Jorge Aguado Martin/iStock via Getty Images

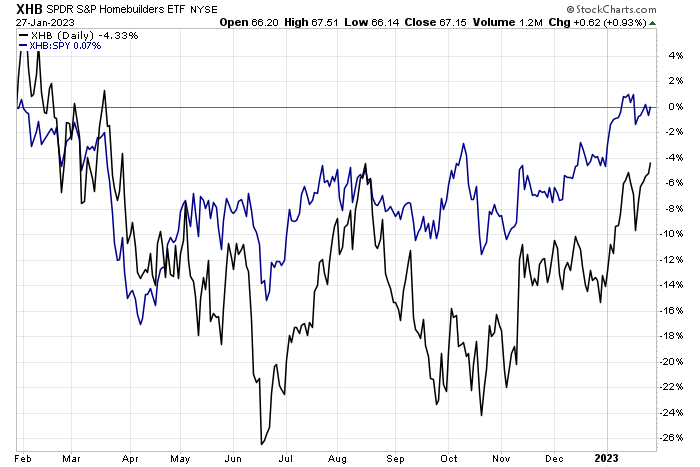

What comes to mind when you think of the homebuilders? The usual names – Lennar, Pulte, KB Home – are known for their highly volatile and cyclical trading action. The group has indeed moved up big from the lows notched in June last year. Despite a plummeting housing market, the SPDR S&P Homebuilders ETF (XHB) is up big from that Q2 2022 nadir as it outperforms the broad market.

One name in the fund, Whirlpool, is awash in bears, though. With a key earnings date on tap, is it time to turn on the buy cycle on this household name, or should you press the off button? Let’s take a look.

Homebuilders Rally Despite Housing Market Turmoil

Stockcharts.com

According to Bank of America Global Research, Whirlpool (NYSE:WHR) is a leading global appliance manufacturer, with a mid-30s% market share in the US and 2021 global revenues of $22 billion. North America is WHR’s largest market, followed by Latin America, EMEA, Asia, and Others. Laundry appliances have historically made up roughly 30% of revenues, as do refrigerators/freezers. Cooking accounts for just under 20% of revenues, with other products accounting for just over 20% of sales.

Whirlpool bears have been in charge with a pair of key downgrades in the last few months following a downbeat guidance announcement earlier this month. WHR spun lower after a guidance cut in its Q3 earnings report in October. Weak consumer demand trends were cited as the culprit of its earnings and revenue misses. In my view, there are clearly bearish headlines floating around, with few signs of improvement despite some optimistic broad spending outlooks from major credit card companies last week.

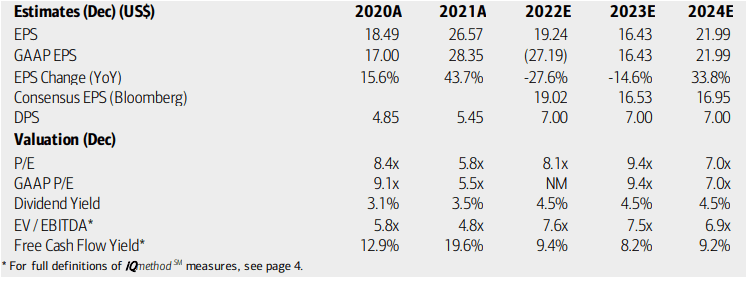

On valuation, analysts at BofA see earnings having fallen sharply in 2022 after a pair of strong years, no doubt driven by the work-from-home trend. But how many dishwashers and washer/dryer sets can you buy? As a result, last year and this year are expected to see sharply negative changes in EPS. The upside is that BofA expects per-share profits to increase markedly in 2024. We’ll see.

Dividends, meanwhile, are expected to hold at $7, which results in a solid yield that should be sustainable given an impressive free cash flow yield about twice that of the broad market. With low GAAP and operating P/Es, there’s pessimism baked in. WHR also trades at a steep EV/EBITDA ratio discount to the S&P 500.

