jittawit.21

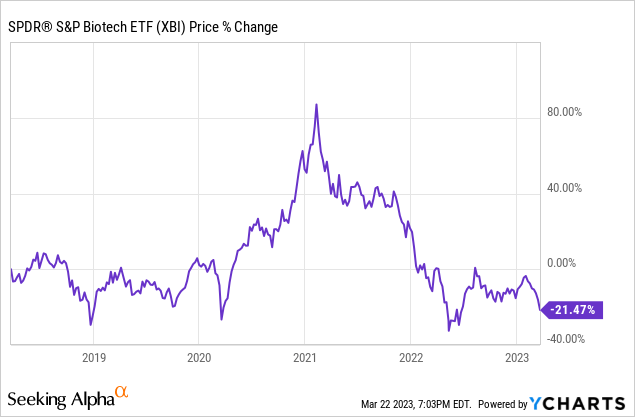

The bull market past the great financial crisis has helped many sectors including the biotech sector. However, after showing stellar returns during the first half of the previous decade (>350%), the ETF in this sector, the SPDR S&P Biotech ETF (NYSEARCA:XBI), has remained flat for the last eight years. Part of the reason for this performance could be the sector was already overvalued from its historic run.

Could this decade start shining a light on this sector again? Biotech is a big part of the healthcare sector and healthcare can be considered a defensive sector. With the current uncertainties in the market, this could be one potential area that could be relatively more resilient. Additionally, this would also benefit if the market turns around. Biotech’s expansion is propelled by fundamental, technological, and demographic shifts, rather than fluctuations in the business cycle. However, the biggest challenge for most investors would be industry-specific knowledge. While most industries are easier to learn and understand, biotech requires a whole body of knowledge just to come up to speed with the basics. But this is just the tip of the iceberg. Most individual names are working on advanced concepts to solve problems that are not within the grasp of many investors.

Owning the ETF

Interested investors need not conduct individual research on the performance of stocks or delve into esoteric studies on complex diseases. This is because diversified biotech funds hold a multitude of stocks, preventing any one firm from having an excessively disproportionate influence on a portfolio (The ETF has holdings in 150 stocks which provides significant exposure to the entire industry) Simply said, each stock can offer unique risks on its own but when owning the ETF as a whole, the risk gets distributed. Broad trends can move the ETF, while individual damages are limited.

Sidestepping the risks of individual names

To understand the risks associated with the individual names in this sector, we will have to go back to the basics. Investing in single names might be unsuitable for risk-averse investors. Smaller companies in the biotech industry carry even more risks as they may not have sufficient funds to withstand any business setbacks.

Clinical Trial Failures

Biotech companies often spend millions of dollars on clinical trials to test the safety and efficacy of their products. While bigger companies have multiple pipelines running in parallel, it is make or break situation for a smaller company. In many situations, the concept of a whole company is built on a single promised drug development; if a product fails in clinical trials, it often tanks the stock’s price.

Regulatory Risk

Biotech companies are subject to a complex regulatory environment, and the approval process for new drugs or medical devices can be time-consuming and expensive. If a product does not meet regulatory standards, it may be rejected by regulatory agencies, leading to delays in its release or even its cancellation. A good example would be one of the components of XBI, FibroGen (FGEN).

In July 2021, the FDA Cardiovascular and Renal Drugs Advisory Committee voted not to approve FibroGen’s roxadustat, which was designed to treat anemia in adult patients with chronic kidney disease. As a result, FibroGen’s stock price plummeted by 42% the following day and has not fully recovered even now. This sudden drop in stock price could have resulted in investors not being able to sell their shares at the desired price due to the volatility of the market.

