TatyanaGl

Introduction

I have a physical watchlist I use to keep track of the stocks I want to add to my portfolio or buy more of. Last week, I added another ticker to that list. It now contains another healthcare company. I decided to look for a buying opportunity in the veterinarian healthcare company Zoetis (NYSE:ZTS). This New Jersey-based company has a dividend yield of slightly less than 1%. However, it has extremely high dividend growth, the benefit of offering top-tier products in a quickly growing healthcare segment, and high free cash flow growth. While I get that people won’t like a sub-1% dividend yield, I think the company is a great addition to most dividend growth portfolios thanks to its ability to deliver outperforming total returns.

In this article, I will tell you why.

What’s Zoetis?

I own two healthcare companies in my dividend growth portfolio:

- AbbVie (ABBV): A high-yield company operating in the drug manufacturers industry.

- Danaher (DHR): A fast-growing supplier of diagnostics and research supplies yielding 0.4%. I covered the company in October.

The company behind the ZTS ticker is a combination of both. The company operates in the drug manufacturers industry (specialty & generic) with a dividend yield of less than 1.0%.

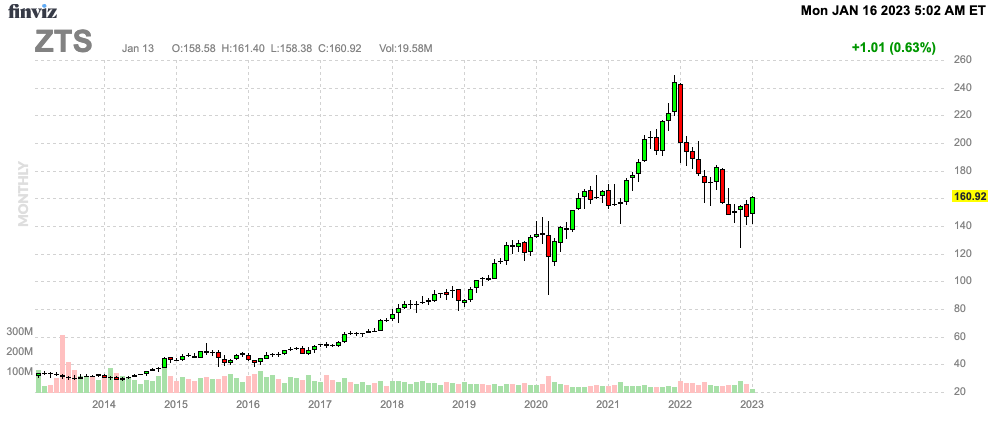

With a market cap of $75 billion, Zoetis is one of the world’s largest pharmaceutical companies. Incorporated in 2012, the company doesn’t have a very long stock price history.

FINVIZ

This is because Zoetis is a spin-off from healthcare giant Pfizer (PFE), which decided to spin off its animal health assets in a move to focus on its higher-margin prescription drug business.