Whirlpool: Earnings, Valuation, Dividend Yield Forecasts

BofA Global Research

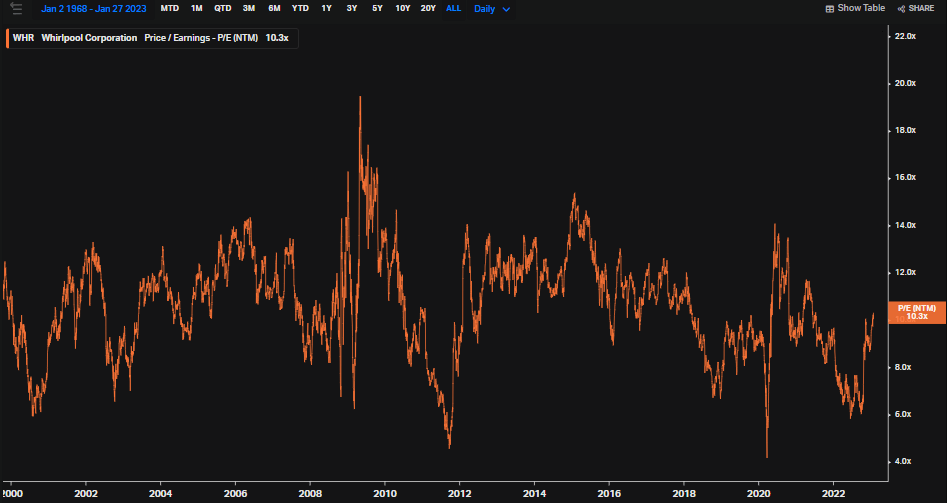

According to Koyfin Charts data, WHR trades near its long-term average forward earnings multiple, so the stock may not be as much of a value as you might think at first glance. Seeking Alpha notes that Whirlpool’s forward price-to-book ratio is very close to the 5-year average as well. Overall, the valuation actually just seems fair to me, but dividend investors can hold the stock for its high yield – at 4.5%, that’s about 120 basis points above the 5-year norm.

