Natali_Mis Akero

Ability is what you’re capable of doing. Motivation determines what you do. Attitude determines how well you do it. – Warren Buffett

In biotech investing, you should pick the leaders in various niches like oncology, gene therapy, liver, etc. After all, investing in leading companies (in their early stages of development) can deliver alpha results. Despite the fact that you have your favorite companies in each investment category, you should keep tabs on upcoming players. Sometimes, they can deliver surprising results to give you tremendous profits. It’s also a prudent strategy to pick several competing firms rather than one single stock.

That being said, I’d like to share with you a new and promising liver disease innovator, Akero Therapeutics (NASDAQ:AKRO). After the company recently posted extremely robust Phase 2 data of its drug designed to treat non-alcoholic steatohepatitis (i.e., NASH), the stock enjoyed a huge rally. But the question remains as to how it will perform into the next few years? In this research, I’ll answer that question by featuring a fundamental analysis of Akero and provide you with my expectation of this intriguing equity.

StockCharts

Figure 1: Akero chart

About The Company

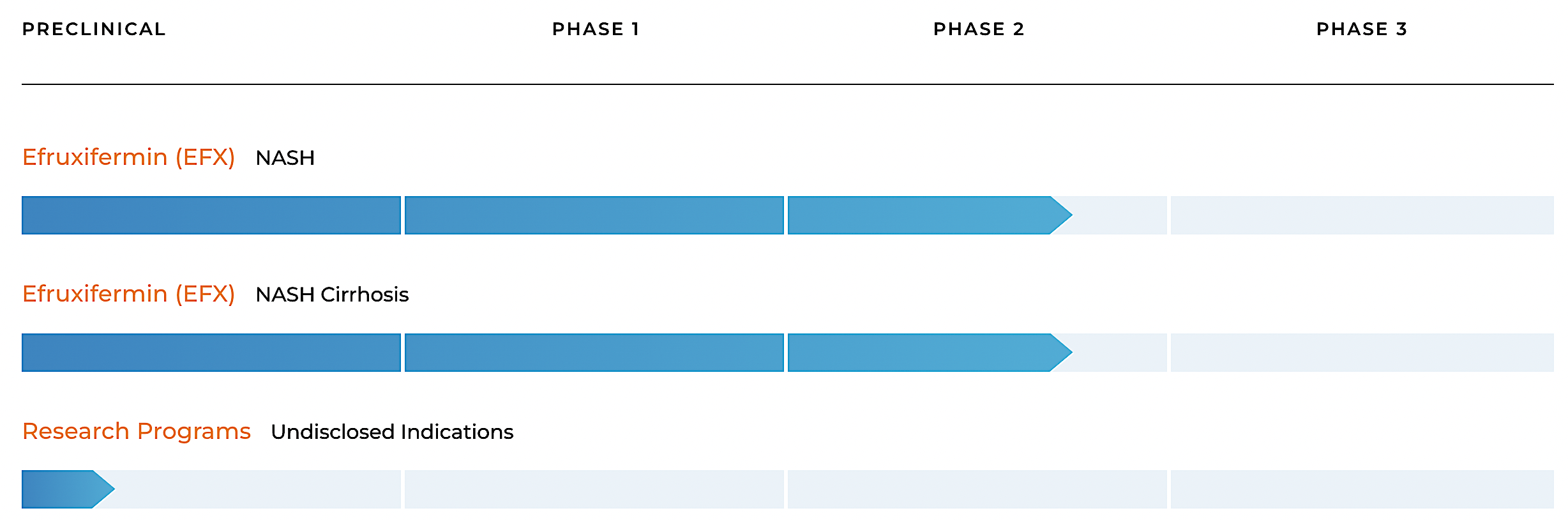

As usual, I’ll present a brief corporate overview for new investors. If you are familiar with the firm, I recommend that you skip to the next section. Headquartered in San Francisco, California, Akero is focused on the development and commercialization of novel medicine to treat serious liver conditions. The company has an extremely focused pipeline of a single molecule dubbed efruxifermin (i.e., EFX or Efru) — designed to treat the silent yet deadly condition, non-alcoholic steatohepatitis (i.e., NASH).

Akero

Figure 2: Therapeutic pipeline

Tracking Akero Investment Thesis

Before moving on with this analysis, you should place Akero into the appropriate investment category. That way, you can better track its progress, thus knowing when to buy, hold or sell. Accordingly, Akero fits into the “growth biotech” category. Here, the key to Akero’s growth is Efru. So long as Akero continues to advance Efru in clinical trials and posting robust results, your investment thesis (i.e. story) is playing out.

That aside, you also saw in the pipeline that Akero is developing drugs for an undisclosed position. Now, it’s not anywhere nearly as important as Efru at this growth stage. However, it could come into play in the future.

NASH

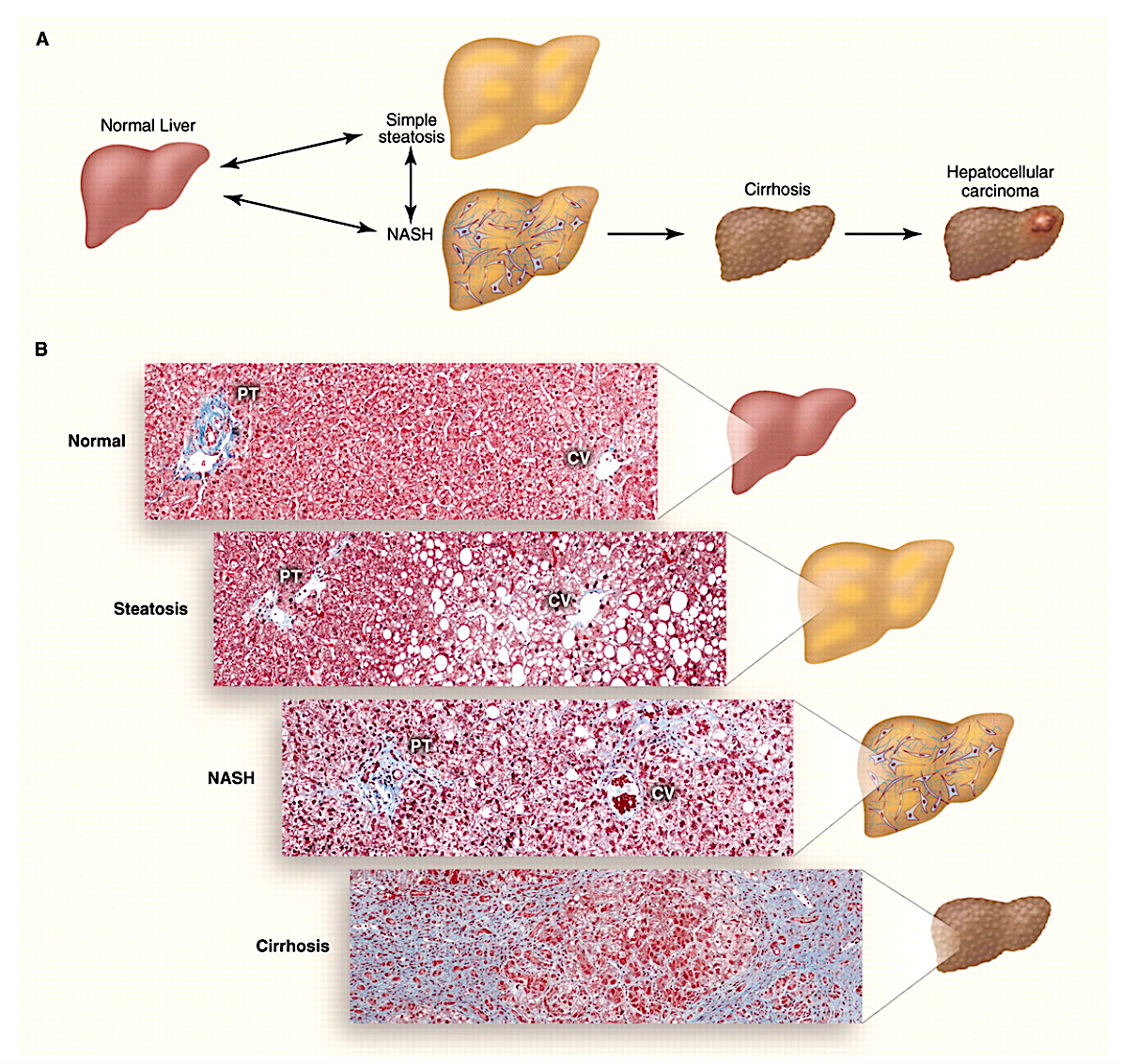

As a nonalcoholic fatty liver disease (NAFLD), NASH has histologic hallmarks of inflammation, cell death, and fibrosis. As you can see, NASH is one of the most common liver diseases (occurring in 3-5% of the US adult population). Notably, it tends to occur with other conditions (i.e., comorbidities), including insulin resistance, obesity, and metabolic syndrome. I elucidated in the Specialty Research on NASH article,

Since 2001, NASH has increased tenfold (and is the second leading cause of a liver transplant in the US). Interestingly, it is estimated that approximately 5% to 25% of patients with NASH will develop cirrhosis within the 7-year follow-up period. Prevalent in people of Hispanic origin, the disease tends to occur in men between 40 and 65 years old. And usually asymptomatic, NASH can exhibit the symptoms of fatigue and weakness in the advanced stages. A workup for NASH is indicated when the patient has certain risk factors in the presence of liver enzymes (“AST and ALT”) elevation. As alluded, those risk factors include the followings: Type 2 Diabetes Mellitus, obesity, metabolic syndrome, and obstructive sleep apnea. Despite the fact that there are different indicators of NASH, a liver biopsy is needed to establish a diagnosis.

ScienceMag

Figure 3: Spectrum of nonalcoholic fatty liver disease

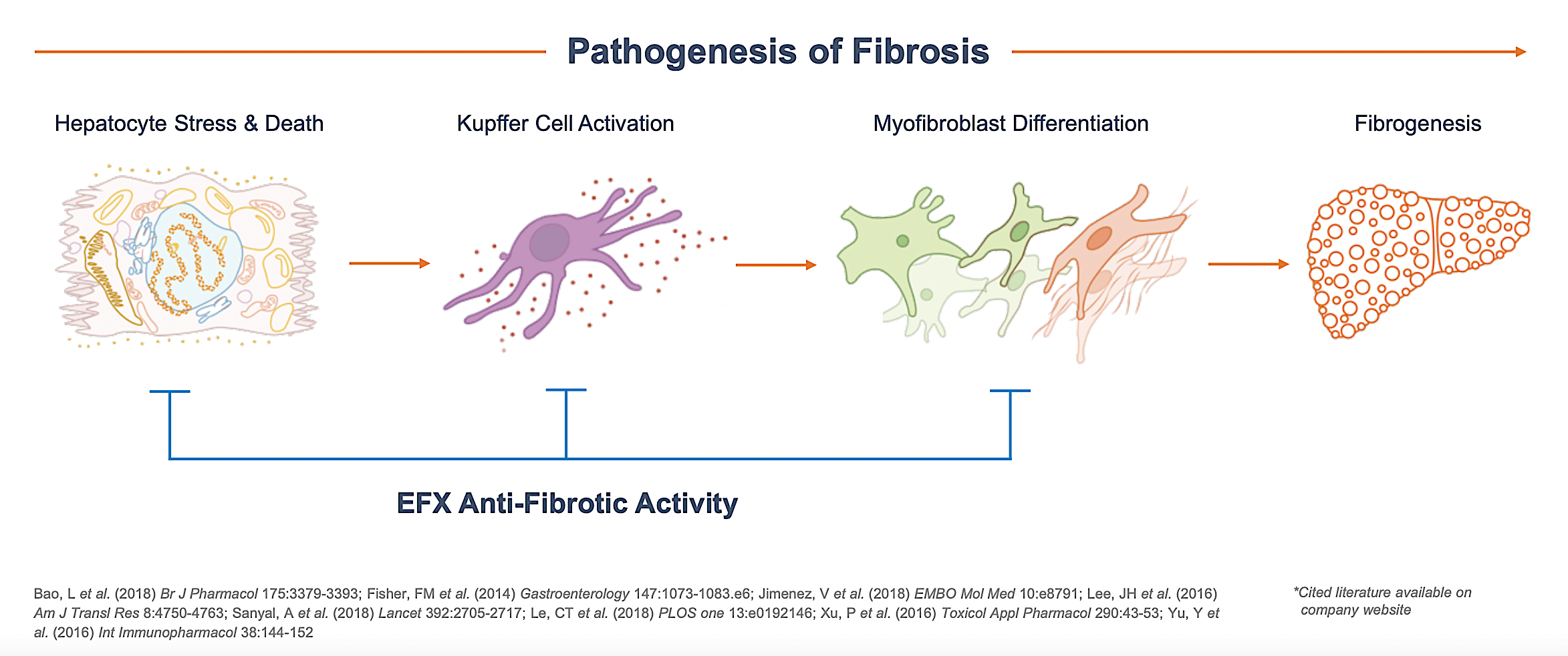

Regarding treatment, there are only therapeutic lifestyle changes (i.e., TLCs). No drugs are currently available. Growing at the remarkable 58.64% GAGR, the NASH market is projected to reach $180B by 2028. From the illustration below, you can see that Efru tackles one of the most important steps in the pathogenesis (i.e., development) of NASH. That is to say, it subdues the formation of fibrosis — a key hallmark of this disease.

Akero

Figure 4: NASH pathogenesis

Efruxifermin

As you know, the frontier (i.e., NASH) market is lucrative yet without any approved medicine. Therefore, a firm like Akero that can deliver positive clinical data and eventual approval could prove to be an investment bonanza.

As the crown jewel of this pipeline, Efru is a fusion protein (Fc-FGF231) designed to mimic the natural activity of Fibroblast Growth Factor 21 (i.e., FGF21). As you can see, FGF21 alleviates cellular stress and regulates metabolism throughout the body to prevent fibrosis. Hence, it has an excellent shot at delivering efficacy for NASH.

Akero

Figure 5: Efru mechanism of action

Robust Phase 2b HARMONY Data

On September 13, Akero reported extremely robust Phase 2b HARMONY data that galvanized the shares to rally over 100% in one single trading session. As a general trend, the stock typically trends down in the following weeks. Opportunistically, Akero immediately raised over $200M in equity offering which suppresses further rally.

Now, certain stocks can continue to witness further run up if the data is stellar and further catalysts are building in the horizon. Hence, it’s important that you analyze the aforesaid data report.

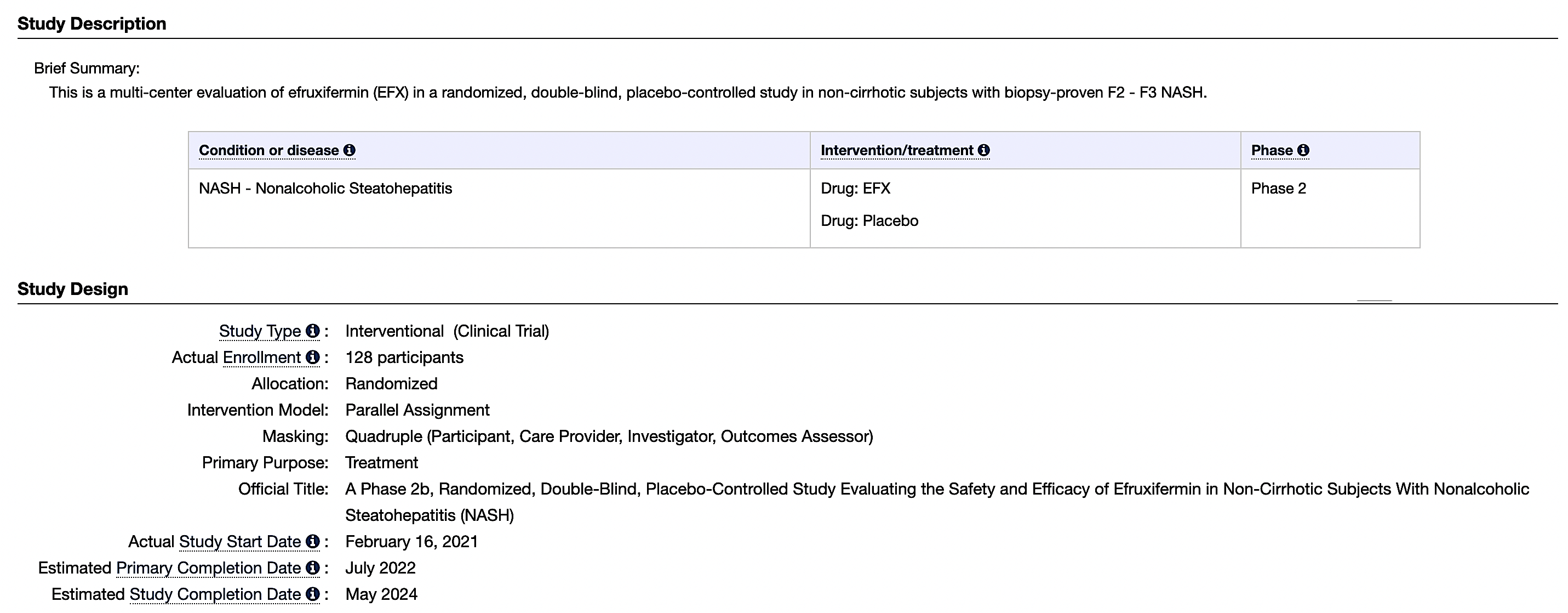

Accordingly, HARMONY is a high quality, randomized, placebo-controlled trial of 128 patients with pre-cirrhotic NASH (i.e., stage 2-3) over a 24-weeks period. Interestingly, roughly 70% of the patients also have Type 2 diabetes. As you know, this is important because NASH and diabetes typically occur together which are known as comorbidities.

Clinicaltrial.gov

Figure 6: HARMONY trial setup

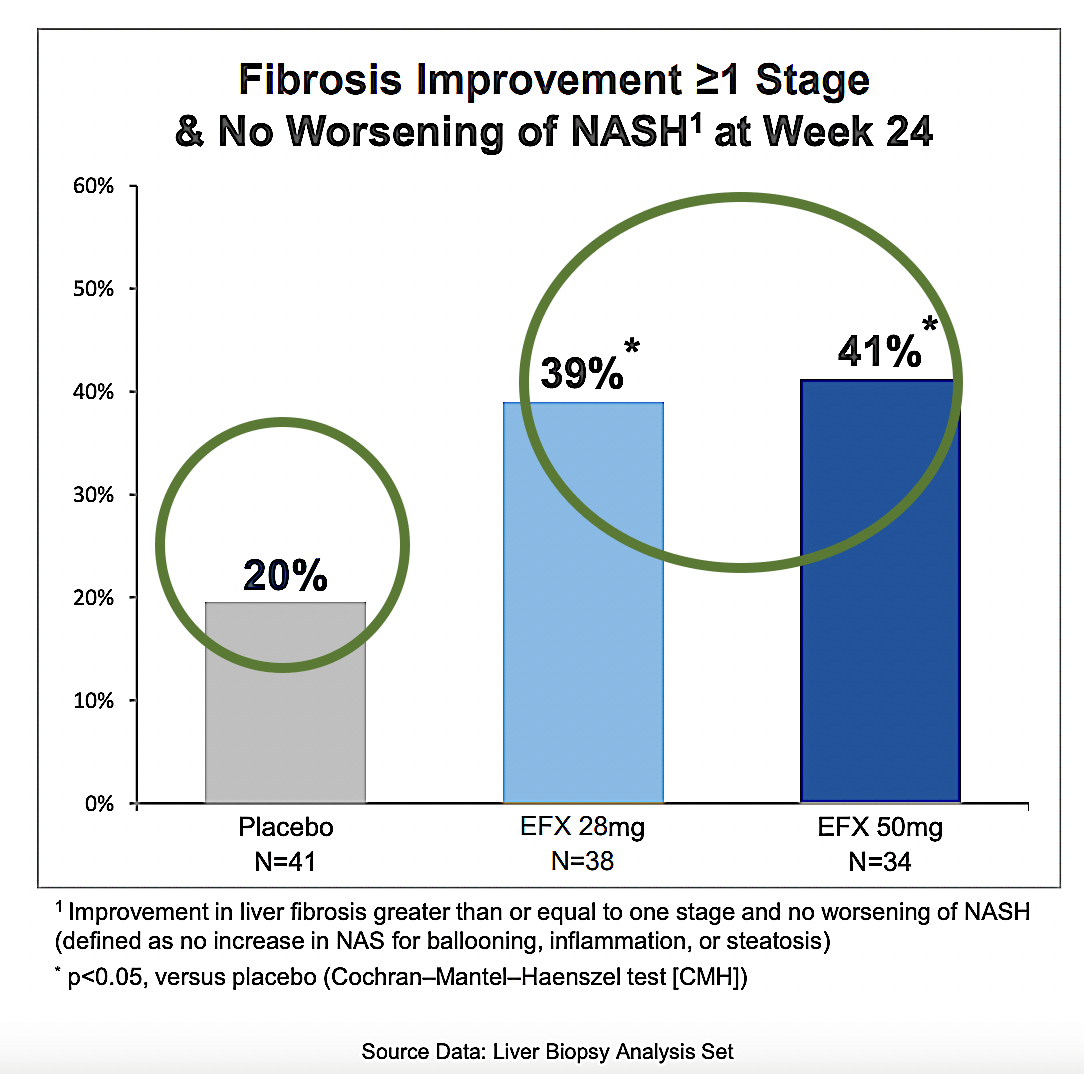

It is remarkable that the study cleared both its primary endpoint (a change from baseline in liver fibrosis with no worsening steatohepatitis) and key secondary endpoints with flying colors. Specifically, both the 28 mg and 50 mg doses respectively posted the 39% and 41% improvement — in at least 1-stage of liver fibrosis without worsening NASH by Week-24) — compared to placebo.

Akero

Figure 7: Phase 2b HARMONY results

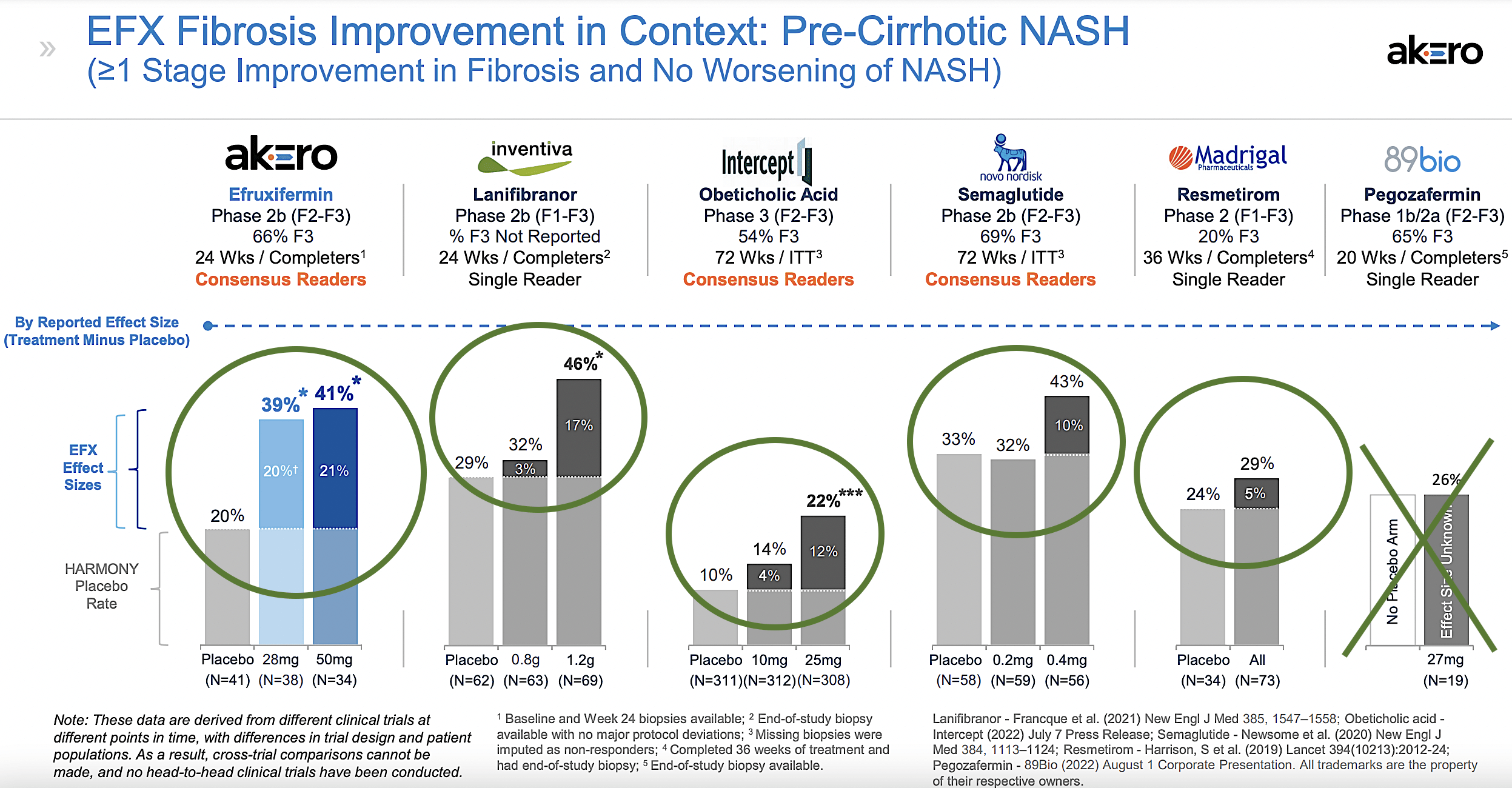

From the picture below, you can see that Efru is quite competitive against various drugs. That is to say, both the 28 mg and 50mg Efru doses delivered the 20% and 21% improvement over placebo which is the best among various molecules. Only Inventiva’s lanifibranor comes close to that. As to 89bio, there was no placebo arm for the data to be meaningful. Intercept (ICPT)’s data is not as robust to be considered in the race.

Now, there are a couple of things to keep in mind. First, the placebo for semaglutide of Novo Nordisk (NVO) also generated 33% responses. The placebo responses for other drugs are also high. Hence, it can be too early to make a definitive conclusion.

Akero

Figure 8: Comparative Analysis of Efru and other leading molecules

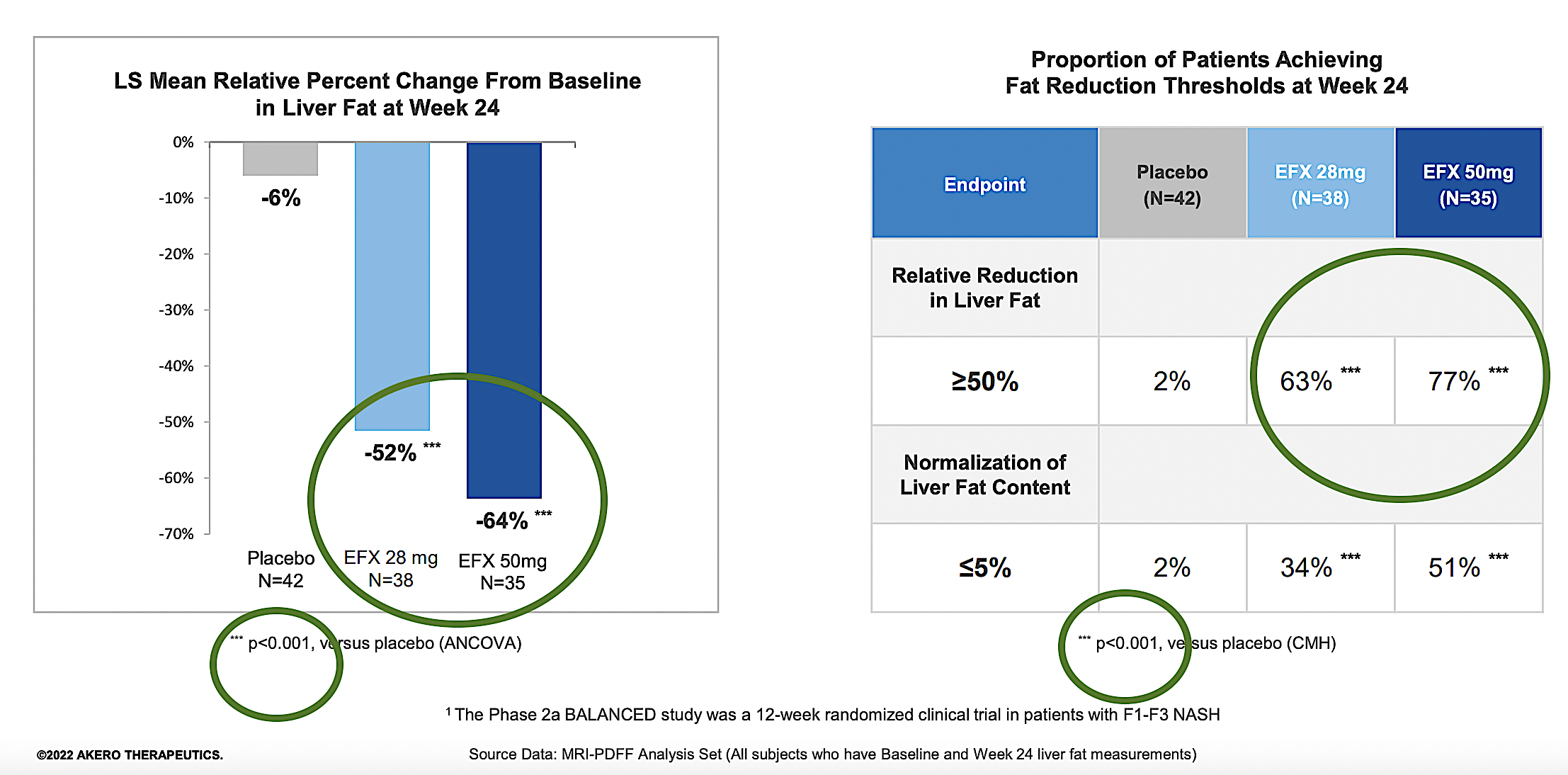

As fat reduction is a crucial metric in assessing NASH treatment, you should analyze its improvement here. On this front, 63% and 77% of patients on the 28 mg and 50mg doses correspondingly demonstrated at least 50% liver fat reduction. Those figures are quite strong.

Similar to the fibrosis improvement above, the aforesaid results are all statistically significant. Simply put, they are not due to random chances because p-values were all less than 0.05.

Akero

Figure 9: Liver fat reduction of Efru

Let’s take this analysis a step further. You know that Efru posted robust results. But how does the aforesaid liver fat reduction compare to Madrigal’s MGL 3196 (i.e., resmetirom or Resme)? Viewing the figure below, you can appreciate that both MGL3196 and Efru generated similar liver fat reduction.

However, data for MGL3196 comes from an extremely high quality Phase 3 (MAESTRO-NAFLD) trial. As a trend, it’s extremely difficult to replicate the Phase 2 results in a Phase 3 study. In fact, MGL3196 is the only drug that posted positive data in a Phase 3 trial. Looking ahead, I would expect Efru efficacy to trend down over time.

| Molecules | Percentage of patients achieving at least 50% liver fat reduction | Relative percent change in liver fat from baseline |

| Efru 28mg (Phase 2 HARMONY, 24-weeks) | 63% | 52% |

| Efru 50mg (Phase 2 HARMONY, 24-weeks) | 77% | 64% |

| MGL3196 80mg (Phase 3 NAFLD, 52-weeks) | 43% | |

| MGL3196 100mg (Phase 3 NAFLD, 52-weeks) | 53% |

Figure 10: Efru vs. MGL3196

Competitor Analysis

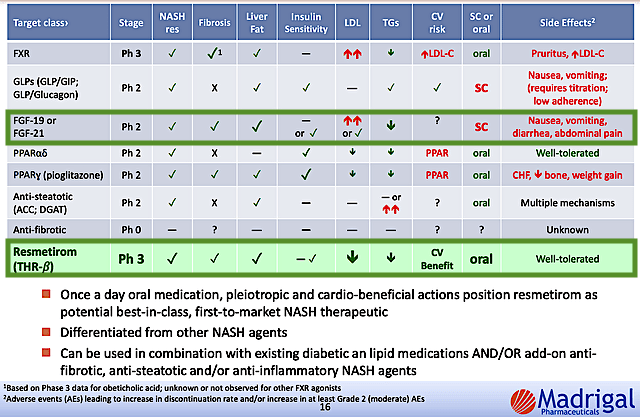

About competition, Akero goes toe-to-toe with many companies and drugs. In my opinion, the biggest competition for Akero is none other than Madrigal’s MGL3196 (i.e., Resme or Resmetirom). Asides posting similar efficacy, Resme has the best safety profile among competing molecules. That aside, MGL3196 is most likely the first drug to the market which enabled the proverbial early bird to get the worms.

Madrigal

Figure 11: Competitor analysis

Financial Assessment

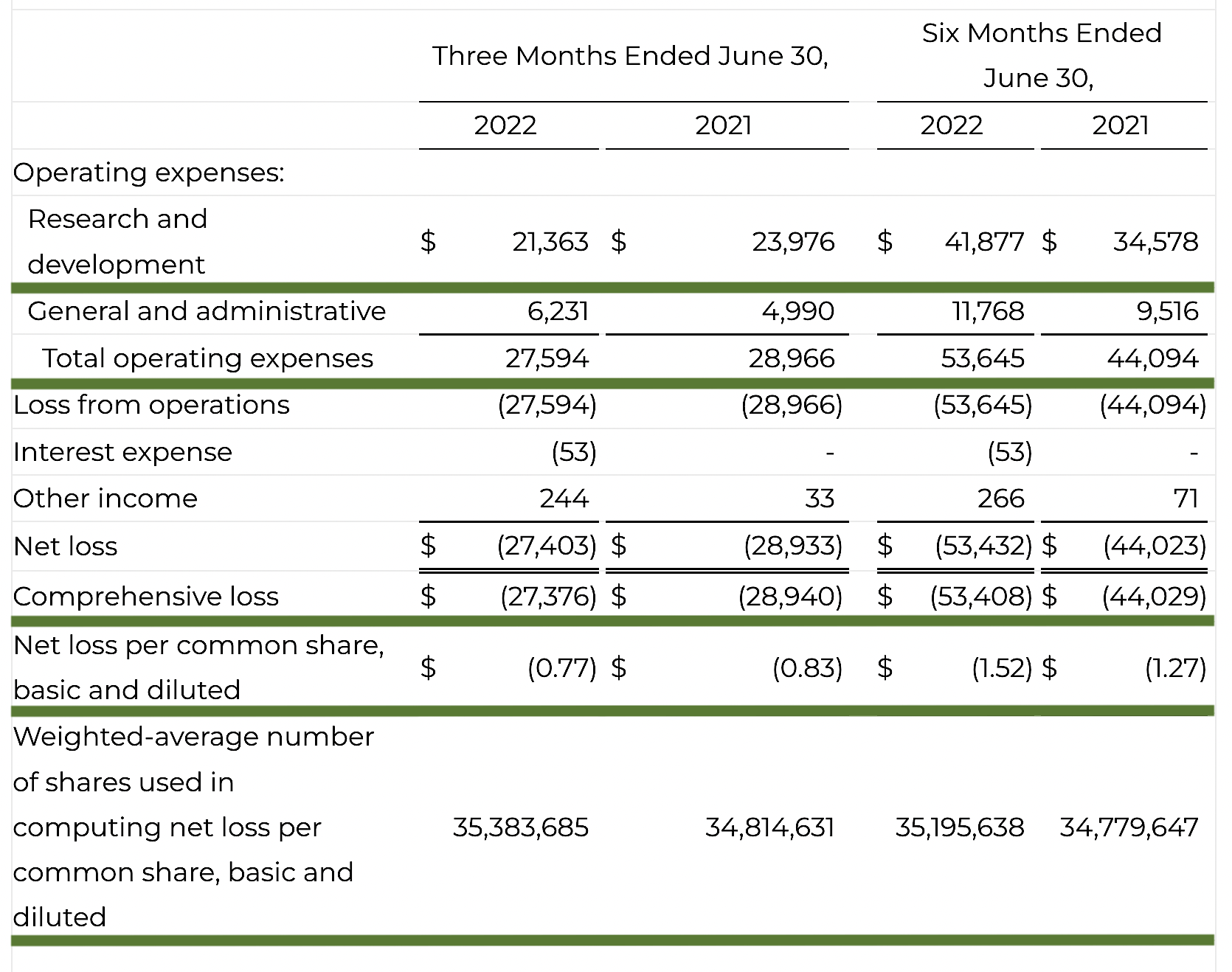

Just as you would get an annual physical for your well-being, it’s important to check the financial health of your stock. For instance, your health is affected by “blood flow” as your stock’s viability is dependent on the “cash flow.” With that in mind, I’ll analyze the 2Q 2022 earnings report for the period that ended on June 30.

Like most developmental-stage operators, Akero has yet to procure a sale. As such, you should look at other more meaningful metrics. On this note, the research and development (R&D) registered at $21.3M compared to $23.9M for the same period a year prior. The R&D remains pretty much the same. I typically like to see to an increasing R&D trend. The money that you invested today can turn into blockbuster profits. After all, you have to plant a tree to enjoy its fruits.

Additionally, there were $27.3M ($0.77 per share) net losses compared to $28.9M ($0.83 per share) declines for the same comparison. As the R&D is lowered, it makes sense that the bottom-line earnings depreciation also narrows.

Akero

Figure 12: Key financial metrics

About the balance sheet, there were $180.7M in cash, equivalents, and investments. On top of the recent $200.0M public offering, the cash position is increased to $380.7M. Against the $27.5M quarterly OpEx, there should be adequate capital to fund operations into 3Q2026 (i.e., 13 quarters). Simply put, the cash position is quite robust.

Valuation Analysis

It’s important that you appraise Akero to determine how much your shares are truly worth. Before running our figure, I liked to share with you the following:

Wall Street analysts typically employ a valuation method coined Discount Cash Flows (i.e., DCF). This valuation model follows a simple plug-and-chug approach. That aside, there are other valuation techniques such as price/sales and price/earnings. Now, there is no such thing as a right or wrong approach. The most important thing is to make sure you use the right technique for the appropriate type of stocks.

Given that developmental-stage biotech has yet to generate any revenues, I steer away from using DCF because it is most applicable for blue-chip equities. For developmental biotech, I leverage the combinations of both qualitative and quantitative variables. That is to say, I take into account the quality of the drug, comparative market analysis, chances of clinical trial success, and potential market penetration. Qualitatively, I rely heavily on my intuition and forecasting experience over the decades.

|

Molecules and franchises |

Market potential and penetration |

Net earnings based on a 25% margin |

PT based on 42.9M shares outstanding and 10 P/E |

“PT of the part” after appropriate discount |

|

Efru for MDD |

$2B (Estimated from the $180B global NASH market) | $500M | $116.55 |

$49.62 (60% discount because the drug is only in Phase 2 study) |

|

Undisclosed molecule |

N/A |

|||

|

The Sum of The Parts |

$49.62 |

Figure 13: Valuation analysis

Potential Risks

Since investment research is an imperfect science, there are always risks associated with your stock regardless of its fundamental strengths. More importantly, the risks are “growth-cycle dependent.” At this point in its life cycle, the main concern for Akero is whether Efru can continue to generate positive future data results.

As I’m optimistic about this medicine, I ascribed a 35% risk of negative data outcomes. Nevertheless, the risk is significant for a failed Phase 3 data report. Being a small company, Efru can burn excessive cash and thereby run into a cash flow constraint. Nonetheless, the recent offering substantially lengthened the cash runway.

Concluding Remarks

In all, I initiate coverage on Akero with a buy recommendation having a 4.8 out of five stars rating. Akero Therapeutics is a highly promising NASH innovator that you should put into consideration. Despite having only one drug in its pipeline, Efru demonstrated highly convincing Phase 2 data that signals more positive future data to come. Nevertheless, the Phase 3 data won’t be as robust.

You should keep in mind that the hurdle to generating positive Phase 3 data is much higher. This high hurdle is one that only Madrigal has managed to deliver. All competitors like selonsertib delivered strong Phase 2 results only to fail in its Phase 3 clinical investigations. In light of the daunting task, my intuition is still positive on Efru.

Be the first to comment