alberto clemares expósito

Thesis

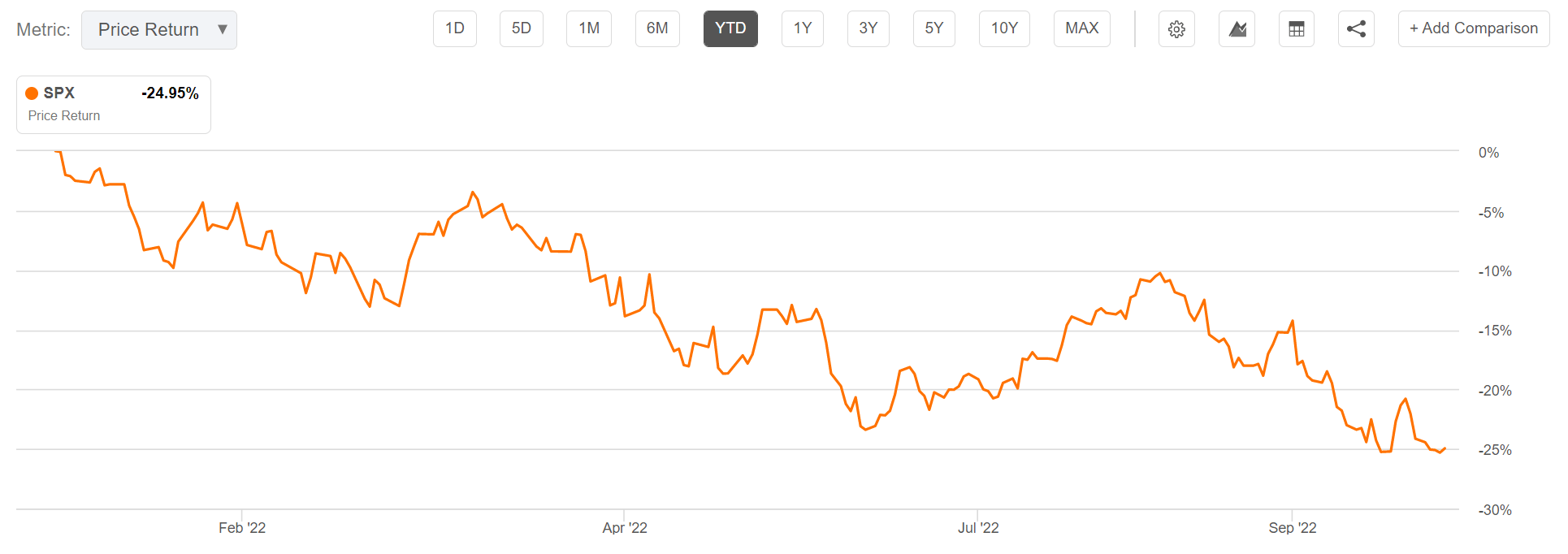

The September CPI print came in at 6.6% year over year and was thus once again worse than expected. Treasuries and the S&P 500 (SPX) reacted quickly, moving sharply up and down respectively. But what are the odds that traders are merely reacting mechanically, without consideration of the value they are trading?

Reflecting on already excessively bearish market sentiment paired with attractive valuations, I argue the sell-off today will provide an excellent risk/reward opportunity to act contrarian: betting that the improved valuation set-up will spark a short-term bear market rally.

Note, given the risk and speculative nature of the thesis, I recommend investors to trade the thesis through derivatives – and I advise to buy 105/115 percent moneyness Call spreads.

Seeking Alpha

September CPI Report

The September CPI print was bad but, in my opinion, not a catastrophe. Here is a summary of the most important data:

Y/Y, CPI: +8.2% vs. +8.1% expected and +8.3% prior.

Increases in shelter, food, and medical care indexes contributed the most to the rise. Those were partly offset by a 4.9% decline in the gasoline index.

Core CPI: +0.5% M/M vs. +0.4% expected and +0.6% prior.

Y/Y, core CPI: +6.6% vs. +6.5% expected and +6.3% prior.

So in other words, the CPI print in September was not only worse than what analysts had expected, but was also worse than the respective report in August.

