Lintao Zhang/Getty Images News

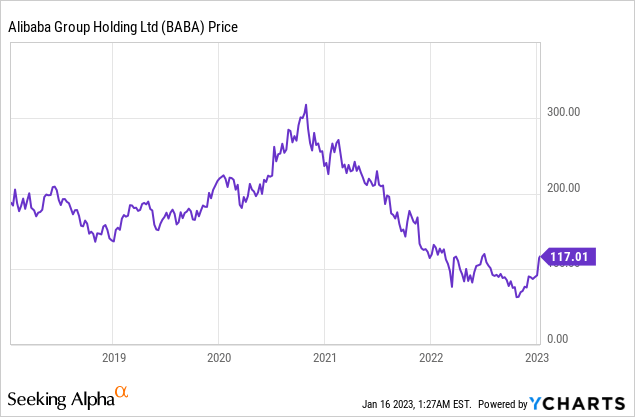

Alibaba (NYSE:BABA) is a Chinese ecommerce titan often considered as the “Amazon of China”. Its outspoken founder Jack Ma, is a genius in many regards but he has clashed with the Chinese government in the past. In 2020, Jack Ma made a controversial speech in which he criticized the Chinese financial system. Then just a short time later, his “Ant Group” had its huge $37 billion IPO halted and Alibaba was smacked with a $2.7 billion fine, related to anti-monopoly dealings. Due to these factors and macroeconomic issues, Alibaba’s stock price was butchered by over 79% from its all-time high in October 2020. The positive news for Alibaba is Jack Ma has recently reduced his control of the Ant Group, which could pave the way for a future IPO. This would benefit Alibaba massively as the company owns approximately one third of the Ant Group. In addition, a Chinese regulator has recently snapped up “Golden shares” in Alibaba, which means they now have a financial stake in the company’s success. In this post, I’m going to break down the plethora of positive news for Alibaba stock, before diving into its technical charts and valuation, let’s dive in.

Golden Share Trade

Alibaba has been at the forefront of bad news over the past couple of years, but now we are seeing some positive news catalysts. An entity setup by the Cyberspace Administration of China, recently purchased a 1% stake in an Alibaba related subsidiary named Guangzhou Lujiao Information Technology, according to Chinese business records. The idea of this investment is so China can better control the video streaming company “Youku” and web browser UCweb. In China, the stakes purchased are known as “Golden Shares” which are really specialist voting shares. Some reports indicate these shares include a board seat and the ability to review content. Now although, in the west this may seem intrusive, there is no doubt that it will be positive for the stock price.

Ant Group – More Positive News

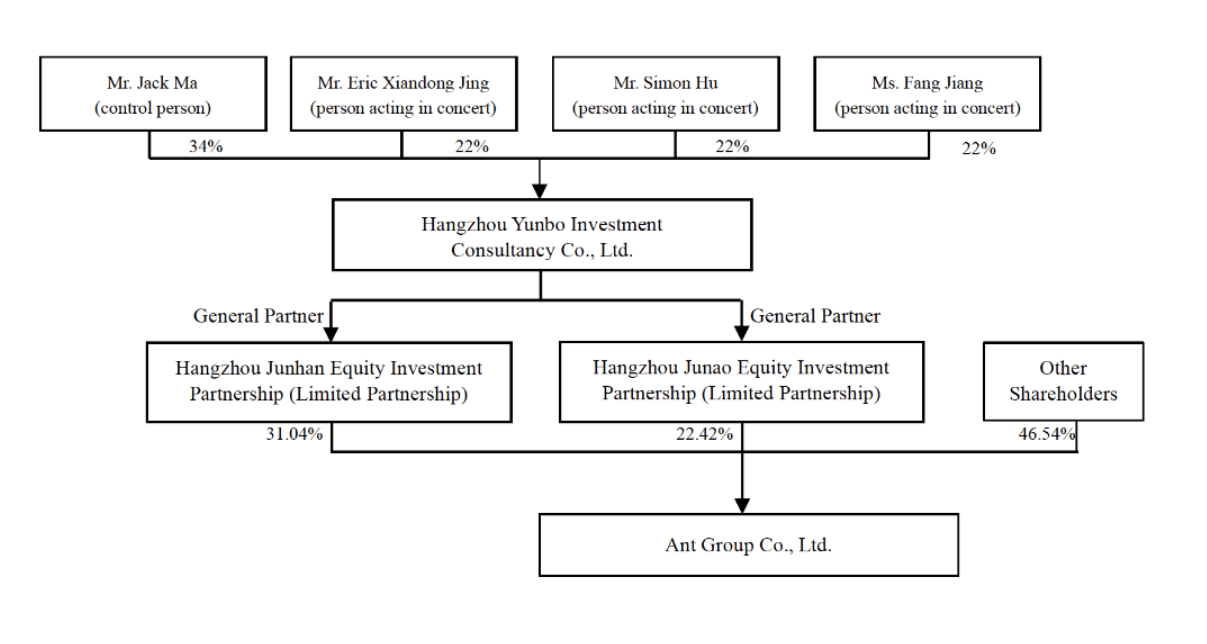

Alibaba owns approximately 33% of Ant Group or Ant Financial, which owns the ubiquitous Alipay, which is used by millions of consumers in China. As mentioned prior Jack Ma previously provoked the Chinese government/financial system, which we can assume impacted the proposed IPO of Ant Group and thus Alibaba. A positive is Ant Group has recently announced a new governance structure. Previously Jack Ma owned ~34% or was the “control person” of two Chinese holding companies namely Hangzhou Junhan Equity Investment Partnership and Hangzhou Junao Equity Investment Partnership. These then subsequently owned 31.04% and 22.42% of the Ant Group Co. Effectively giving Jack Ma control over the Ant Group, with over 50% of voting rights. This is likely an issue for Beijing given he clashed with the government/traditional financial system in China and is seen as a threat to many state owned banks.

Ant Group Holding Structure old (Ant Group)

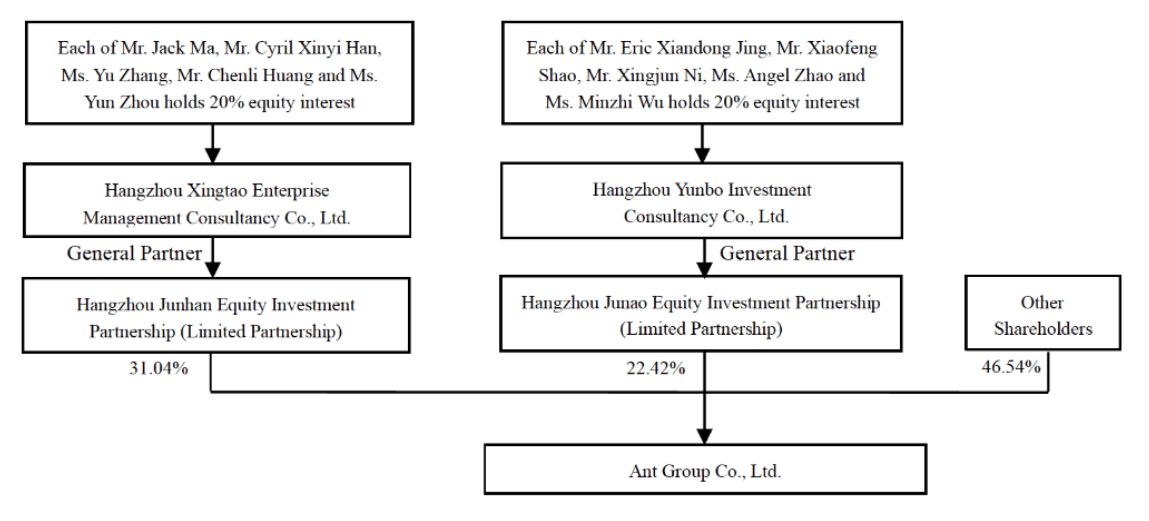

The positive is the new ownership structure includes Jack Ma and 5 other people which own a 20% combined stake in Hangzhou Xingtao Enterprise. This company then acts as a “general partner” for Hangzhou Junhan Equity Investment partnership, which then owns a 31.04% stake in the Ant Group. Taking a step back, as Jack Ma is one of five people, he effectively only has ~3.33% stake. Although I have seen reports which mention ~6%, which I am guessing includes the other 5 individuals. Either way, his voting rights have been significantly reduced from 50%. As Jack Ma is no longer the controlling person, this means a future IPO for Ant Group is possible which will directly help Alibaba.

Ant Group ownership structure new (Ant Group)

Capital Expansion Approval – Positive News

Another piece of positive news is the Ant Group has been approved for an extra $1.5 billion capital expansion by Chinese regulators. This means the Ant Group can now increase its capital from $ $1.16 billion (8 billion CNY) to $2.7 billion (18.5 billion CNY).

In other news, a government shakeup has meant China has a new foreign Minister named Qin Gang. He was previously the ambassador to the U.S and is seen as “pro” U.S-China relations, especially given his recent tweets.

