hynci/iStock via Getty Images

This article was published on Dividend Kings on Monday, January 23rd, 2023.

——————————————————————————

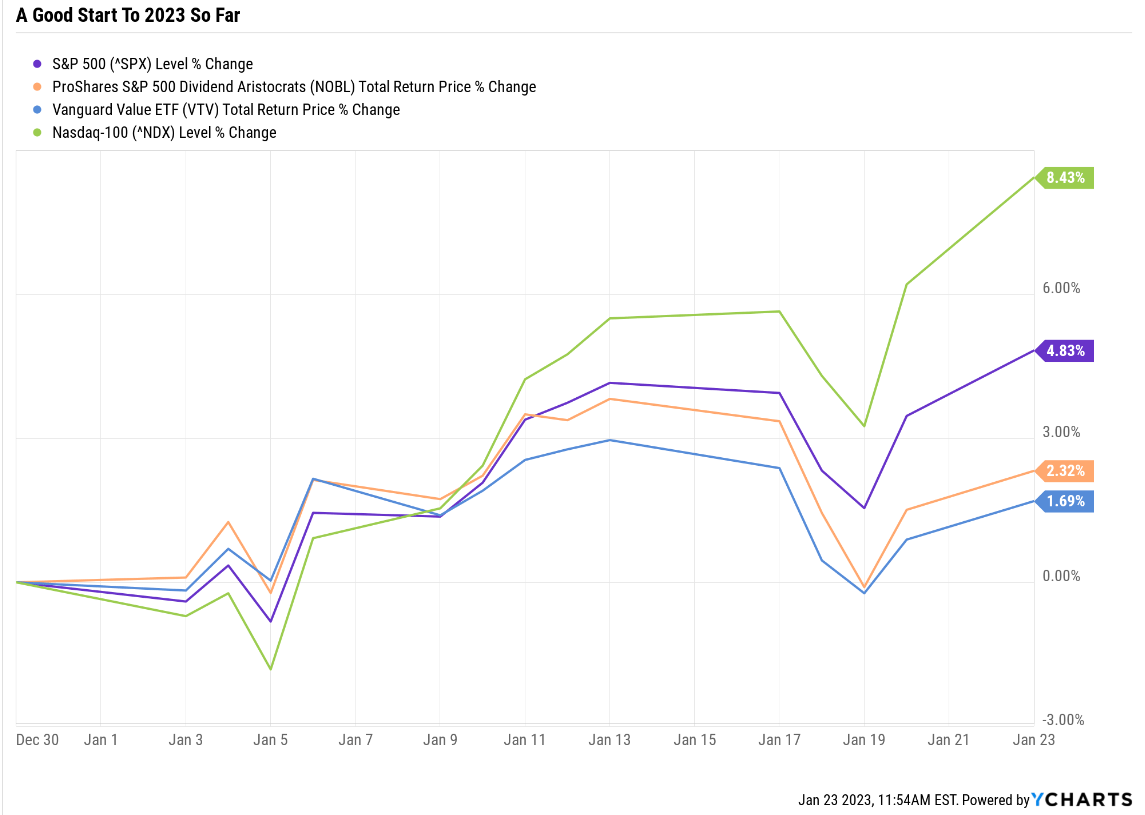

So far, stocks are off to a solid start in 2023.

YCharts

Everything is up but the most beaten-down stocks of 2022 are having the best recovery in 2023.

So does that mean the “dust has settled”? Is it safe to start buying stocks again? The answer is simple in my view, it’s always safe to buy world-beater blue-chips, as long as your time horizon is 5+ years.

Some investors are starting to get a bit of FOMO again, watching tech stocks rocket higher. Are we back to the new normal again? Are growth stocks going to dominate value and dividend stocks once again like they did during the last decade?

Or is the 2022 value rotation created by the return of historically normal interest rates just the beginning of a decade-long value bull market?

Stock Market Map

History would indicate that value, which is still extremely undervalued relative to growth, should outperform over the next 20 years.

But guess what? Value vs. growth is the wrong question to ask. No value investor buys a high-yield blue-chip expecting no growth, and do you think investors in MA or LOW think their dividends won’t grow?

There is arguably no such thing as a growth or value investor. Every “growth investor” thinks they are buying growth at a reasonable price.

Every value investor expects positive growth, otherwise, they would just buy 4% yielding treasury bonds for yield.

So what about 2023? Is it safe to buy stocks yet?

