jittawit.21

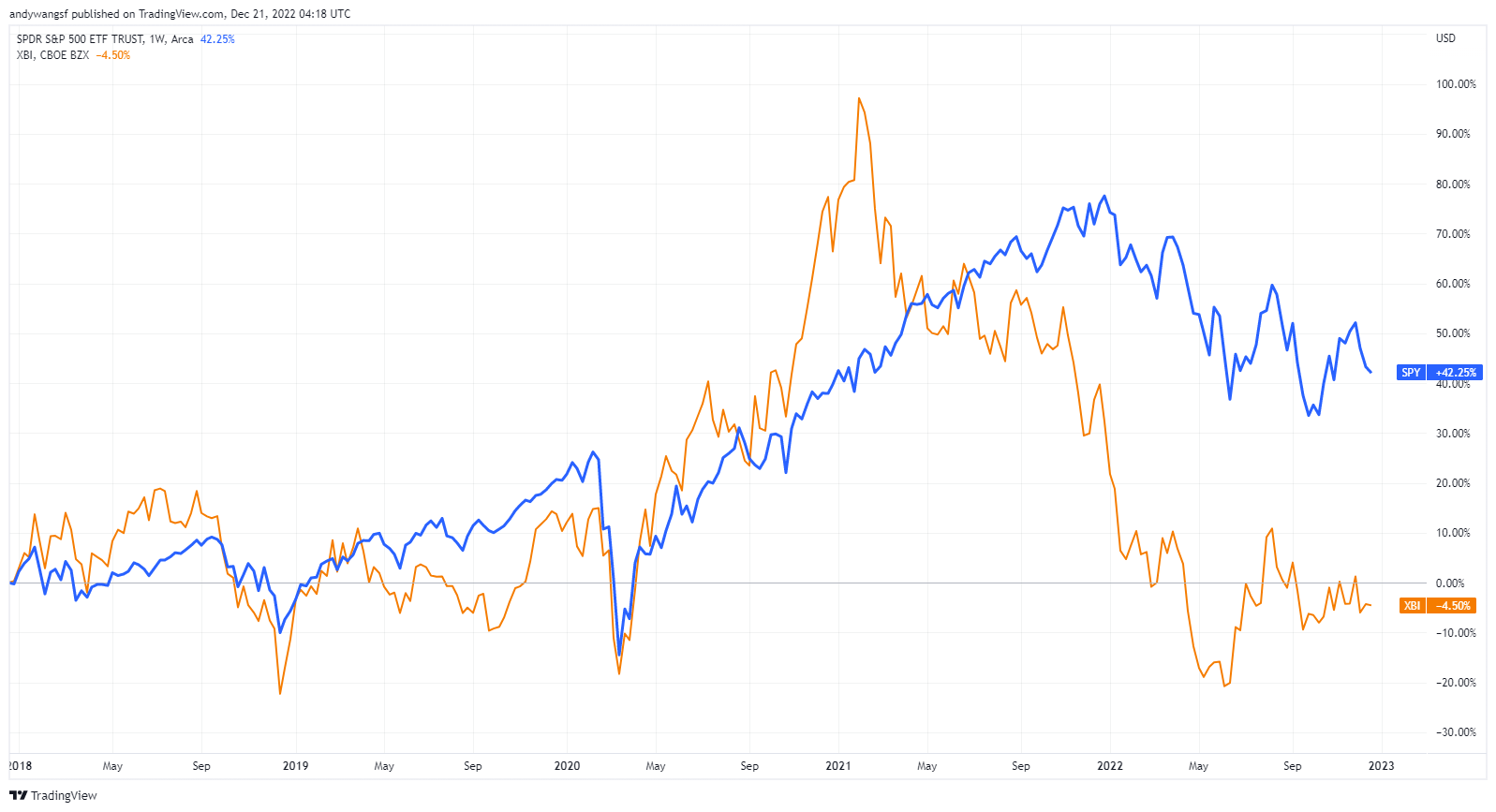

Valuations on biotechnology stocks have moderated substantially since the pandemic peak in 2021. At the time of writing, the SPDR S&P Biotech ETF (NYSEARCA:XBI) has erased more than 5 years’ worth of gains since December 2018. The SPDR S&P 500 Trust ETF (SPY) on the other hand is still sitting on a 42.3% gain over the same period.

TradingView.com

In the initial stages of the bear market, the sharp sell-off in biotech stocks can perhaps be justified by overstretched valuations and higher interest rates translating into deeper discounts on future cash flows of growth stocks. However, the persistent underperformance in biotech stocks in recent months appears to be increasingly driven by sheer pessimism and lack of investor interest in the sector rather than deteriorating fundamentals.

A quick survey of research publications on the outlook for biotech shows revenues are expected to grow at a compound annual growth rate of (‘CAGR’) of 9.0% (Janus Henderson Investors) to 13.9% (Grand View Research) over the next 4-8 years. Our own conservative assessment of the biotech sector suggests that biotech revenues should be able to sustain a healthy 7% CAGR over the next 5 years. Based on these estimates and with the XBI currently trading at just 13.6x forward P/E, we think XBI presents attractive growth at a reasonable price.

Below we quote some of the most compelling reasons offered by Janus Henderson Investors for investing in biotech stocks back in March 2022.

…there’s reason to believe many areas of the sector have become oversold. As of early 2022, a remarkable 16% of U.S.-listed biotechs traded below the level of cash on their balance sheets, more than during the 2002 and 2008 equity bear markets (8% and 11%, respectively). And by the end of February, valuations for large-cap biotechs sat well under their long-term average, as well as the average for the broader equity market.

Not only have valuations on biotech stocks become more attractive, but fundamentals also show no signs of deteriorating.

Even as biotech stocks have sold off, the sector’s innovation has continued to advance. Last year, more than half of drugs approved by the FDA were considered first-in-class, meaning the medicines had mechanisms of action different from those of existing therapies. Nearly three-quarters (74%) used one or more expedited development and review methods, available for drugs that have the potential to significantly advance the standard of medical care.

For investors who are willing to tolerate higher volatility and are aiming to compound returns over a longer investment horizon, XBI may be an excellent addition to a well-diversified portfolio.

To be sure, we acknowledge the risk of XBI underperforming in the near term due to cutbacks in biotech investments and subdued M&A activity. We also anticipate that some readers may feel that we are too early at timing the turnaround in biotech stocks, especially given that more interest rate hikes are just around the corner. However, we think that the opportunity cost of failing to catch biotech stocks at current valuations far outweighs the risk of suffering short-term price volatility. Furthermore, given the overwhelming pessimism surrounding biotech stocks over the past 18 months, we believe that most of the bad news has already been priced into current valuations.

The long-term growth story for biotech remains intact and advances in artificial intelligence have only recently begun to open up new possibilities for improving efficiencies in the discovery of new drugs and innovative treatments.

Investing Broadly To Manage Idiosyncratic Risks

Due to the high idiosyncratic risks associated with the performance of biotech companies, studies show that active managers have produced mixed results in trying to stock-pick within the biotech space. There may be many reasons why picking winners is extremely challenging, but we think it essentially boils down to the binary nature of biotech research. The research and development of any potentially revolutionary drug conclude either with the drug being proven to be highly effective in clinical trials and successfully passing the FDA’s strict requirements, or the drug failing completely and having near zero financial value.

The lifecycle of developing the next blockbuster drug could also stretch for several years, during which the financial performance of a biotech company will not adequately reflect the potential risk and reward for investing in the company. Thus, active managers are left with few clues as to which biotech companies are more likely to emerge as winners.

SPDR S&P Biotech ETF

Perhaps humility in investing means understanding that active investing is not a “one-size fits all” solution and that there is no shame in settling for a more passive approach so long it gets the job done. As such, we prefer investing broadly across large, mid and small-cap biotech names, and the XBI is ideal for our purposes.

