interstid

A little over two years ago, when we were still all worried about the pandemic, I wrote one of my most-read articles ever in which I argued that real estate investment trusts (“REITs”) would pummel Tech stocks going forward.

In today’s article, we first review the results since then, and we then update our outlook for the future.

Back in August 2020, REITs were heavily discounted because the pandemic had essentially shut the real world, causing some rents to go missing and tenants to default. Moreover, Amazon (AMZN) was stealing market share of retail properties… Airbnb (ABNB) was stealing market share of hotel REITs… And Zoom (ZM) was allowing people to work remotely, putting great doubt on the future of office buildings…

SL Green

Tech stocks (QQQ), on the other hand, were flying high. They were the biggest beneficiaries of the pandemic since people were locked inside in many parts of the world, and spent a lot more time scrolling Facebook (META) and watching Netflix (NFLX). All sorts of new tech businesses suddenly emerged and quickly gained huge valuations. The best example is perhaps Peloton (PTON) and its live-streamed workouts, which for a while were believed be about to replace people’s gym memberships…

Peloton

I argued that the market was too pessimistic about REITs and overly optimistic about Tech stocks because:

- Most REITs don’t invest in offices, malls, or even hotels. Most invest in defensive sectors like cell towers, storage, apartments, farmland, etc.

- The valuation discrepancy between the two had reached an extreme.

- The pandemic was a severe, but temporary crisis.

- It wouldn’t change our social human nature.

- The vaccines would greatly benefit REITs, but hurt tech stocks as things return to normal.

- And finally, there is only so much that you can grow. More than half of US households already had a Netflix account… How much more can they really grow?

Here we are two years later, and there are a few interesting things to note:

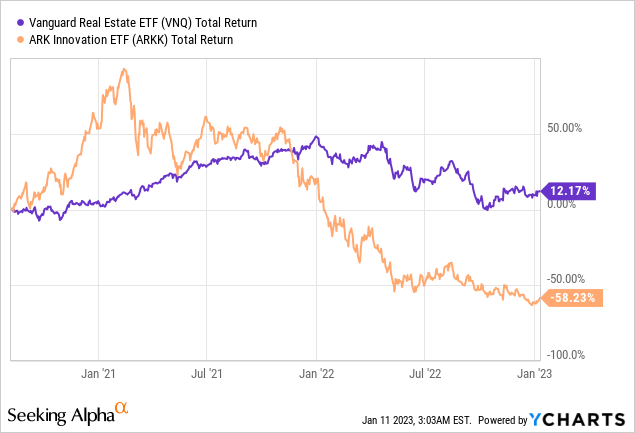

Firstly, REITs absolutely crushed the returns of the highly innovative tech stocks as represented by ARK Innovation ETF (ARKK) that benefited the most from the pandemic:

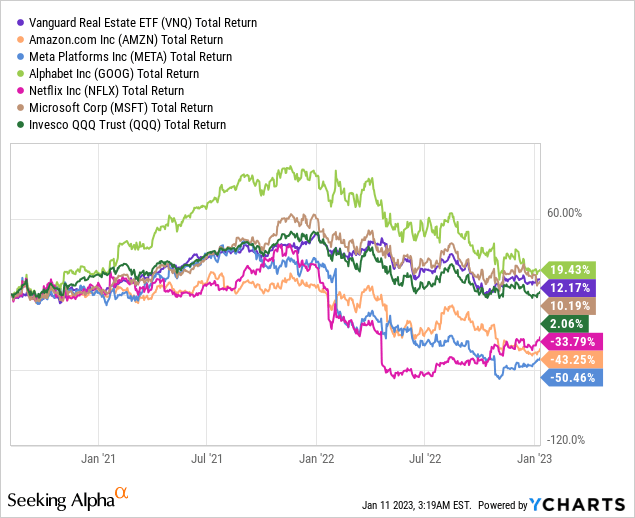

Secondly, REITs also did materially better than most FAANG stocks, with Meta, Amazon, and Netflix losing significant value. Microsoft (MSFT) performed almost in line with REITs, and Alphabet (GOOG) even managed to outperform. Still, overall, Tech stocks did quite a bit worse, but not as badly as I would have expected:

But what about today?

Do we still expect REITs to keep outperforming going forward?

Or should we now start favoring tech stocks again?

Today, it is more difficult to answer these questions.

Yes, REITs remain undervalued, but tech stocks also aren’t as insanely expensive as they were two years ago. Most of them have grown quite significantly even as their share prices collapsed.

