Before I start this article, we have to revisit an article we posted back on June 12 titled, “Bottom Of The 2nd Inning – What Signs To Look For On Oil.” In that article, we talked about what signs to watch for in case the oil market turns the other way. Here’s what we wrote:

In order for the oil market to show signs of turning, we must first see physical oil market signals turn bearish. In this case, Brent timespreads will be the first to flip.

Barchart.com

As you can see from the latest Brent 1-2 chart above, we are still far away from that. But when we do see the spreads fall and possibly close below 0 (and into negative), that’s when we will know something has shifted in the market.

If Brent timespreads start to fall and refining margins are not moving higher, then something is amiss.

Barchart.com

In normal markets, if the end-user demand is strong, and crude falls, then refining margins will rise. If crude falls and refining margins follow, then it implies even weaker demand. Now given how elevated refining margins are, a drop back shouldn’t be seen as severe demand weakness, but if the recent surge is materially reduced, then we should be aware that material demand weakness is on the horizon.

Before we begin, it’s important to understand that the baseball analogy here represents the length we believe this structural oil market to last. Yes, we’re in a structural oil bull market, but markets don’t go up in a straight line, so there will be moments like the ones we are seeing today that will test your resolve.

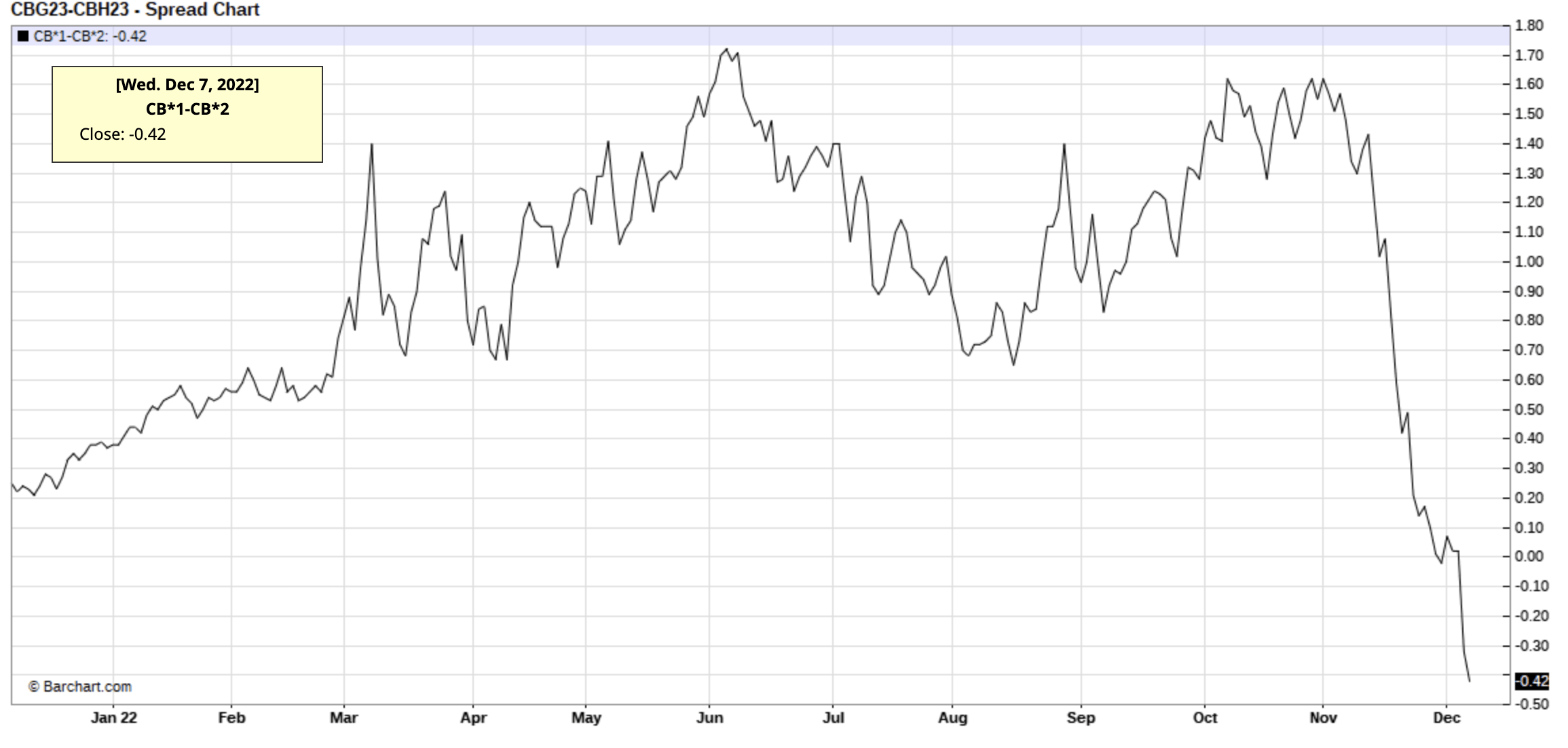

So fast forwarding to today, all the signals we said to watch out for are flashing red. Here’s the latest snapshot of the Brent 1-2 timespread:

Barchart.com

This has now flipped into a contango.

And if you look at the vanilla 3-2-1 crack spread, cracks are also starting to fall.

Barchart.com

Given that the physical oil market is only starting to materially weaken now, we would have to say that the financial market was well ahead of its time by pushing prices lower. With us trading at $72/bbl WTI and below where we started at the beginning of the year, you have to really wonder if we are all missing something on the demand side.

Judging by the way the physical oil market is trading and how long the contango persists (first half of 2023), the market is saying to us that global oil inventories will build. This means that the demand side will be very weak.

How weak?

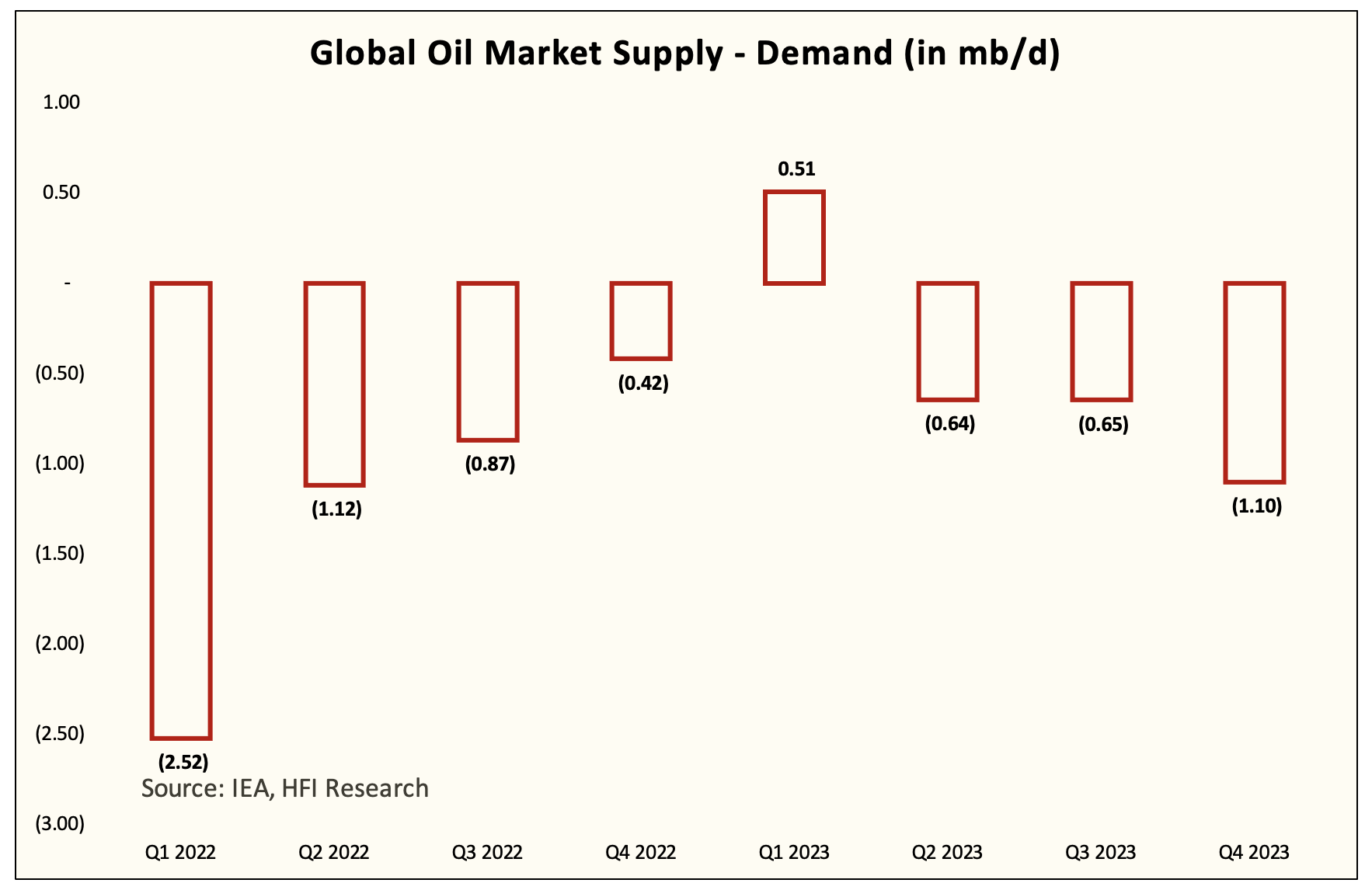

IEA, HFIR

We have drastically reduced our oil demand estimates to reflect what the market is seeing. In order for Q1 to be a build of 0.51 million b/d, global oil demand needs to come in around ~98.5 million b/d.

To put this into context, at 98.5 million b/d, this will be a y-o-y decline of ~940k b/d. This decline takes into account worries over the global economy. And as the low demand in Q1 carries out for the rest of 2023, total oil demand is expected to average ~100.44 million b/d or barely above the 2019 average of 100.24 million b/d. We see China’s reopening pushing up demand by H2 2023, which should help push the oil market into a steeper deficit.

While it’s not our base case to assume that global oil demand will be this weak, this is what the market is saying to us, and we have to take these physical oil market red flags as signals.

Now to put our conservativeness into context, IEA has global oil demand averaging ~101.39 million b/d in 2023. For Q1 2023, it has ~99.64 million b/d. In our view, if the global oil market was expected to remain in deficit in Q1, then Brent timespreads should not be in contango, but here we are. Clearly, we are missing something on demand.

So on one end, the bad news is that the market appears to suggest a build for Q1. On the other end, even if we drastically lower global oil demand forecasts for 2023, we should still see global oil inventory draws from Q2 to Q4. Keep in mind also that we are assuming Iran barrels to return in the 2nd half of 2023.

This is a structural bull market, but this is a big speed bump…

We believe this is a structural oil bull market fueled by years of underinvestment in supplies. We’re going to be seeing a structural supply deficit going forward. The problem is that while we can say that we are in a structural oil bull market, major speed bumps will come along the way and knock some people out of the bus. The key is to manage expectations and your portfolio risk well.

In this case, a global recession will impact demand, and this is precisely what the oil market is saying to us. Where do oil prices bottom? I don’t know, but what I can say with confidence is that even with the major demand revision to the downside, we should still see 2023 oil inventories draw in totality. This also is what the market is saying by indicating that the futures curve remains in backwardation.

While it’s important to keep the big picture in mind, managing portfolio risk and expectation is equally as important. Let’s get through this major speed bump in front of us (demand surprising to the downside).

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment