vitapix

Dear readers/subscribers,

York Water (NASDAQ:YORW) remains the same company that I’ve been reviewing for over a year. The upside is limited at higher valuations, and even at lower valuations, you’re seeing relatively low double-digits annually. What you get is the sort of safety that has existed longer than most nations in their current state.

York Water has a longer history and a dividend than most central-European, African, Asian, or other nations in the current configurations – and there aren’t many companies that can claim this. That in itself has value. I use similar arguments to showcase the upside or safety for companies like LVMH (OTCPK:LVMUY), and some of their brands which are over half a millennia old at this point.

So, I’m no stranger or underestimating that sort of conservative fundamental.

But, it doesn’t nullify that we’re wanting a good valuation before investing our hard-earned money.

Updating on York Water (and news) for 2023

So, York Water is still the same play I’ve been writing about for over a year now. It’s the longest dividend-paying stock under a certain set of circumstances/rules. It’s neither large nor its market cap small. Under most circumstances, it wouldn’t catch the eye of most investors – it’d be too small, and too uninteresting.

However, the dividend history isn’t everything that YORW has going for it, of course. It’s also a water business – and water business investments have the same sort of fundamental safeties and potential positives as other rate-based companies – such as waste management/recycling, electricity/power and heat. The argument here is you exchange growth potential, of which there is very little in these companies, for the safety found in slow but inexorable growth in income, hopefully in line with, or above the rate of overall inflation.

YORW’s line of business does not make it immune to the current inflation and overall cost increases that we’re currently seeing. The recent rate cases allow for the company to increase for 75,000 water and wastewater customers across three core counties. Now, even with these increased rates, the company is one of the lower-cost utilities across the nation. The latest rate case is expected to increase the average bill by about $6.5/share to just above $53, which for one change is still quite substantial. It’s a 22 cent per day increase, which brings the per-gallon cost to around a penny each.

Last time the company increased its rates was in 2019.

The funds will be used, among other things, in the following ways:

- Retrofitting existing infrastructure, including classical relining, reinforcement and replacing of up to 4.5% of the water mains, to both increase efficiency and lower interruptions in service.

- Design upgrades to the Lake Williams dam to get another 100 years of service out of the asset.

- Standard maintenance and replacing service lines, meters, hydrants, etc.

- Replacement of still-existing lead service lines (at no cost to customer).

- A new wastewater treatment plant due to increased demand from a growing customer base.

- Investments in physical and cyber-based security to address the new set of threats.

Now, there are some specifics to be aware of. Water rates are set by the company’s uniform rate structure – wastewater rates are not. The company’s wastewater rates are instead based upon what specific system is in place, and some of those increases are higher due to investments and low historical rates – the average wastewater bill is up significantly more than the average water bill, by about $26 per month.

So, as you can see, customers of YORW are in no way immune to what the company is seeing here.

Other than the new rate case, the company fairly recently completed the M&A of the SYC Wastewater Treatment plant and related collections systems in New York County – as well as a water system in Franklin. So when I say that there’s very low growth, it’s low but sometimes there’s some, because these inorganic additions obviously contribute to earnings. However, such M&A’s in this business segment are extremely long processes, and the number of customers are sometimes extremely limited – as evidenced by the recent M&A of the Albright Estates, mobile homes, which add a total of 60 residential water customers in the area, and the Scott Water company in Franklin as well, which added a grand total of 25 customers.

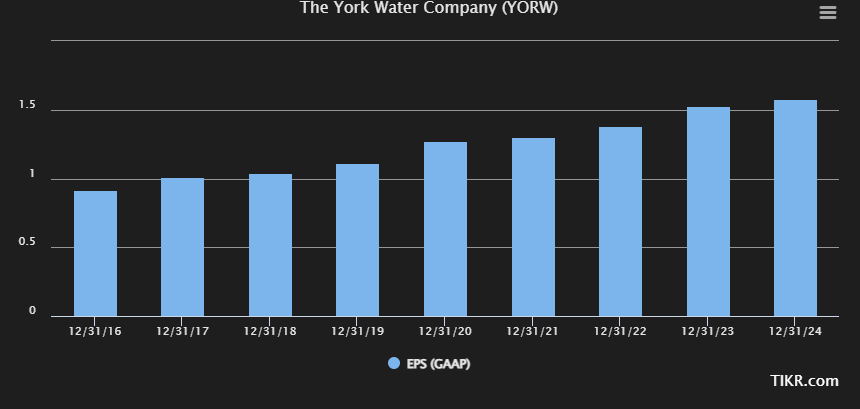

So, growth is slow, and this is expressed in the current set of forecasts for the coming few years. “Slow but steady” is the mantra that’s quite suitable here, if you take a look to at least the 2024E, which is as far as this company’s forecast goes. Remember the company’s size – it’s actually quite a wonder that we have as much as this, given that most company’s this side often don’t even have analysts following.

