Cancan Chu/Getty Images News

Back in November of last year, we saw Alibaba Group Holding Limited (NYSE:BABA) as a play positioned at the junction of value and growth. The best of both worlds. We chose to resist the temptation to go long however, as we felt BABA had a bumpy road ahead with the implosion of its home country’s mega real estate bubble. The valuation was getting compelling on a price-to-sales basis, we still chose to remain on the sidelines back in May and provided our reasoning.

But in a deflating real estate environment, with spiraling costs, nothing stops this from heading lower to 1.5X or lower. The earnings will always make it look cheap at whatever price you check it at, but they are destined to go lower. We think the upcoming conference call will once again reiterate the challenges of retail when real estate drops and energy pops. We think the stock will remain range-bound until the earnings picture improves.

Source: Bears Have Been Dead On Target

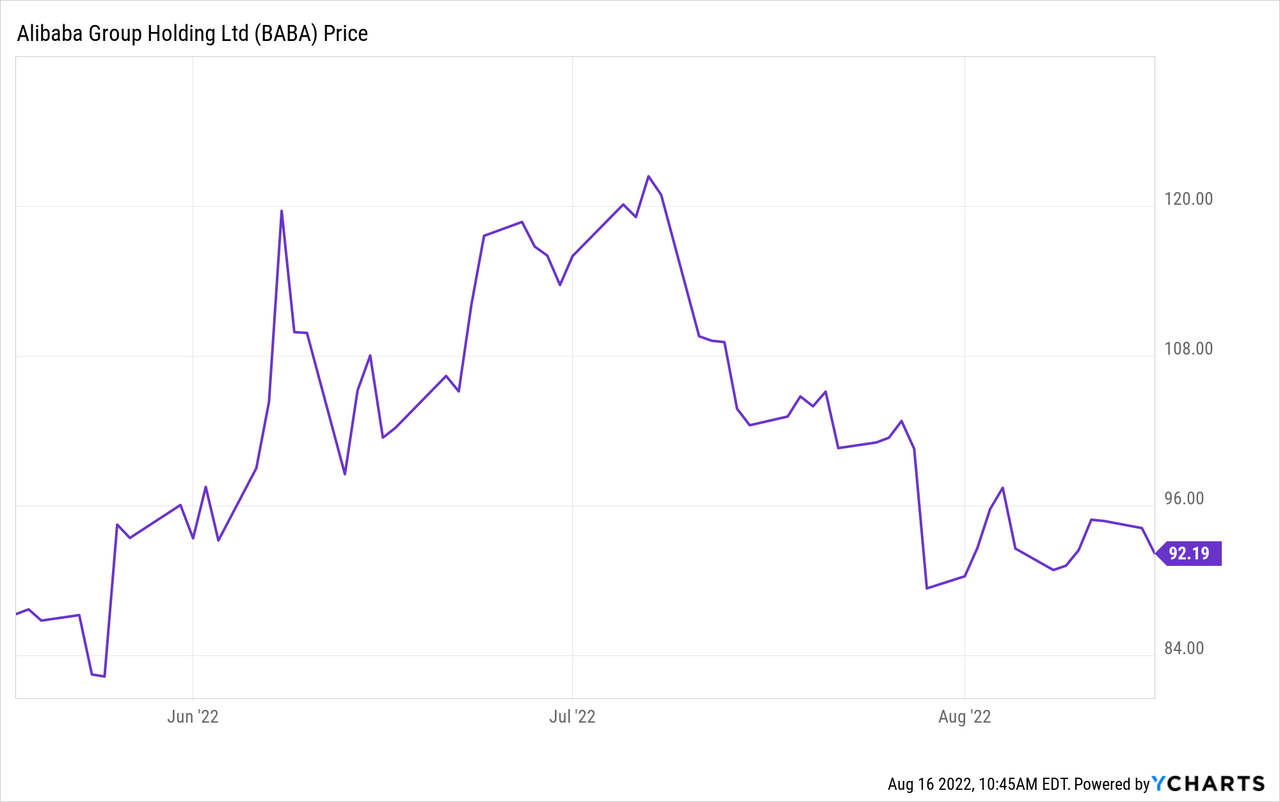

The stock price soared after its Q4 results but settled to a level only a tad higher since our last piece.

Recent market focus has been on a potential delisting as many Chinese firms are already going that route.

PetroChina Co. (PTR) dropped 3.4% in Hong Kong, while China Life Insurance Co. (LFC) and China Petroleum & Chemical Corp. (SNP) lost more than 2% each. Sinopec Shanghai Petrochemical Co Ltd. and Aluminum Corp of China Ltd. (ACH) also fell. The rush to leave the US market was seen as reflecting rising bilateral tension and a lack of progress in reaching agreement over giving American regulators better access to Chinese firms’ financial data.