The 2023 Recession Might Take Longer To Strike, But It’s Still Likely

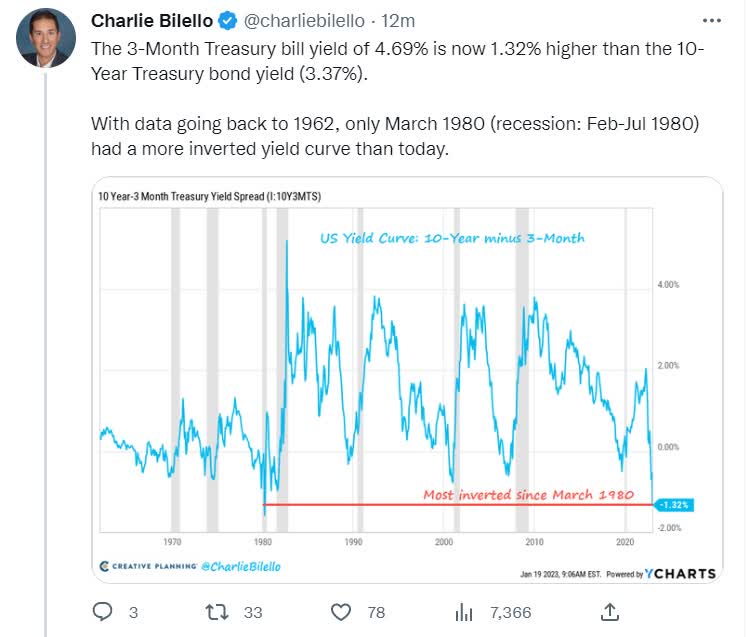

Charlie Bilello

According to studies from the NY, Chicago, Dallas, and San Francisco Feds, the best recession forecasting tool in history is the yield curve. This is now the most inverted since 1980.

Charlie Bilello

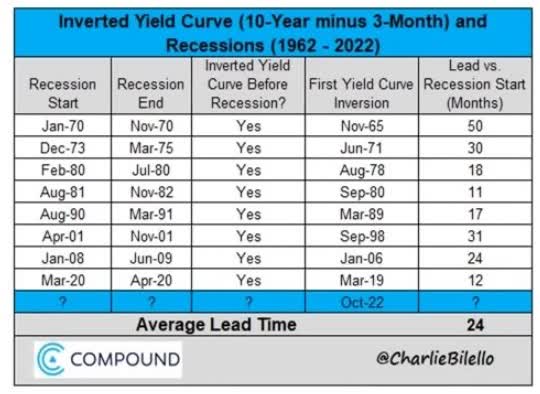

But guess what? You can’t use the yield curve to time the economy. The recession might begin in a few months, or not begin for a few years.

Historically speaking, it’s likely by October 2024.

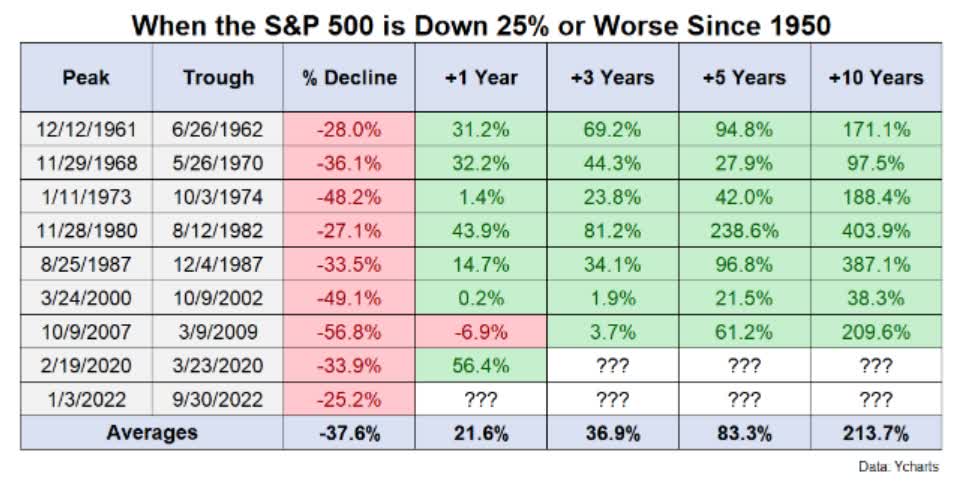

But guess what else? Even if you could time the economy perfectly, it probably wouldn’t beat buy-and-hold blue-chip investing.

Charlie Bilello

Outside of the Great Depression, when the economy fell 25% and stocks by 87%, perfect economic timing wouldn’t have delivered better returns than buy and hold.

Are stocks LIKELY to fall to new lows? Yes.

S&P Bear Market Bottom Scenarios

| Earnings Decline In 2023 | 2023 S&P Earnings | X 25-Year Average PE Of 16.8 | Decline From Current Level |

| 0% | $217.85 | $3,666.42 | 9.0% |

| 5% | $206.96 | $3,483.09 | 13.5% |

| 10% | $196.07 | $3,299.77 | 18.1% |

| 13% (median, average since WWII) | $189.53 | $3,189.78 | 20.8% |

| 15% | $185.17 | $3,116.45 | 22.6% |

| 20% | $174.28 | $2,933.13 | 27.2% |

(Source: DK S&P Valuation Tool, Bloomberg Consensus)

Stocks are likely to fall 9% to 27% before they hit their eventual bottom.

But does that mean they will? No, that’s not how probabilities work.

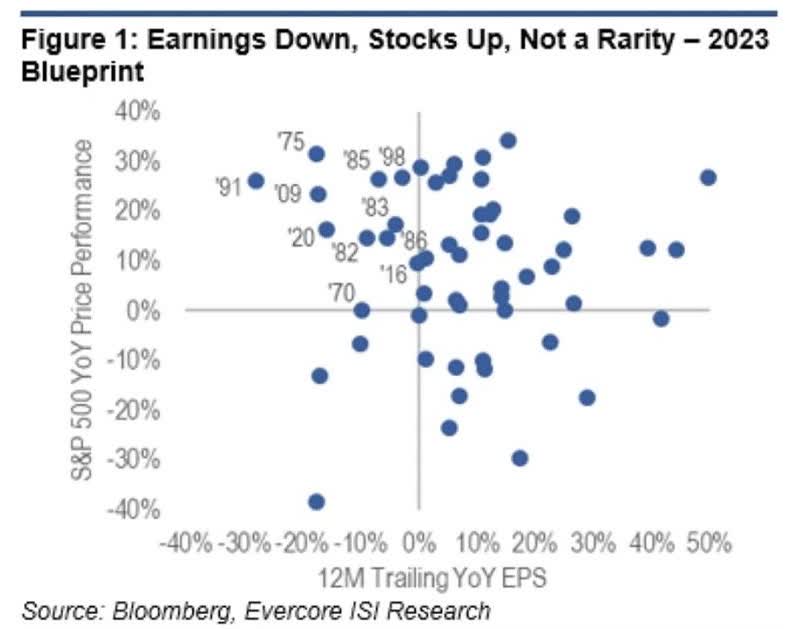

Ben Carlson

There are plenty of examples of stocks going up even when earnings fall. In fact, since WWII of 17 years with negative earnings growth, stocks went up 11 out of 17 years.

- 65% of the time

- stocks go up 76% of all years

In other words, even if earnings fall, stocks still have a good chance of going up. Not when they are trading at current valuations, mind you, but the point is that if stocks have a good 2023 that wouldn’t be surprising.

Ben Carlson

In fact, historically speaking, stocks could be 22% higher by October 2023 if we avoid recession.

If we don’t, then they might be flat or down a bit.

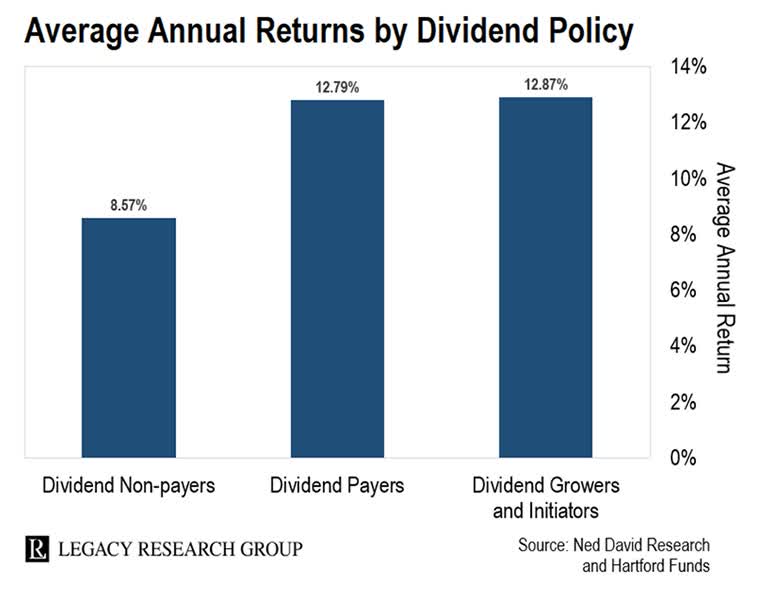

So what’s a smart long-term investor to do? Stop obsessing over 2023, and remember that dividend blue-chips are the best wealth and income-compounding tool in history.

Legacy Research

Over 50 years, dividend blue-chips delivered 450X returns. That’s 450,000%.

- 7X better than non-dividend stocks

What if a blue-chip you want to buy falls 20% after you buy it? Then buy more if the fundamentals are intact. Why not wait for it to fall 20% first?

- because it might not fall 20%

- it might fall 5% or 10% or not fall at all

When you’re looking at 2000+% long-term returns, the kind that rich retirement dreams are made of, do you know what a 20% lower price would get you?

An extra 25% over decades.

If you’re hunting for 2000% returns, a 20X rich retirement return, do you think 2025% returns will make your retirement any richer? It won’t.

But if you don’t buy at all? Because you’re convinced stocks “have to fall X%”? Then you risk missing out on 2000+% long-term returns in exchange for a theoretical 25% more.

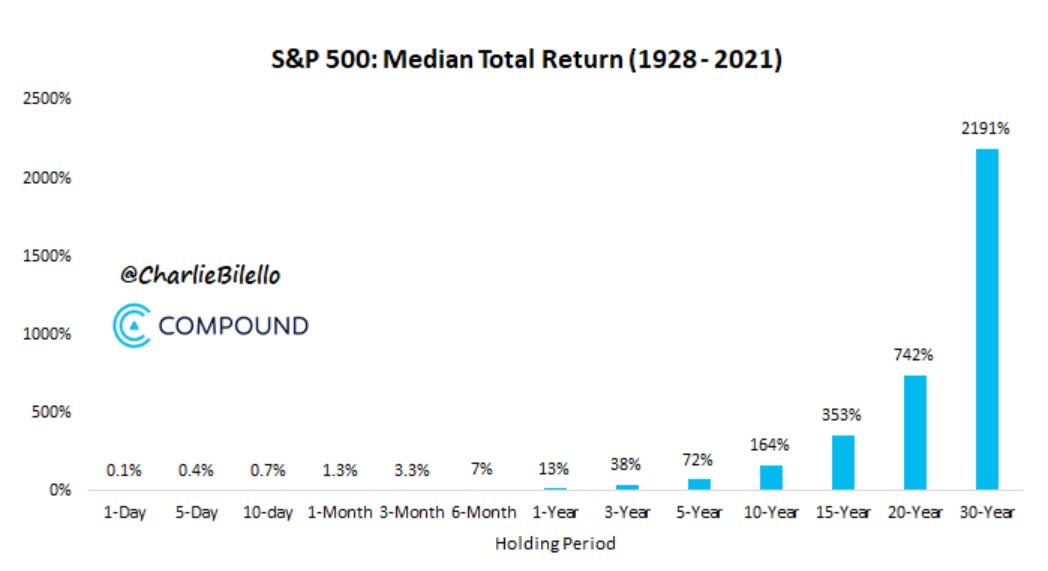

Charlie Biello

The market’s median 30-year return, the retirement time frame for anyone under the age of 70, is 2200%.

Do you know what you’re really doing if you refuse to buy any blue-chips in a bear market just because we’re not hitting new lows?

- possibly risking not making potential 23X returns to try to make 23.25X returns

It’s like risking not making $88 because you are convinced you can make $89.

That extra $1 won’t make you retire richer, but if you don’t make the $88 you might not retire at all.

So what’s the answer? How about coiled spring dividend aristocrats?

Some of the most undervalued yet high quality and dependable dividend growth stocks in the world?

Let me show you why Essex Property Trust (ESS) and Carlisle Companies (CSL) are coiled spring aristocrats that I think COULD soar 30%+ in 2023 alone. More importantly, I’ll show you why they could help you achieve the rich retirement of your dreams once this recession is over.