Likely Fed Response: Higher Yields

Following an unfavorable inflation report, the yield on U.S. treasuries immediately shot up. The 10-year treasury yield, for reference jumped from 3.89% to 4.01% in less than 5 minutes (a more than 10 basis point increase), as traders priced a hawkish response from the Federal Reserve.

Higher yields are of course negative for equity markets. There are two major arguments: First, the higher the interest rates on “riskless” fixed income securities, the less attractive are equities in relation to such securities. Second, the higher the interest rates, the lower the value of long-duration cash flows due to higher discount rates (think about a discounted cash flow valuation).

The S&P 500 reacted as quickly as U.S. treasuries: trading lower by about 2% points 5 minutes following the report.

But haven’t we already known that the Fed will move aggressively? Already two months ago, Fed Chair Jay Powell highlighted that (emphasis added):

We are taking forceful and rapid steps to moderate demand so that it comes into better alignment with supply, and to keep inflation expectations anchored

Thus, although I acknowledge that the CPI report for September is unfavorable, and will confirm the Fed’s aggressive stance against inflation, it doesn’t really provide investors with any new information. The improved valuation set-up, however, is new.

Sentiment In Panic Territory

Independent of the CPI report, I would like to point out that investor sentiment has been extremely bearish already.

The highly followed investor survey from Bank of America (BAC) in September highlighted that 52% of respondents are underweight stocks, a reading that is “unquestionably” the worst since the financial crisis in 2008/2009, according to BofA strategist Michael Harnett.

Similarly, Citigroup’s Levkovich Index (formerly Panic and Greed Index) is clearly in panic territory – which has historically suggested a greater than 90% probability that the stock market will deliver a positive 12-month forward return. The Levkovich index is one of my personal favorite analysis tools and a highly reliable contra-indicator. The index reflects data including (Source: Citi Pulse Monitor).

NYSE short interest as a percentage of float, margin debt, TRF volume % of US tape, Market Vane and AAII bullishness, National Financial Conditions Nonfinancial Leverage, put/call ratio, CRB futures, gasoline prices, and 25 delta put/call skew.

Given such bearish sentiment, it should be no surprise that as of early October, an estimated $5 trillion of cash and money-market holdings is waiting on the sidelines – waiting to rush into the market and buy the dip on improving sentiment.

Attractive Valuations

Sentiment and expectations towards the Fed will likely remain the major drivers of equity markets. But from a technical perspective, valuations are starting to get very attractive for stock-pickers.

A research note from Bloomberg (Source: Bloomberg Intelligence Primer, S&P 500 as of September 2022) highlighted two very interesting considerations. First, the percentage of S&P 500 constituents that have recently made a new four-week lows stands at above 85%, a reading seen only twice in the past decade – in 2018 and 2020. Secondly, percentage of S&P 500 constituents that trade at deep value multiples – as defined by a TTM P/E below 10 – has reached 21%.

So, at what point is the market attractive enough for dip buyers and value investors to start buying equities? Following an additional 2% of the September CPI print, simply as a function of valuation, I believe we are slowly getting there.

Implications For Investors

Reflecting on the worse-than-expected September CPI print, I like the odds of taking a contrarian view: I believe a short-term bear market rally may be very likely – simply as a function of excessive bearishness and attractive valuation.

(To test if my thesis is correct, watch how the S&P 500 closes today – if the current valuation set-up indeed attracts dip buyers and value investors, then the 2% sell-off at market open should recover by at least 1 percentage point by close. If not, my thesis is probably wrong).

But a word of caution: investors should note that speculating on a rebound during a structural bear market can be dangerous, because the dominant trend for prices is undoubtedly lower. Only recently, Jamie Dimon, Chairman and Chief Executive Officer of JPMorgan Chase (JPM), has said that volatile markets are a “guarantee.” And depending on a soft landing versus hard landing outcome, there could be another “easy 20%” downside to equity valuations.

Trade Recommendation

Given the speculative nature of the thesis, I believe buying call spreads provides the best risk/reward for investors interested to trade the prospects of a bear market rally – given that the loss for call spread is limited to the options premium outlay.

Personally, I advise to buy the 115/105 percent moneyness call spreads with about 3 weeks to expiration. The trade would offer a pay-off of approximately 8:1, if the S&P 500 closes above the long strike on expiration.

Be the first to comment