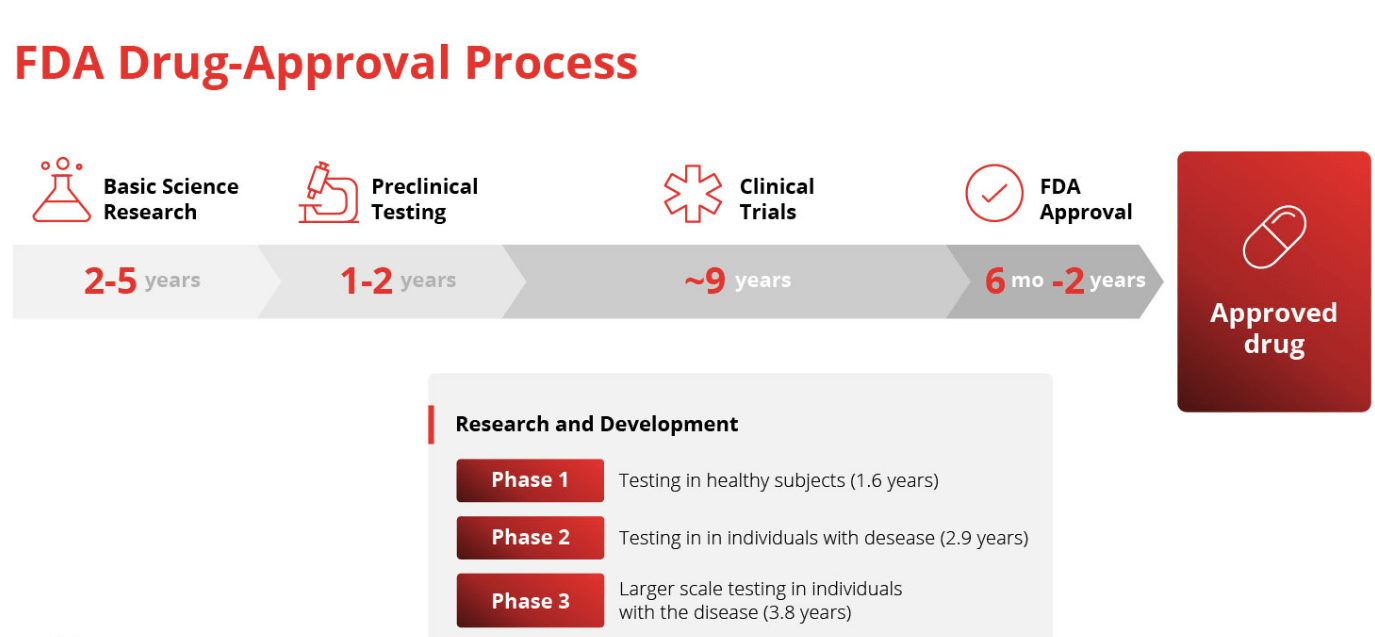

For a more general idea, it would be helpful to see some overall stats. Out of 5,000 compounds discovered in pre-clinical trials, only one progresses beyond the first few phases of the process and is granted FDA approval. The lengthy pipeline also becomes a significant risk with the average time frame to release a new FDA-approved drug to the public being 14 years. Any further challenges to this timeline become a big stretch for players with smaller budgets.