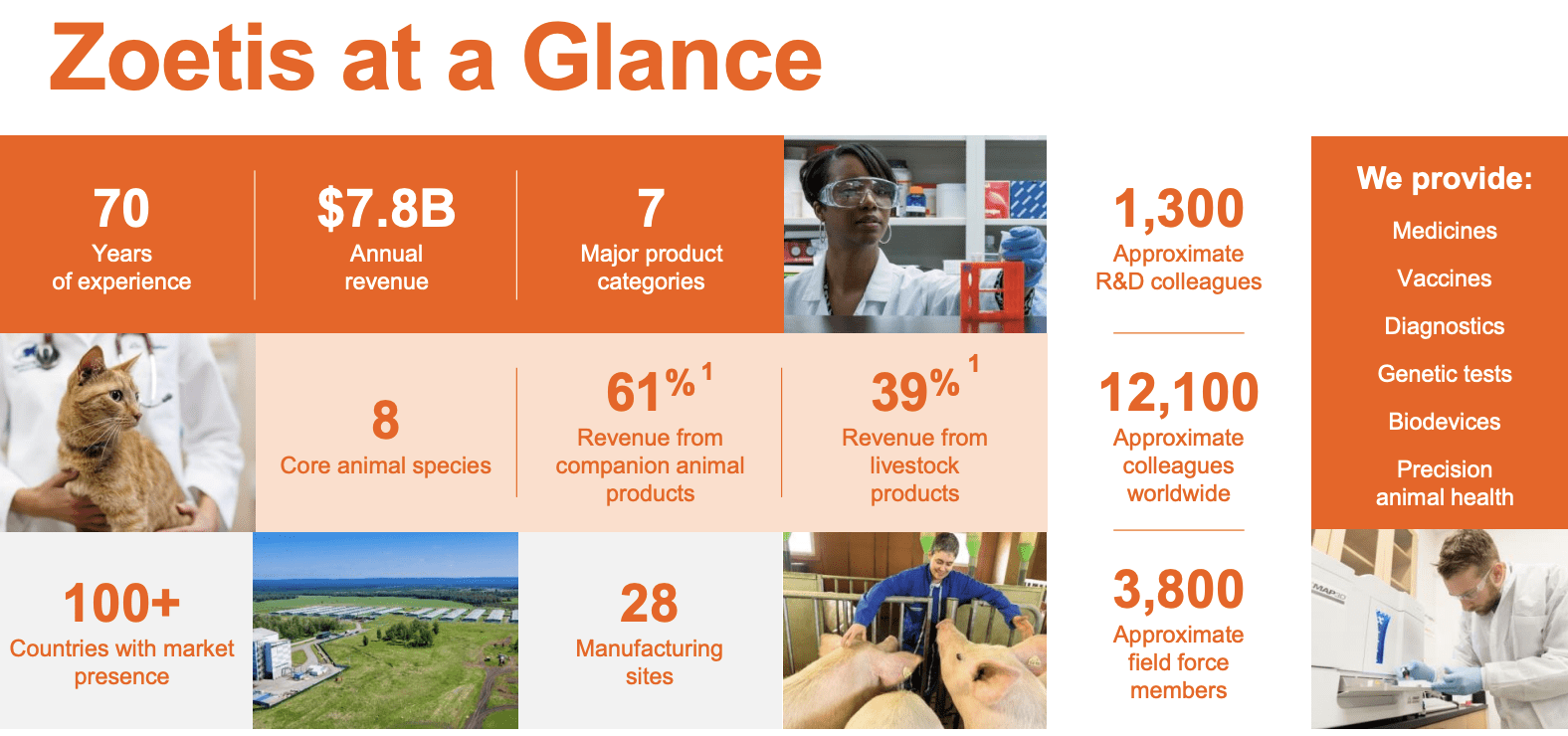

Now, the company is a global leader in animal health, focusing on discovering, developing, manufacturing, and commercializing medicines, vaccines, diagnostic products, services, and so much more.

Zoetis generates roughly 40% of its sales from livestock products. The other 60% are generated from companion animal products, which target cats, dogs, and other animals we don’t eat.

Zoetis

In 2021, the company generated 22% of its money from vaccines, an important part of companion and livestock animals. Half of the company’s revenues were generated in the United States.

The company’s top 10 products account for 47% of total revenue. These products are part of a portfolio of more than 300 product lines, including 15 leading blockbuster brands that do more than $100 million in annual revenue each. The average market life of the top 24 product lines and products is 30 years. In the past five years, the company introduced more than 1,000 new products and lifecycle innovations.

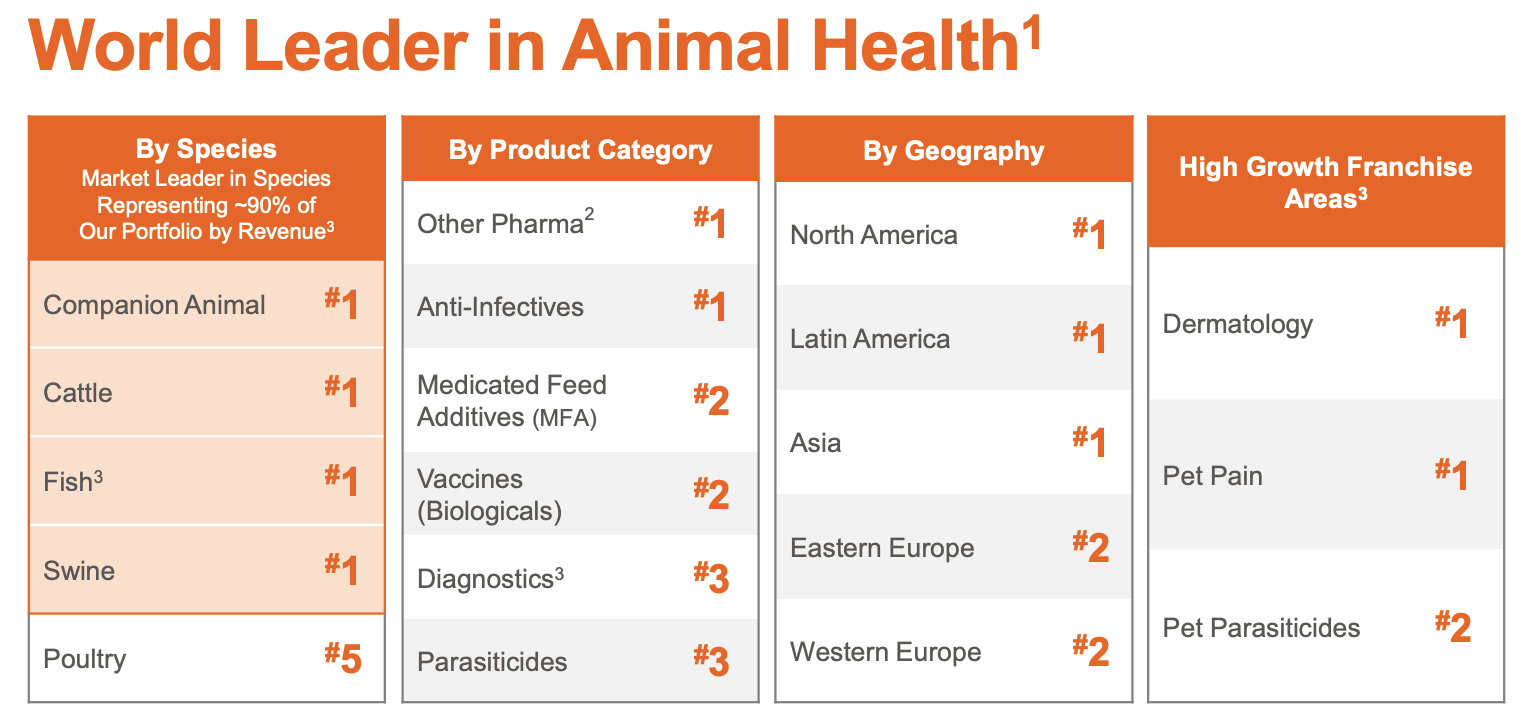

Moreover, the company is the market leader in all animal species but poultry and all regions except for Europe. Note that the company is also gaining market share. In early 2022, it was number three in Western Europe, to give you one example.

Zoetis

In other words, the company is well-protected against generic brands and the loss of patents.

Moreover, while livestock healthcare demand is somewhat cyclical due to consumer spending on proteins, the company does benefit from anti-cyclical spending on pets, which grew by almost 4% in the Great Financial Crisis of 2009, according to CEO Kristin Peck. So, overall, ZTS does have a very resilient business model.

It also benefits from these key trends:

- More people buy pets.

- People spend more time with pets.

- People are more willing to spend money on pet health.

- Innovation is driving market growth (new possibilities in health).

- Global protein production is rising (livestock demand).

- Protein production needs higher efficiency.

- Sustainable food production is key.

It’s also fast-growing.

Zoetis Is A Fast-Growing Healthcare Company

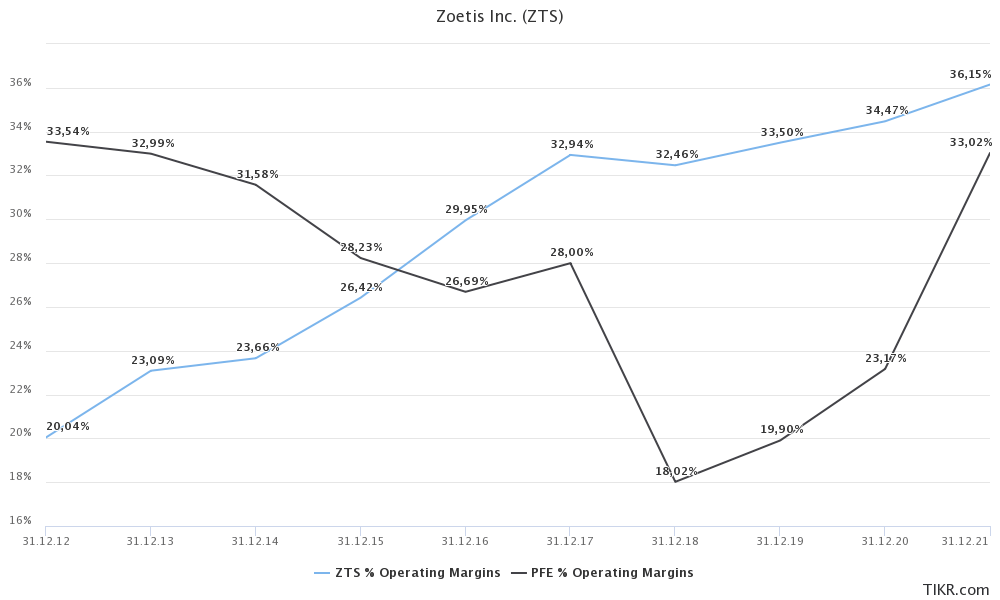

Earlier in this article, I said that Pfizer spun off Zoetis because it wanted to focus on higher-margin products. At least, that was one of the reasons the company stated publicly. Back in 2012, when Zoetis was incorporated, it had an operating margin of 20.0%. Pfizer had an operating margin of 33.5%. At the end of 2021, Zoetis had an operating margin of 36.2%, beating Pfizer by more than 300 basis points!

TIKR.com

Now, add that revenue growth is strong. In the 2012-2024E period, revenue is growing by 6.5% CAGR. That is a very satisfying number with consistent growth. In 2021, revenue growth was 16.5%. This year, it is likely 6.3%. Next year, that number could accelerate to 8.0%.

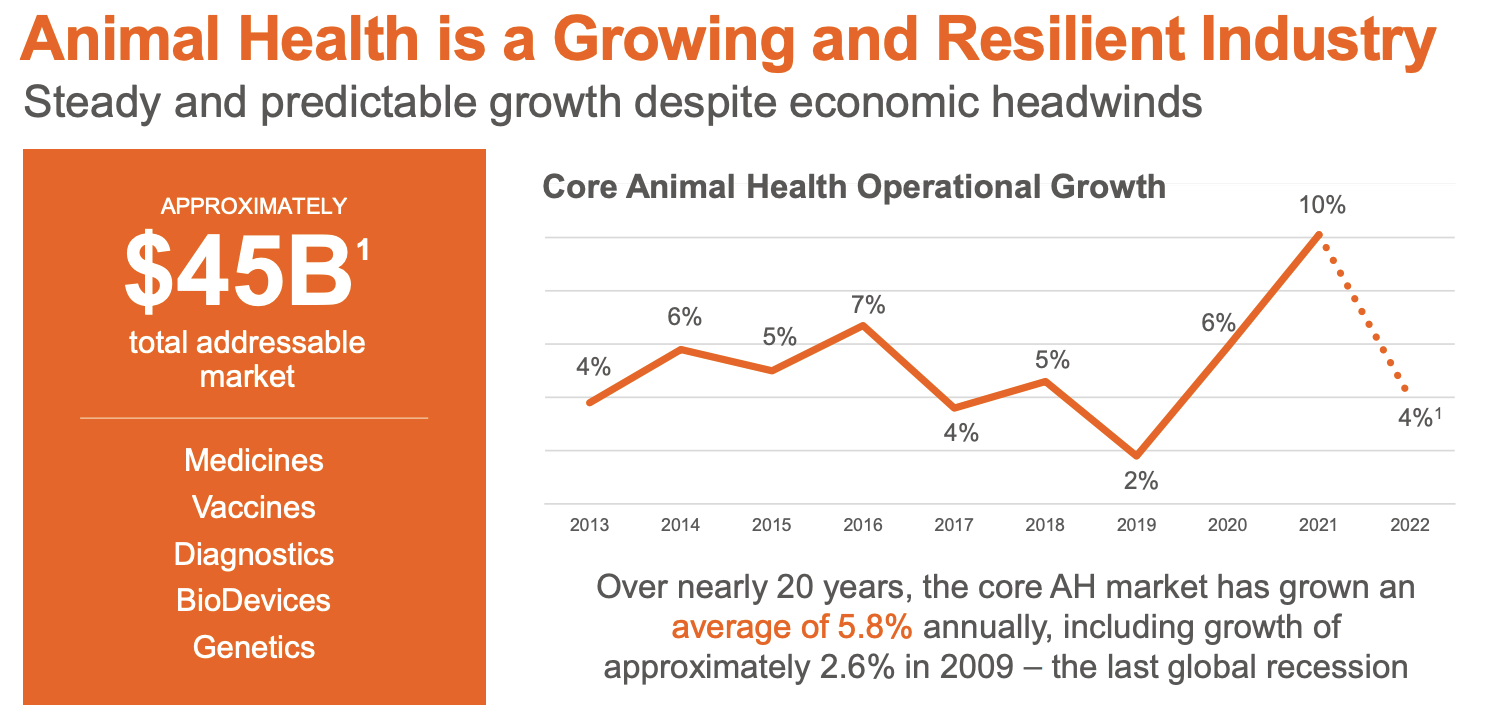

This means that Zoetis is outperforming an already strong industry average growth rate of 5.8%.

Zoetis

When adding the aforementioned margin expansion, it is no surprise that EBITDA growth in the 2012-2024E period is 13.1% CAGR.

However, it is important to mention that the company did run into some headwinds. In its third quarter (the most recent quarter), the company reported 1% higher revenues, yet a 5% decline in adjusted net income.

The company also lowered its 2022 guidance to reflect struggles due to supply constraints, veterinary workforce challenges, and foreign exchange rate headwinds. After all, the company generates half of its sales outside of the United States.

The 2022 operational revenue growth estimate was lowered to the 7%-8% range. This is down from the prior estimate of at least 9.5% growth.

Nonetheless, the company sees no reason to worry as these temporary issues are fading.

As we look toward the end of the year and into 2023, I expect us to continue setting the bar on innovation, cultivating a high-performing culture, and delivering superior customer experiences. All of this will have us growing significantly above the market and building enduring value for shareholders in this dynamic market.

Here’s what this means for shareholders.

The ZTS Dividend

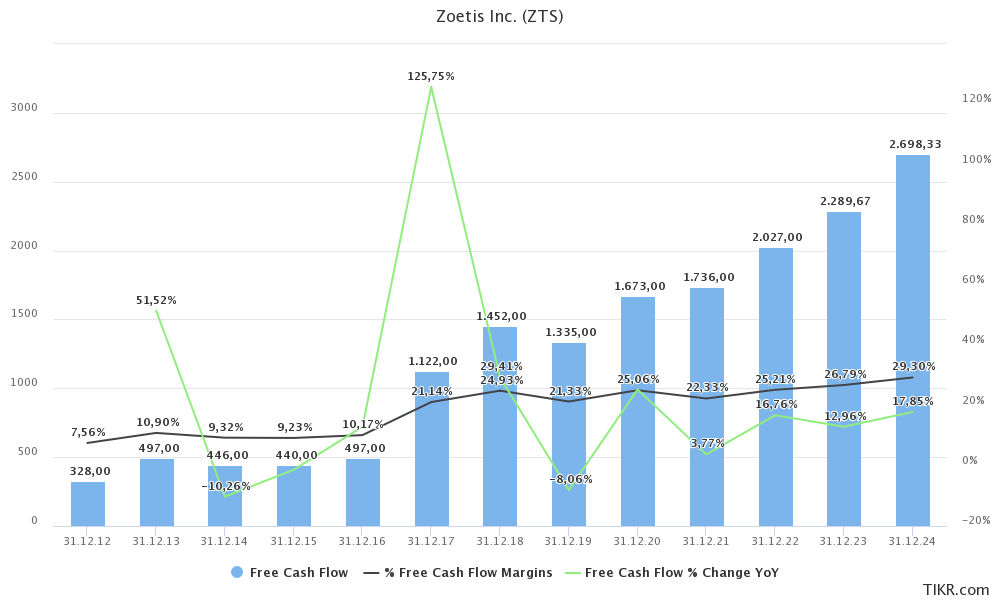

One of the charts I wanted to show in the segment above perfectly fits this article segment. Not only did the company improve margins, allowing for strong EBITDA leverage, but it also became increasingly cash-efficient.

Free cash flow, which is operating cash flow minus capital expenditures, is growing by 19.2% CAGR in the 2012-2024E period. Outperforming EBITDA growth by 610 basis points.

As the graph below shows, free cash flow has benefited from an FCF margin expansion from less than 8% to almost 30% in 2024E. Even better, the free cash flow growth rate is expected to remain in the high-double-digit territory.

TIKR.com

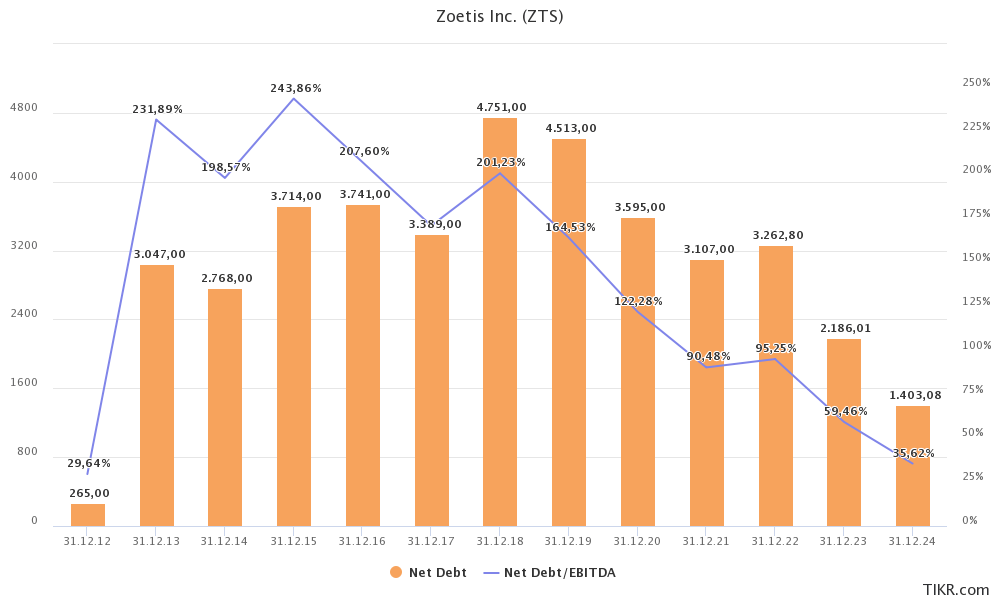

At this point, it’s also important to mention that the company has a healthy balance sheet, meaning it does not need to prioritize debt reduction over shareholder distributions. In 2018, the company had $4.8 billion in net debt. That was its all-time high with a leverage ratio of 2.0x EBITDA. This year, that number is expected to come down to $2.2 billion, or less than 0.6x EBITDA.

TIKR.com

As a result, the company has a Baa1 credit rating, which I believe will turn into an A rating in the years ahead.

With all of this in mind, we have a company that:

- Has high and growing free cash flow after dealing with R&D and CapEx requirements.

- Has a healthy balance sheet with rapidly declining net debt and a low leverage ratio.

This means there is a lot of room for shareholder distributions.

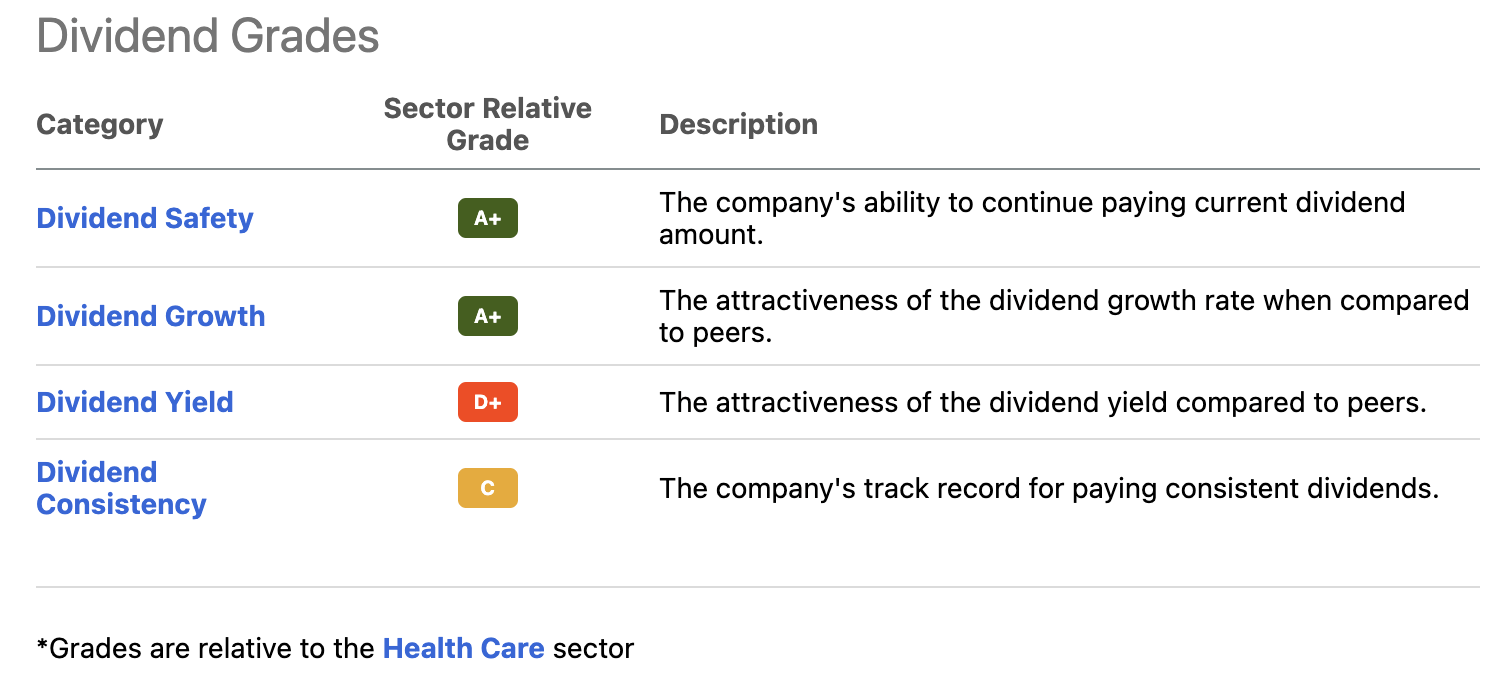

When looking at the Seeking Alpha dividend growth scorecard, we see something very typical for a young, fast-growing dividend growth stock. The company scores extremely high on safety and dividend growth yet, low on yield and consistency (I disagree with that, as I will show you in this article).

Seeking Alpha

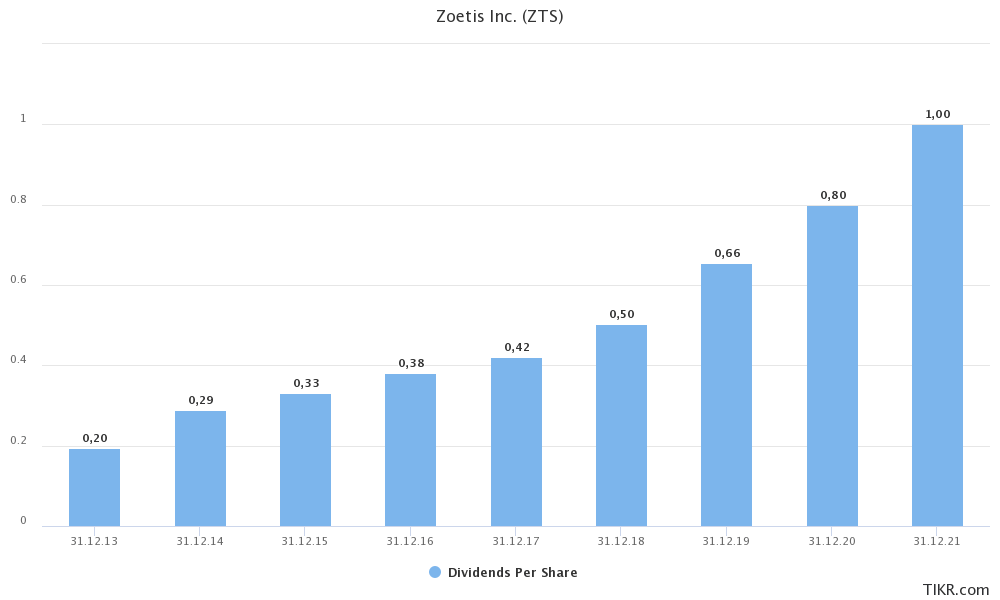

The company’s current dividend is $0.375 per share per quarter. That’s $1.50 per share per year or 0.93% of the current stock price. That is a low yield. The sector median is 1.4%, which explains the poor relative score.

However, that’s where the bad news ends. Dividend growth is fantastic. The company has fast-growing free cash flow and a dividend payout ratio of less than 30%.

The company started paying a dividend in 2013. Since then, it has been consistently hiked every year, which is why I disagree with the low dividend consistency score. However, bear in mind that the aforementioned grades are automatically generated. Hence, it’s always good to double-check, which is what we’re doing.

TIKR.com

Over the past five years, the average annual dividend growth rate was 20.8%.

These are the most recent hikes:

- December 2022: +15.4%

- December 2021: +30.0%

- December 2020: +25.0%

Moreover, the company also buys back stock, which is an indirect way to distribute cash to shareholders. It is more tax-friendly, yet it doesn’t end up putting more cash in the pockets of existing shareholders.

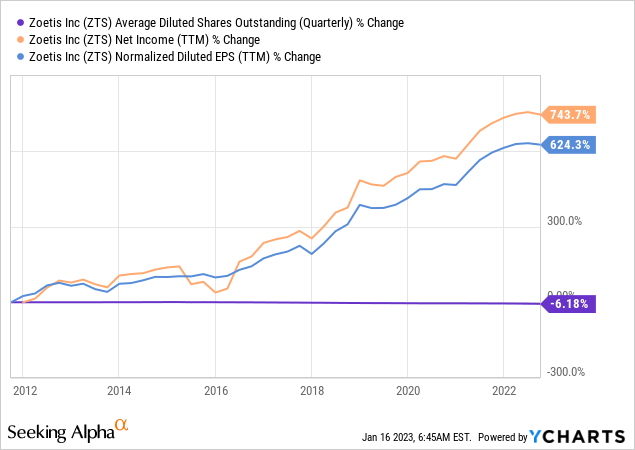

Over the past ten years, the company has net bought back 6.2% of shares outstanding. This is not a huge number, yet enough to leverage 624% net income growth into 744% earnings PER SHARE growth.

But wait, there’s more good news.

Outperformance & Valuation

A <1% dividend yield is low, and I get that people who depend on cash flow from their investments will skip this stock – or any stock with a yield this low.

However, the bigger picture is what matters. The company has all the characteristics that make a dividend stock a great investment (among other things):

- Rapidly rising free cash flow.

- A healthy balance sheet.

- A robust business model providing safety and growth.

When adding that dividend growth is very high and ZTS is spending additional cash on buybacks, we get high outperformance.

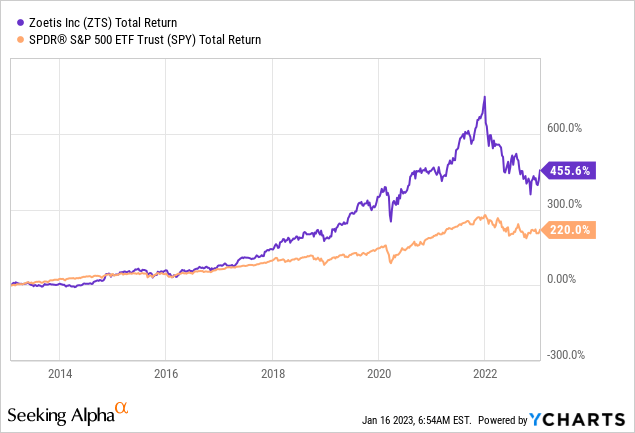

Since its spin-off, the company has returned 456%, outperforming the market by more than 230 points (not basis points).

While I do not expect outperformance to maintain this magnitude – after all, it was boosted by a significant surge in margins – I expect ZTS shares to outperform the market on a long-term basis.

On a side note, it has to outperform by a wide margin to make up for having a low yield. Otherwise, why would dividend investors bother buying it?

That said, ZTS shares are currently trading roughly 35% below their all-time high. That is a rather significant sell-off, as the market is down less than 20%. However, ZTS was a major winner of the pandemic, which caused the stock to surge by almost 130%. Now, a lot is being unwound.

- The pandemic trade has faded (investors went from growth to value stocks).

- Rates are rising.

- Economic uncertainty is high.

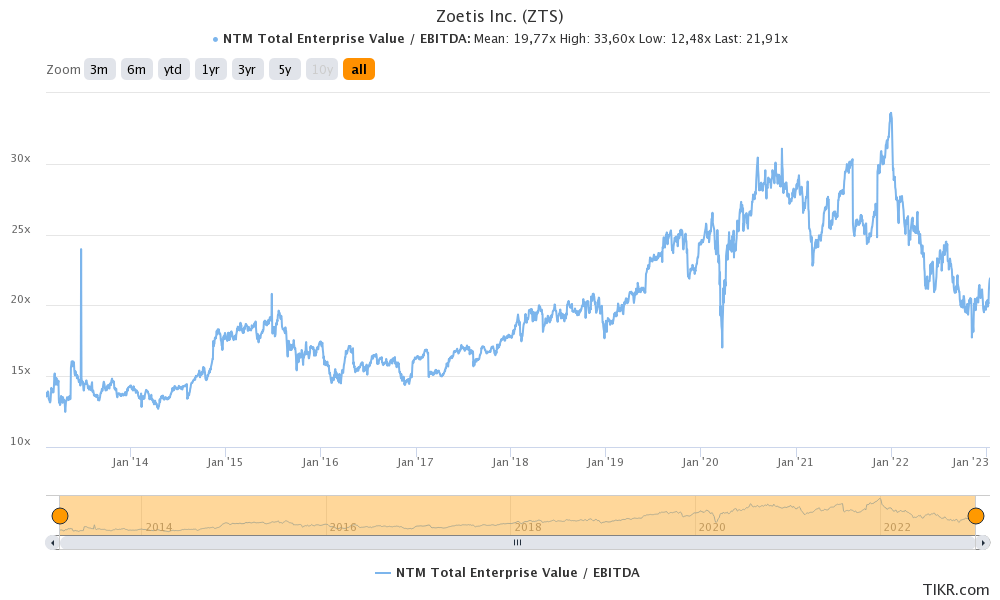

Yet, ZTS is still not cheap. The company is trading at 20.9x 2023E EBITDA, using its $75 billion market cap, $2.2 billion in net debt, and $3.7 billion in expected EBITDA.

