Tryaging

With ZIM Integrated Shipping Services Ltd. (NYSE:ZIM) hitting new lows in December, I positioned myself against market sentiment and nearly doubled my exposure to the shipping company.

I believe the market is currently overly bearish on shipping companies, including those with competent management teams, strong balance sheets, and free cash flows.

ZIM Integrated Shipping is now my second-largest portfolio holding, and I believe the market is incorrect in assigning the company a P/E ratio of 5.9x. The technical chart profile also indicates that the stock has bottomed, which could indicate an impending upward retracement.

Not Oversold, But Seriously Punished In 2022

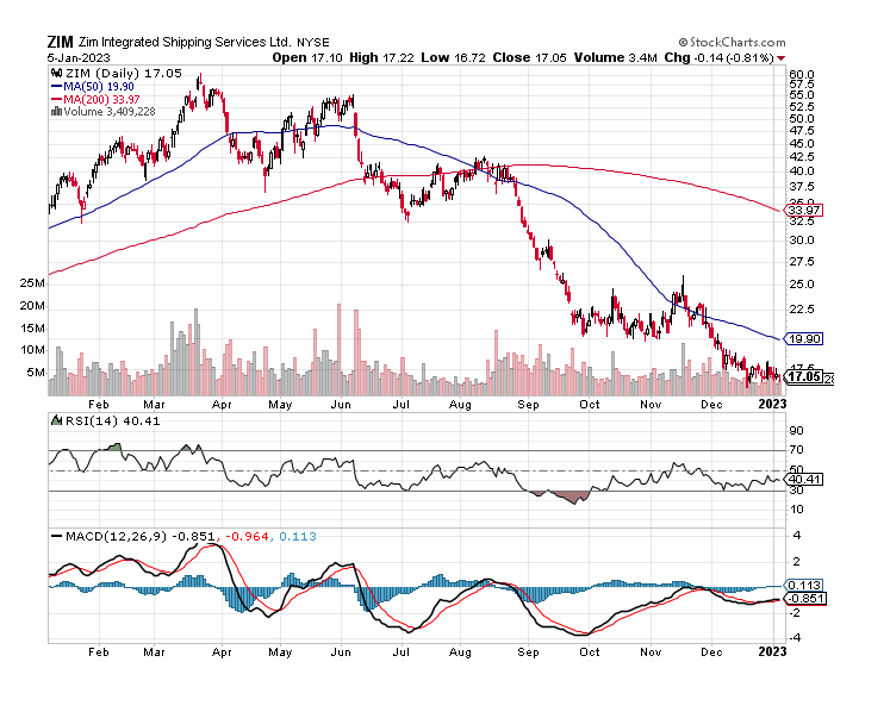

First, the bad news: ZIM Integrated Shipping’s chart picture over the last twelve months does not look promising. This year, the stock has made successive lows and been rejected at both the 200-day and 50-day moving average lines. The decline in cargo spot rates, which has wreaked havoc on the container shipping sector, explains the disappointing stock performance.

Having said that, there are signs that a bottom is forming in ZIM Integrated Shipping’s chart profile. Furthermore, a significant support level is forming at the $17 price level, from which the stock could launch an upward rebound.

Moving Averages (Stockcharts.com)

Spot Rates Will Remain Pressured, EBITDA Outlook for 2022

Due to falling spot rates in the shipping market, ZIM Integrated Shipping revised its EBITDA forecast for 2022. The company is now budgeting $7.4-7.7 billion in adjusted EBITDA, up from a $7.8 billion to $8.2 billion forecast in 2Q-22.

Given that spot rates have dropped to around $2.1K at the time of writing, representing a 77% YoY decline, the short-term outlook for ZIM Integrated Shipping’s adjusted EBITDA is negative.

Investors should expect a significant decline in EBITDA in 4Q-22 due to ongoing pressure on spot rates, and I believe the shipping company has a realistic chance of earning $6.5-6.8 billion in adjusted EBITDA.