Foundershield website

Foundershield

Intellectual Property Risk

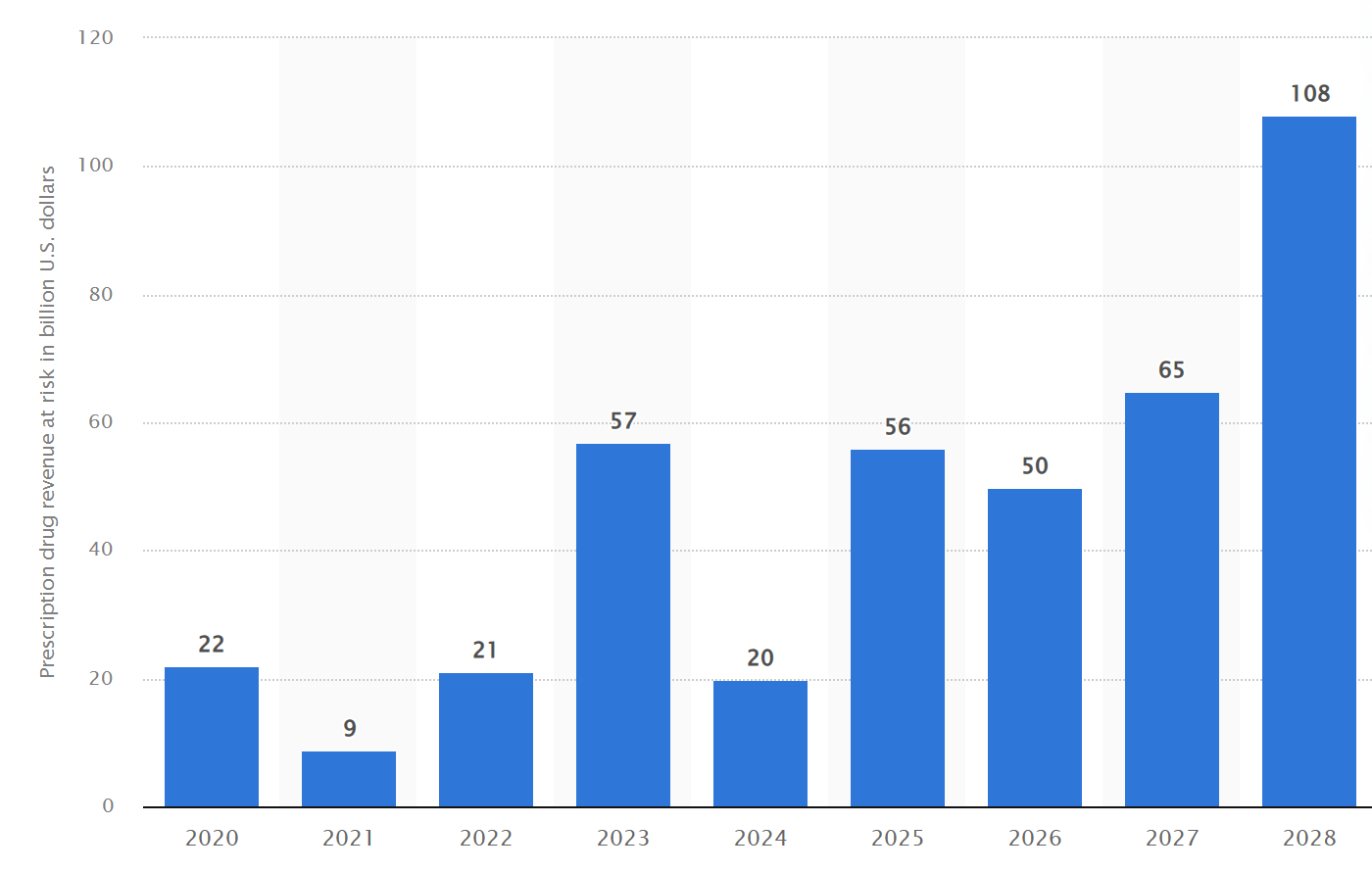

Many biotech companies rely on patents to protect their products and prevent competitors from copying their technology. However, there is always the risk of a patent challenge, which could invalidate a company’s intellectual property and open the door to competition. There is also a patent cliff which refers to the revenue drop faced by companies with expiring patents. This is more of a problem with established bigger players and in order to grow, often times a company is left with no choice but to acquire untested or early-stage pipeline companies.

Worldwide total prescription drug revenue at risk from patent expiration from 2020 to 2028 (Statista)

Safety risks

Since a lot of Biotech companies are involved in cutting-edge research, there is always the risk that a company’s products may not work as intended or that new research may reveal unforeseen safety concerns. Years after a product is established it may face lawsuits that can severely affect a company’s bottom line.

How do all these risks make owning the ETF better?

Qualitatively, we have covered the shortcomings of owning individual names versus holding an ETF but let’s take a look at this quantitatively as well.

The ETF has about 150 holdings and each holding’s maximum weighting is around 1%. It regularly rebalances with the aim to spread the cash equally around each position.

| Market Capitalization Category | Number of Companies |

| Largecap | 14 |

| Megacap | 1 |

| Microcap | 2 |

| MidCap | 34 |

| SmallCap | 95 |

SPDR website

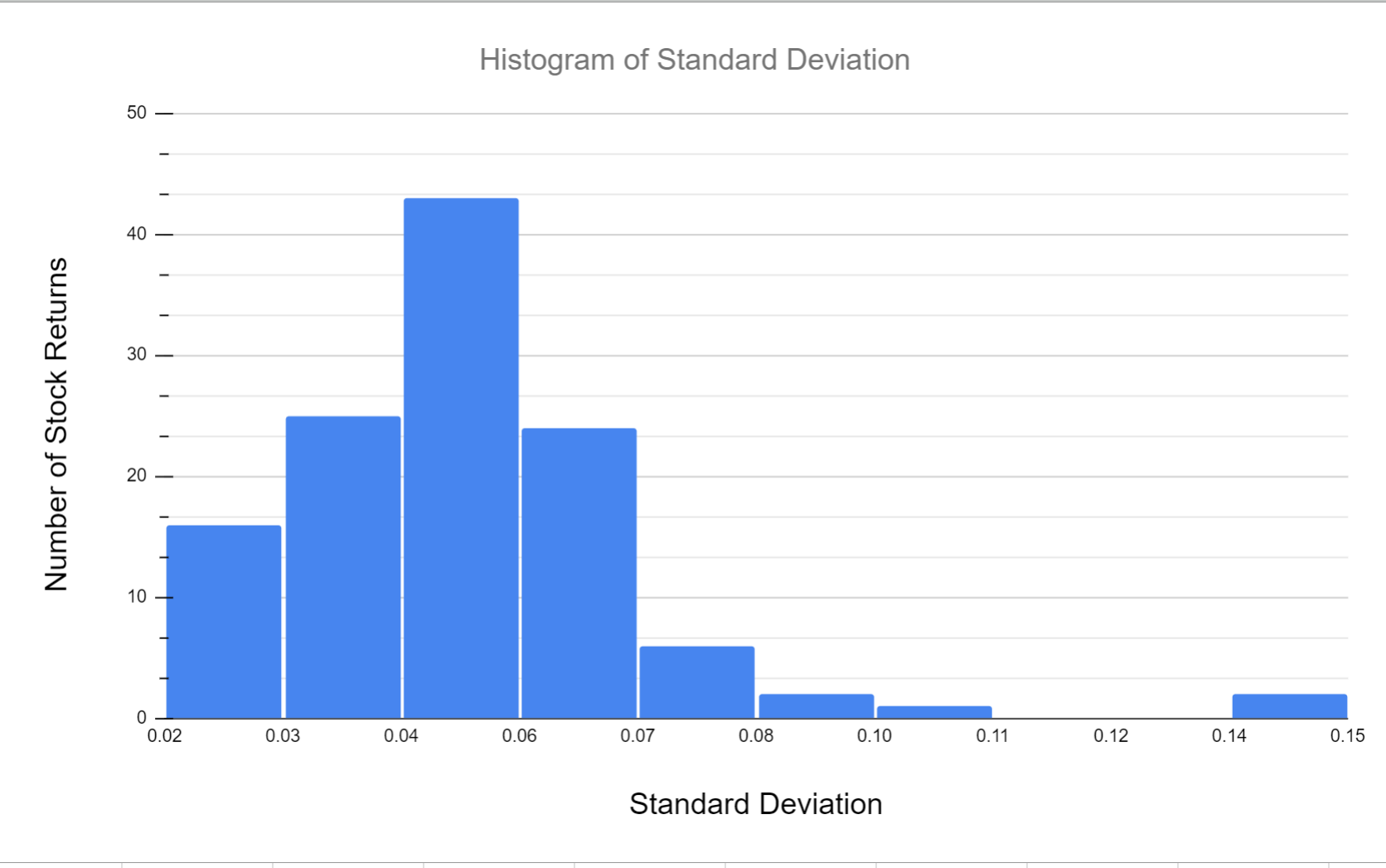

The result is a mixture of companies from different market cap categories. Quantitatively, a quick way to understand the volatility of individual names that would tie up to the risks covered in our previous section would be to measure the standard deviation of daily returns. When I calculated this for a period of three years, I saw results ranging all the way from around 2% to 15%! (The ETF itself is 2.5% and higher the standard deviation higher the volatility).