Even then, I continue to favor REITs and invest most of my capital in them rather than tech stocks, and there is one main reason for this:

The recent surge in inflation and interest rates strongly favors REITs over tech stocks.

Let me explain why…

Until recently, interest rates were at near-0% and so valuations and profitability did not really matter.

All the market cared about was the future. Will a company be able to grow rapidly and generate significant profits sometime in the future?

Even if those projected profits were 10 years into the future, it did not really matter because inflation was low and interest rates were near-0%. In valuation models, you could use very low discount rates and come up with insane valuations, despite making no profits today.

But this has now changed.

Inflation suddenly took off and so did interest rates. As a result, the projected profits that are 10 years away suddenly aren’t worth as much anymore… and investors care a lot more about today’s profits.

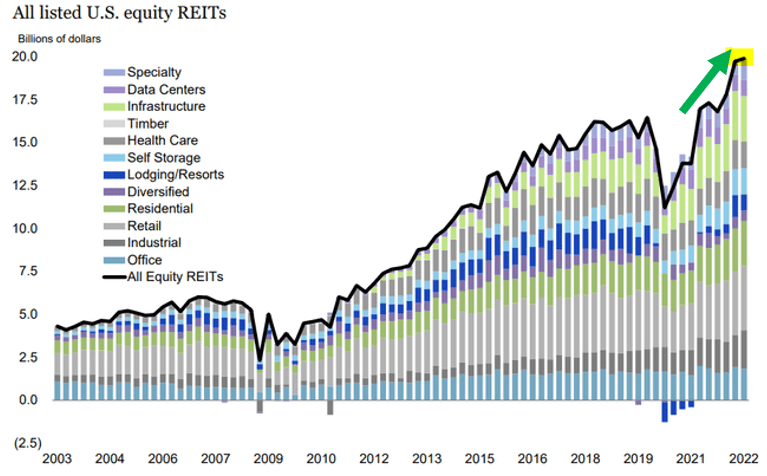

REITs are well-positioned for this environment because they generate significant profits today and these profits are now growing rapidly because the high inflation results in growing rents. Just take a look at the growth in 2022:

NAREIT

Moreover, REIT balance sheets are today the strongest ever with just 35% debt, mostly fixed-rate, and maturities are long on average at around 8 years. So the impact on their interest expense is very manageable.

Tech stocks, on the other hand, are much worse positioned in most cases.

Many of them weren’t profitable even before the recent surge in inflation and interest rates. Now suddenly, their costs are going up significantly even as competition is growing because the high valuations attracted a lot of new VC investments in recent years.

Moreover, something that the market is overlooking in my opinion is that a lot of tech companies have a leadership problem.

In recent years, the market only cared about topline growth and so that’s what management teams focused on. They invested heavily, made huge losses, and no one really cared. You could always raise more equity at a low cost to reinvest in growth.

Those days are now over, and tech stocks need to grow their bottom line and reach profitability. But the skill set and leadership that’s needed for this are very different and I fear that a lot of tech stocks will have to make major management changes because some CEOs are good at growing revenues… and others are better at growing profits.

And so lots of tech stocks are now facing a cascade of issues:

- Their access to equity and debt markets is now limited

- They are scrambling to reach profitability

- Even as their costs and competition are rising

- And their management teams may not have the right skills for this.

So yes, valuations are down, but rightfully so in many cases.

REITs, however, are also discounted, but the market’s rationale for discounting them is a lot more questionable. It is discounting REITs because of rising interest rates, but it appears to underappreciate the fact that REIT balance sheets are the strongest they have ever been and rents have grown a lot.

It is easier to make a case here that they are undervalued and so that’s where most of my capital is going.

Some of My Top Picks

I recently posted a video in which I cover two of my top picks:

BSR REIT (OTCPK:BSRTF) owns apartment communities in rapidly growing Texan markets. Its same property NOI is expected to rise by 12-14% for the full year of 2022 (4th quarter not yet released), and yet, it is priced at a 40% discount to its total net asset value.

Whitestone REIT (WSR) is similar, but it focuses on service-oriented strip centers in other rapidly growing sunbelt markets, and it is equally discounted:

These are just two examples of REITs that are heavily discounted. We own a portfolio of 24 such REITs at High Yield Landlord. They represent the bulk of my net worth, and I only hold a small portfolio of tech stocks in comparison.

Bottom Line

REITs did a lot better than tech stocks as the world reopened and we moved past the pandemic. This benefited REITs and hurt many tech stocks.

Now, we expect more of the same as inflation and rising interest rates hurt tech stocks a lot more than REITs.

REIT cash flows are rising rapidly and yet, they are heavily discounted.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment