Woman is delivering a small package that may have great value FG Trade

I am going to analyze the construction of 15 small-cap value ETFs to give my opinion on which ones actually deliver the small-cap value premium.

The Small-Cap Value Premium

Eugene Fama and Kenneth French are two academics who are well known for the three-factor model which attempts to explain stock returns based on:

- market-wide stock performance

- size

- value

The conclusion they reached was that small value stocks produce the highest returns. There is still much debate over this topic and they have written many papers since then. In addition, the size and value premium are not constant and some feel it is disappearing.

It is not within the scope of this article to debate the small-cap value premium. My personal feeling is that the small-cap value premium is still very much alive and well. But it cannot be captured by simply looking for small market capitalizations and low price-to-book stocks. You need a mechanism to separate the high-risk stocks. I have found no better measure than free cash flow. But I will get to that later.

Assuming you want exposure to the small-cap value premium, which of the following 16 ETFs make suitable candidates?

- (VBR)Vanguard Small-Cap Value ETF

- (IJS)iShares S&P Small-Cap 600 Value ETF

- (AVUV)Avantis U.S. Small Cap Value ETF

- (SLYV)SPDR S&P 600 Small Cap Value ETF

- (VIOV)Vanguard S&P Small-Cap 600 Value ETF

- (RWJ)Invesco S&P SmallCap 600 Revenue ETF

- (VTWV)Vanguard Russell 2000 Value ETF

- (XSVM)Invesco S&P SmallCap Value with Momentum ETF

- (ISCV)iShares Morningstar Small-Cap Value ETF

- (RZV)Invesco S&P SmallCap 600® Pure Value ETF

- (FYT)First Trust Small Cap Value AlphaDEX Fund

- (ISVL)iShares International Developed Small Cap Value Factor ETF

- (SVAL)iShares US Small Cap Value Factor ETF

- (AVSC)Avantis U.S Small Cap Equity ETF

- (DEEP)Roundhill Acquirers Deep Value ETF

Small-Cap Definition

First up, we want to know if our small-cap fund is actually investing in stocks which we consider to be small.

- A common definition of small-cap is a stock which has a market capitalization between $300 million and $2 billion.

Popular ETF’s amassing huge amounts of capital will often stretch the reasonable limits of the small-cap definition due to capacity restraints. A fund with tens of billions in assets cannot possibly invest responsibly in a focused group of small-cap value stocks.

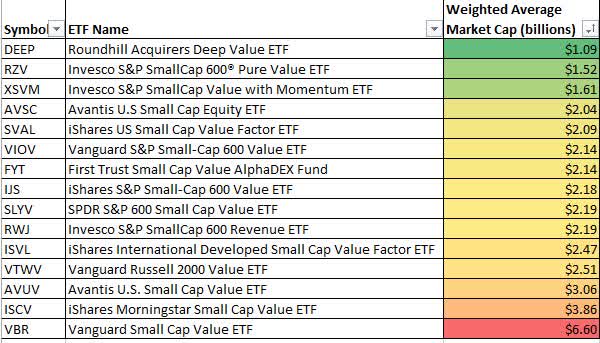

Our first test is to look at the weighted average market capitalization of the stocks in the small-cap value funds. These numbers were extracted from ETF.com

ETF.com

Remember that these are averages. Some stocks in the funds have higher capitalization and others are lower. If we adhere to our definition of small-caps being $300mm to $2B, then I would prefer the average should be closer to $1B. DEEP, RZV and XSVM would fit these requirements.

I could even be coaxed into going a little higher to possibly include a mix of small-cap and mid-cap stocks. But VBR is definitely not a small-cap fund. It is solidly footed in the upper end of the mid-cap range and some of its holdings are large-cap.

Weighting Scheme

Another important aspect is how funds choose to weight positions. Many funds choose to weight according to market capitalization where larger stocks get more weight within the fund. This scheme lowers turnover when rebalancing and thus lowers cost. Friction costs are also reduced as less capital is placed in smaller stocks with higher slippage. While it makes sense on a cost basis and allows the fund to trade more capital, it does not make sense to weight towards larger stocks when trying to capture the size premium. You are working against yourself and the very premium you are hoping to gain.

Any fund that is market-cap weighted and one that is fundamentally size weighted (RWJ) are nixed from the recommendation list.

Derived from ETF provider websites

Small-Cap Value Contenders

So far, this is the list of small-cap value ETFs that warrant further investigation after we refine the list based on weighting scheme and average size of stock in the fund.

- DEEP

- RZV

- XSVM

- AVSC

- SVAL

- FYT

Questionable Definition of Value

But we are not finished with these funds yet. How do they define value? There are a number of acceptable ratios such as

- low price-to-book

- low price-to-sales

- low price-to-earnings and so forth

But one definition that I reject with full force is to change the label on low growth companies to value. A company with slow and declining revenue or fading earnings growth is not necessarily a value stock.

Yet, some index providers do just this. The justification is that they are trying to label a stock as a value stock or a growth stock and they want these two ideals to be mutually exclusive. But guess what? You can have a stock which has growth AND value properties.

Therefore, any fund that employs this method of defining value is not a fund I want to hold. It will have you holding bad value where growth is slowing and profitability may be negative. I want deep value where growth is improving. I prefer an under-the-radar value stock instead of a high-priced and falling meme stock.

FYT and RZV get a fail with this rule. They use low-growth as one of the definitions of value.

This takes us down to 4 small-cap value ETFs.

Number of Positions

Another aspect I like to consider is the number of positions. A fund that has too many positions is likely watered down and not capturing the premium.

I would remove AVSC from the list as they have 1142 stocks in the fund. Furthermore, the weighting scheme is a blend of market-cap weighting and other characteristics such as value, momentum and profitability.

This takes us down to three funds: DEEP, XSVM and SVAL

Removing Higher Risk

One of the best measures I have found to remove high-risk and low-performing small-cap stocks is to filter out those with negative free cash flow. Negative earnings would be a second-best measure if you cannot calculate or find free cash flow easily. You can read about the affect positive free cash flow has on small-cap stocks in this article where I discuss DEEP in more detail.

A fund with a low percentage of stocks with positive free cash flow would be a red flag for me.

- DEEP – 85% of stocks have positive FCF trailing 12 months

- XSVM – 75% of stocks have positive FCF trailing 12 months

- SVAL – 83% of stocks have positive FCF trailing 12 months

All three funds would get a pass although I would place a little more emphasis on SVAL and DEEP.

Final Thoughts

All three small-cap value funds would make suitable holdings for an investor wanting strong exposure to the size and value premiums.

ycharts.com

A few things to keep in mind:

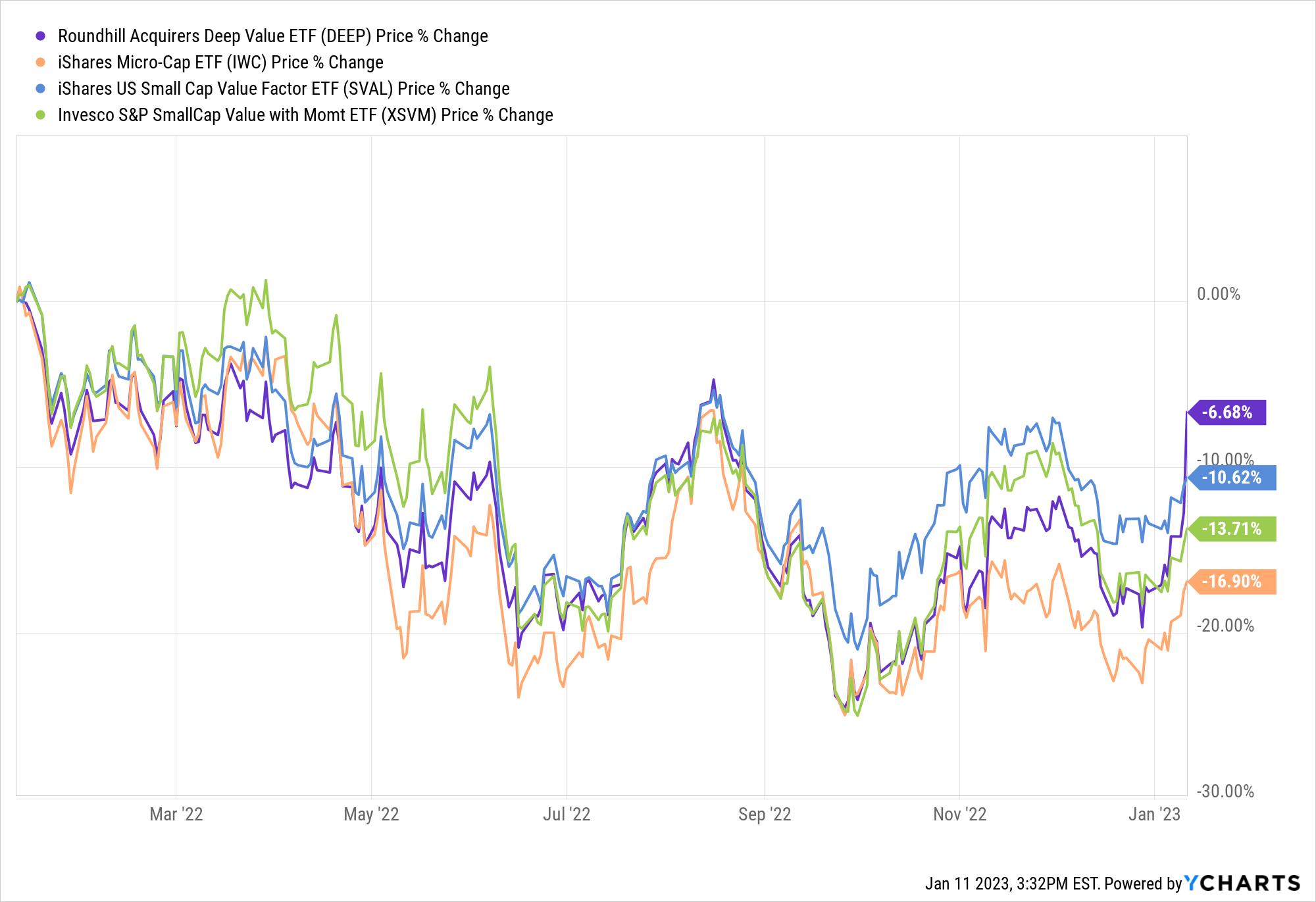

Any performance before October 23, 2020 on DEEP should be ignored. It was a different strategy run by a different team following a different index. The ticker was taken over and it bears no similarity to what the fund was before that date. It is too bad because I feel they would have a lot more AUM if the previous history of the large-cap strategy was removed.

XSVM is a value momentum fund. I have found that value and momentum work well together. Just be aware that there is another factor at work and it isn’t a pure size and value premium.

DEEP has the highest expense ratio at 0.80%. XSVM clocks in at 0.36% and SVAL is 0.20%. Although DEEP is the highest, don’t discount it. True active small-cap funds should charge a little extra premium. DEEP has a fairly extensive process to remove high-risk companies. It is a concentrated and focused fund. They need to command a higher expense as the fund will probably never amass billons of AUM. And I hope it never does because then they will employ methods that water down the size and value premium. All three have acceptable expense ratios.

My recommendation is to place all three in your portfolio in the allocation designated for small size and deep value. It is also my firm belief that some of the best equity premiums of the next 10 years will be size and value.

Be the first to comment