Source: Bloomberg

BABA obviously has been in the rumor mill as it has faced numerous questions over its audit standards. Meanwhile, the analysts continue to vigorously fine tune their estimates for this giant.

Seeking Alpha

Let’s review the results that have been released since we last wrote on this retail giant and provide an update to our outlook.

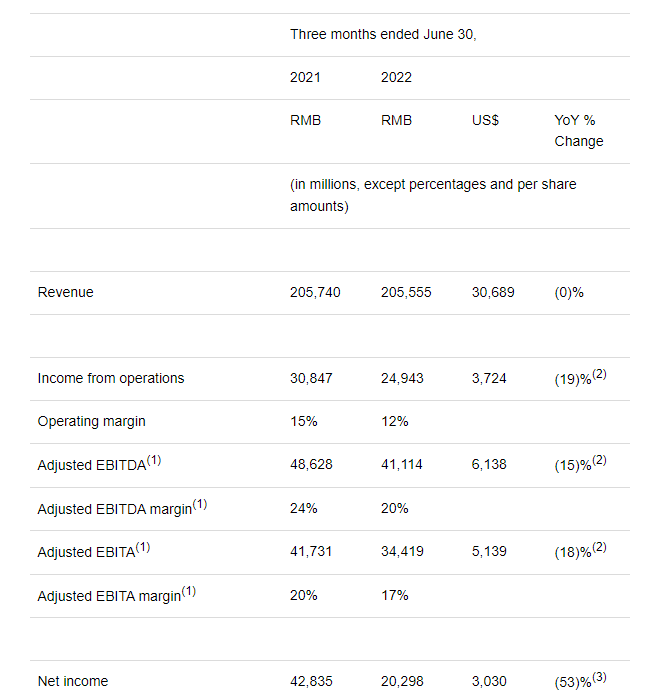

June 2022 Results-Growth Be Gone

If we move past the analyst estimates, we can appreciate just how rough these numbers were for the former growth darling.

BABA Results

Revenue flatlined and operating margins dropped by about 20%. Adjusted EBITDA was also lower and net income was cut in half. These numbers were despite the Cloud segment still managing to pull a 10% growth rate year over year. The stock actually rose on the news and that was of course due to estimates being lowered enough for a “beat”.

Outlook

If there is one hill analysts will die on, it will be their collective refusal to ever price in a recession. Hence earnings will have only a single direction. Up. In the case of BABA, the first quarter did jolt them to price an earnings decline, but there on, again it is onwards and upwards.

Seeking Alpha

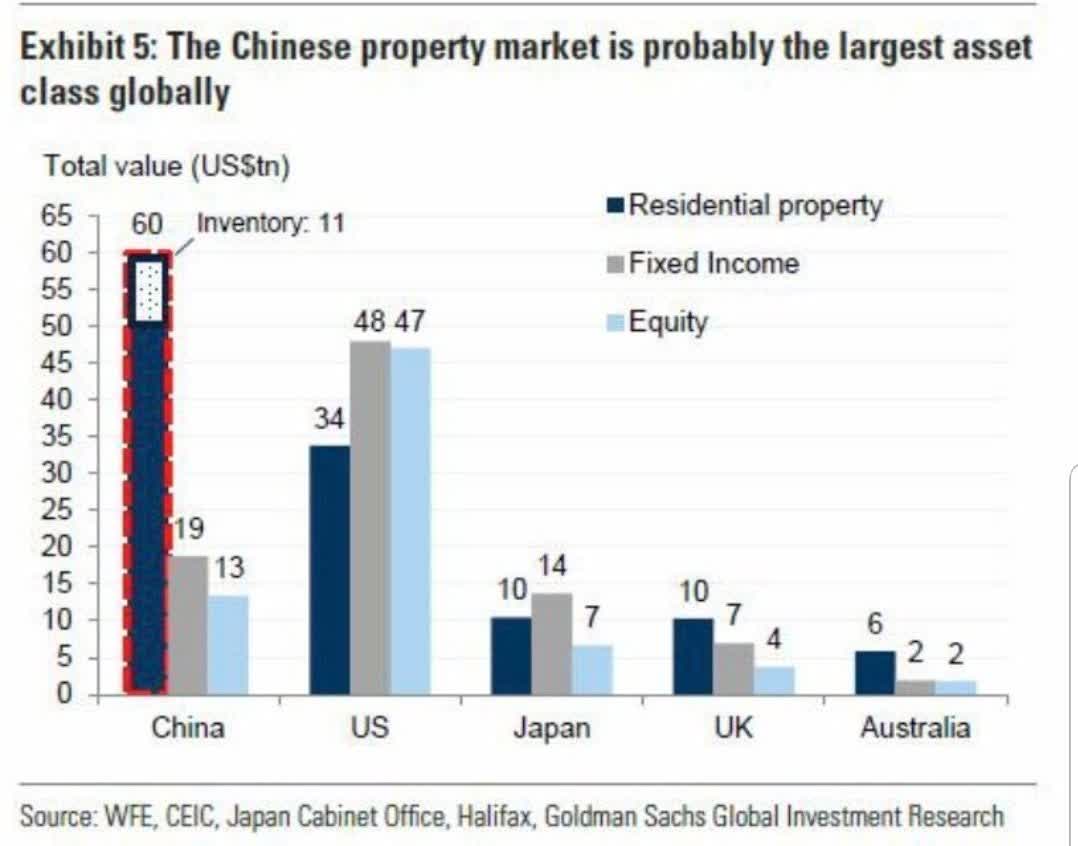

While anything is possible, China currently faces one of the most challenging environments it ever has. We are not even referring to the self imposed and self inflicted “Zero-Covid” policy. We are referring to the collapse of the largest bubble known to mankind.

Goldman Sachs

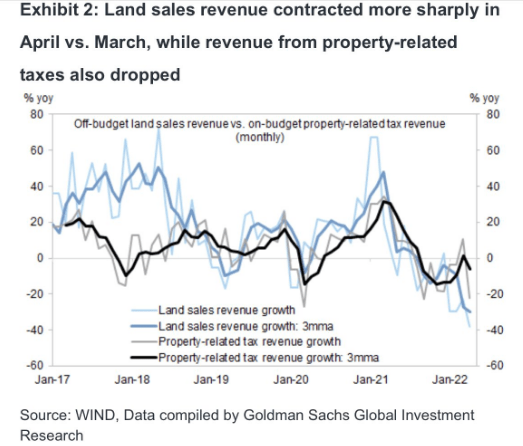

In our last coverage, we showed that the leading indicators of forward sales looked grim.

Goldman Sachs

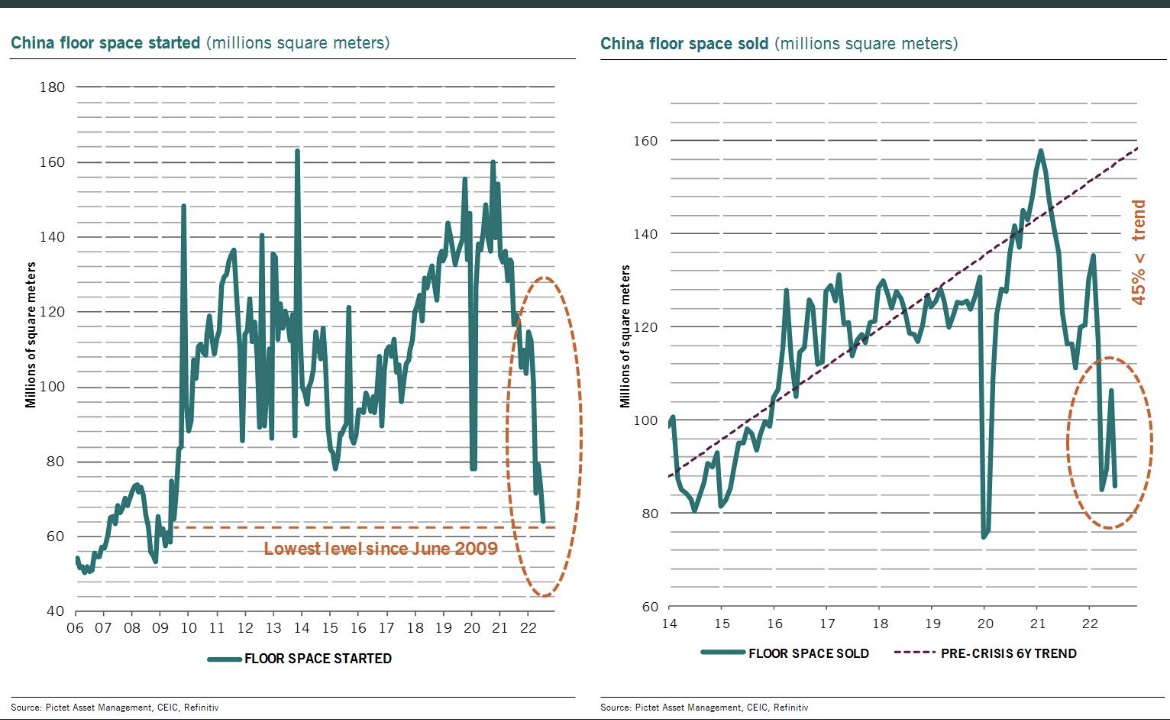

Well guess what? Those leading indicators were completely accurate. China floor space started has now collapsed to 2009 levels.

Pictet Asset Management

The run rate is now approaching the worst point of COVID-19 for the country. Is this coming from the Zero COVID policy? Yes, there is definitely some contribution, but the bulk is coming from the bubble going kaput. China built and built to power their GDP and all the animals (not just the chickens) are coming home to roost.

Fifty million empty flats threaten to plunge China’s troubled property market further into crisis, warns think tank

The average vacancy rate in mainland China is 12.1 per cent, according to BRI, meaning millions of empty units could flood the market

Now the property boom is over, the unoccupied homes are beginning to feel like a burden for their anxious owners

Source: SCMP

Adding fuel to this overbuilt paradise is the mortgage boycott that is gaining steam.

Some buyers across China have refused to pay mortgages for unfinished projects for months now, but this week it coalesced into a group movement. A list that started with just 30 projects grew to more than 300 by last weekend. Mortgages aren’t as common in China as in the West: Only 18 percent of homeowners have one, and it’s more common to borrow money from extended family, who invest collectively in a property.

The movement against the presale system puts as much as $350 billion in payments at risk, and Chinese authorities have already moved to censor it. However, the crisis continues to feed on itself: As developers’ cashflow dries up, even more projects are being suspended, leaving more consumers angry and fearful that they may never be finished. The authorities are now leaning on lenders to bail out projects to help keep developers afloat.

Source: Foreign Policy

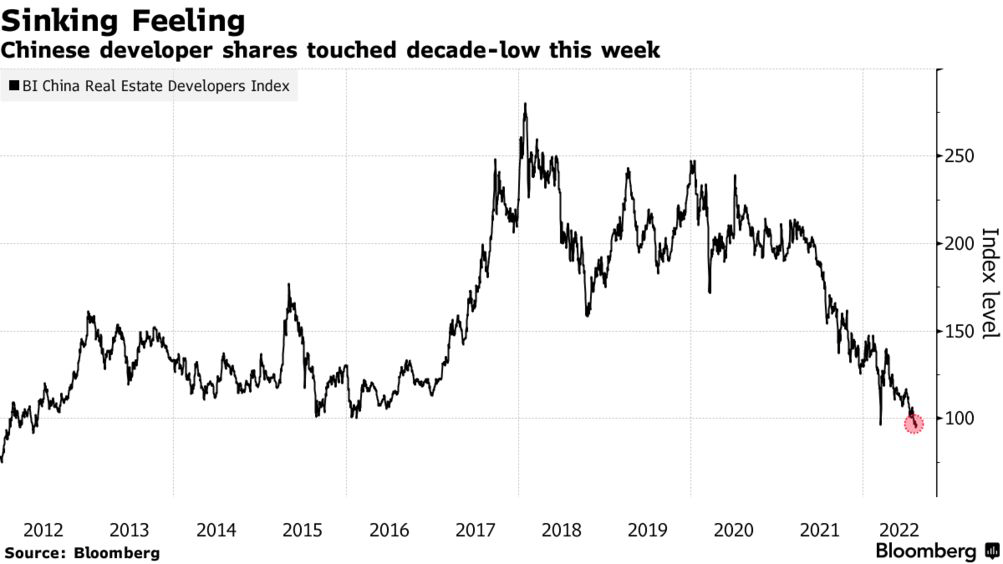

Chinese developers are pretty much hanging on with the assumption that there will be some state rescue.

Bloomberg

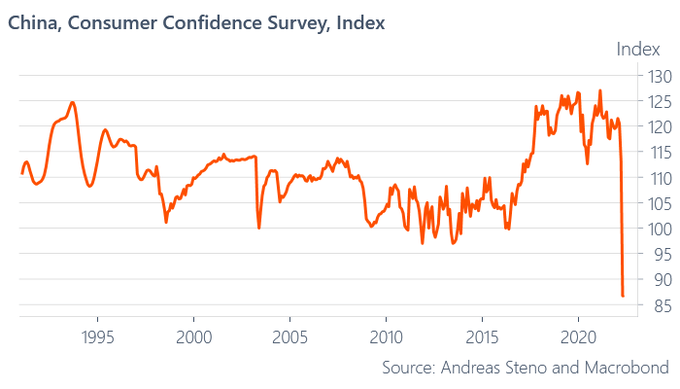

All of this turmoil has sent Chinese consumer confidence down with the velocity of a “StableCoin”.

Macrobond

Verdict

The current situation makes us wonder if the macro is remotely conducive to the kind of sales growth being priced in.

Seeking Alpha

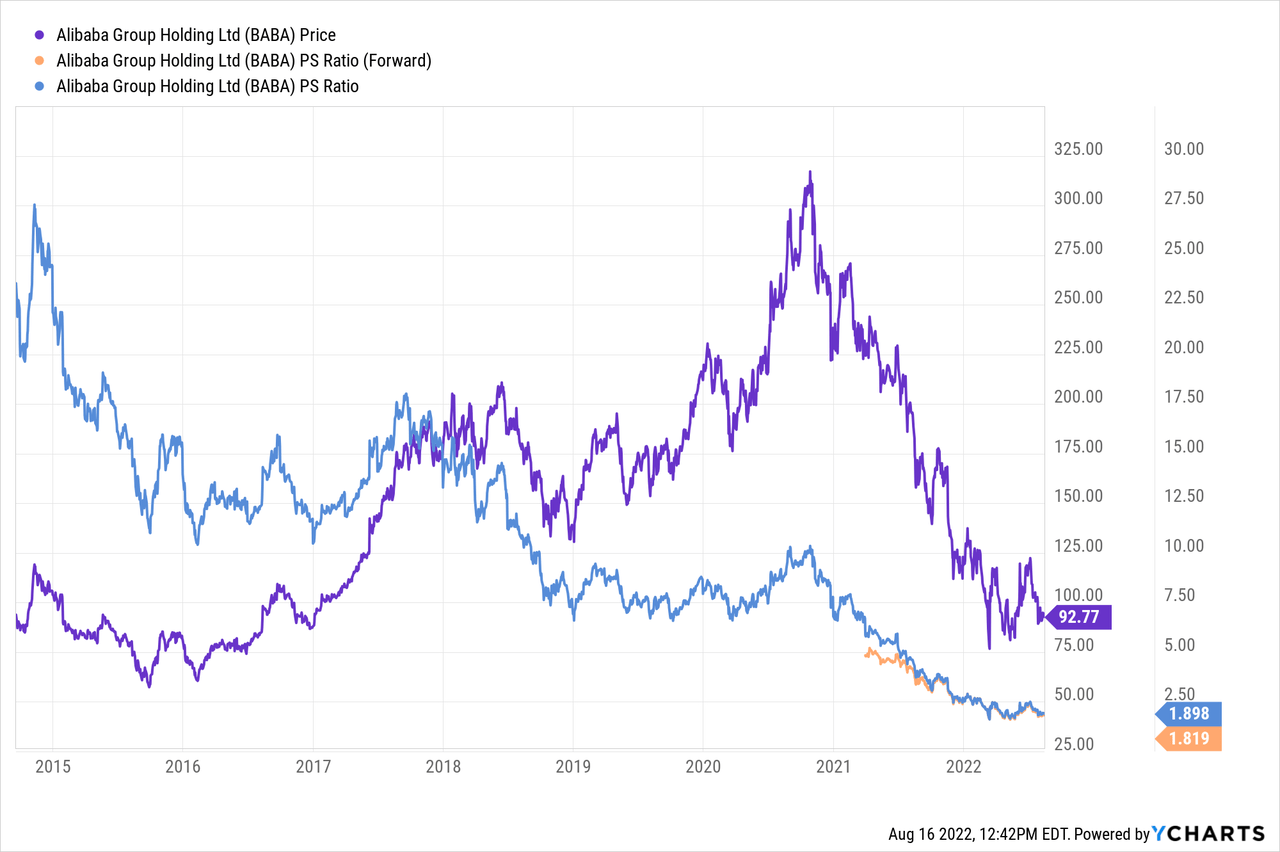

The latest retail sales grew at just 2.7% promoting a cut in the MTLF interest rate by the People’s Bank Of China. The current environment remains extremely difficult and investors may want to exercise prudence. Yes valuation has compressed, BABA is buying back shares and even laying off people to improve profitability.

At 1.8X sales you are not remotely paying as much as those cowboys ready to pony up 10X sales at the 2020 peak. So the odds are in your favor, but the risks are enough to make this a value trap and we are staying out.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints

Be the first to comment