Scott Heins

ALLY: The Battering Carries On

Leading consumer finance company Ally Financial Inc. (NYSE:ALLY) has seen its stock crumble further after our previous update, as buyers spurned our thesis of a bottoming process. Notably, we didn’t glean any signs of a bear trap that could have offered a more robust defense. However, we were confident that the downgrades in Ally’s earnings projections could have reflected significant pessimism.

Notwithstanding, the market had other ideas, as macroeconomic headwinds have worsened. With the global economy stuttering toward a recession in 2023, consumer discretionary stocks have fallen further, as seen in the underperformance of the Consumer Discretionary Select Sector ETF (XLY) against the S&P 500 (SPX).

Given Ally’s exposure to automotive finance, investors need to price in the attendant risks, given the battering seen in auto stocks. At a recent conference, Ally also said these risks could worsen in 2023. The economists’ consensus also points toward what is probably the most well-telegraphed recession in recent times.

As such, worries over Ally’s exposure to auto leaders, including used car dealers like Carvana, have likely caused some investors to panic, given the massive run-up from its 2020 lows. Hence, investors sitting on massive gains from those lows have likely used the opportunity to take more profits and cut their exposure to sectors/industries that are more sensitive to consumer discretionary spending.

Goldman Sachs Likely Preparing For A Recession

Moreover, Goldman Sachs’ impending job cuts in January 2023 have likely not helped matters. CEO David Solomon confirmed recent reports of headcount cuts in a year-end note to employees. As such, even though the bank’s economists do not anticipate a recession in 2023, its management team is taking no chances.

Moreover, credit unions have also intensified their competition against Ally and its peers, even as the Fed ramped up its interest rate hikes to combat elevated inflationary pressures.

A recent report from Experian shows that credit unions have continued to gain market share and have risen as the top lender for used car loans. Management also highlighted the competition with the credit unions in a recent December conference, as CEO Jeff Brown articulated:

You see the credit unions play in that space. What has transpired over the course of this year is credit unions, up until recently, really had not moved [pricing]. And so, obviously, the big banks that play there were not capturing any volume. All paper was going to the credit unions, and we can argue all the reasons why. We don’t think that was prudent decisioning [by] the credit unions. But again, they sort of [switched] posturing recently, but the big banks that often talk about playing in auto basically saw no flow there. (Goldman Sachs US Financial Services Conference)

So, with a worsening economy, faltering auto market, and more intense competition from not-for-profit credit unions, is there still hope for Ally Financial to recover from its malaise in 2023?

ALLY: Estimates Have Been Slashed

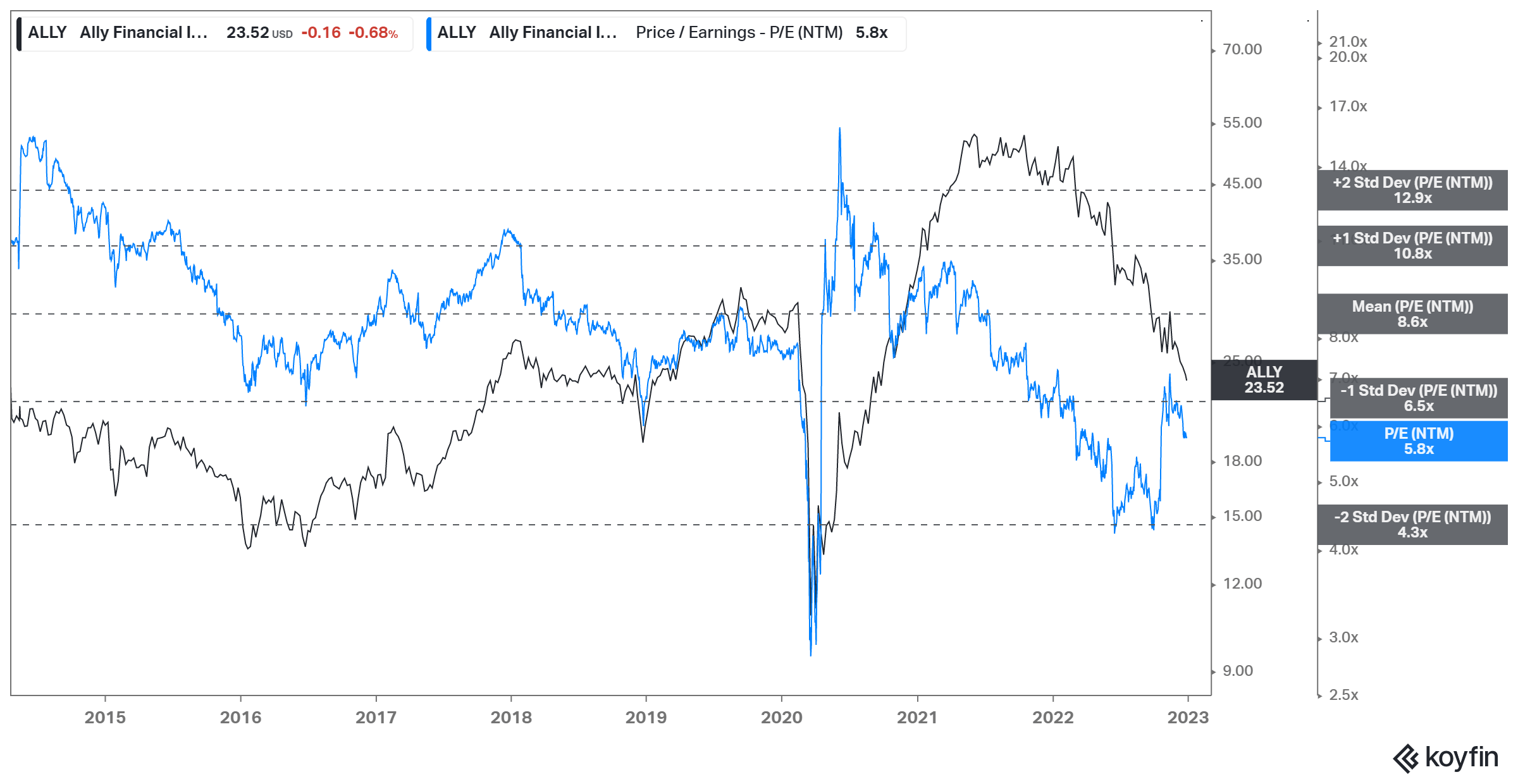

ALLY NTM P/E valuation trend (koyfin)

As seen above, ALLY’s NTM P/E fell to the two standard deviation zone under its 10Y average in October. However, the earnings estimates cut by Wall Street analysts after its Q3 earnings sent its valuation surging back up. Hence, we believe the Street has likely penciled in poor execution risks in 2023, which could help ALLY sustain a recovery. Is it reasonable?

Analysts now expect Ally Financial to post an adjusted EPS growth of -27.5% in 2023, way below its broad industry peers’ average of -8.3% (according to Refinitiv data).

Takeaway

Notwithstanding, we did not glean an obvious valuation dislocation against its closest peers. Accordingly, its NTM P/E of 5.8x is in line with Capital One Financial’s or CapOne’s (COF) 5.6x but is below Synchrony Financial’s (SYF) 6.5x. Brown also highlighted that Ally competes directly with CapOne, suggesting the market de-rated both lenders broadly.

Our price action analysis suggests that ALLY continues to follow a well-established medium-term bearish bias, with no signs of a capitulation or bear trap. Hence, further downside volatility cannot be ruled out, even though its valuation has been pummeled.

Rating: Buy (reiterated)

Be the first to comment