SEC Checks Going Well

Chinese stocks have previously faced headwinds from the SEC, which has threatened to delist Chinese companies from U.S exchanges, which don’t comply with accounting disclosure. Previously China and the U.S butted heads on this topic, but over the past few months we have seen positive process. China agreed to cooperate with U.S demands and a delegation of U.S accountants/regulators were sent to Hong Kong to dive into the financials of U.S listed Chinese stocks. These investigators were reportedly given free access to interview auditors from leading account firms such as KPMG Huazhen LLP and PwC in China. Although the report hasn’t been completed yet, this is a positive for U.S-China relations.

Technical Analysis

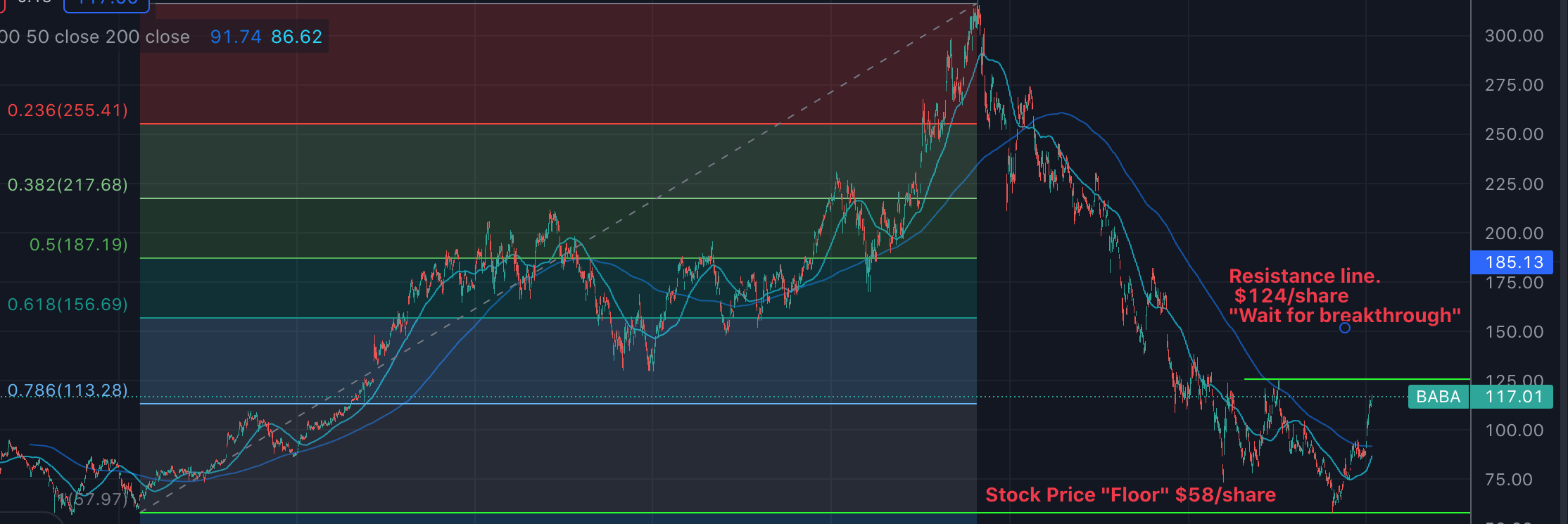

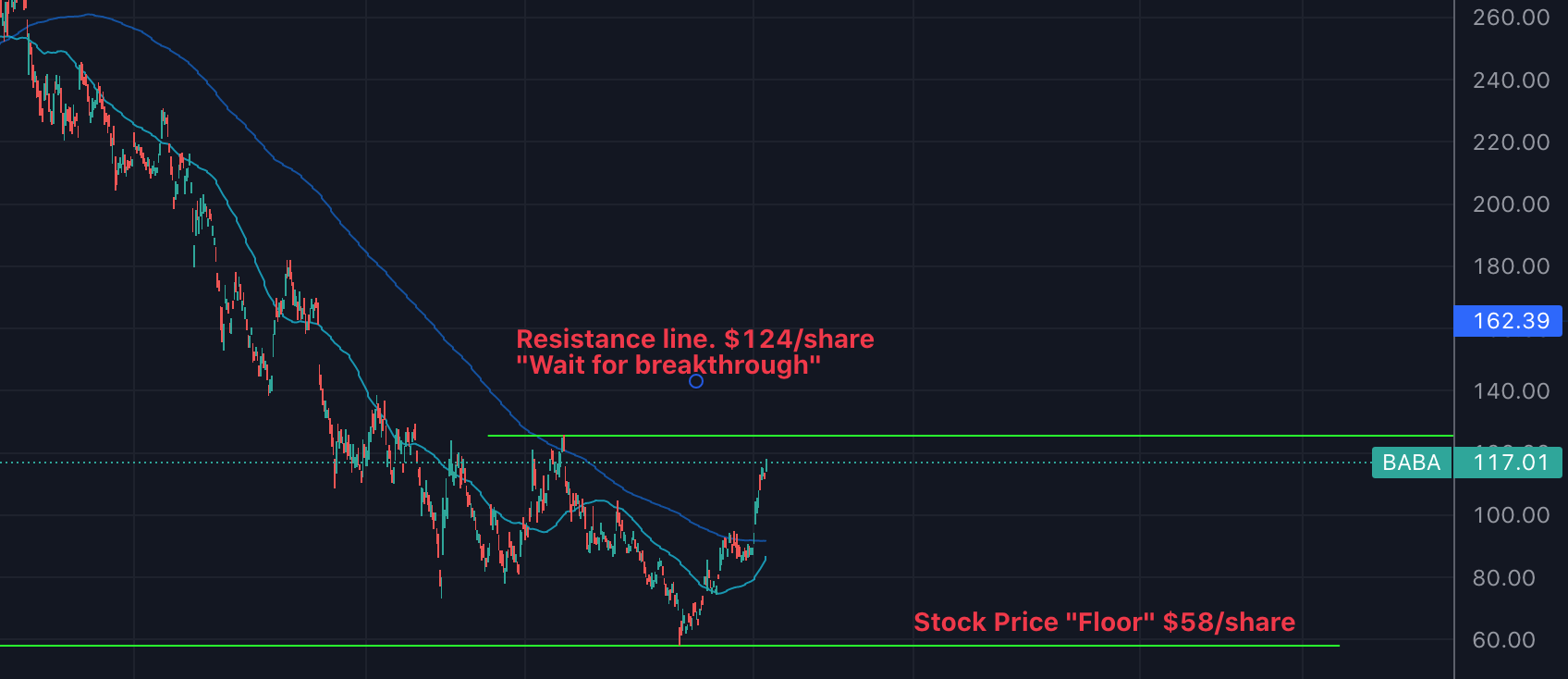

Generally when analyzing a stock I will review the “fundamentals” only such as a company’s revenue and earnings. However, it also makes sense to analyse the technical charts in order to get an idea of past zones where investors have seen value in a stock. If the chart below looks complicated, don’t worry I will walk you through what each part means. Starting on the left side, I have added a “Fibonacci retracement” indicator which is the colored lines/boxes. These help to indicate possible support and resistance lines, through a mathematical analysis of past data. From this indicator, and my own analysis I can see the stock price has a “floor” at ~$58/share. This is a strong buy point as it equates to the all-time low of the stock, which occurred in both 2016 and then again in November 2022.

Alibaba technicals 1 (Created by author Deep Tech Insights)