YORW Forecasts (TIKR.com)

Beyond that, S&P Global analysts don’t even take a stab at the company’s dividend forecasts. We have some from FactSet, and these call for the dividends to essentially keep growing in line here. As it stands, the company seems quite set and clear to keep growing here.

This company remains one of those businesses that works with not a 5 year or even a 10-15 year vision – it works in the centuries. This can be seen when looking at some of the latest property purchases YORW engages in, including a very recent one in December, where the company acquired 54 strategic acres adjacent to a core filtration plant. What the company says is fairly self-explanatory in terms of how executives seem to think here.

“Just as our predecessors had the foresight and vision to establish York Water’s treatment works on the elevated slope overlooking the City of York, to secure the high ground and benefit from gravity, we invest for the needs of our customers not simply today, but for 30, 50, or 100 years from now.”

(Source: YORW President, York Water IR)

The company has owned the area around and in Reservoir park for over 140 years, and its purchases are made with exactly that sort of thinking.

York Water is the sort of investment that doesn’t “do anything” in terms of major risks. It’s water, and it’s not going anywhere. At the right price, it can give double digits, and at lower prices, it goes down to single digits.

Let’s look at where we are going into 2023.

York Water’s 2023 valuation isn’t good enough for investing

Since late 2015, this company has seen some significant premiumization of its valuation. While it’s not as bad now as it was after COVID-19 when YORW traded at above 40x P/E – a multiple I will never pay, nonetheless, it’s still above where I’d be comfortable investing in the business.

I have stated with clarity in previous articles that the time when the company becomes expensive is when it goes above a $44/share PT. For the coming years, given increased earnings, I might bump this to $45, which would turn this current price of $44.77 barely undervalued/close to fair value for the company, but given that we don’t have exact clarity for this yet, I’m sticking to below $44/share for the time being.

Again though, even when YORW goes below $44, it doesn’t even yield 2% it has an inverse P/E EPS yield of less than 3.5%, and it currently trades at 32x P/E blended. Yes, it may be A- rated, but it’s also less than a $1B in market cap – less than $700M as a matter of fact. The normalized P/E ratio that we see estimated here is 37.52x, but this is based on a positive set of historicals that I don’t view as being rational, given the relatively modest pace of growth at around 6%.

If we forecast at 32-37x P/E, that gives us no less than a 9-13% annualized Upside, but there’s too much exuberance to those targets for me. I want that sort of upside on 30-32x, which we don’t have.

There is still only one analyst following YORW at S&P Global – and he is as insistent 10-30% above the company’s share price as he has always been. The target for that analyst has now gone up to $59/share, which would imply a 31.8% upside at today’s price.

I do not agree with this price target.

In terms of every relevant peer, some of which are more than 15x the size of YORW, the company trades at an excessive premium in terms of revenues, sales, and earnings. Even American States Water (AWR) doesn’t trade as high as that, nor does California Water (CWT). There are international peers as well, and they don’t come close to this.

Because of this, I view this as an asymmetric play – in the wrong sense of the usually positive word. I, unfortunately, believe that at this price, you’re likely to see YORW underperform, as the company has since my last article covering it. YORW also isn’t a good option play, not here and not as I see it.

That leaves me with the following thesis for 2023 for YORW here.

Thesis

My thesis for York Water Company is the following:

- This is the oldest consistently dividend-paying company in existence. It’s trading at a significant premium but may well deserve some of this premium.

- My target for YORW is a 30-33X P/E, accepting the 10-year P/E average, giving us a PT of $44/share – and that’s the highest I’m willing to go here, no matter what.

- YORW has gone too far and it’s not going down – I’m “HOLD” in here, and I consider it better to wait to drop before buying more. Check out European and other US peers to see if they’re more to your liking.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic, good upside based on earnings growth or multiple expansion/reversion.

As you can see, the company still fulfills only 3 out of 5 criteria here – making it a “HOLD” to me.

Be the first to comment