According to fund information provided by the issuer State Street Global Advisors, XBI seeks to provide investment results that correspond generally to the total return performance of the S&P Biotechnology Select Industry Index. The index is a modified equal-weighted index which provides the potential for unconcentrated industry exposure across large, mid and small-cap biotech stocks.

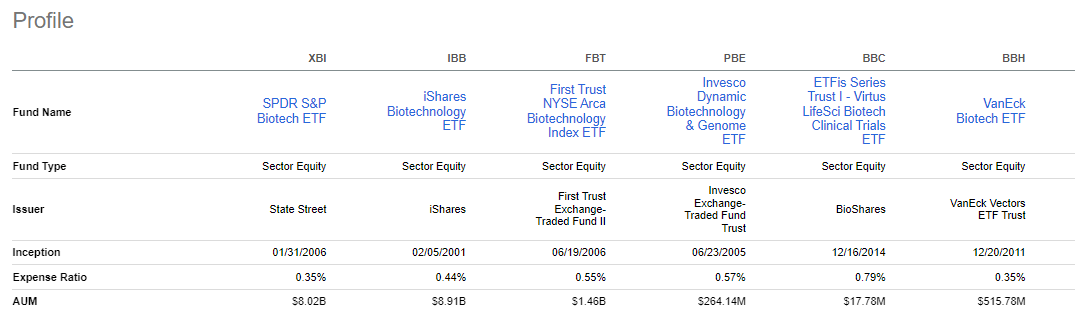

Comparing XBI with other biotech ETFs, we note that XBI is one of the largest with around US$8 billion in assets under management and has one of the lowest expense ratios at 0.35%.

Seeking Alpha

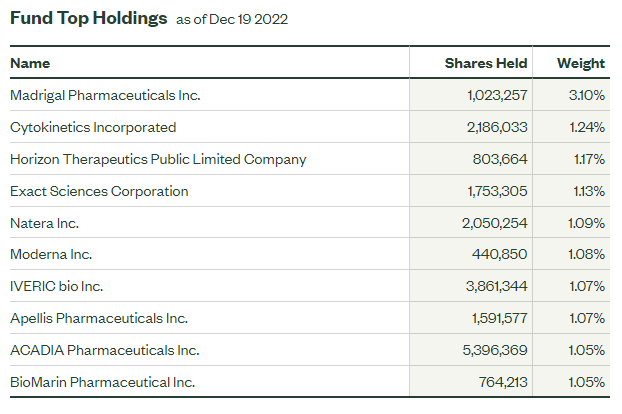

We also particularly like how well-diversified XBI is relative to its peers with a total of 155 holdings in its portfolio. The portfolio is equal-weighted and rebalanced quarterly, with each holding usually being less than 1.5% of the portfolio.

In the table below, Madrigal Pharmaceuticals (MDGL) has an abnormally large weighting of 3.1% in XBI’s portfolio due to a sharp 232% spike in the company’s share price on 19 Dec. Such volatility is the nature of biotech stocks and this provides a timely example of why diversification and regular rebalancing of portfolios may be a great idea.

