Philiphotographer/iStock Unreleased via Getty Images

Investment Thesis

We last covered Alibaba (BABA) in November, as we encouraged readers to consider staying out until we have clarity over its regulatory stance. Two months on, the stock is still about where it was (+/- 3%), and there is still no clarity over Beijing’s guidance.

Nevertheless, Alibaba held an investor’s day in December, as they sought to assuage investors to focus on its long-term growth story as management discussed new growth areas.

BABA stock is undoubtedly cheap given that it is trading at just 12.7x NTM EBITDA (3Y mean: 19x). But we know stocks are cheap for a reason. In the case of Alibaba, we believe that until Beijing is finally done with BABA, its stock will likely continue to underperform the market.

Beijing, When Will You Be Done?

Your guess is as good as ours. Since our last article, the Chinese government has continued to surprise us. So, for now, we think we can safely say Beijing is not done yet.

On 5 January, Nikkei/Caixin reported that the rules concerning the use of algorithms in making recommendations would come into effect on 1 March. Such restrictions prevent companies from using these algorithms for price discrimination. While the draft rules have already been in place since August, it continues to demonstrate Beijing’s concerted efforts to continue reining in its Internet companies.

Then shortly after, Caixin reported that China’s “new technical standards for unifying digital payment barcodes have laid the groundwork for tearing down the walls between different payment platforms.” Notably, it also emphasized that it’s still a big question mark hanging over how Beijing intends to enforce interoperability between the payment platforms. As a result, investors have no idea to what extent Beijing intends to tear down the walled gardens between its major payments platform. Caixin emphasized (edited):

The new specifications for integrating payment barcodes, produced by the People’s Bank of China, lay out a set of unified technical requirements for payment service providers, including quick response codes. If strictly implemented, the standards are expected to have a significant impact on the booming multitrillion-dollar mobile payment market, shaking the duopoly of Alipay and WeChat Pay (OTCPK:TCEHY). (Caixin)

It also came shortly after the central bank launched its digital yuan App for pilot testing, as China moves ahead with its digital yuan project. It’s pretty clear that unless China can “entice” its consumers to consider ditching their WeChat Pay or Alipay, it’s going to be very challenging to move them to the central bank’s platform. But, if China can enforce interoperability between WeChat Pay and Alipay, it could significantly reduce the incentive for consumers to stick with either platform. Consequently, that could also encourage consumers to move to the central bank’s digital yuan platform, as Tencent’s and Alibaba’s payments duopoly gets dismantled. Of course, this is just our conjecture. But the lack of clarity over Beijing’s intention is troubling.

It’s Made Worse By COVID, Real Estate Market, And Flagging Economy

China telegraphed its plans to focus on stabilizing the economy in 2022 after a tumultuous year that has significantly impacted its real estate market and equity markets. Consequently, it has also markedly affected consumers’ sentiments as China’s real estate market accounts for about 15-20% of its GDP. Coupled with the supply chain disruptions and China’s strict COVID policies, it has continued to hamper its economic recovery. Despite achieving 8% GDP growth in 2021, economists expect China to aim for just 5% growth this year, as it continues to see headwinds. While the real estate market could bottom out in H1’22, we should not expect the good old days to be back. Caixin reported that the readout from China’s Central Economic Work Conference (CEWC) was clear in its message. It reported (edited):

The CEWC called for pushing forward social housing construction, accelerating the development of the long-term rental market, supporting the commodity housing market in better satisfying homebuyers’ reasonable housing demand, and facilitating the healthy development and ‘a virtuous circle’ of the property sector. The meeting also reiterated the government’s position that housing is for living, not for speculation. (Caixin)

Therefore, while economists believe that China is keen to engineer a “soft landing” for its real estate market, it is not eager to return it to its heydays. It’s already challenging enough for investors to cope with tremendous regulatory uncertainty. Now, investors also have to deal with significant structural changes in demand and consumer sentiment. We have no idea what Beijing’s idea of a soft landing is at this point. As long as consumer sentiment continues to be weak, it will impinge on their ability and willingness to spend. Given Alibaba’s significant exposure to discretionary spending through its commerce businesses, it’s another notable headwind to deal with.

Then, Caixin reported that China “released a five-year plan for developing digital economy with specific targets and tasks, aiming to boost the contribution of core digital economy industries to 10% of GDP by 2025.” We were initially encouraged by the plan’s objectives and thought perhaps Beijing could be near the end of wielding its regulatory wand. However, as we read on, it seems Beijing knew precisely what we were looking out for, and China is committed to making it clear, as Caixin reported (edited):

The plan also emphasizes fair competition, curbing monopoly, data privacy protection, preventing the disorderly expansion of capital, and improving regulation to ‘safeguard the security bottom line.’ (Caixin)

Just like that, we are back to square one. We have no idea what those equivocal statements mean and what Beijing still has in mind. We don’t think China is bent on shutting out foreign investors; that is clear. However, we believe Beijing has more important plans that could take precedence currently. Until we know exactly what those plans are and how they will implement them, it’s better to be extra cautious.

BABA Stock Momentum Is Extremely Weak

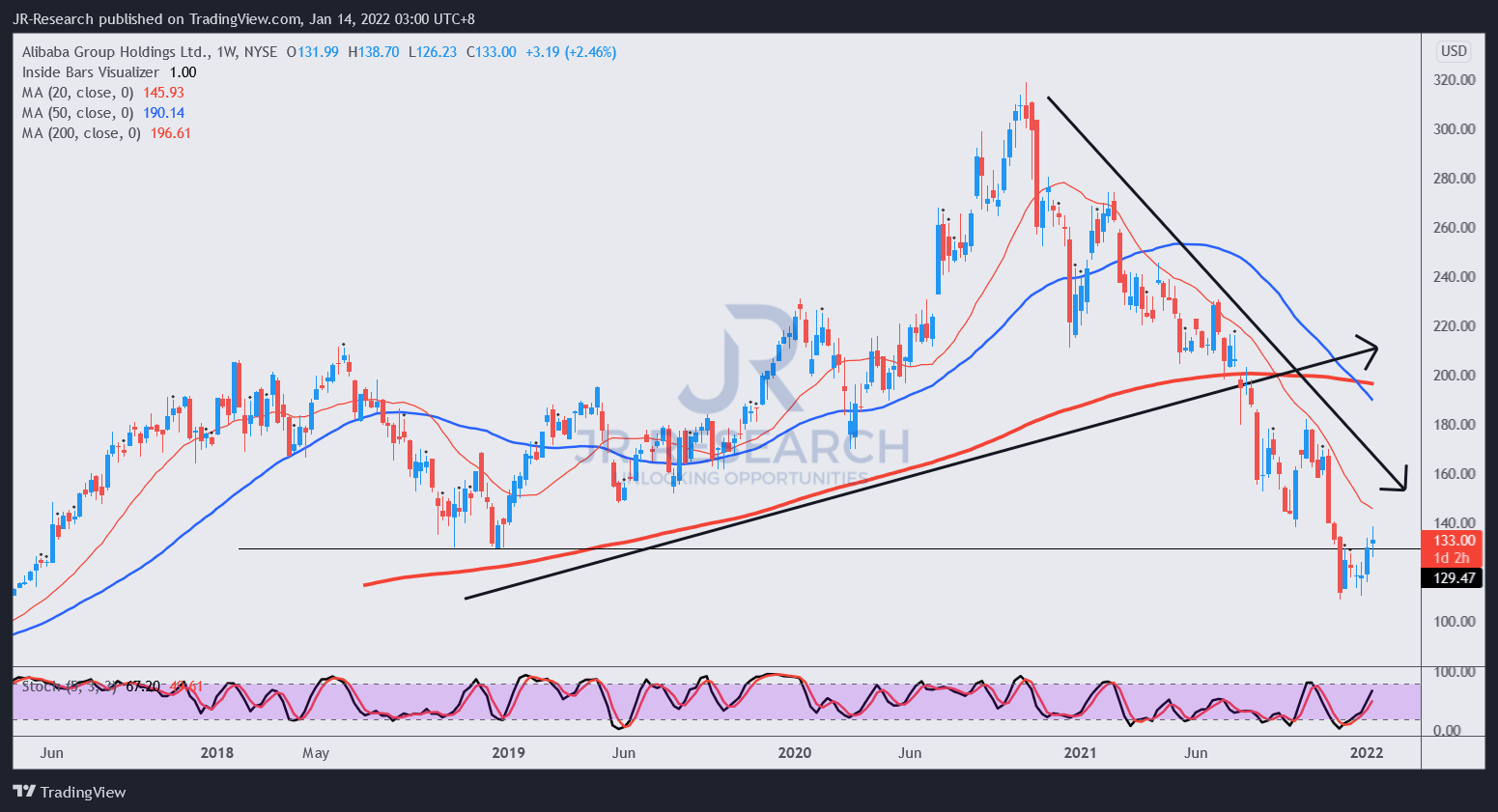

BABA stock price action (weekly chart) Tradingview

Moreover, the momentum in Alibaba’s stock is extremely weak now. We presented its weekly chart above. Price action and momentum investors should be familiar that a weekly chart is suitable to analyze BABA stock’s long-term trend bias. Notably, BABA has an undisputed downtrend bias. Its 20-week moving average (thin red line) has consistently resisted any attempt by BABA to resume its uptrend since 2020. Until this long-term downtrend bias is overturned, BABA could remain stuck in this vicious cycle.

Next, BABA’s last line of defense, its 200-week moving average (thick red line), was also broken in July’21. The 200-week is a critical long-term support level that has supported BABA stock consistently over the last three years. Thus, when it’s broken convincingly, as in the case of BABA’s stock, the message from the market is clear. Despite Charlie Munger’s positioning, it’s not going to be enough to overturn BABA’s downward momentum.

Nevertheless, there’s little doubt that BABA’s stock is cheap. It’s a high-quality company that really shouldn’t trade at such valuations. However, we believe that until China’s intentions over its Internet stocks are clear, it’s better to stay on the sidelines.

Therefore, we reiterate our Neutral rating on BABA stock for now.

Be the first to comment