107.63 billion in total liabilities, of which $64.25 billion is long-term debt. Under current assets, Alphabet has $139.65 billion in total cash and equivalents on the books. When marketable securities are under current assets rather than non-current, they can be liquidated quickly if needed. With one check and a stroke of the pen, 100% of Alphabet’s total liabilities could disappear without tapping the debt markets. Alphabet could eliminate its entire long-term debt pile and still have $75.4 billion in cash left over on the books. This doesn’t even include the tens of billions in net income Alphabet generates in profits each quarter. Alphabet may have the strongest balance sheet in the entire market; if not, it’s definitely in the conversation. Either way, inflation or a recession will not impact Alphabet’s balance sheet.

Alphabet 10-K

Why Alphabet Is Bound To Outpace Inflation In 2022?

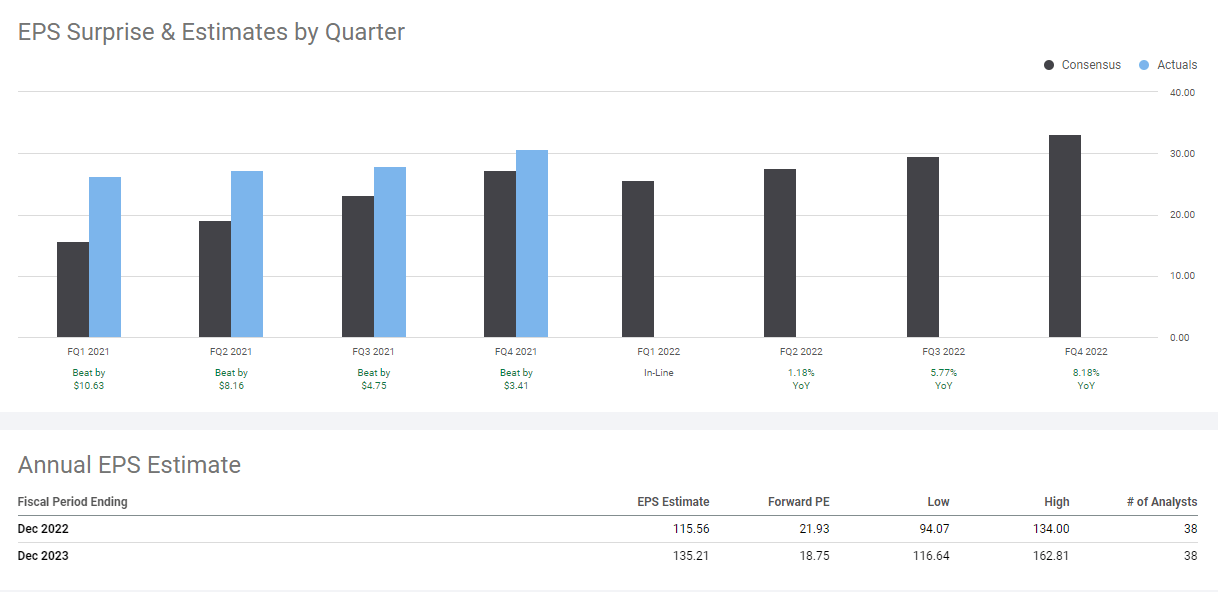

Alphabet is trading off its 52-week high of $3,030.93 by -16.38% (-$496.33) and its recent high established on 4/4/22 of $2,859.43 (-11.36%). Alphabet’s current price of $2,534.60 is still an appreciation of 10.91% over the past year, while inflation has just about doubled to 8.5%. Strong earnings could put Alphabet’s share price past $3,000 in just several trading sessions.

Seeking Alpha

Alphabet also has a major catalyst on the horizon, and it’s their 20-1 stock split. A stock split doesn’t add value to the company initially, but it creates opportunity. The bottom line is investors aren’t banging on the door to buy shares of Alphabet due to its $2,534.60 share price. Alphabet’s trading volume was 1.58 million shares on 4/15, while AAPL saw 75.33 million in shares traded.

Normally when a board of directors declares a stock split, it’s taken as a vote of confidence that its company’s share value will continue to increase, which is a bullish indication. A 20-1 split would put Alphabet’s share price around $126.73, becoming more attractive to new investors and retail investors. At $126.73, the volume will increase, increasing Alphabet’s liquidity in the market as more shares are being traded. Stock splits can also indicate a positive signal to rating agencies which could positively impact the share price. We will also see the derivative markets open up as options become affordable outside of institutional investors. A May 20th call option just out of the money with a strike of $2,550 had a last sale of $99.01. Buying a naked call would cost $9,901, or having the ability to sell a covered call would mean owning 100 shares of Alphabet or having the equivalent of $253,460 in cash as collateral. An AAPL May 20th call just outside the money at $170 had a last sale of $4.10. You could buy the naked call for $410, and having the ability to sell a covered call would mean owning 100 shares of AAPL or having $16,529 in cash as collateral. The 20-1 split is going to have long-lasting positive effects in the derivative markets as options volumes are bound to increase.

I believe we’re going to see drastic demand for shares of Alphabet as they become accessible to the vast majority of investors. Trading volumes should increase as we see a flood of buy orders due to demand for the newly priced shares.

Most importantly, it comes down to earnings, and Alphabet is expected to crush earnings throughout 2022. Increased earnings correlate to increased profits, and this is a category Alphabet isn’t short on. A critical component for share appreciation is expanding earnings and in an inflationary environment, it becomes harder for companies to increase their earnings potential. In 2021 the consensus was that Alphabet would generate $85.28 in EPS. Alphabet beat the consensus estimate each quarter and delivered an additional $26.95 (31.60%) in earnings as they produced $112.23 in EPS. In 2022 the consensus estimates have increased by $30.28 (35.51%) from 2021 as the street expects Alphabet to generate $115.56 in EPS in 2022. Alphabet’s growth is far from over, and the street is expecting big things in 2022 from Alphabet, and I bet they will deliver. The combination of big earnings beats, a stock split, and YoY revenue and profit growth should put Alphabet on easy street toward outpacing inflation in 2022.

Seeking Alpha

The Risks Of Investing In Alphabet

No investment comes without some degree of risk. While I am very bullish on Alphabet, some risks should be considered. In 2018, the EU had fined Alphabet $5 billion for manipulating Android mobile devices to give the Google search engine an advantage over rivals. In 2021, the EU’s General Court upheld a European Commission ruling against Alphabet for antitrust infractions, and they are facing another $2.8 billion fine. Alphabet has also had its share of problems stateside as the U.S. Justice Department and 11 states had filed a lawsuit in 2020 alleging that Alphabet used its market power to fend off rivals.

When you consider Alphabet’s dominance, especially since Google Chrome has 64.53% of the global browser market share and Google has 91.56% of the search engine market worldwide, the word monopoly becomes synonymous with Alphabet. It gets even worse when Android enters the conversation, as it has 71.7% of the mobile operating system market share worldwide. While Alphabet can pay billions in fines and not feel the repercussions, it’s putting them right in Washington DC’s crosshairs. Alphabet has been on Capitol Hill and testified more than they would like. A common theme among some lawmakers that has gained traction is Alphabet has become a monopoly. Alphabet faces the risk that its conglomerate is forced to break up if they are deemed a monopoly by the United States Government. If political opposition continues to grow, Alphabet could find themselves on the hill more frequently and pressures from DC could intensify with an unfavorable ruling against Alphabet.

Conclusion

The old school mentality of which sectors should be your defensive plays during volatility, inflation, or recessions needs to be revisited and rewritten. The world in 2022 is completely different than the late 70s and early 80s when inflation was at these levels. The best companies during hard economic environments are ones that are growing revenue, gross profit, net income, FCF, and EPS while maintaining strong balance sheets. Alphabet checks off all of these boxes in spades. Utilities have always been a safe haven, and I am a shareholder of Southern Company (SO), but when it comes down to it, Alphabet generated more in net income ($76.01B) than SO did in revenue ($22.41B) throughout 2021. The same goes for the king of consumer staples, Proctor & Gamble (PG). PG generated $76.12 billion in revenue in 2021, which is basically the equivalent of Alphabet’s pure profit. The best defense is always a strong offense because you don’t have to rely on defense. Alphabet has $139,65 billion in cash, generates $76 billion in net income, grows its revenue by double digits YoY, and is projected to expand its earnings in 2022 and 2023. Alphabet is a unicorn making just about every other company look uninvestable. I think 2022 will be a huge year for Alphabet; the stock split will drive volume, and earnings will be extraordinary. These are why I am currently a shareholder; I plan to buy more and will be using shares of Alphabet to beat inflation.

Be the first to comment