Spencer Platt

Investment Thesis: Yelp Inc. (NYSE:YELP) could see a strong rebound in growth on the basis of continued revenue growth, as well as strong performance across the Restaurants and Home Services business.

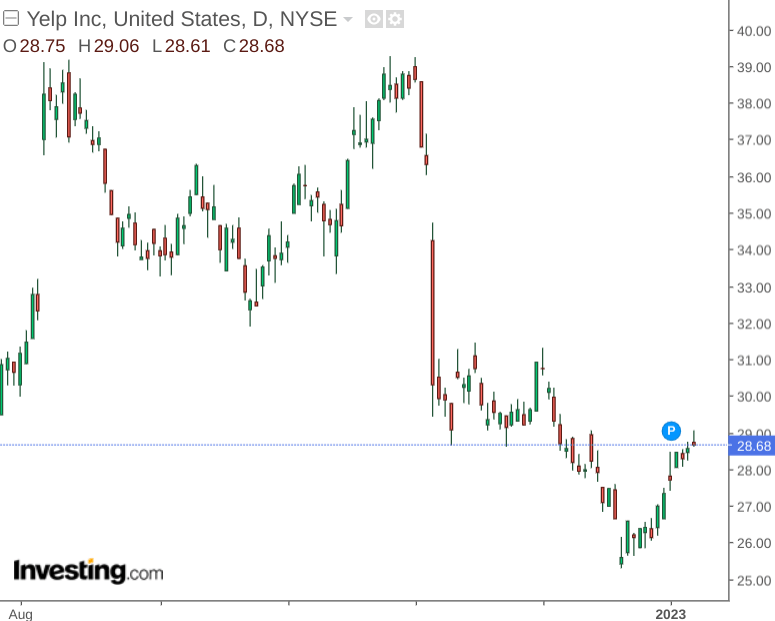

In a previous article back in August, I made the argument for a long-term bullish view on Yelp based on strong growth in net revenue and earnings, as well as an attractive EV/EBITDA ratio and a healthy cash position.

In spite of these assertions, the company has seen significant downside – with the stock down by just over 22% since my last article:

investing.com

The purpose of this article is to assess whether the recent downside has been justified, and whether we could see a rebound in performance going forward.

Performance

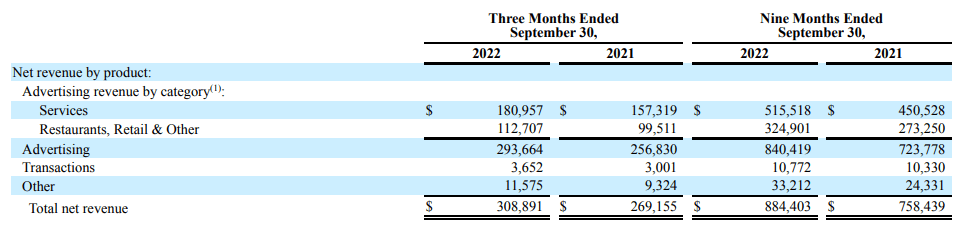

For Q3 2022, we can see that advertising comprised the majority of overall net revenue – with advertising revenue up by over 14% since Q3 2021.

Yelp Q3 2022 Financial Results

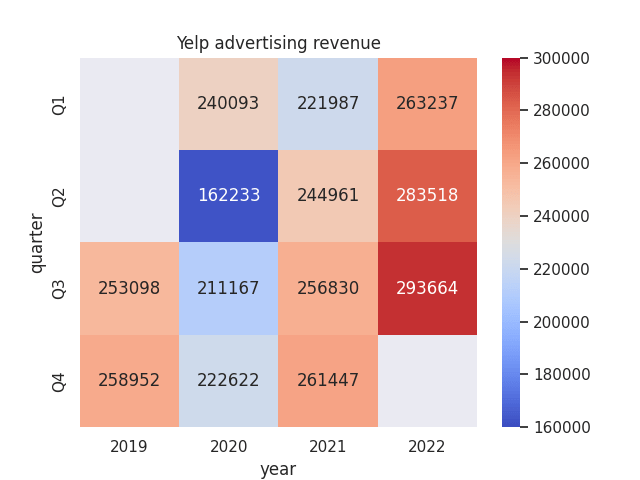

Moreover, when we look at quarterly advertising revenue trends since Q3 2019, we can see that Yelp has more than compensated for the initial drop in revenue during the COVID-19 pandemic – with current advertising revenue up significantly from levels seen in 2019.

Figures sourced from Yelp historical quarterly reports. Heatmap generated by author using Python’s seaborn.

However, this has clearly not been enough to appease investors.

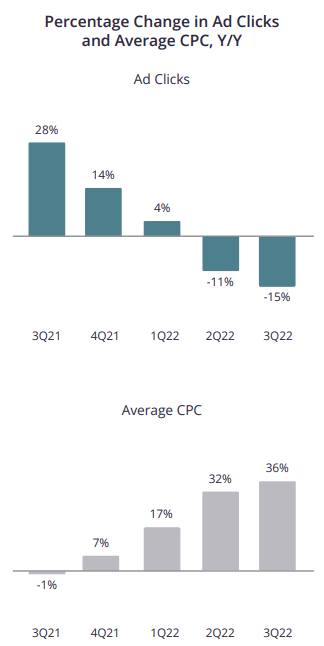

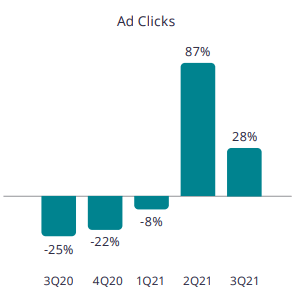

Specifically, investors have been concerned about the decline in ad clicks for Q2 and Q3 2022:

Yelp Q3 2022 Letter to Shareholders

However, the company notes that the percentage of ad clicks converted to leads remained higher than that of Q3 2021. Additionally, with cost per click up by 36%, Yelp has seen strong advertiser demand for performance-based ad products. While the decline in ad clicks remains a concern – some moderation in growth can be expected after the strong boost in 2021 following the “reopening” stage of the COVID pandemic:

Yelp Q3 2021 Letter to Shareholders

In this regard, despite concerns over inflation lowering demand for advertising revenue – I take the view that the long-term trajectory for growth will continue to be to the upside.

The Services business – which accounted for over 60% of advertising revenue in Q3 – has seen growth of over 15% – which was predominantly led by the Home Services business – up by 25%.

Meanwhile, the 13% growth in Restaurants, Retail and Other was driven by a 10% year-on-year increase in Paying advertising locations.

From this standpoint, I take the view that the market may have been short-sighted in focusing on Yelp’s decline in ad clicks in isolation. Longer-term growth has been to the upside – and Yelp has seen growth in the percentage of ad clicks converted to leads.

Looking Forward

Going forward, I take the view that Yelp is in a good position to bolster advertising revenue further.

With Yelp having significant exposure to the restaurant industry, growth in restaurant sales has been vibrant in spite of inflation – with demand post-COVID continuing to remain high and U.S. sales at bars and restaurants up by 1.6% in October followed by 0.9% in November.

Additionally, Home Services – which constitutes of services such as interior decorating, plumbing and electrical services, and so on – has led growth for the Services segment overall.

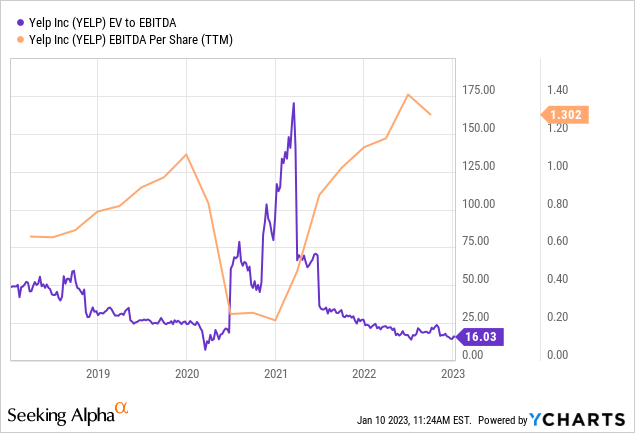

When looking at earnings, we can see that EBITDA per share is near a five-year high – while the EV to EBITDA ratio is trailing near a five-year low.

ycharts.com

In spite of the current apprehension over the short-term decline in ad clicks – one potential risk is the effect that inflationary pressures may have on the current demand we are seeing for Home Services.

Specifically, with higher interest rates and recessionary fears having the potential to cause a slowdown in housing demand – there is a possibility that a decline in new house purchases could also lead to a decline in demand for Home Services – which might impact growth across the Services segment overall.

However, there have been no indications of this thus far – with the segment continuing to perform strongly.

Conclusion

To conclude, Yelp Inc. has seen a decline in the past few months, which appears to have been at least partially driven by apprehension over a decline in ad clicks.

In spite of this, long-term growth for this metric remains encouraging and Yelp has seen substantial growth in revenue despite this.

I take the view that the recent decline in Yelp’s stock is an overreaction by the market and expect that a rebound in upside is quite possible.

Be the first to comment