WHR: Historical Forward P/E History

Koyfin Charts

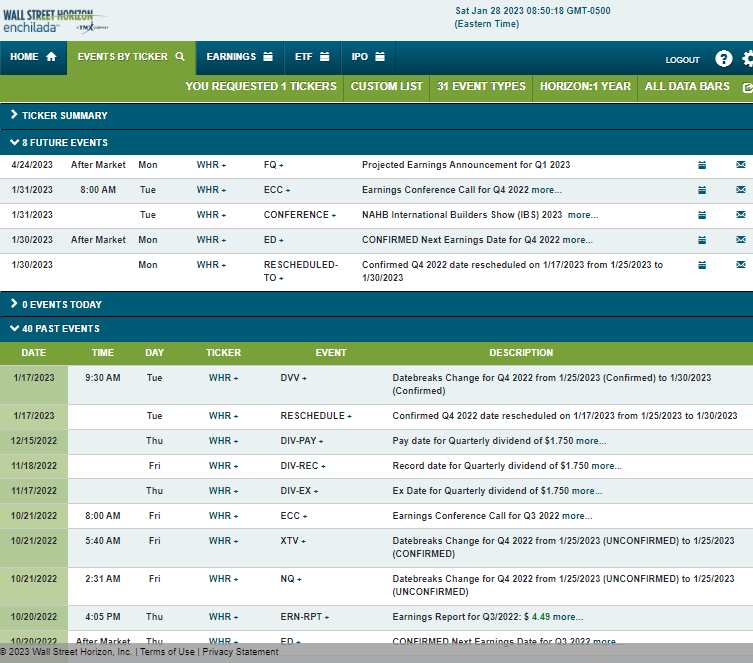

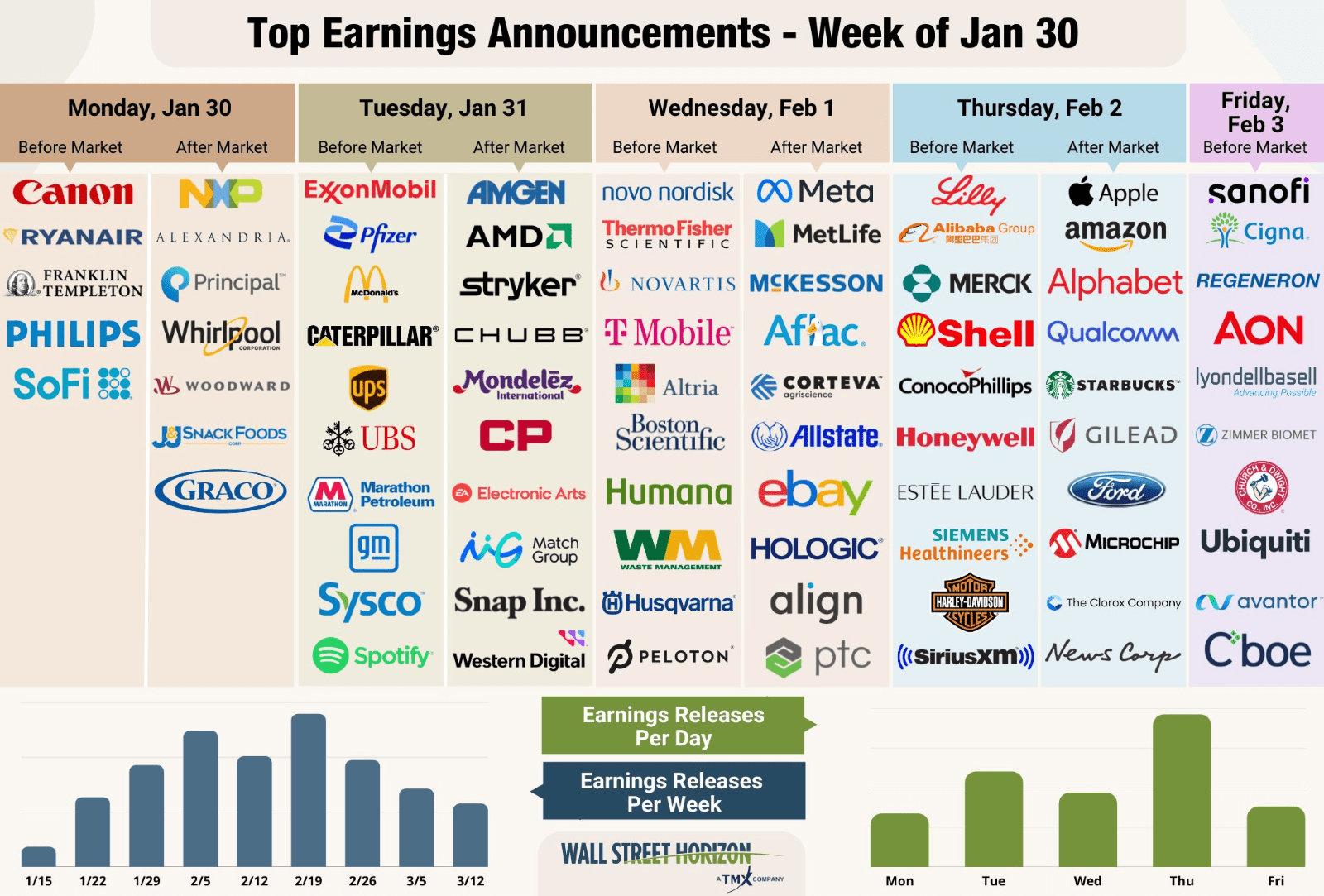

Looking ahead, corporate event data from Wall Street Horizon show a confirmed Q4 2022 earnings date of Monday, January 30 AMC with a conference call the following morning. You can listen live here. More volatility could come Tuesday through Thursday when the National Association of Home Builders hosts its International Builders’ Show 2023. Whirlpool’s management team is expected to present.

Corporate Event Risk Calendar

Wall Street Horizon

Whirlpool is one of many S&P 500 companies reporting Q4 results this week.

Earnings This Week

Wall Street Horizon

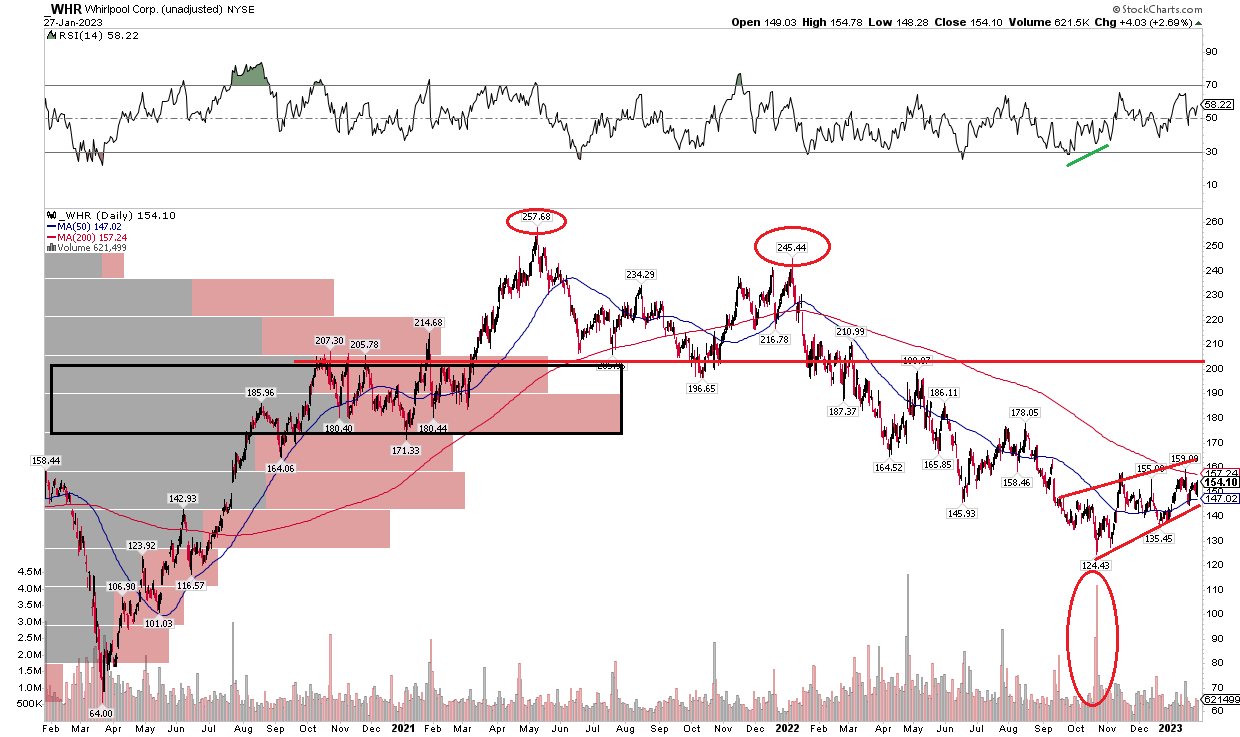

The Technical Take

With a lukewarm valuation and high yield, what does the chart say? I see bearish risks. Notice in the chart below that WHR put in a bearish double-top pattern from 2021 to 2022, then broke key support in the $197 to $215 range. With a bear market enduring for nearly two years now, the bulls’ grip on the stock that has persisted since late October could be about to break. I spot a bearish rising wedge pattern. If the $140 to $145 range breaks, then I see a downside target to near $105.

Also on the chart we see big bearish volume notched at the October low. While that sometimes signals a capitulation low (and it featured bullish RSI momentum divergence), without a strong upward thrust off that level, it likely portends more downside to come. Finally, even if we see a continued rally, there’s heavy volume by price right under the noted resistance point – there are many ‘dead bodies’ there to bring a supply of shares to the market.

WHR: Bearish Rising Wedge

Stockcharts.com

The Bottom Line

WHR is an underperforming name without a compelling valuation case right now. Moreover, the technical picture is bearish in my view ahead of earnings Monday night. I would lean short on this name and wait for further downside before deeming Whirlpool’s fundamental and technical conditions clean.

Be the first to comment