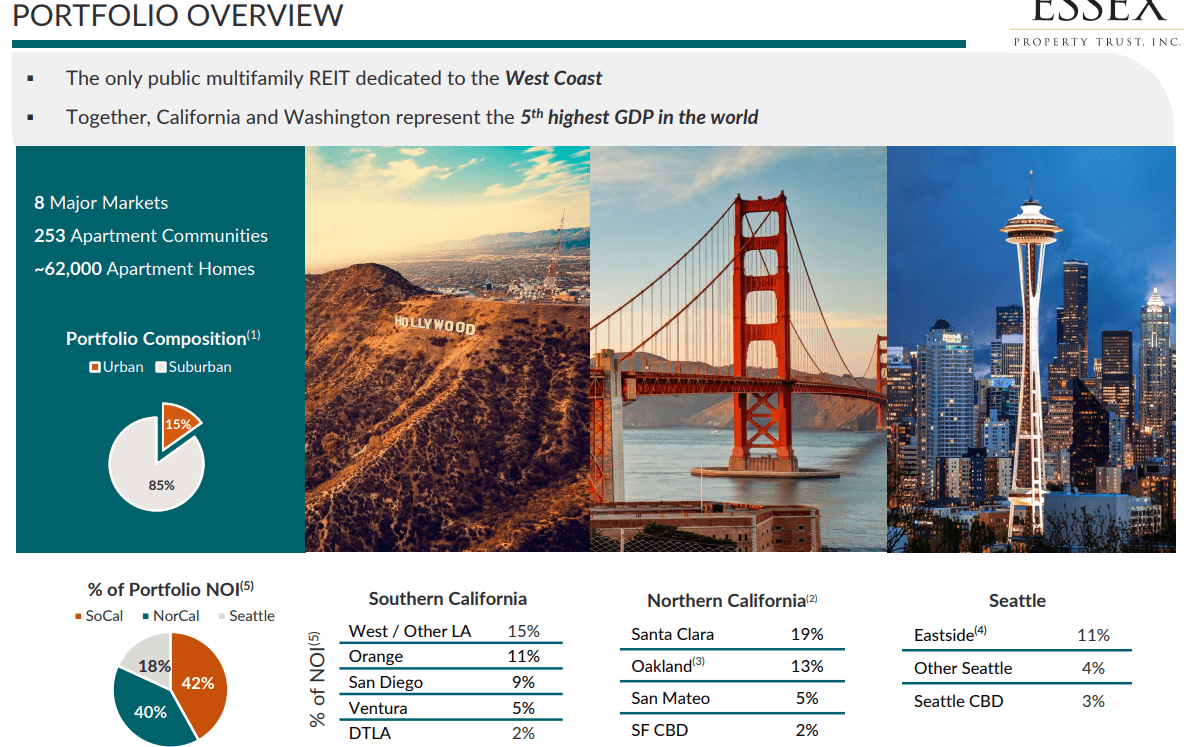

Essex Property Trust: A Dividend Aristocrat Apartment REIT You Can Trust

Further Reading

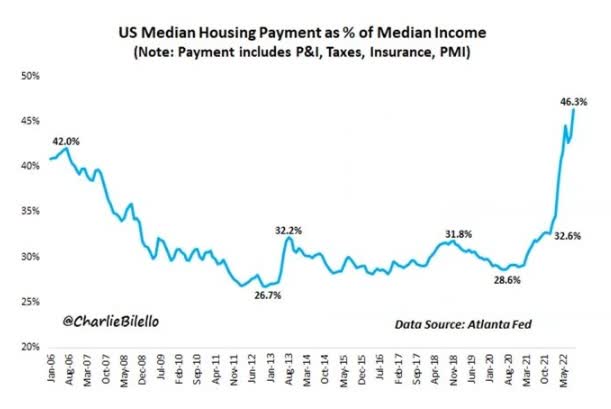

What’s the investment thesis for Essex? It can be summarized by a single chart.

Charlie Bilello

Home affordability has never been worse in US history.

It takes almost 50% of the median American’s income to buy a house. But everyone needs a roof over their heads, and that’s where Essex Property comes in.

(Source: investor presentation)

This BBB+ rated dividend aristocrat REIT was one of just 17 REITs that didn’t cut their dividend in the Great Recession. And guess what they own? 253 apartments in Seattle and high-cost California, where home prices are even more obscene.

ESS’s apartments are in some of the richest cities in the country, with very favorable demographics for apartments.

- median home price of $983K

- median household income $115K vs $71K national median

- average rent-to-income ratio of 23.5% (33% or less is considered affordable)

ESS’s apartments are a bargain compared to buying a home in these rich cities.

And guess what else?

| Investment Strategy | Yield | LT Consensus Growth | LT Consensus Total Return Potential | Long-Term Risk-Adjusted Expected Return |

| Essex Property Trust | 4.1% | 7.3% | 11.4% | 8.0% |

| REITs | 3.9% | 6.1% | 10.0% | 7.0% |

| Schwab US Dividend Equity ETF | 3.4% | 8.6% | 12.0% | 8.4% |

| 60/40 Retirement Portfolio | 2.1% | 5.1% | 7.2% | 5.0% |

| Vanguard Dividend Appreciation ETF | 1.9% | 10.0% | 11.9% | 8.3% |

| Dividend Aristocrats | 1.9% | 8.5% | 10.4% | 7.3% |

| S&P 500 | 1.7% | 8.5% | 10.2% | 7.1% |

| Nasdaq | 0.8% | 10.9% | 11.7% | 8.2% |

(Source: DK Research Terminal, FactSet, Morningstar)

ESS is growing at over 7% per year, faster than the REIT sector’s 6.1%. It yields slightly more but that’s a yield that’s much safer than not just most REITs but most other companies, of any kind.

In fact, analysts think that ESS’s strong position in west coast apartments could deliver almost Nasdaq-like returns in the future, but with a 5X higher very safe yield today!

But you don’t have to wait for decades to get rich with ESS. Because just look at how undervalued it is.

Essex Property: A Wonderful Company At A Wonderful Price

- fair value: $314.34

- current price: $216.58

- discount: 31%

- DK quality rating: 95% low-risk 13/13 Ultra SWAN quality dividend aristocrat REIT

- DK rating: potential very strong buy

What does a 31% undervalued 4% yielding aristocrat growing at 7.3% mean for investors in the short-term?

Essex Property Trust 2025 Consensus Total Return Potential

FAST Graphs, FactSet

How about potentially 64% returns in the next three years? That’s a Buffett-like 18% annual return from a high-yield aristocrat with a decades-long secular megatrend at its back.

Coiled Spring Essex Property Trust Has The Potential To Soar 56% By The End Of The Year

FAST Graphs, FactSet

If ESS were to grow as expected and return to fair value by the end of the year, that would be a potential 52% gain. Do I think ESS is actually going to go up 52% in a year? No, but that’s what its fundamentals would justify.

That’s how much of a coiled spring this 27-year dividend streak aristocrat is.

If the market does take off this year, surprising most investors, a coiled spring like ESS could easily achieve a 30% return. But more importantly, over decades, that 11% to 12% return potential could deliver life-changing income and wealth.

- 14X inflation-adjusted return over 30 years (retirement time frame)

