photoschmidt

Investment Thesis

Affirm Holdings, Inc. (NASDAQ:AFRM) remains a highly speculative fintech stock since its IPO, given its historically elevated trading valuations and its lack of profitability for the next few years. It is apt since AFRM would need to further rely on more debt in order to finance its expanding operations and partnerships moving forward. Akin to the average Joe relying on BNPL to purchase their Peloton bikes during the COVID-19 pandemic hype then.

Anyhow, we expect more downwards pressure on AFRM’s stock performance, given the rising inflation tightening discretionary spending and the potential recession. Therefore, anyone looking for a swift stock recovery would be sorely disappointed since the S&P 500 Index had fallen by 21.8% by H1’22, with analysts predicting either another plunge of 22% or a steep rebound of 24% by the end of the year. We shall see.

Speculatively, we believe the AFRM stock has more to fall to $10s over the next two quarters, which may prove to be a more attractive entry point then. Patience for those who have yet to add. In the meantime, sell for existing investors.

AFRM Continues To Expand Its Capabilities And Debts At The Same Time

S&P Capital IQ

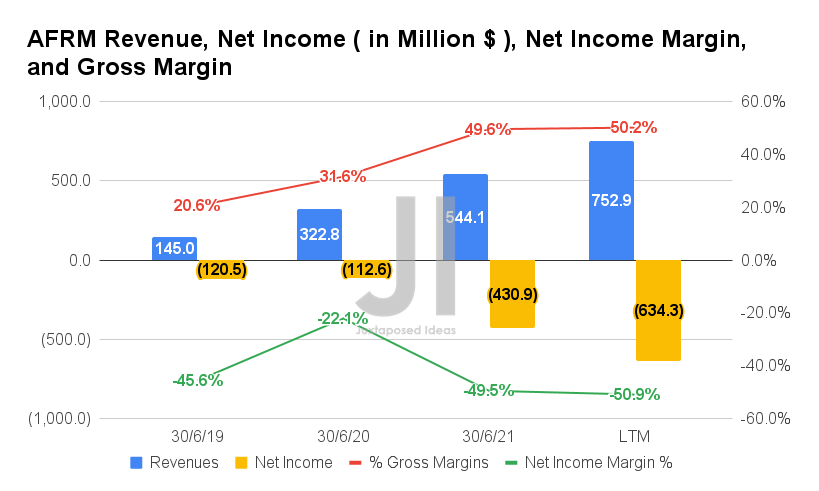

It is evident that the COVID-19 pandemic has been good for AFRM, given the tremendous growth in its revenue in the past two years. By the LTM, the company reported excellent revenues of $752.9M and record gross margins of 50.2%, representing massive improvements of 233.2% and 18.6 percentage points from FY2020 levels, respectively. Nonetheless, despite the windfall, AFRM has struggled with profitability thus far, reporting net incomes of -$634.3M and net income margins of -50.9% in the LTM, representing huge decreases of 563.3% and 28.8 percentage points from FY2020 levels, respectively.

S&P Capital IQ

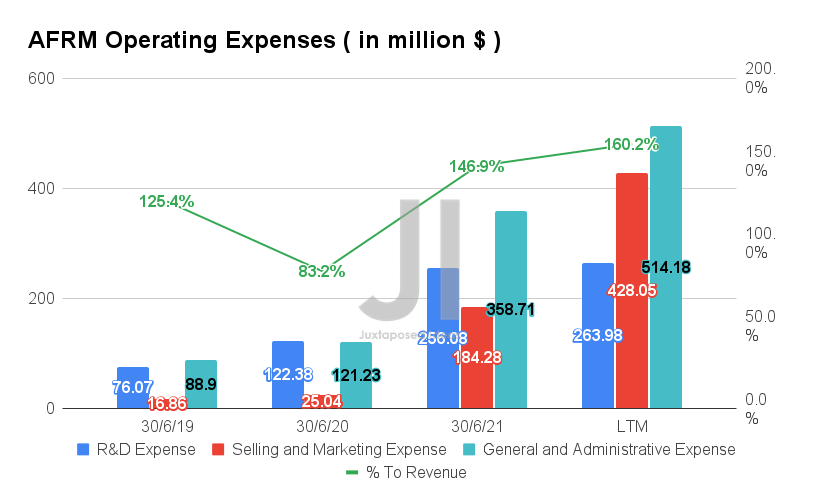

The lack of profitability could be attributed to AFRM’s aggressive increase in operating expenses in the past two years, with a total of $1.2B reported in the LTM, representing 160.2% of its revenue then. It also represented a gargantuan increase of 446.6% from FY2020 levels, indicating the company’s current growth-at-all-cost stage. Given AFRM’s rate of expansion and growth in partnership, we expect the company to remain unprofitable for the next few years, prior to reaching an inflection point in the next five (or so) years.

S&P Capital IQ

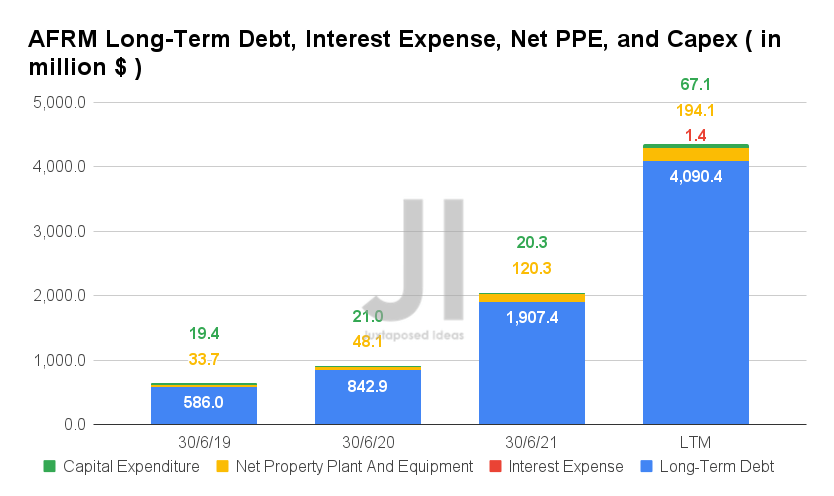

Therefore, it is evident that AFRM has yet to report positive Free Cash Flows (FCF) thus far, with -$190.1M of FCF and -15.2% of FCF margins in the LTM. The company would need to further rely on long-term debts for its expanding operations moving forward. By the LTM, the company reported long-term debts of $4.09B, representing a massive increase of 486.9% from FY2020 levels. In the meantime, AFRM’s net PPE assets and capital expenditure continue to grow to $194.1M and $67.1M in the LTM, representing a massive increase of 403.5% and 319.5% from FY2020 levels, respectively.

S&P Capital IQ

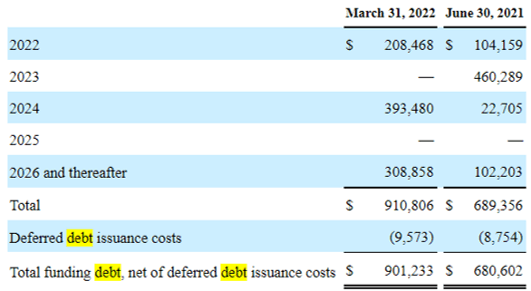

AFRM Funding Debt Maturities

Seeking Alpha

Much of AFRM’s long-term debts include funding debt, convertible senior notes, and revolving credit facility. This strategy has allowed the company to extend around $3.91B of loans for FQ3’22, which indicated a more-than-healthy growth in the company’s business thus far.

Nonetheless, it is also apparent AFRM had to rely on $1.725B of 0% convertible senior notes due 2026 for its growing operations, given the lack of profitability. These would constitute a potential share dilution of up to 8M shares, representing a minimal dilution of 2.8% from the current count, assuming the initial conversion price of approximately $215.65 per share. Otherwise, speculatively up to 72.3M based on current share prices, depending on the eventual adjustments to the agreement. This would translate to a notable dilution of 25.3% based on current share counts. Rather alarming, though we shall continue monitoring through 2026.

In the meantime, AFRM continues to incur losses thus far, with a deficit of $1.4M in the latest quarter, representing a massive increase of 55.5% YoY. Therefore, since the company is not expected to report any profitability by FY2024, we expect further reliance on “the sales of equity securities, borrowings from debt facilities and convertible debt, and third-party loan sale arrangements.” Literally, Borrow Now Pay Later.

S&P Capital IQ

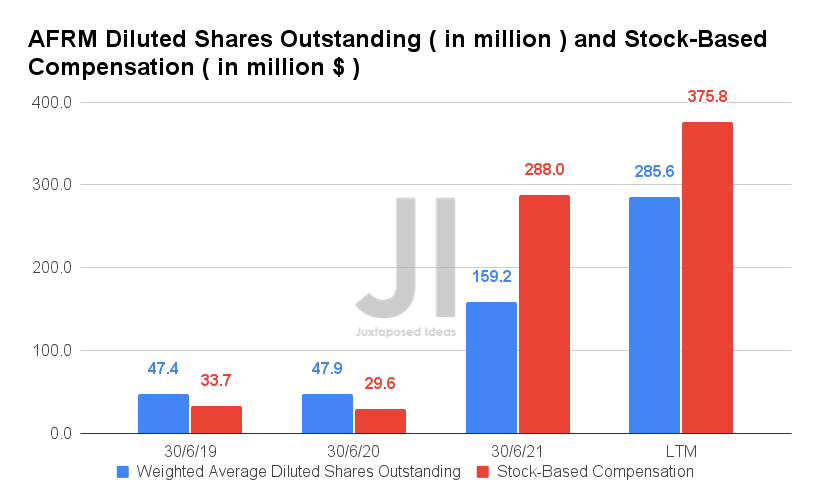

Therefore, AFRM may continue to rely on stock-based compensation (SBC) moving forward, with already $375.8M already reported in the LTM. Rather disturbing, since it easily accounts for half of the company’s revenue then. At the same time, its diluted shares outstanding continue to grow to 285.6M by the LTM, representing a notable 22.4% increase since its IPO. Assuming a similar rate, we may expect to see AFRM reporting up to 428M of share count by FY2024, indicating a massive 83.4% dilution since March 2021, given its lack of projected profitability and share buyback program then. Investors take note.

S&P Capital IQ

Over the next two years, AFRM is expected to report revenue growth at a CAGR of 38.74%. It is apparent that consensus estimates are still very optimistic about its YoY revenue growth, despite the projected deepening net losses to -$888M by FY2024. Given the intense competition from legacy and startup fintech companies jumping on the overcrowded BNPL bandwagon, the company may also continue to face a challenging environment for the next two years, worsened by Apple’s (AAPL) recent entry.

However, AFRM also proved to be adept in expanding its partnership beyond Peloton (PTON), by recently adding Agoda, part of Booking Holdings (BKNG), and SeatGeek, a ticketing platform for live events, as its latest partners. Nonetheless, given the rising inflation and potential recession, it remains to be seen if consumers will act as optimistically as consensus estimates over the next two years. AFRM’s upcoming FQ4’22 earnings call in September 2022 would definitely provide some insights into the consumers’ behavior thus far. We shall see.

So, Is AFRM Stock A Buy, Sell, or Hold?

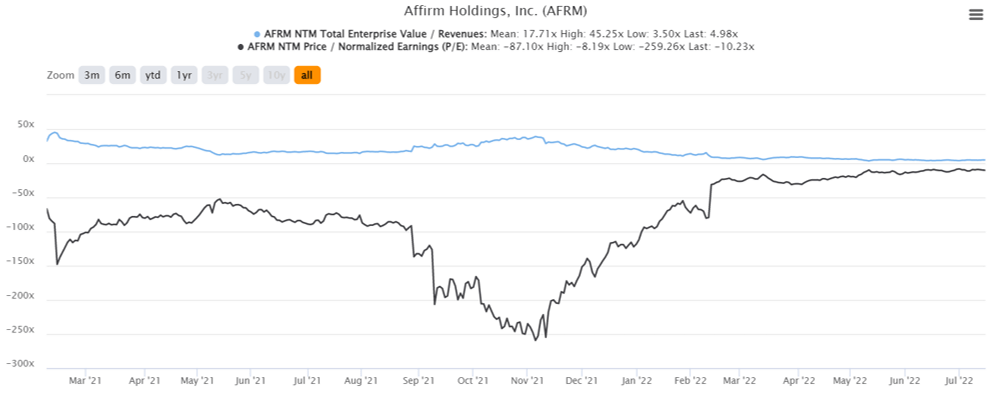

AFRM 1Y EV/Revenue and P/E Valuations

S&P Capital IQ

AFRM is currently trading at an EV/NTM Revenue of 4.98x and NTM P/E of -10.23x, lower than its 1Y mean of 17.71x and -87.10x, respectively. The stock is also trading at $23.84, down 86.5% from its 52 weeks high of $176.65, though at a 74.7% premium from its 52 weeks high of $13.64.

AFRM 1Y Stock Price

S&P Capital IQ

It is evident that AFRM has been massively moderated from its pandemic highs to settle at current lows. We expect the stock to continue underperforming for the reasons stated above, post-COVID-19 hypergrowth. Therefore, despite consensus estimates’ price target of $42.57, we are not convinced of its 78.57% upside.

Based on the results of a survey conducted by Paysafe, AFRM may be also headed for a drastic retracement to $10s, since more than 80% of the US consumers are “cutting back drastically on spending due to inflation.” This is assuming another moderation in its PE valuations to -5x, as we have witnessed since the start of the year, given the double whammy effects of the potential recession and bearish market sentiments for the next few months. As a result, it is likely that AFRM would only recover by 2023 or 2024, if any.

Therefore, we rate AFRM stock as a Sell for now. Preserve your capital and get in again at new lows for the bulls.

Be the first to comment