Roughly 21x EBITDA is what the company used to trade at in 2019. During the pandemic, that number was closer to 30x.

TIKR.com

Moreover, the company’s average EBITDA growth rates are easing a bit to the high-single-digit range, which does warrant an elevated multiple, but nothing (far) above 20x NTM EBITDA.

The current analyst consensus price target is $209. This implies 30% more potential upside. I agree with that assessment.

Takeaway & Personal Considerations

In this article, we discussed Zoetis, a fast-growing dividend stock with a sub-1% yield, a dominant market position, a very healthy balance sheet, and the ability to maintain outperforming growth rates in its industry.

The company would be a great addition to my dividend growth portfolio as it adds high-quality healthcare exposure and dominance in an industry that, I believe, will continue to do well.

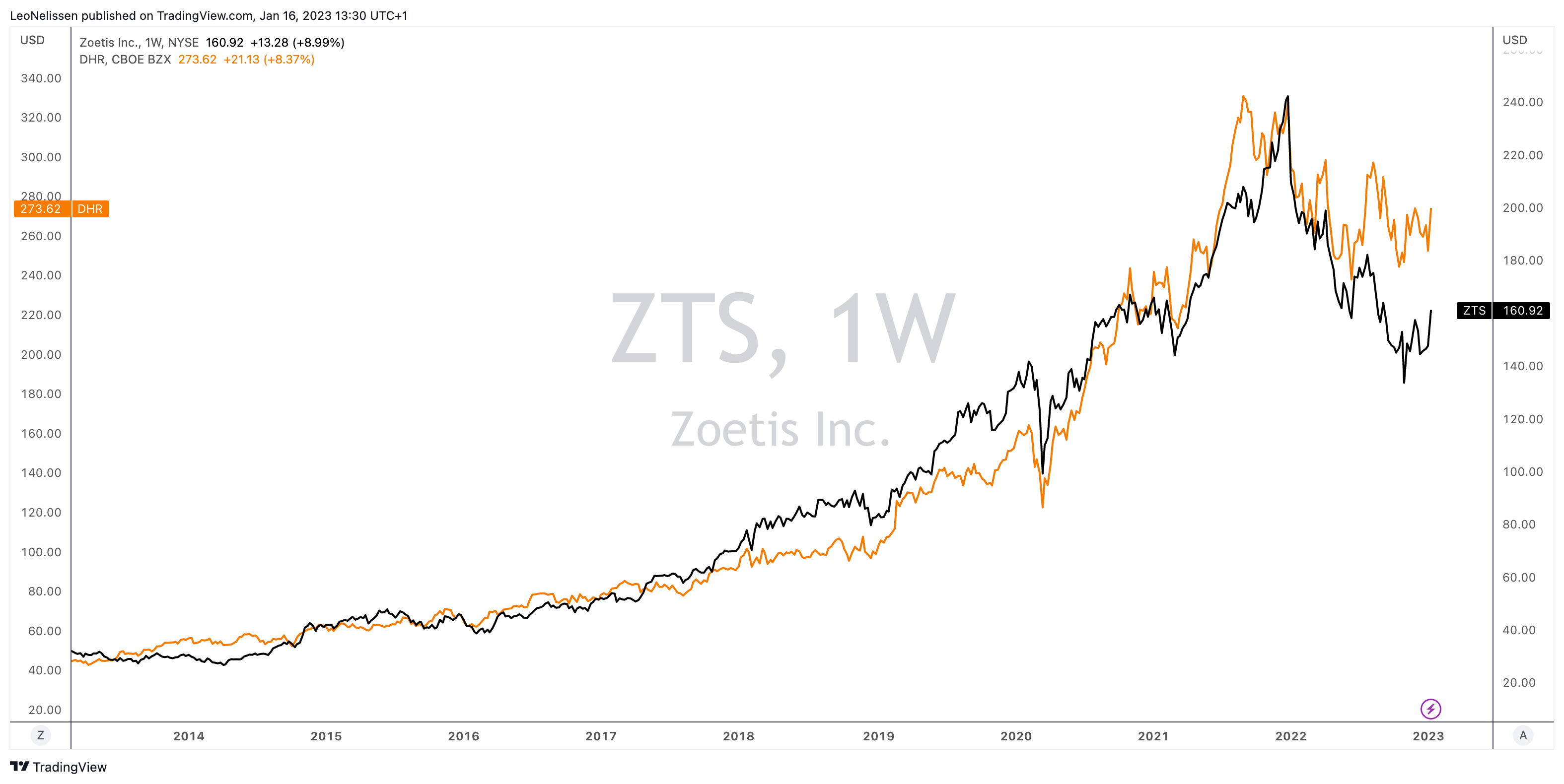

While I am trying to buy this stock on weakness, I am thinking of the combination of my existing holdings, Danaher and Zoetis. Danaher does give me healthcare exposure as it sells equipment to all major providers. It also does have high growth rates and a stock price highly correlated to Zoetis.

TradingView (ZTS, DHR (Orange))

This information doesn’t apply to most readers, yet after starting to be more open about my personal investments since this article last week, I think it makes sense to communicate these personal considerations a bit more.

That said, let me know what you think of Zoetis in the comment section down below!

Be the first to comment