- 59X inflation-adjusted return over a 60-year investing lifetime

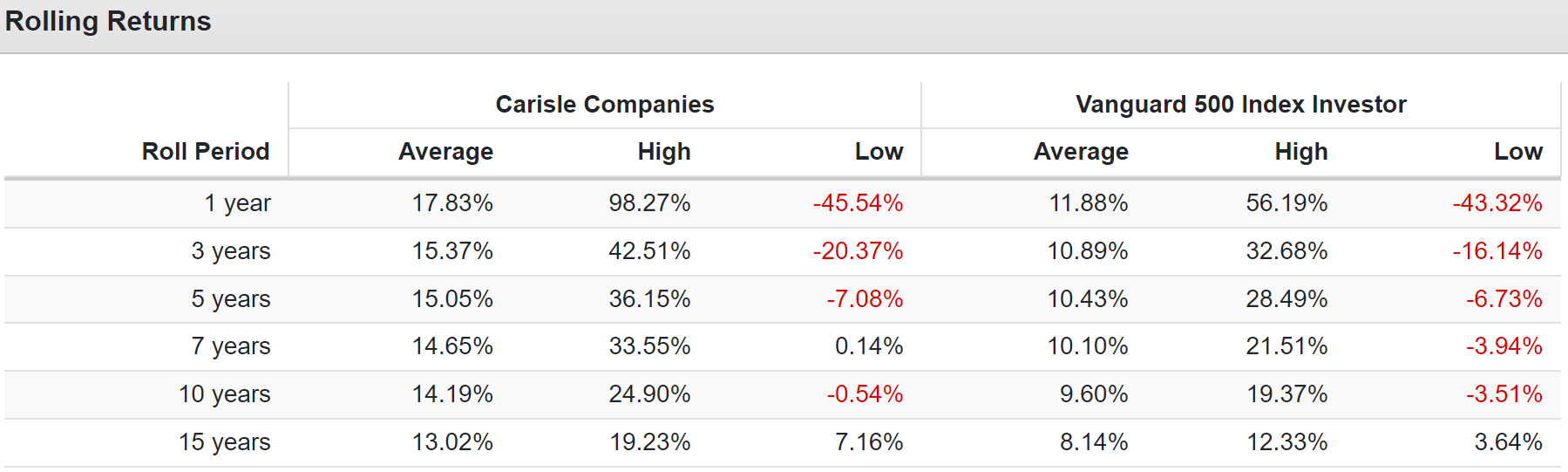

Carlisle Companies: One Of The Best Hyper-Growth Aristocrats You’ve Never Heard of

Further Reading

The safest dividend is the one that’s just been raised, is a famous axiom on Wall Street. Well, guess what? CSL raised its dividend by 39% in 2022.

How’s that for management saying it’s confident in this business? Even more impressive? That was its 46th consecutive annual dividend hike. CSL is going to become a dividend king in 2026, or I’ll eat my hat.

Even better?

This construction-focused industrial has a $40 trillion to $150 trillion infrastructure megatrend that analysts expect to drive 16% long-term growth and 17% long-term annual returns.

| Investment Strategy | Yield | LT Consensus Growth | LT Consensus Total Return Potential | Long-Term Risk-Adjusted Expected Return | Long-Term Inflation And Risk-Adjusted Expected Returns |

| Carlisle | 1.2% | 16.0% | 17.2% | 12.0% | 9.8% |

| Schwab US Dividend Equity ETF | 3.4% | 8.6% | 12.0% | 8.4% | 6.1% |

| Vanguard Dividend Appreciation ETF | 1.9% | 10.0% | 11.9% | 8.3% | 6.1% |

| Nasdaq | 0.8% | 10.9% | 11.7% | 8.2% | 5.9% |

| Dividend Aristocrats | 1.9% | 8.5% | 10.4% | 7.3% | 5.0% |

| S&P 500 | 1.7% | 8.5% | 10.2% | 7.1% | 4.9% |

| REITs | 3.9% | 6.1% | 10.0% | 7.0% | 4.7% |

| 60/40 Retirement Portfolio | 2.1% | 5.1% | 7.2% | 5.0% | 2.8% |

(Source: DK Research Terminal, FactSet, Morningstar)

Wow, 17% returns over the long term? That would run circles around pretty much any investment strategy on Wall Street!

- 65X inflation-adjusted return potential over a 30-year retirement time frame

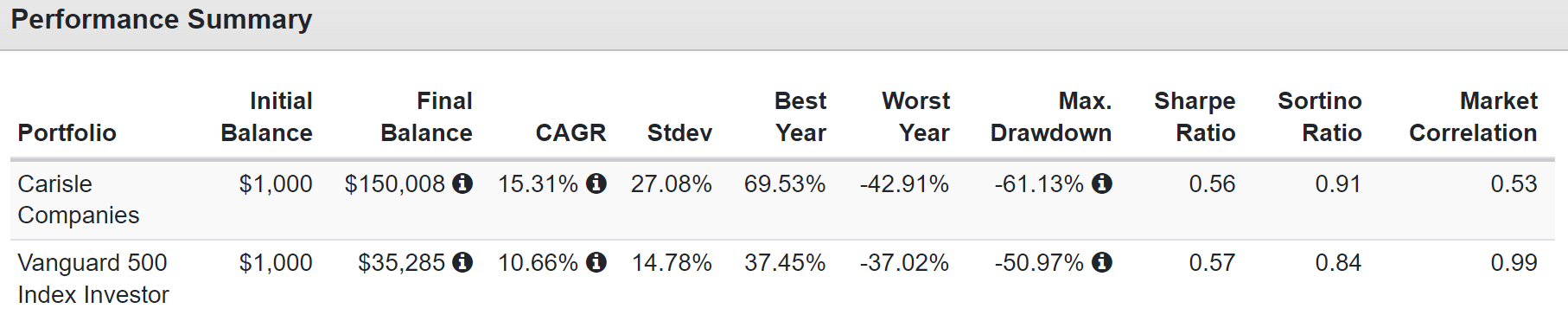

Historical Returns Since 1987

Portfolio Visualizer Premium

This is a hyper-growth aristocrat (and soon-to-be dividend king in my opinion) that has delivered 150X returns over the last 35 years.

- 58X adjusted for inflation vs. 14X S&P 500

Portfolio Visualizer Premium

Not only is CSL expected to keep delivering returns similar to what it has in the past, of around 18% annually on a 12-month rolling basis, but don’t forget this is a bear market coiled spring aristocrat.

- fair value: $413.77

- current price: $241.98

- discount: 42%

- DK quality rating: 91% quality medium-risk 13/13 Ultra SWAN dividend champion

- DK rating: potential ultra-value buy

CSL is trading at 11X earnings and historically trades at 20X.

Its cash-adjusted PE is just 9.3X, pricing in almost no growth from one of the fastest-growing aristocrats on earth.

What kind of returns are possible from such a table-pounding aristocrat buy?

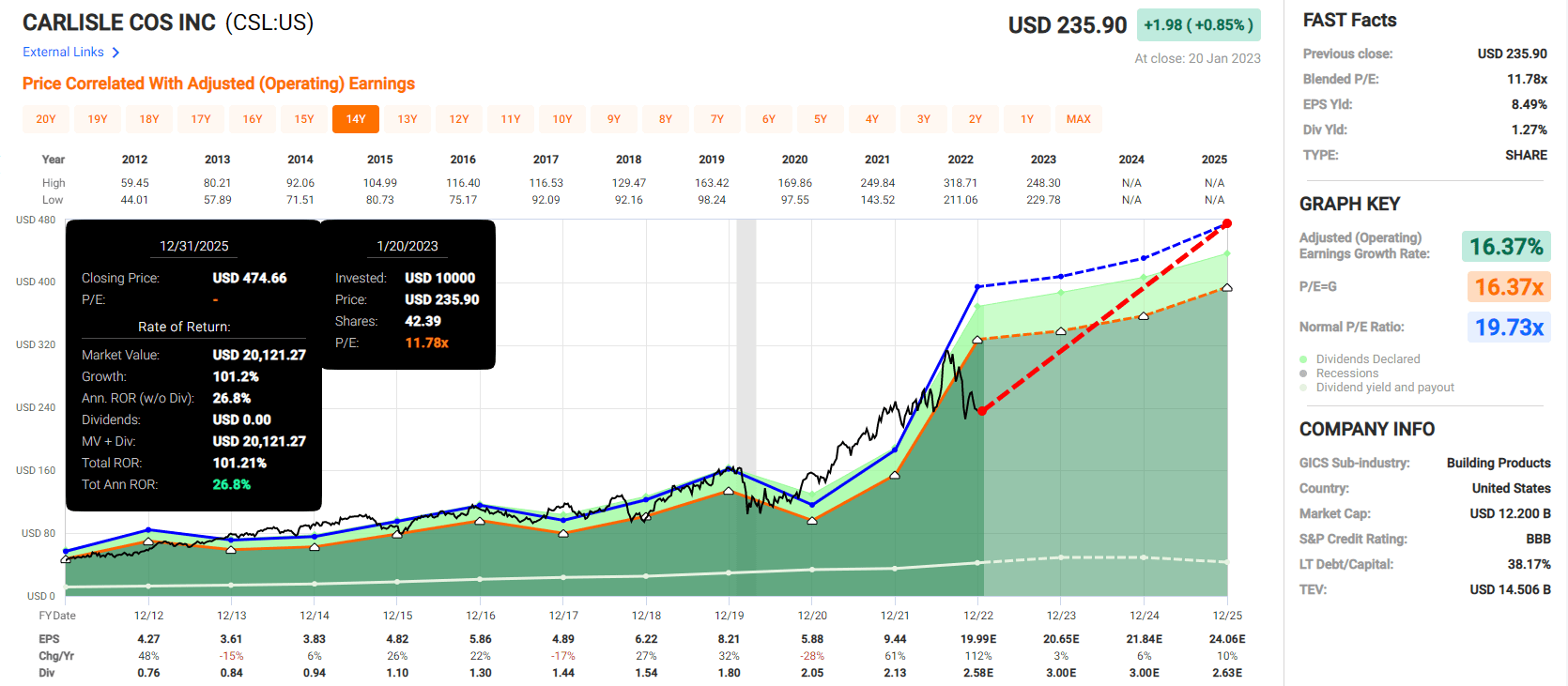

Carlisle Companies 2025 Consensus Return Potential

(Source: FAST Graphs, FactSet Research)

How many aristocrats do you know growing faster than Microsoft (MSFT) which could potentially double in three years? That’s a Buffett-like 27% annual return potential.

(Source: FAST Graphs, FactSet Research)

Are there aristocrats more undervalued than CSL? Sure, VFC is 47% undervalued.

Are there aristocrats growing faster than CSL? Sure, LOW is growing at almost 21%.

But how many aristocrats growing at 16% are trading at a Buffett-style “fat pitch” table-pounding cash-adjusted PE of 9.3X? Only Carlisle.

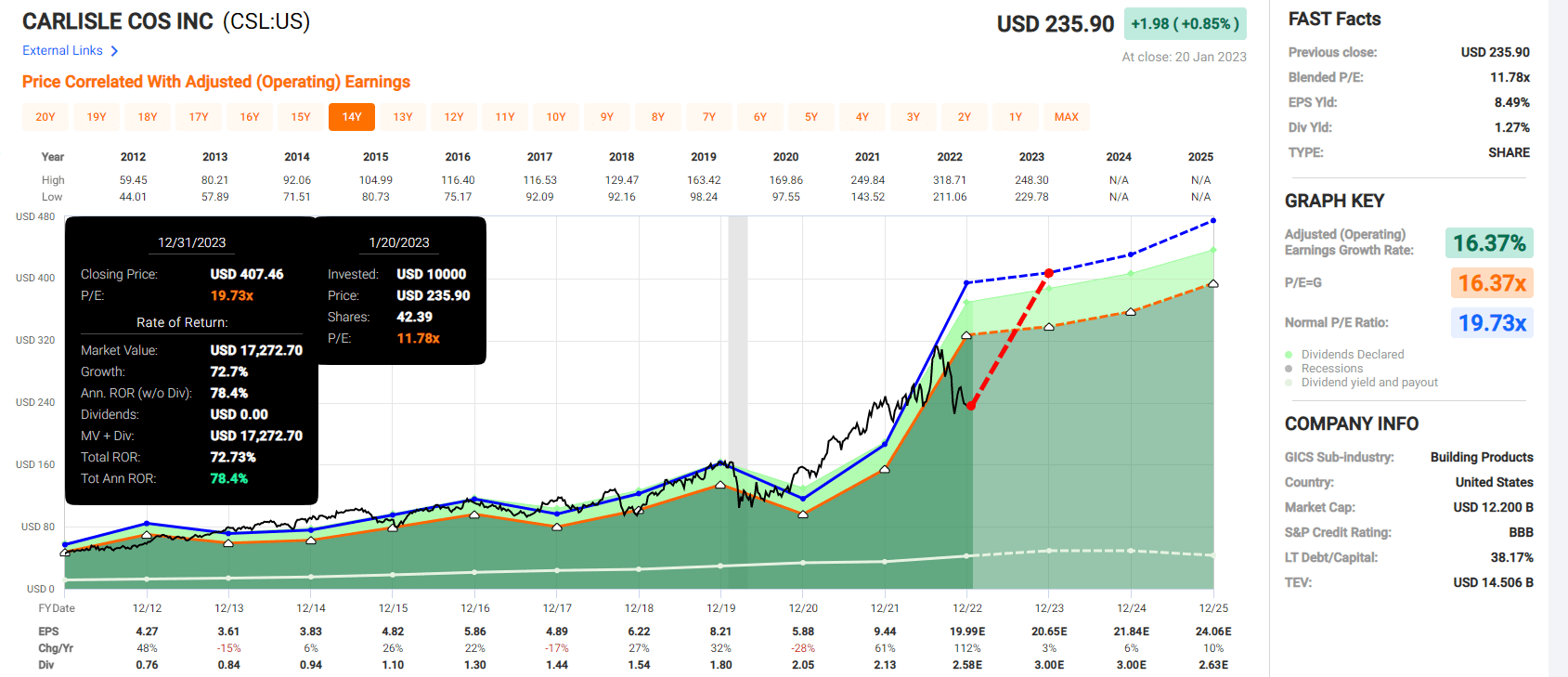

What if we avoid a recession in 2023? What if we avoid recession entirely? Then Carlisle is one of the most tightly coiled aristocrat springs of all and could potentially deliver a 40% gain in 2023.

On the way to potentially over 6000% long-term inflation-adjusted returns in the coming decades.

When such life-changing returns are possible from a company this safe and high quality, demanding a 20% lower price (a 7.4X cash-adjusted PE) to earn an extra 25% doesn’t just seem foolish, it seems downright reckless.

Bottom Line: ESS And CSL Are Coiled Spring Aristocrats You Can Safely Buy Today

Let me be clear: I’m NOT calling the bottom in ESS or CSL (I’m not a market-timer).

Ultra SWAN quality does NOT mean “can’t fall hard and fast in a bear market.”

Fundamentals are all that determine safety and quality, and my recommendations.

- over 30+ years, 97% of stock returns are a function of pure fundamentals, not luck

- in the short term; luck is 25X as powerful as fundamentals

- in the long term, fundamentals are 33X as powerful as luck

While I can’t predict the market in the short term, here’s what I can tell you about ESS and CSL.

Both are highly undervalued coiled spring dividend aristocrats that offer high-yield and hyper-growth investors something incredible.

Impeccable safety and quality during this recession, combined with some of the best valuations in years.

That combination of yield, growth, and value creates the potential for 50+% gains in a year or two, all while you sleep well at night knowing that your money is in safe hands.

These are skilled management teams and some of the most dividend-friendly corporations on earth.

They have survived and thrived through dozens of recessions, bear markets, and interest rates and inflation environments that make our current situation seem tame by comparison.

If you’re looking for rock-solid coiled spring aristocrats that could potentially deliver 30% to 40% returns in 2023 and life-changing returns 1300+% long-term, then ESS are CSL are well worth considering today.

Be the first to comment