Competitive Advantages of ZIM Integrated Shipping: Average Freight Rates And A Low-Debt Balance Sheet

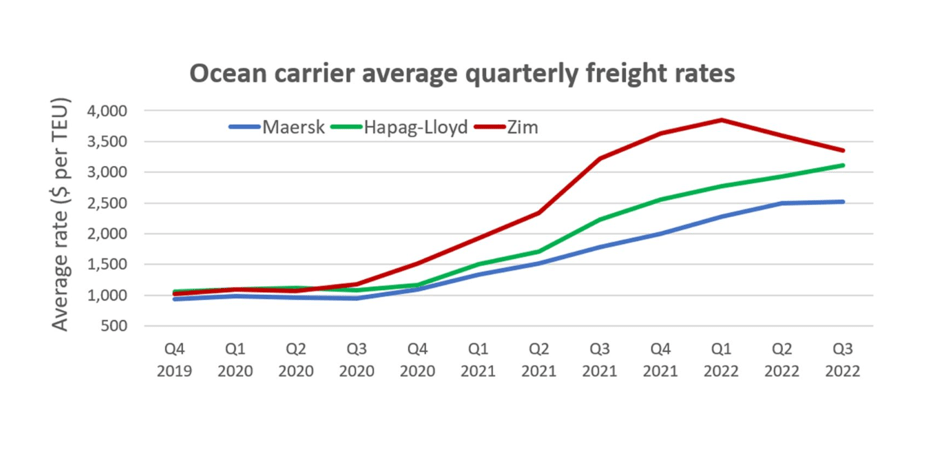

When compared to the competition, ZIM Integrated Shipping is still doing well. Average freight rates are comparable to those of companies such as Hapag-Lloyd and Maersk.

In 3Q-22, ZIM Integrated Shipping’s average freight rate increased 4% YoY to $3,353/TEU.

Average Shipping Rates (ZIM Integrated Shipping Services)

Aside from above-average cargo rates, ZIM Integrated Shipping had a net debt of only $250 million as of September 30, 2022, which is practically nothing. The low debt position could provide a significant competitive advantage, especially during a recession.

Personally, I believe ZIM is underappreciated for its strong balance sheet and low debt position. Regardless, it makes the stock even more appealing to me.

Declining Earnings Forecast, But Still A Highly Compelling Valuation

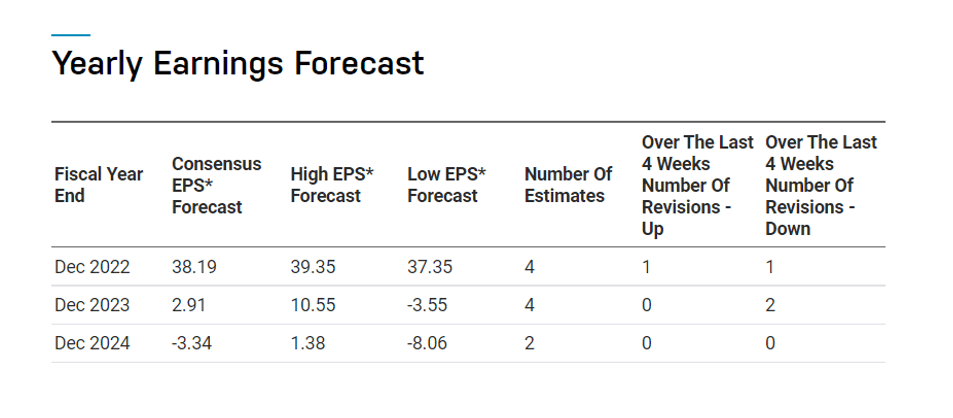

The consensus EPS forecast has fallen in the last month, according to Nasdaq, as spot rates for shipping containers continue to fall. The yearly earnings per share forecast for 2023 is currently $2.91, representing a $1.27 per share decrease (30%) since the end of November.

The market’s current average EPS implies a 2023 P/E ratio of 5.9x, which, in my opinion, indicates an outrageous undervaluation.

Yearly Earnings Forecast (ZIM Integrated Shipping Services)

Why ZIM Integrated Shipping Could See A Lower Valuation

ZIM Integrated Shipping has low debt on its balance sheet and contracted freight rates that are higher than average, providing downside protection for the shipping company’s valuation.

Even though the stock recently hit a new 52-week low, I believe the downside is rather limited here because the market has already fully priced lower cargo rates into shipping company valuations.

Spot rates may continue to fall in the short term, but ZIM Integrated Shipping, in my opinion, is in the best position of any shipper to navigate this downturn.

My Conclusion

This week, I increased my exposure to ZIM Integrated Shipping by about 100%, and I am prepared to double down on the shipping container company if the stock falls to new lows in the first quarter or later.

Despite all of the talk about a global recession, I believe ZIM Integrated Shipping is a good shipping company to invest in because of its low debt.

With its variable distribution policy, management has proven to put shareholders first, and while the dividend yield moving forward will be much lower than in the past, I believe ZIM Integrated Shipping’s low valuation does not do its well-managed business, above-average cargo rates, and fortress balance sheet justice.

Whether you like it or not, I believe ZIM is a good buy at 5.9 times earnings.

Be the first to comment