Histogram of standard deviation of daily returns (Author Computed from Price data) Author Computed from Price data

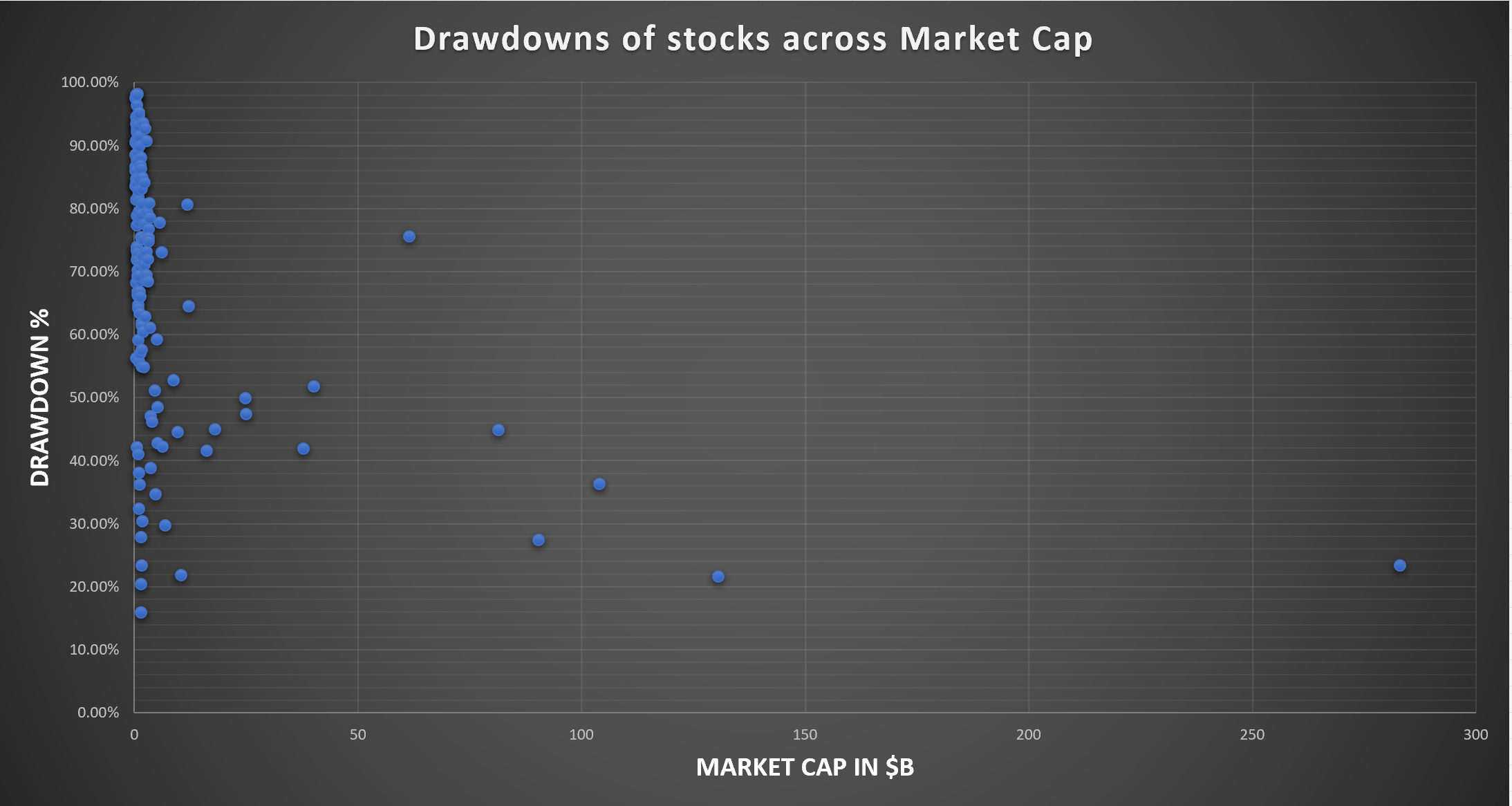

Drawdowns also came in a wide range. Some stocks had experienced drawdowns of as much as 98%! (The ETF itself saw a maximum drawdown of 60% in the same time frame).

All time performance of individual stocks does not look great either. While XBI has returned 1300% since its inception, a lot of the underlying names have been underwater since their IPO.

All of this data demonstrates that holding the ETF significantly de-risks the individual stock exposure to the biotech sector while also providing good CAGR over a long time frame.

Action

I will be adding XBI as a small position to my portfolio and hope to benefit from the exposure to the sector.

Be the first to comment