FG Trade/E+ via Getty Images

Introduction

Shares of Winmark Corporation (NASDAQ:WINA) have risen 17% YTD. Despite the growth of macro and geopolitical tensions, the company continues to demonstrate not high, but stable revenue growth. In addition, the company’s business model and product positioning allow us to maintain historically high levels of operating and gross margins. However, in my view, future cash flows are already included in the company’s current stock valuation, and there is limited room for improvement in operating and financial performance.

Projections

I decided to build a model of the future cash flows of the business in order to understand how much the current stock valuation already includes future cash flows and to understand if there is a fundamental upside for making a decision to buy WINA stock.

Below, I would like to share the main inputs to my model that have the greatest impact on the future cash flows of a business.

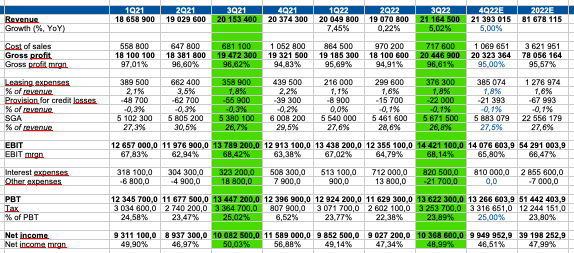

Revenue growth: I’m conservatively forecasting solid revenue growth of 5% in Q4 2022 and 5% revenue growth through 2026. In my personal opinion, uncertain macro and geopolitical conditions are helping to support demand for the company’s business model. In addition, the company continues to recover from several quarters of COVID restrictions in previous years.

Gross margin: I predict a gradual improvement in the gross margin from 95% in Q4 2022 to 97.5% in 2026 due to the company’s ability to raise prices for the end consumer, effectively manage the product mix and selling area. I understand that my gross margin forecasts may look optimistic against the backdrop of macro headwinds, however, even such optimistic assumptions do not allow us to see a fundamental upside in the company’s shares.

Leasing expenses: In my forecasts, I assume a decrease in leasing expenses (% of revenue) from about 1.6% in 2022 to 1.2% by 2026 due to a change in the company’s product mix.

SGA: I predict stable SGA spending (% of revenue) at 27.6% until the end of 2026. You can see the results of my forecasts of future financial results in the charts below.

You can see the results of my forecasts of future financial results in the charts below.

Quarterly projections:

Personal calculations

Yearly projections:

Personal calculations

Valuation

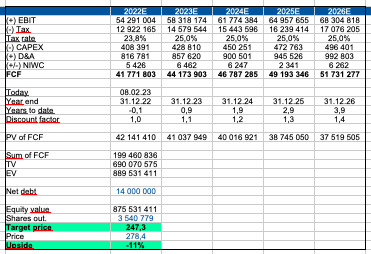

In my personal opinion, the DCF method is the most preferred method for company valuation because:

1. The company operates in a stable market and a predictable market, where the use of the DCF model for valuation is most preferable.

2. An extensive array of historical data and management commentary from which I can make assumptions about future cash flows.

3. The use of DCF allows you to make assumptions about the dynamics of revenue growth and operating profitability of the company in the future.

The main inputs in my model are:

WACC: 8.6%

Terminal growth rate: 3%

Personal calculations

Thus, according to my calculations, the fair value of the stock is $247.

Multiples

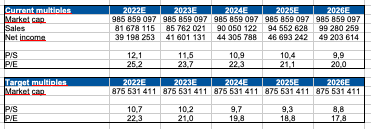

I calculated P/S & P/E multiples based on my Sales & Net income projections. You can see the results of my calculations in the table below. In my personal opinion, the current multiples are too high relative to peers and historical averages.

Personal calculations

Drivers

Margin: An increase in the average check, a favorable change in the product mix and effective management of operating expenses can help support the operating profitability of the business.

Revenue: The opening of new stores, the growth of the average check, the shifting of inflation to the end consumer may support the company’s shares in future periods.

Macro: A recovery in consumer real disposable incomes, lower inflation and a drop in consumer confidence could push up consumer spending on clothing, which could support the company’s bottom line going forward.

Risks

Competition: Increasing competition can lead to lower market share and higher marketing and advertising costs, which can lead to lower revenue and margins.

Margin: Rising inflation and operating costs, coupled with a weakening consumer who is not willing to pay more, can lead to a decrease in the operating profitability of the business.

Macro: Accelerating inflation, declining real disposable income and consumer confidence could lead to a drop in consumer spending, which is a negative factor for the company’s revenue.

Conclusion

Despite the fact that I like the sector and the company’s business model, in my personal opinion, now is not the best time to go long. First, in my view, the company currently has limited potential to improve operational and financial results. Second, I believe that future stable cash flows are already fairly factored into the share price. In addition, I consider the current level of business valuation according to multiples high. Thus, according to my estimate, the fair price of the share is $247 with a downside potential of 11%. At the moment, I start my coverage of the company with a “HOLD” recommendation.

Be the first to comment