sornwut tubtawee/iStock via Getty Images

XPEL Inc (NASDAQ:XPEL) is enjoying rocketing growth in revenue and profitability over the last few years, and shareholders have seen a +5,400% return in 5 years to show for it.

However, to maintain the exponential growth, the firm has been increasing its leverage significantly, changing the profile of the firm’s risk/reward ratio for investors.

In this piece, we’ll look at some of the underlying causes of the rocketing share price, and look a little closer at what’s happening under the hood, so to speak.

Exponential Growth, Exceptional Scale

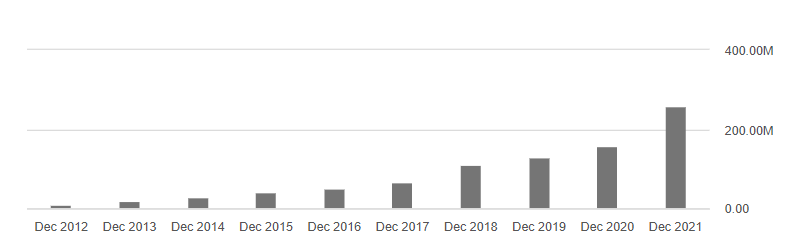

XPEL has enjoyed a CAGR of revenue of 38% since 2012 ($10.7m > $259.3m), which is truly incredible for any business, and management must be congratulated on this result.

Seeking Alpha

Even more commendable is how the business has successfully scaled its profits alongside its revenue, and that growth has not been painful for the firm.

Both Gross Profit and Operating Income margins have grown over the last 10 years (34.06% > 35.75% for GP and 10% > 15.47% for OI).

Pair this revenue with XPEL’s accounts receivables, and we see receivables are ~8% of revenues, indicating excellent turnover of accounts, and inventory turnover is close to a 3X multiple.

In the past 10 years, the firm has only issued an additional 1.8m additional shares (6.9% of 2012’s shares out), indicating the firm is taking excellent care of shareholders not to dilute equity.

Overall it’s very easy to see a strong narrative justifying outsized share price gains and a premium valuation ongoing, with all the elements of growth investors love.

But this is not the whole story, and over the last few years, the firm has been funding its growth with financial leverage, which is beginning to change the risk and reward profile of the firm. Let’s explore.

Debt Is Not A Dirty Word

In the last 2 years, the firm has been taking on debt in order to fund growth, with total debt now $41.4m in the MRQ, representing 36% of equity. While this is a very moderate level of debt for any US firm (the median for the All US Stocks screener is 39%), the firm is spending big on Property, Plant & Equipment (up $21m, 237% in 2 years) as it invests in manufacturing capacity.

This should lead to large returns in the coming years as the firm capitalizes on this investment, but until now the firm has outsourced all manufacturing. So while the diversity of revenues is welcome, XPEL is changing its business model which changes how we should view the firm going from an asset-light organization to a capital-thirsty manufacturing entity.

Underlying Profitability Takes A Hit

Where I do see some worrying signs is while the income statement looks great, underlying profitability (calculated from the cash flow statement, Cash from Operations + Cash from Investing = Underlying Profit), we see investment spending has put a dent in cashflows when we exclude financing activities.

Author & Seeking Alpha

This is of course expected while the firm invests in physical capital, but it’s worth having an eye on.

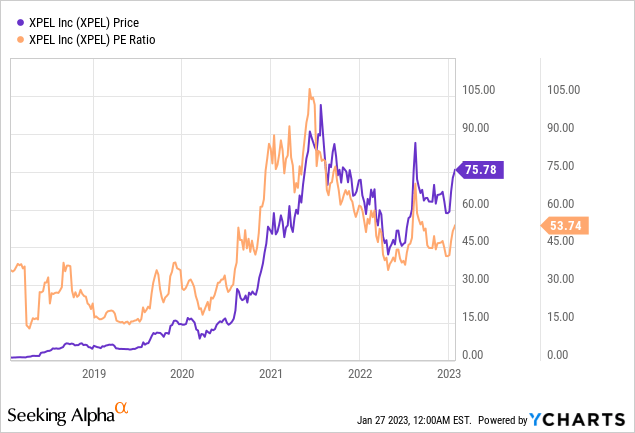

Does A 53 P/E Still Suit XPEL?

A P/E ratio this high puts XPEL in the 88th percentile of all US stocks, indicating investors expect continued growth.

Expectations have been tempered over the last 5 years, as shown in the below graph, and given growth has continued on an exponential path I don’t see any reason to suggest this is not warranted.

Provided these large debts being taken on can be invested wisely, I see no reason why we’re not seeing a natural progression of scale for XPEL, on an exciting upward trajectory.

Closing Thoughts

The market has punished sky-high valuations lately, especially in the tech space, but XPEL is certainly quite different (given it is profitable, is undergoing exponential growth, and is scaling its profits along with revenue growth).

While the additional capital and debt changes the risk profile of XPEL somewhat, the firm is well within the norms of debt levels, and doing it at the right time in its growth story.

Overall I give XPEL a Buy recommendation, though I also recommend keeping an eye on underlying profit and monitoring return on capital given the recent large investments.

Be the first to comment