Laser1987

While Rite Aid Corporation (NYSE:RAD) posted $6.1 billion in revenue for Q3, the increase in same-store sales failed to impress investors. The pharmaceutical retailer is too small to compete. It posted an earnings per share loss in the third quarter of 2022.

Rite Aid’s revenue outlook is within the consensus outlook. However, it expects huge losses in 2023. In addition, its adjusted EBITDA is below its previous guidance.

In this bear market, investors will not endure companies that lose money. Is RAD stock an exception to this rule?

Rite Aid’s Loss Increases in Third Quarter of 2022

Rite Aid posted revenue falling by $100 million from last year to $6.1 billion. Comparable same-store prescriptions rose by 4.4% while same-store acute prescriptions increased by 8%. Same-store front-end sales increased by 2.7%.

Losses increased in the quarter. The firm lost $1.23 a share, nearly double the 67-cent loss from the prior year. It did not have the Covid vaccine and testing lift from the comparable period. In addition, store closure and a planned loss of covered lives and Elixir hurt results.

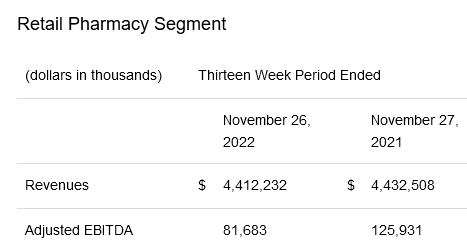

Revenue from Rite Aid’s pharmacy segment inched lower. Adjusted EBITDA fell by even more. Store closures failed to offset the revenue reduction from lower Covid vaccine and testing.

Rite Aid Q3/2022

The company depended on 72% of its total drugstore sales on prescription sales. This could prove its downfall. Amazon (AMZN) introduced an online pharmacy in 2020. Customers may conveniently buy prescription medicines on their desktop or the Amazon App.

Walmart strengthened its pharmacy program by offering a discount offering in 2021. Members could get medication discounts of up to 85% off.

CVS Health (CVS) offers home delivery for customer medications. Competitor Walgreens (WBA) offers customers free prescription delivery options, as fast as one to two business days.

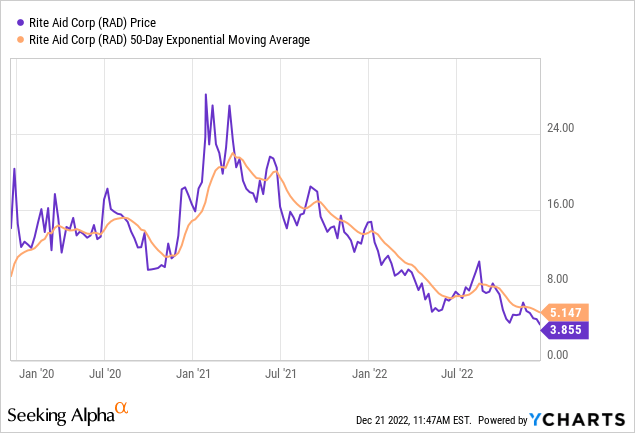

With the benefit of hindsight, RAD stock is another victim of the Covid pandemic rise and fall story. The stock more than doubled from $10 in late 2020 to peak at over $30, albeit briefly. Sellers overwhelmed buyers from 2021 to 2022.

Above: RAD stock sold off whenever it crossed the 50-day moving average.

As the chart showed, Rite Aid shareholders sold the stock at the down-trending moving average.

Executive Commentary

The company’s Chief Executive Officer highlighted the top and bottom line results beat consensus. The CEO also pointed to the accelerated sales growth at retail. However, shrink is higher. Seasonal markdowns and pharmacy margins offset any revenue growth progress.

CEO Heyward Donigan said that Rite Aid will kick off a performance acceleration program. He promised improved sales, script volume, and operating margin.

Outlook

Rite Aid expects revenue in the range of $23.7 billion to $24.0 billion in fiscal 2023. This is within the consensus estimate. It expects its Retail Pharmacy Segment revenue at $17.4 billion to $17.6 billion. The company expects to lose between $584 million and $551 million. Adjusted EBITDA of $410 million to $440 million is below its previous guidance of $450 million and $490 million.

Rite Aid cited lower pharmacy margins and cautious consumer demand as some of the reasons for the weaker adjusted EBITDA.

Lost Opportunity

The bet on Rite Aid’s revenue converting to profits did not play out. Its business has negative free cash flow. Still, Rite Aid expects to spend around $225 million on capital expenditures. It is investing in digital transformation. This adds digital capabilities to business operations. It will also invest in prescription file purchases and distribution center automation.

CEO Donigan said that the company is doubling down on the pharmacy business. It has a mail order and specialty pharmacy to capture market share in the $1 trillion marketplace.

Rite Aid may promote pharmacists as the most trusted healthcare adviser in the community and healthcare ecosystem. However, customers may easily rely on CVS Health or Walgreens for the same or better service.

It could empower its retail pharmacists with the tools to practice the medicine of pharmacy. However, the CEO cited such tools as Zoom (ZM) for digital engagement.

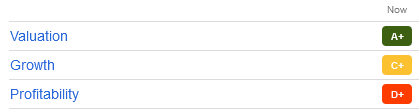

RAD Stock Grade

RAD stock earned an A+ on valuation.

Seeking Alpha Premium

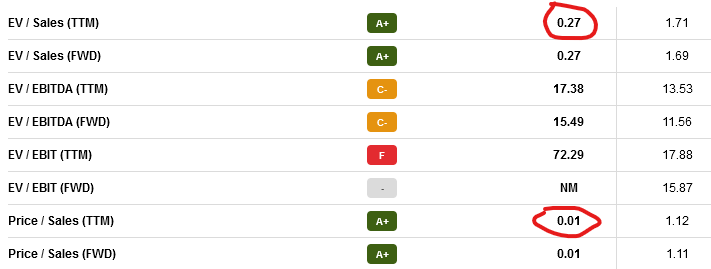

The company trades at a fraction of the median EV/Sales and price/sales multiples. In the table below, the figure on the left is that of Rite Aid. On the right is the sector median.

Seeking Alpha Premium

Investors will gladly pay a premium for CVS stock instead. CVS scores a D+ on value, hurt mostly by the GAAP TTM P/E of 39.9 times. The sector median is 24.1 times.

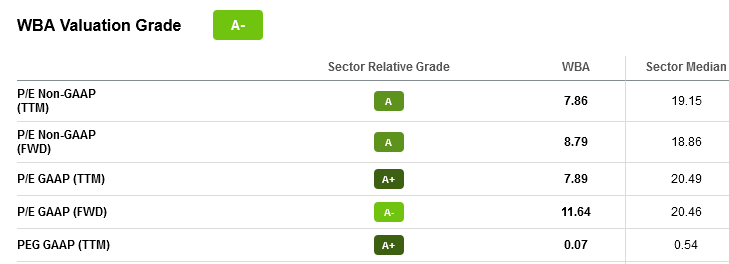

Value investors could buy Walgreens instead. WBA stock has an A- grade on value:

WBA Valuation Multiples (Seeking Alpha Premium)

Your Takeaway

Speculators continue to unwind their bet on Rite Aid. The post-pandemic boom-bust cycle is over. Covid is an endemic that did not lift this company’s business in 2022.

Since pulling back from $110 earlier this year, CVS is a better alternative. The stock pays a dividend that yields 2.4%, after raising it by 10% on Dec. 15, 2022. Walgreens Boots Alliance pays a dividend that is almost double that of CVS stock. It also raised $1.0 billion, which it will use primarily for debt paydown and funding its strategic priorities.

Be the first to comment