State Street Global Advisors

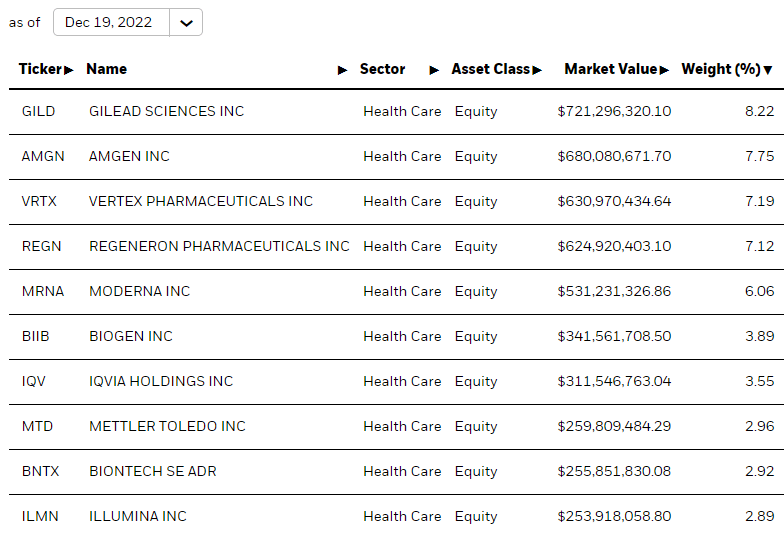

In contrast, although the iShares Biotechnology ETF (IBB) has a much larger number of holdings at 371, the portfolio is actually much more concentrated. Just four stocks make up 30% of IBB’s portfolio: Gilead Sciences (GILD), Amgen (AMGN), Vertex Pharmaceuticals (VRTX), and Regeneron Pharmaceuticals (REGN).

iShares

Based on the comparison above, we consider XBI the ideal choice for executing our idea to invest broadly across large, mid and small-cap biotech names.

However, for investors who prefer to be slightly more selective and wish to overweight on some of the more established biotech names in IBB, then IBB may be a more suitable choice. Investors should also note that the expense ratio for IBB is slightly higher at 0.44% and that could add up for long investment horizons. Alternatively, it is also possible to first establish a base exposure to biotech through XBI and then invest a small sum in the specific names they are looking to overweight.

ETF.com

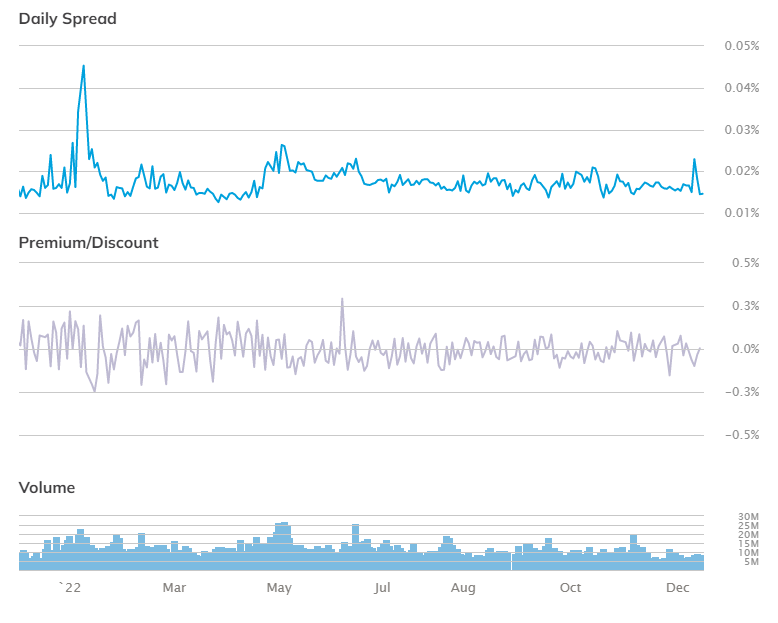

In terms of trading metrics obtained from etf.com, XBI is highly liquid and trades at very low and stable spreads with a high average daily volume of around US$778 million. XBI also trades very close to NAV with daily deviations of less than 0.1%.

In Conclusion

We think the SPDR S&P Biotech ETF presents attractive growth at a reasonable price, with the expectation that biotech revenues should be able to sustain a healthy 7% CAGR over the next 5 years.

Due to the high idiosyncratic risks associated with the performance of biotech companies and therefore the difficult task of stock picking, we prefer investing broadly across large, mid and small-cap biotech names. The XBI is thus ideal for our purposes given its well-diversified portfolio and wide coverage of biotech stocks.

We initiate our coverage of XBI with a “Buy” rating.

Be the first to comment