In the next chart below, I have zoomed in on the right side of Alibaba’s chart. In this case, I see the stock price bounced of the stock price “floor” of $58/share before increasing by ~80%. This would have been a great time to load up on Alibaba, but required a strong contrarian attitude given the market consensus. The stock price is now above both its 50 day moving average (blue line) and 200 day moving average (green line). This is a positive sign overall, but we could see some “reversion to the mean” which would be negative.

Alibaba technicals 2 (Created by author Deep Tech Insights)

The key factor we are looking for now is for Alibaba to “breakthrough” a resistance line at ~$124/share. If it can do this then the stock could blast higher, although it would make sense to wait for this. As if it hits the resistance line, the stock will likely drop to ~$90/share. A move either way could be driven by a “catalyst” such as a strong earnings report by Alibaba, or more positive news related to the Ant Group or the SEC. In the next section, I will review its valuation.

Advanced Valuation

I will not dive into Alibaba’s financials deep in this post, as I have covered it extensively prior, but here is a quick review.

Alibaba reported tepid financial results for the “September quarter” of 2022. The company reported $28.95 billion in revenue which rose by just 3% year over year in RMB. In addition, due to a strong U.S dollar this declined by ~6% year over year. This was mainly driven by lower demand in China’s domestic consumer market. This looks to have been mainly caused by hard lockdowns across China, which has caused the consumer to slowdown purchases. The good news is I expect this to be a cyclical change. In addition, I think the lockdowns will not occur forever and there have been many protests in China.

Alibaba reported adjusted earnings per share [EPS] of $1.81 in the September quarter, which surpassed analyst expectations by $0.16. This was driven by improving operating efficiencies across the company with lower sales & marketing expenses.

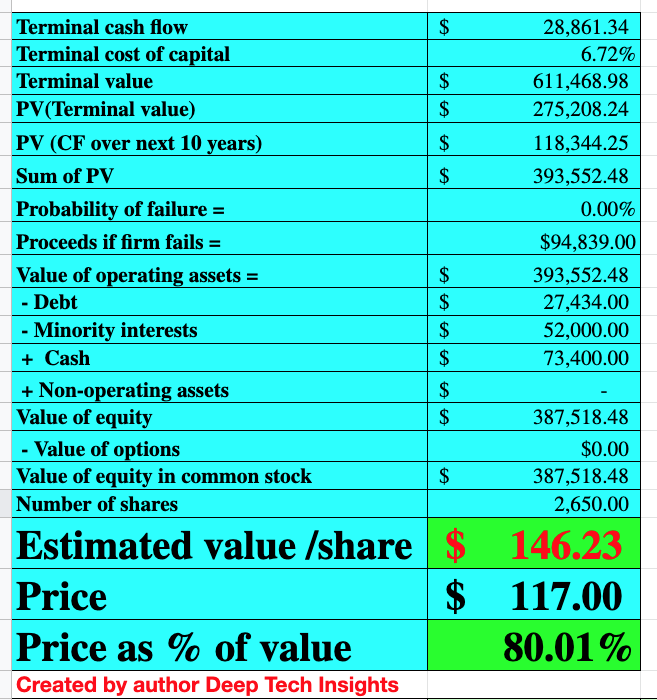

Diving into my advanced valuation model below, I have forecast 10% revenue growth for next year, and 12% revenue growth in years 2 to 5. I expect this to be driven by cyclical changes in the economy and stronger growth in years 2 to 5, which has been forecast by economists for China.

Alibaba stock valuation 1 (created by author Deep Tech Insights)

To increase the accuracy of the valuation model, I have capitalized R&D expenses which has lifted net income. In addition, I have forecast a pre-tax operating margin of 19% over the next 8 years. I forecast this to be driven by continued growth in Alibaba’s cloud segment, driven by digital transformation tailwinds. In addition, I forecast a rebound in ecommerce demand, which should drive repeat purchases and help keep customer acquisition costs reasonable.

Alibaba stock valuation 2 (created by author Deep Tech Insight)

Given these factors I get a fair value of $146/share, the stock is currently trading at $117/share at the time of writing and thus it is ~20% undervalued.

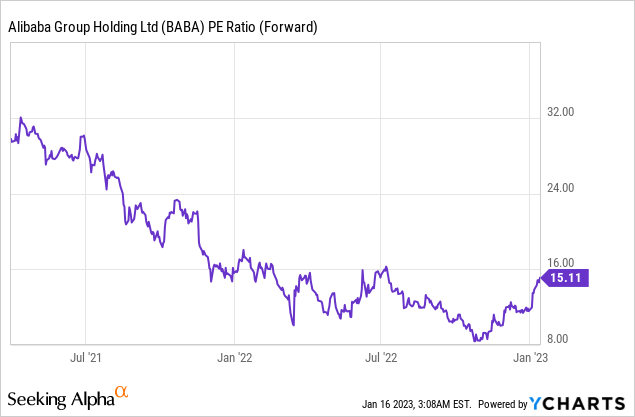

Alibaba also trades at a non GAAP P/E ratio = 14.94, which is close to 36% cheaper than its 5 year average. The company also trades at a price to sales ratio = 2.58, which is close to 64% cheaper than its 5 year average.

Risks

Chinese Government/Recession

When investing into Chinese stocks there is always three parties, you (the investor), the company and of course the Chinese government. The recent purchase of “Golden Shares” in Alibaba (indirectly), could be seen as a negative by some people who believe Beijing will have a greater say on how the business operates. This is possible, but personally I believe it will act as a positive as at least incentives are more aligned. In addition, many analysts have forecast a recession in 2023, in the U.S and the western world. This could impact China indirectly, as the company makes a large portion of its GDP from exports. A positive for China, is a recession hasn’t been forecast, although its GDP has been cut from 4.5% to 3.8%.

Final Thoughts

Alibaba is an ecommerce titan with a diverse business model which covers everything from fintech to B2B services. The company has faced a number of headwinds from regulators in both China and the U.S. However, now we are seeing some light at the end of the tunnel. The reduction in control by Jack Ma, is a positive sign for the Ant Group, and the “Golden Shares” could also be an interesting catalyst. Alibaba’s stock is undervalued intrinsically and it looks to be close to a breakout on the technical chart.

Be the first to comment