andresr

Introduction

I read a lot of investors who, in the current market environment, are investing in mature companies. As an investor, we are all seeking for that alpha, the outperformer, right?

So, what are the reasons for investing in a mature company whose growth and margins may currently come under as much pressure as those of a growth company in the same sector? Let me answer that question: it’s the safety and comfort of having something familiar, so we can invest, sit back and relax while our money works for us.

Unfortunately, this is not the way the stock market works as the current market environment proves. ‘If you are looking for comfort, the stock market is the wrong place to be’, Ken Fisher once said.

If safety and comfort is the goal, then an investor is probably better off investing in fixed income bonds or an S&P ETF, as Warren Buffett often suggests.

The task of the investor in such a market environment, however, is to filter the stocks that can deliver outperformance in the future and manage to grow further, especially in the current market environment.

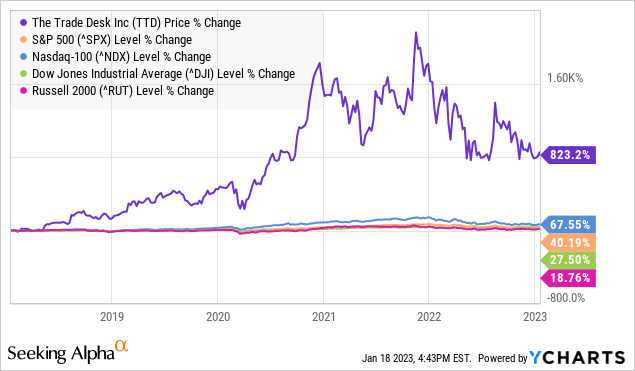

The ad-tech company The Trade Desk (NASDAQ:TTD), which delivered investors a staggering 823% return over a period of five years, could be one of the potential outperformers as soon as the tide turns (see chart).

TTD vs major indices over 5 years (YCharts)

So, while past performance is no guarantee of future performance, what else could currently favor TTD’s future outperformance?

Business model

TTD is an ad-tech company and acts as a demand-side platform (DSP). It offers advertisers a cloud-based, data-driven, self-service platform to create, manage, and optimize digital advertising campaigns across all ad formats and devices on a global scale.

With the help of TTD, advertisers like Coca-Cola can buy an ad for a spot on Hulu or ESPN. TTD generates revenue by charging the ad buyers with a percentage of gross spend on their platform.

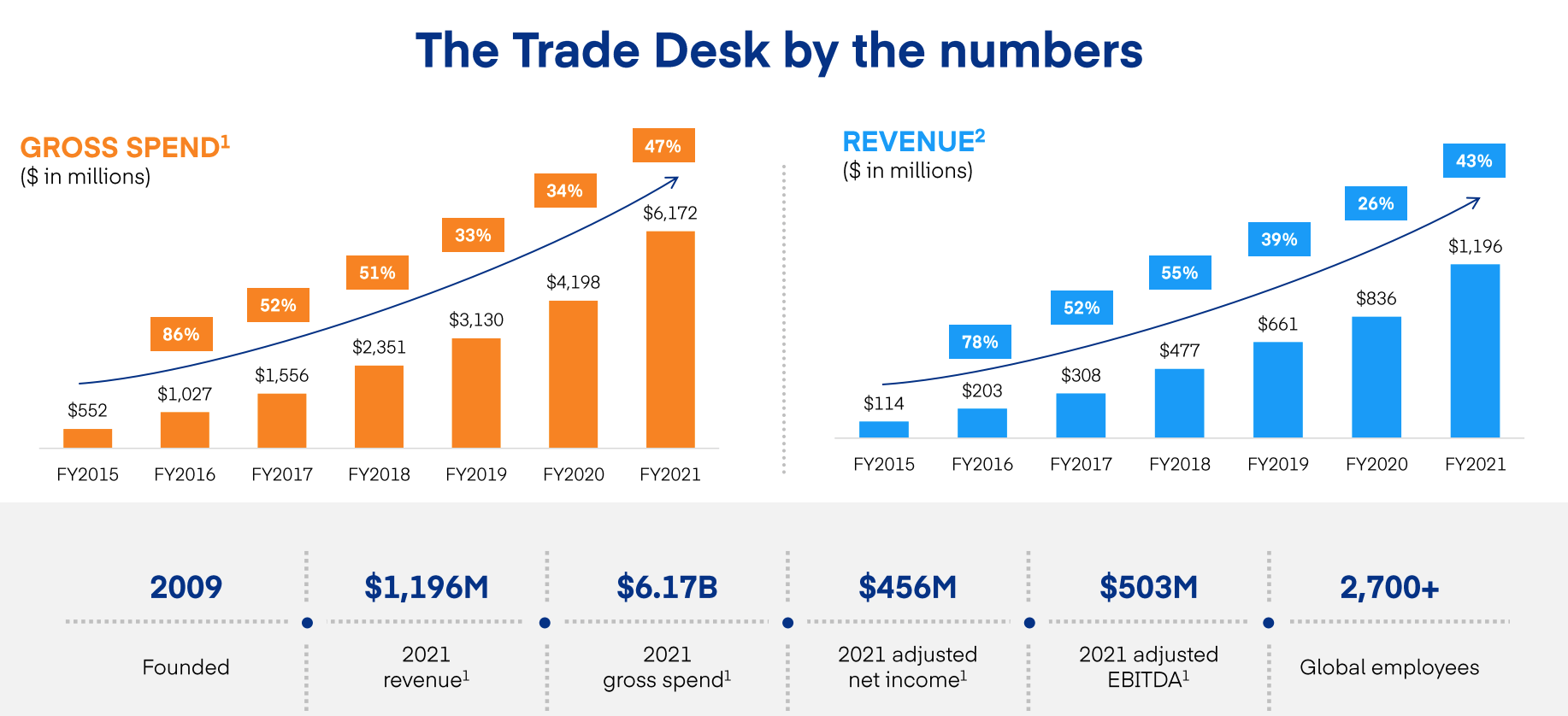

The following figure presents TTD’s growth over the last years.

TTD’s growth over the years (The Trade Desk)

Growth catalysts and competitive advantages

TTD has several growth catalysts and competitive advantages going forward.

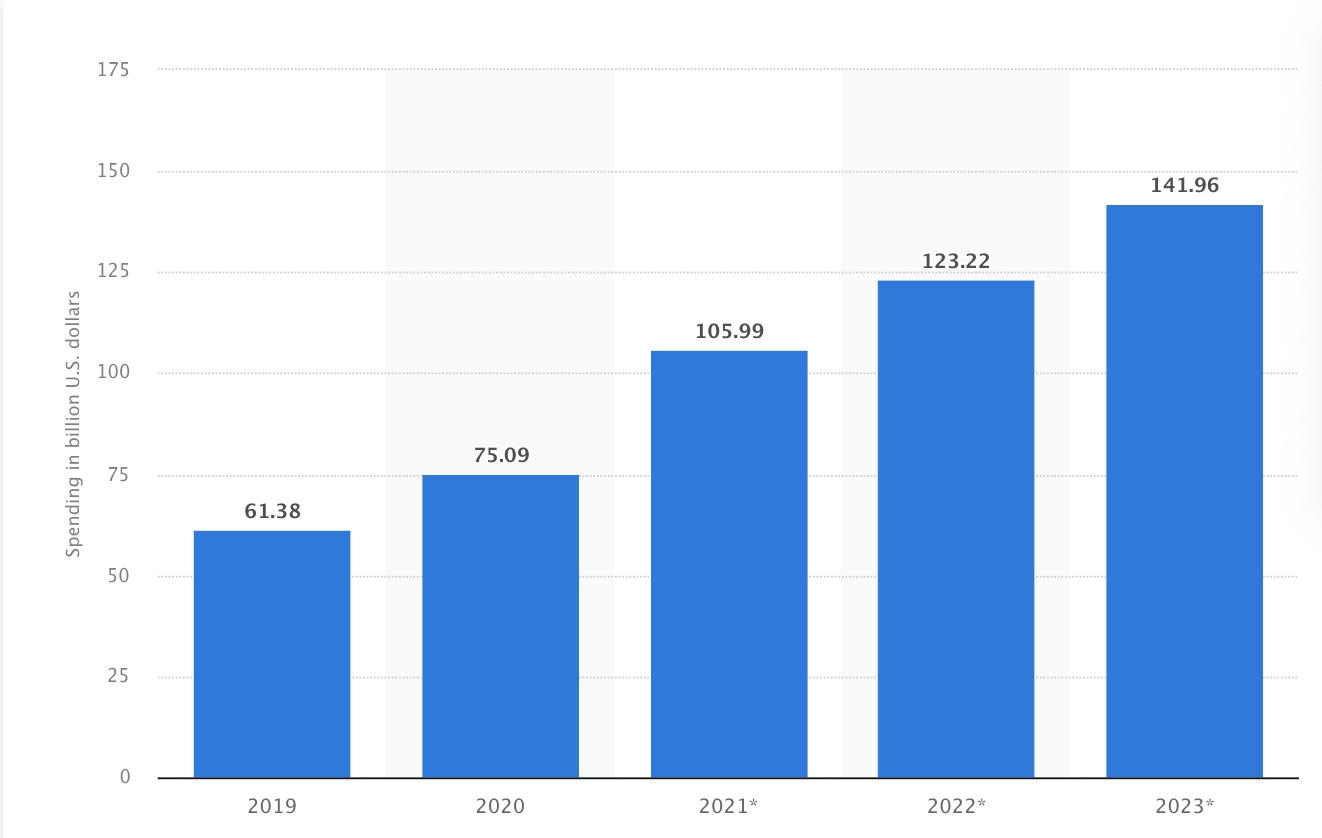

First, TTD estimates its current total addressable market at $816 billion, representing total global advertising spend, whereas programmatic ad buying is a fast-growing business with double-digit growth rates (see figure). In the US alone, the programmatic ad spending is estimated at $123 billion in 2022. This gives TTD tremendous supply-demand tailwinds in the fast-growing programmatic ad buying market.

Programmatic digital display advertising spending in the United States from 2019 to 2023 (in billion U.S. dollars) (Statista)

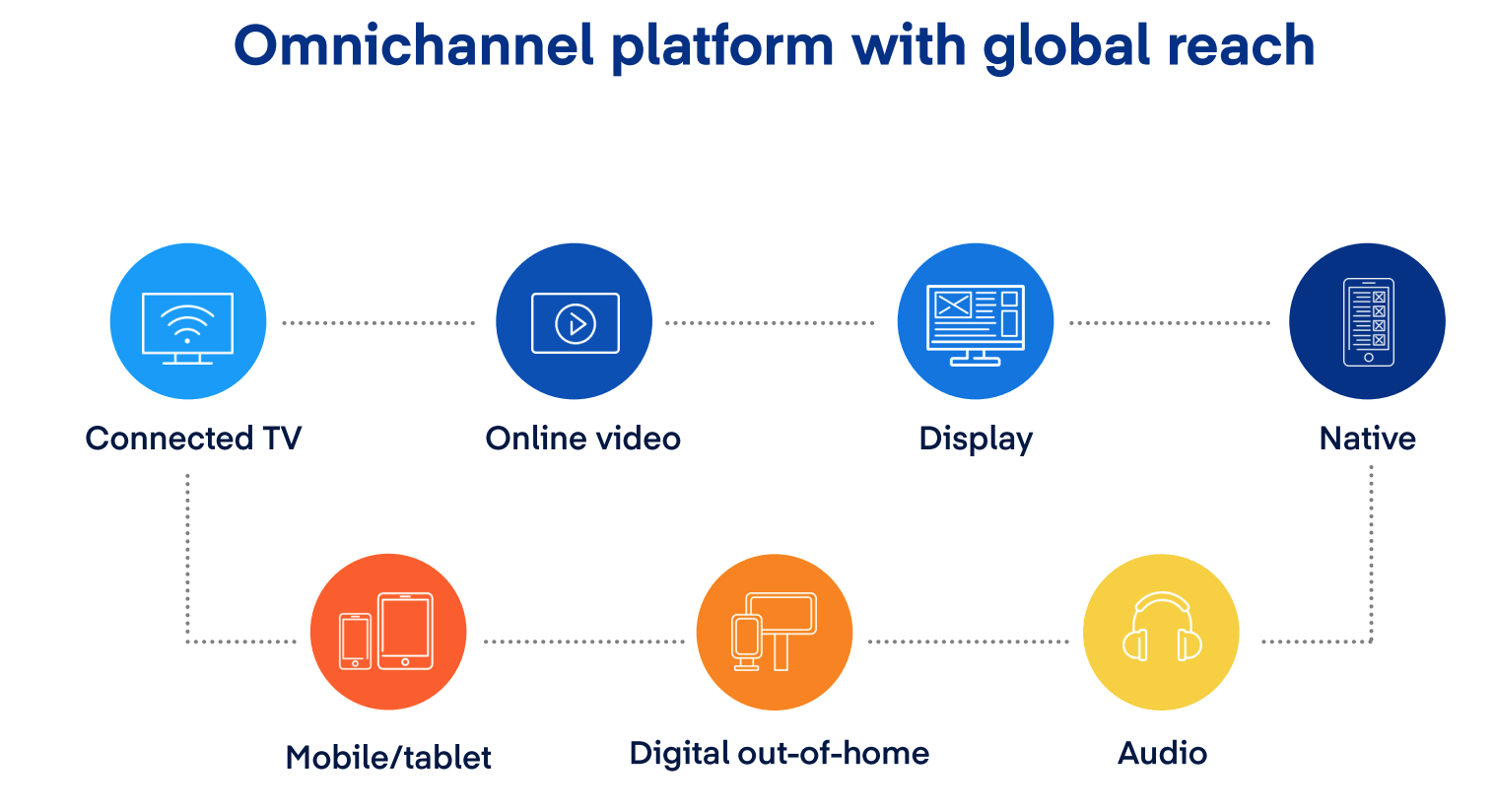

Second, TTD is a beneficiary of the increasing migration of advertising campaigns from traditional channels to digital channels and the internet since it serves as an omni-channel platform across all digital platforms (see figure).

TTD’s omni-channel platform (The Trade Desk)

Third, TTD managed to become the largest independent DSP after its foundation in 2009. So TTD becomes a beneficiary of its network effects and economies of scale. Since larger DSPs have larger scale than smaller competitors, they have lower costs per ad campaign. Consequently, they are likely to offer their advertisers cheaper conditions compared to smaller competitors. As a result, TTD could get more ads to place and more data to target these ads with. As TTD collects more data over time, their insights, analysis and data-driven campaigns get more efficient and create better results for customers. This, in turn, leads to increased customer loyalty.

Fourth, connected TV (CTV) is one of the company’s most important long-term growth drivers as ad-supported streaming services and devices proliferate, such as Roku, Xbox and most recently Netflix (NFLX). TTD reached globally more than 90 million households and 120 million CTV devices in 2022, according to the company’s investor presentation. According to Nielsen, streaming claims largest piece of TV viewing pie in July 2022, even surpassing the time viewers saw during the pandemic lockdown in April 2020 (see figure).

Streaming vs traditional TV (Nielsen)

Fifth, the company sees significant growth potential by increasing its international presence. The company’s international revenue share grew from 6.5% to 14% from 2015 to 2021. Additionally, shopper marketing, specialized on all the ways brands present themselves to online shoppers, is identified as another main growth driver going forward.

Sixth, the company is highly innovative with its technologies called Solimar and Unified 2.0. Solimar is an artificial intelligence powered platform that gathers more first-party data for advertisers to lessen their dependence on third-party data and at the same time achieve more return on their investment. Unified ID (UID) 2.0, on the other hand, is an open-source technology that helps advertisers to serve targeted ads while adding more privacy for online users and eliminating the need for third-party cookies. Procter & Gamble (PG), for example, announced adoption of UID 2.0 in September 2022.

Fundamentals and Valuation

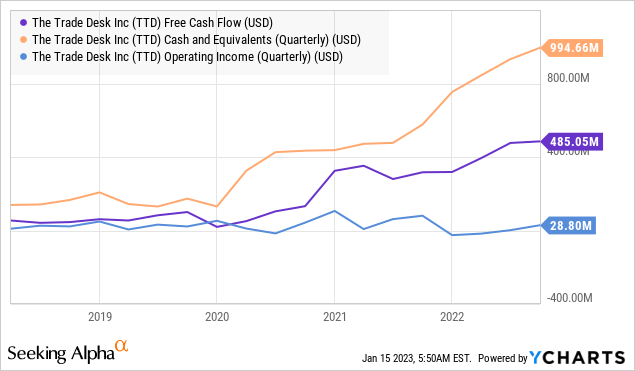

With regard to the fundamentals, it can be stated that TTD has solid financials and is net debt-free (see following figure).

TTD net debt (Seeking Alpha)

TTD also has a very comfortable cash pile of $1.3 billion with positive free cash flow and operating income. While founded in 2009, the company is profitable since 2013, which demonstrates TTD’s cost efficiency, profitability and abilities for economies of scale (see chart).

TTD financial metrics (YCharts)

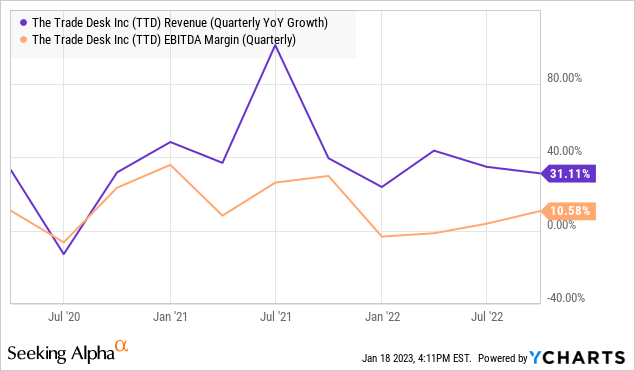

With regard to the valuation, I will use the rule of 40 by using the revenue growth rate and EBITDA margin, which is mainly used for evaluating growth stocks. According to the rule of 40, a promising investment should have a ratio of 40 or more.

With a revenue growth rate of 31.11% and an EBITDA margin of 10.58% in the most recent quarter, TTD has a ratio of 41.69 (31.11 + 10.58), according to the rule of 40, which makes TTD an attractive investment case (see figure).

TTD’s quarterly revenue growth rates and EBIDTA margin (YCharts)

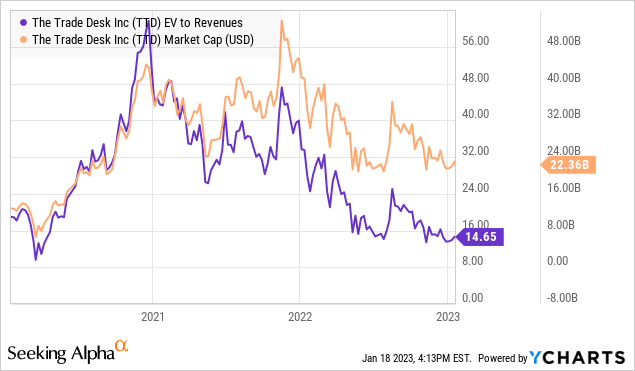

With regard to the company’s EV/S ratio and market cap, it can be seen in the following figure, that TTD’s valuation has fallen sharply due to the market sell off. While an EV/S ratio of around 15 can still be seen as expensive, the company’s profitable growth in connection with its immense growth potential could justify paying a premium.

TTD’s EV/S ratio and market cap (YCharts)

Technical Analysis

With regard to the technical analysis, it can be stated that TTD is still stuck in a downtrend. Although the stock made a breakout attempt after the most recent quarter due to a solid earnings report, the weakness in the market pulled the stock back down (see chart).

Currently, the stock is on the verge of trying a new breakout. However, I assume that a breakout will be highly depending on a recovery of the general market conditions and at least will need a retest for confirmation.

Nevertheless, the stock managed to stay much higher than its pre-COVID highs and, therefore, shows relative strengths during the current market turmoil.

TTD chart analysis (TradingView)

Risks and challenges

The biggest threat for TTD is a potential recession where advertisers could cut ad spending in order to save costs. This, in fact, could slow down TTD’s revenue growth and potentially hurt its ability to add new customers. However, the cut in general ad spending could be compensated by the proliferation of ad-supported streaming services and TTD’s increased engagement in the growing area of CTV as well as the increasing share of programmatic ad buying.

Thus, advertisers could shift their ad spending to more efficient advertising campaigns offered by TTD. This, in turn, could also offset some of the potential revenue slowdown. However, with a revenue growth rate of 31% in the most recent quarter, TTD is already growing twice as fast as the programmatic ad buying market.

Another threat, mainly for the stock, would be rising interest rates in connection with further selling pressure at the stock market leading to a further sell off of TTD shares. However, given its growth rates, the stock should be able to recover quickly as soon as the tide turns.

Conclusion

TTD operates in a fast-growing sector, has tremendous growth potential, and delivers real value to its customers, as evidenced by its double-digit growth rates and customer retention rate of over 95%.

Going forward, TTD has several major growth drivers such as the increasing migration of advertising campaigns to digital channels and the internet, the increased proliferation of CTV and ad-supported streaming services as well as the company’s innovative technologies Solimar and UID 2.0, which make advertising campaigns less dependent on third-party data or cookies and lead to more efficient advertising campaigns for advertisers.

Moreover, TTD has double-digit growth rates, is profitable, has a comfortable cash pile and is net debt free and is growing twice as much as the programmatic ad buying market.

With regard to the valuation, an EV/S ratio of over 15 seems expensive considering the current market environment and the Fed’s tightening monetary policy. However, the company’s profitable growth could justify paying a premium. Moreover, a ratio of 41.69 concerning the rule of 40 also indicates an attractive investment case.

Nevertheless, according to my chart analysis, the stock is still trapped in a downtrend despite two breakout attempts. Therefore, I believe that investors would be wise to mix TTD into their portfolio by buying on weaknesses since the selling pressure could persist if macroeconomic headwinds continue or even worsen.

Be the first to comment