John M Lund Photography Inc/DigitalVision via Getty Images

Thesis: The Original “Buy” Thesis Has Broken

Over the last year, senior housing landlord National Health Investors (NYSE:NHI) has navigated a storm of overdue deferred rent balances, rent restructuring agreements, tenant transitions, and conversions of net leases into SHOP (senior housing operating portfolio) leases.

Back in 2021, I had high hopes that NHI would survive the COVID era disruption relatively unscathed and be well-positioned to enjoy huge upside from aging demographics down the road. Hence my two bullish articles in June and August:

- NHI: The Long-Term Outlook Remains Strong Despite Current Weakness

- NHI: The Most Bearish Bull Thesis I Ever Hope To Write

Indeed, my argument that the bad news appeared to be adequately priced in proved more or less accurate, as NHI didn’t have much further downside after those articles came out.

And NHI remains conservatively managed REIT in this space, sporting a fairly strong balance sheet with net debt to EBITDA of 4.5x. Moreover, after a nearly 20% dividend cut during the pandemic, NHI’s payout ratio is comfortable at around 80%, implying that another dividend cut is unlikely at this point.

But my original “buy” thesis for NHI implicitly relied on the company remaining a net lease REIT rather than a hybrid of net lease and SHOP, wherein the REIT takes operational risk while also enjoying more potential revenue upside. I think operators are going to struggle to increase profits for a long time to come, perhaps permanently, which made the net lease structure far more appealing to me.

So, in short, I decided to sell NHI recently for three main reasons:

- One of the primary reasons why I picked NHI over other senior housing REITs was its emphasis on net leases rather than SHOP properties. I liked the (perceived) downside protection of net leases. Now that many of those net leases have been converted into SHOP properties, that original differentiator for NHI is gone.

- As explained in an exclusive report on the healthcare labor market for High Yield Landlord, I believe inpatient healthcare (including assisted living) faces a permanent labor shortage going forward, and technology will have a hard time replacing workers. Demand for senior housing will likely still rise due to aging demographics, but I am far less optimistic than I used to be about operators’ ability to profitably take advantage of this wave of demand.

- Home healthcare appears to be poised to take more market share from senior housing than I thought a few years ago.

Let’s get a quick update on NHI before discussing the labor shortage and home healthcare issues.

Update On NHI

I have to admit: the COVID-era issues facing NHI have dragged on far longer than I thought they would. In fact, they appear to have morphed into indefinite issues at this point. Sure, occupancy is slowly improving, but tenant-operators’ rent coverage is still languishing.

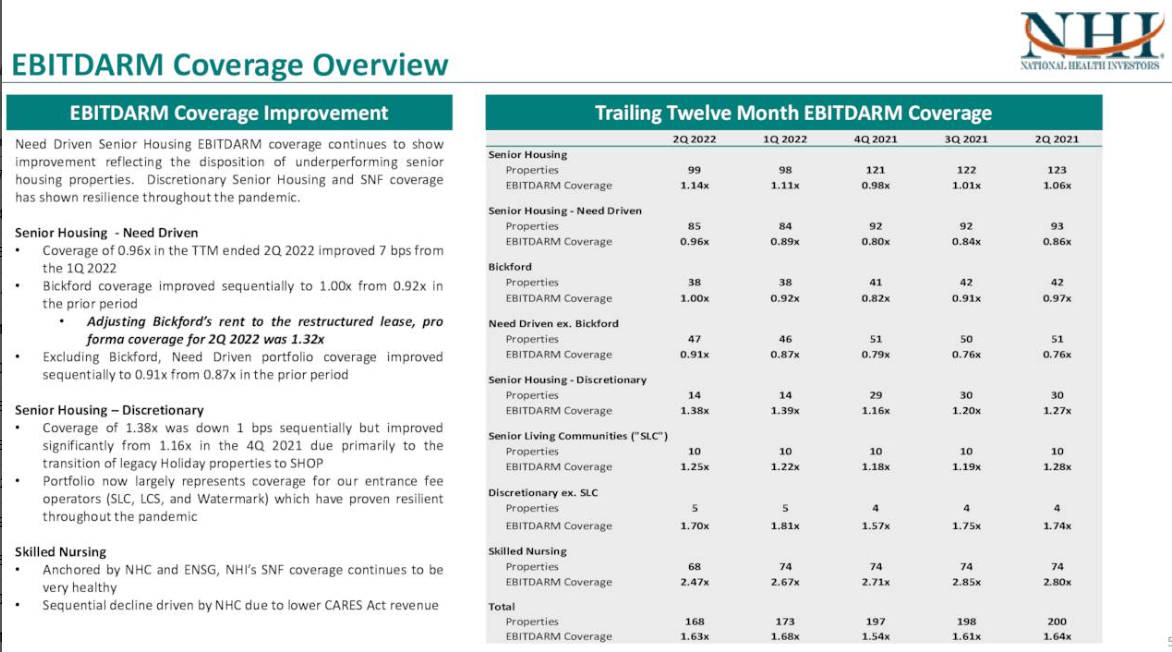

NHI’s rent coverage ratios have only improved through selling many of its properties with the lowest rent coverage levels, and only slightly (from 0.98x in Q4 2021 to 1.14x in Q2 2022 on a TTM basis).

NHI Q3 2022 Update

Eric Mendelsohn commented on the Q3 2022 conference call:

Since we announced our optimization plans in the second quarter of 2021, we have completed the sale of 32 senior housing properties for net proceeds of $296 million and had a cash NOI yield of just 2.7% and EBITDARM coverage of only 0.47 times.

On the conference call, management noted that they were targeting another $50 million to $60 million of property sales in the near future (probably Q4 2022 and 1H 2023).

NHI also increased rent coverage (from 1.0x to 1.32x) with one of its largest tenants simply by giving a rent reduction in April 2022.

NHI Q3 2022 Update

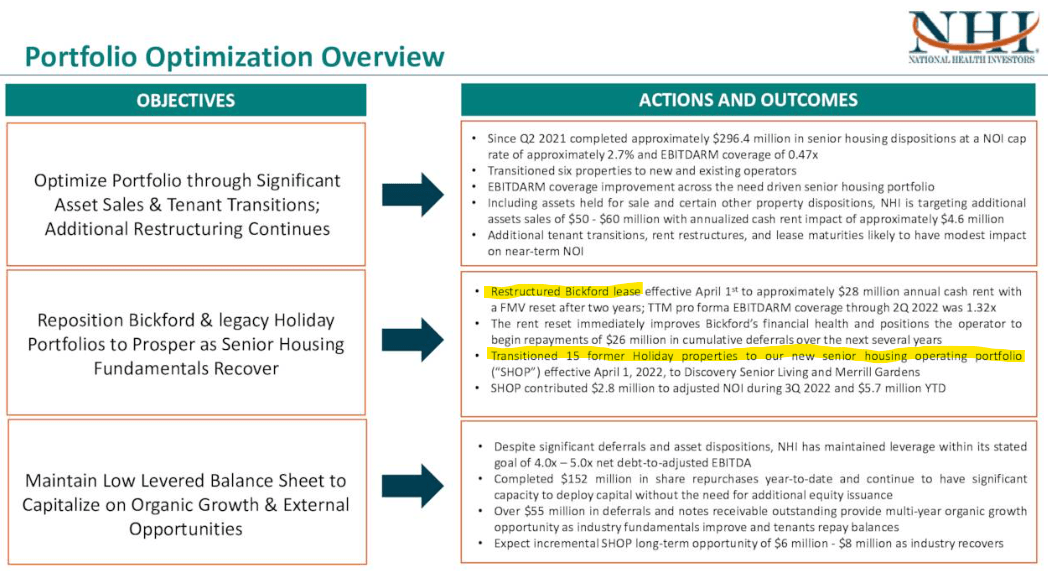

Worse (in my mind) is that in response to a certain tenant’s weakness, NHI decided to convert triple-net leases with that tenant into SHOP properties, wherein NHI entered into a joint venture with new operators.

NHI Q3 2022 Update

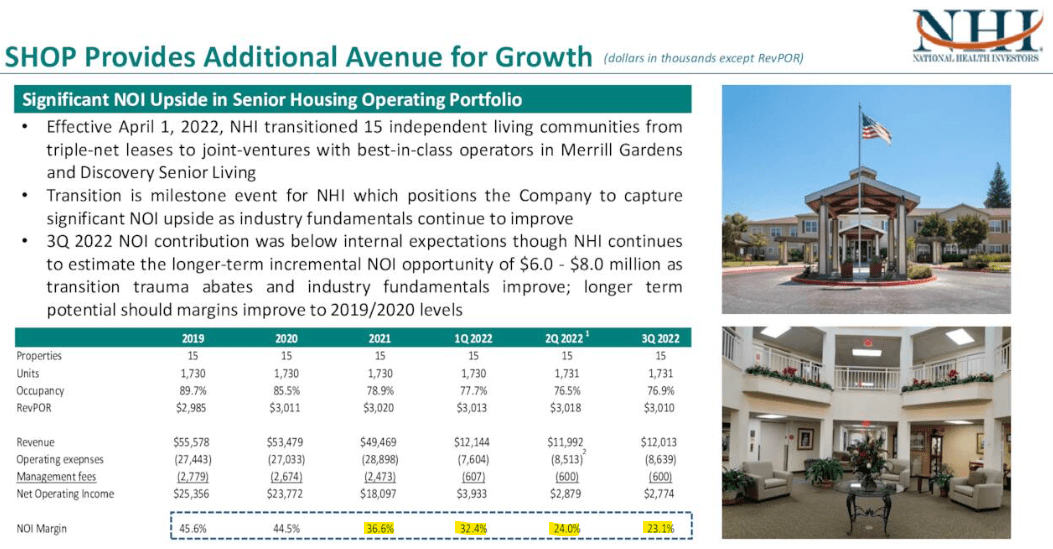

While NHI touts the benefits of SHOP being future NOI upside, it would take quite a bit of NOI upside just to return to the level of NOI generated by the same properties when they featured triple-net leases. Notice the NOI margin line at the bottom of the slide above. The leases in question transitioned from triple-net to SHOP at the beginning of Q2 2022, so you can see the steep drop-off in NOI that came with this transition.

In fact, at these SHOP properties, NOI continued to erode from Q2 to Q3.

Here’s Mendelsohn again from the Q3 conference call:

While the third quarter results exceeded our expectations, the operating environment for our tenants in the SHOP portfolio remains challenging, with labor and other inflationary pressures weighing on margins.

One of the things that originally drew me to NHI was its steadiness and predictability. That’s the benefit that comes with net leases. The upside is capped, but the downside is far more limited as well.

To be fair, only a minority of properties were converted from net leases to SHOP, but I fear NHI will have to convert more triple-net leases into SHOP properties sooner or later. That makes NHI far less appealing to me.

The bright spot for NHI is the REIT’s balance sheet, which has remained strong through the entirety of the COVID-era troubles. The credit rating of BBB- sits just on the right side of investment grade status, but the outlook remains stable at all three major ratings agencies.

NHI Q3 2022 Update

Moreover, recent property sales have allowed NHI to repay $377 million of debt.

But the REIT still had $415 million of maturing debt in 2023, as of the Q3 2022 update. That is a sizable chunk of NHI’s total debt. How does management plan to handle it?

Here’s the only hint we heard from CFO John Spaid on the Q3 conference call:

We have three upcoming maturities in 2023 totaling $415 million.

You will see us initially retire the first $125 million note due in January using proceeds from our revolver. But we will be working toward a new debt facility in 2023, and we’ll keep you apprised of our strategy and progress.

Since NHI would probably have to refinance its maturing notes with interest rates in the 5-6% range, it is instead repaying the first tranche of maturing debt with funds from its floating rate credit facility.

Since BBB bond yields have been drifting downward so far this year, NHI may be able to refinance the other two maturing notes with new unsecured notes, albeit most likely at higher rates. Thus, rising interest costs creates another headwind for NHI, albeit a relatively small one.

Competition From Home Healthcare

The biggest problem with NHI and the senior housing sector more broadly, as I see it, is the combination of a labor shortage and home healthcare taking market share.

These two factors are somewhat intertwined, in my view, because home healthcare seems to have poached many of the workers who left the senior housing industry.

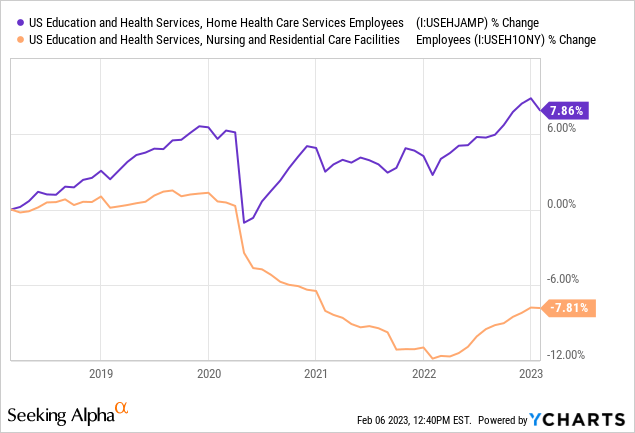

Below we find the total growth in home healthcare employees in purple and nursing & residential care facility employees in orange over the last five years:

When COVID-19 hit the US in March 2020, both industries saw a quick exodus of workers, but home healthcare bounced back far faster. Today, senior housing remains around 8% below its pre-pandemic level, while home healthcare sits about 2% higher than its level immediately preceding the pandemic.

It makes sense why workers would flee assisted living facilities for home healthcare when the staff-to-resident ratio at assisted living may be 1:8 or more, while home healthcare is 1:1. The pay may be higher at senior housing facilities, but the level of stress and burnout rate is much higher as well.

What’s more, technology improvements are making it increasingly easier to accommodate elderly patients’ needs at home, where the vast majority of seniors say they would rather be than a senior care facility.

Meanwhile, not only does the supply side look better for home healthcare, the demand side looks better, too.

According to Insider Intelligence, the US home healthcare market is expected to surge from $100 billion in 2016 to $225 billion in 2024.

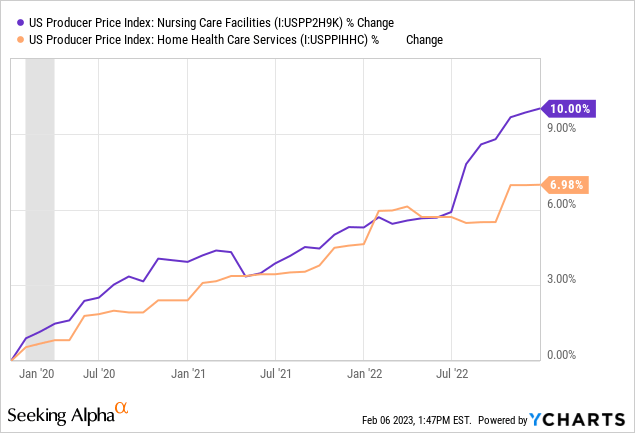

And, perhaps due to the capital-light nature of the service, the costs of home healthcare have risen much slower over the last three years than nursing care facilities.

When faced with these realities, I had to ask myself: Do I really want to remain invested in the more expensive and less appealing option for the vast majority of seniors?

And while the situation is bound to improve to some degree for senior housing, is the upside significant enough to make continued ownership of NHI the best use of my investment dollars?

Bottom Line

The answer I ultimately came up with to these questions was “no.”

Because of aging demographics, the number of workers going into senior care will likely continue to diminish relative to the number of seniors who require residential care. And the workers in this space seem to prefer the working conditions of home healthcare rather than inpatient facilities.

Moreover, the drastic steps NHI has had to take in order to keep its tenant-operators afloat have made the long-term case for owning the REIT far less appealing to me.

I initially bought NHI because I liked that 100% of properties were net leases. Since that is no longer the case, part of my original investment thesis is broken.

I have not become bearish about NHI. Returns from here will, I believe, be middling. But the investment case was not attractive enough, given the ostensible risks and persistent troubles facing the industry, to continue holding the REIT. Thus, I sold NHI and reinvested into similarly high-yielding names that I believe have far better long-term growth potential.

Be the first to comment