Alistair Berg/DigitalVision via Getty Images

Dear readers/followers,

Westlake (NYSE:WLK) is a company I’ve been writing about before, and consider to be qualitative. It, unfortunately, mixes a low yield with this, in a sector where high yields are typically more “standard”. Most basic materials companies I own come with a yield of no less than 4-6% on a YoC basis, and WLK does not even offer half that at current prices.

Still, there is quality to be had, and a reason for why WLK is a popular investment with many. Let’s use this article to revisit the case for this company, and look at what we might expect for the year of 2023.

Westlake – Revisiting the company for 2023

So, Westlake is in no way a bad or risky business, beyond the typical specifics of its cyclicality related to its activities in the basic materials segment. Westlake is a vertically integrated producer of vinyls, polymers, and building products. Their selection includes some of the most basic material components in the world, including things like packaging, automotive, coatings, water treatment, refrigerants, and the infrastructure/Construction sector.

This makes Westlake similar to other companies I follow in the same segment. WLK is focused on Vinyls and Olefins, and part of the reason investors like this company so much is the degree of vertical integration we find here. The company owns large parts of its own supply chain meaning that while it won’t be completely immune here, it’ll probably be at the very least more protected at this time of inflation and cost increases.

WLK IR (WLK IR)

Major products include PE, Styrene Monomer, and PC, which are materials found in basically every segment on earth. Plastic industry building blocks, insulation, profiles, piping and the like.

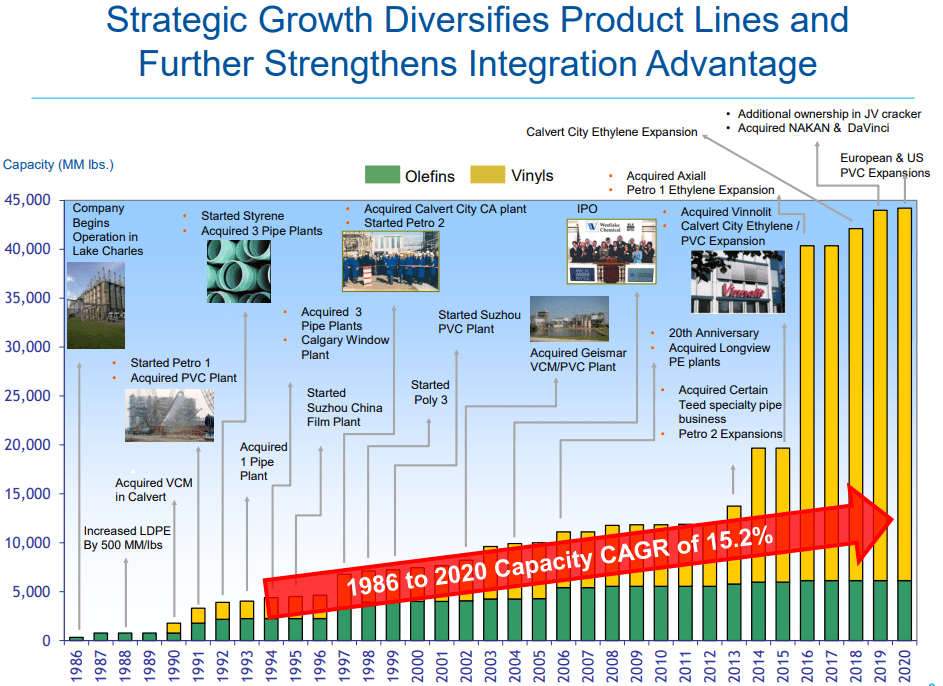

The company has the capacity to produce millions of pounds of the stuff on an annual basis, not just in the US, but in facilities in Germany. It’s German exposure is not necessarily an advantage in this particular environment, but it’s something I see as a fundamental strength going forward, as I’m looking for globally diversified businesses to invest in.

Westlake benefits very highly from integrated production facilities that take raw materials into end-products and higher VAP chemicals, and in its entire company together with M&As and JV has aggregate production capacities of 44.3B Lbs.

The primary trend to look at for WLK, aside from straight sales, is feedstock acquisition and trends. It acquires most of the required ethylene from OpCo through Ethane feedstock, and overall, WLK is one of the more integrated chemical companies I’ve seen – not just in feedstock, but in electricity, steam, and other resources/products that the company needs, which theoretically means it should have done better than most/all of my other chemical holdings because these are not as well-integrated.

This is somewhat the case – but not as much as you’d think. Outperformance is here, but it’s not as though as it’s 20% better than the market, as some of my more successful picks.

The company operates facilities in 11 nations and is the #2 producer of specialty polyvinyl chloride on earth. It’s also #2 in PVC and Chlor-alkali, and #2 in PVC fittings in all of the Americas.

Also, M&As are a heavy part of this company’s overall strategy.

WLK IR (WLK IR)

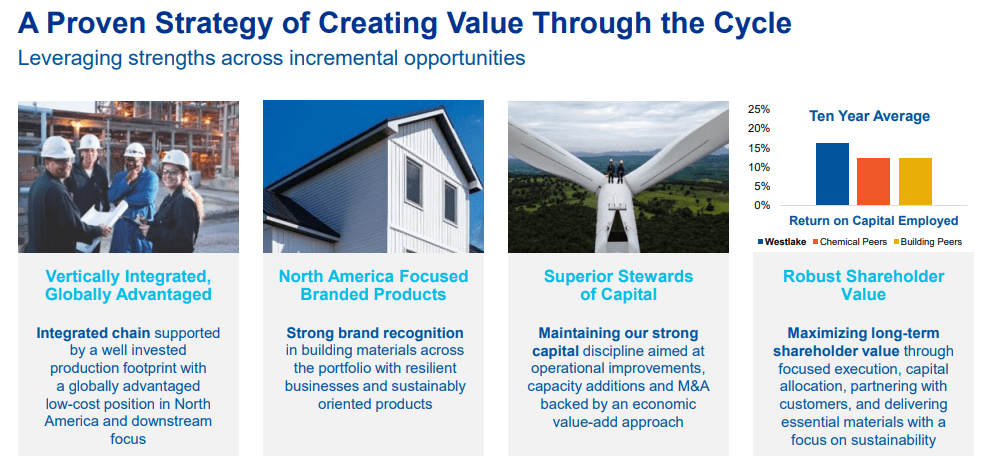

Latest results are good, but not stellar. 3Q22 came in above YoY on the top-line in sales, but net income was down 34% YoY due to legal charges and other headwinds. The company’s EBITDA saw a decrease of 25%. The company manages to stay well above board due to accretive M&As, and with 85%+ of its production NA-based, it’s relatively well-insulated from the ongoing troubles that currently are in Europe.

The company’s balance sheet continues to be top-class, with $1.8B in cash/equivalent, and $4.8B in debt, meaning net debt of around $3B. This debt is attractively laddered at good rates though, with average maturity of 17 years at a rate of 3.2%. It’s well below the current interest rate headwinds, and it’s not an exaggeration to say that Westlake is one of the most conservatively leveraged companies I’ve ever looked at in this field.

The headwinds are far from only “legal”. Westlake is equally impacted by global demand headwinds, driving down sales prices for broadly-produced commodities like PE and PVC resin, particularly true outside of the NA due to increased logistical costs and other issues. Lower infrastructure activity is also causing issues for Westlake, as demand for infrastructure-related PVC products and sales decline. Energy, despite the company’s vertical integration, is also a major concern in terms of pricing – particularly, of course, in European Geography.

However, its leading market positions and globally advantaged energy costs make certain that it stays as high as it “can”, and remains one of the more fundamentally appealing businesses here.

WLK IR (WLK IR)

So, the company presents a relatively simple thesis for 3Q22 and going into the fiscal of 2023. The demand side for many of the company’s core products is tight, given the slowing rate of construction demand due to interest/mortgage. While repair and remodeling remain stable, the construction demand is influencing things here, and this might persist for 1-2 years, even if the long-term fundamentals of housing in NA, due to underbuilding, remain solid.

There are also tailwinds in the form of the Infrastructure Investment and Jobs Act, with plenty of projects coming online.

At the same time, the NA cost-advantaged production of chemicals during a time of high energy prices remains appealing, with Epoxy extending the company’s overall global end markets.

However, the image that I want to leave you with as we move on here, is that the shorter-term trends are unclear, and the company might be moving lower. The reasons for this are the potential construction materials chemicals company, of slowdown in Asia. Westlake has a large exposure to Asia, so any large slowdown – which I believe is not only happening, it already has happened and is continuing – will heavily impact sales.

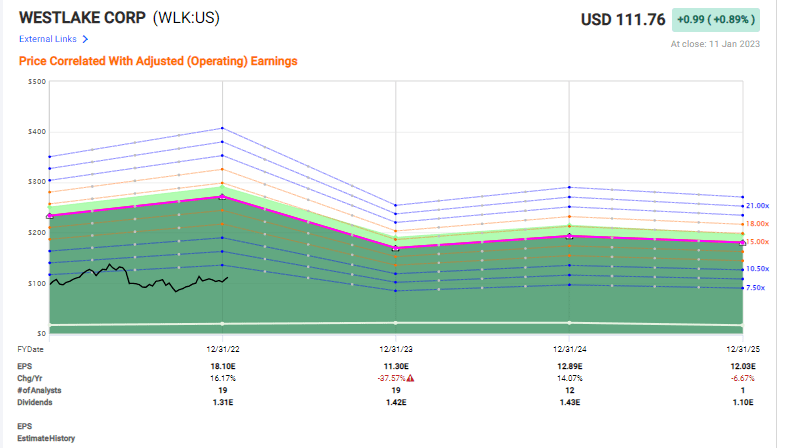

This is part of the reason for the relatively declining EPS we’re going to see in the forecast side of things – because Westlake primarily sells exactly these chemicals (PVC, Acetyls, EDC, epoxies for construction, etc.), and much of the recent growth hasn’t just been US demand, but Asia.

Demand due to infrastructure increase in the US would of course be very welcome to offset some of this, but the clarity here is somewhat lacking.

Let’s look at what happens with the company’s forecasts due to this.

Westlake Valuation

So, here we run into some problems. Remember that I invest in a lot of Chemicals, and I analyze a lot of these companies. Unlike peers such as BASF (OTCQX:BASFY) and in some cases even with companies like LyondellBasell (LYB) which has a market cap that’s almost six times as large as Westlake, Westlake does not have a comparatively great luxury of diversification at this particular time.

BASF does better even in trough years, and that is despite being a cyclical chemicals company. Westlake is more cyclical because it’s dependent on fewer products, even if Westlake in turn is equally or more vertically integrated than BASF – just look at the fears that Ludwigshafen was going to be wound down for a while due to natgas shortage, a primary BASF feedstock.

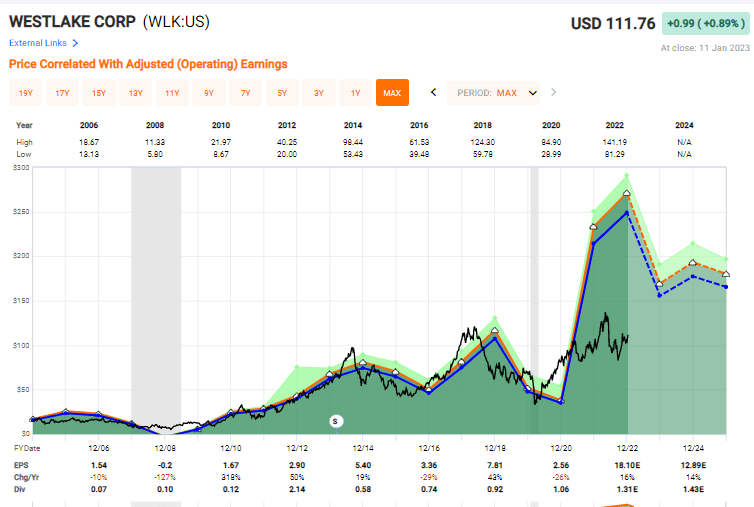

Westlake remains very lumpy in terms of earnings. While it had an absolutely explosive 2021, with adjusted earnings growth of over 500%, this is not a company that can be relied upon not provide stability either in earnings or share price.

If bought at share prices such as the ones we’re seeing right now, the comparative returns would have been mostly negative for a period of 4-8 years, or barely above 2% annually. This of course disregards that the current earnings trends are vastly different than we saw back in 2017-2018, and 2013-2014. However, the expectation has always been for Westlake’s earnings to normalize at higher levels. But they never have – at least not for the time being.

WLK Valuation (F.A.S.T graphs)

Because of that, I take a more conservative view of Westlake’s near term and even its longer-term potential. Take a look at the current trends.

F.A.S.T graphs WLK (F.A.S.T graphs)

Bulls will argue that this new level of EPS will mean a normalization to higher multiple levels – eventually. And maybe so – but let me tell you something as an experienced value investor. Any time you have a company that “should” hit some new highs based on new earnings or trends, it often times doesn’t materialize for many, many years, or it doesn’t materialize at all. There is an upside here – of that we are agreed.

The debate is regarding the size of this upside.

I would be very cautious forecasting this company at anything above 10-12x this normalized new P/E range. Based on current forecasts, this means that we’re looking at a 5%-9.98% annualized upside. Given the low-end range here, I would not consider that all that attractive.

Especially when we consider that we’re investing in the midst of a downcycle. Earnings will very likely go down at least in the next fiscal, and we’re in a rocky market characterized by recessionary trends.

What is the company able to deliver in times like those?

I can’t point to any one specific area and say “This one is definitely going to underperform”. I can only say that the mix of the following factors:

- A very rocky/lumpy EPS tradition

- A sub-par dividend

- Plenty of peers with bigger size

- Exposure to APAC infrastructure trends

…make for a tough sell for me here. If the company spent a little more on that dividend, conservative 10x P/E returns might have been 8-9% – and in that case, I could have been more welcoming to an investment like this.

But conservative annualized return potential is one of the things I am looking for. I don’t always get it, I’ll be the first to admit. But I mostly get it – and I make sure of that by not going into down-trend investments at these sorts of forecasts.

Much of the previous positivity for the company is now based on the fact that the company can offer somewhat close to repeat performances for EPS following 2021 – which it didn’t. Just as before, we’re at a top in 2022, that’s going to be declining over time, at a forecasted negative 1.61% growth rate.

What should we pay for such a business?

I bought my WLK at below $100/share, and my previous PT was $100. While analysts are somewhat more positive than me, they aren’t positive on the stock at $112. 17 analysts following the stock are at $85-$138 in range, with an average of $111.5. That means that at the current share price, S&P Global analysts believe the company to be 0.2% overvalued. Only 3 analysts give the company a buy.

I would go so far as to say that the company is more than 5% overvalued, with my previous conservative price target of $100. At that, we get a conservative annualized RoR that’s around 8% on the low side, which is enough for me to be interested in.

Thesis

My thesis for WLK is currently:

- A superb chemicals company with excellent fundamentals – possibly one of the most vertically integrated chemicals plays on the market in certain industries, and the company has world-class management.

- However, based on the valuation, I reiterate my previous price target and rating for the company. There’s too much uncertainty in current trends for me to go much higher here.

- WLK is a “HOLD” here. A price target that I would consider attractive for investment based on my goals would be around $100/share – though every investor of course needs to look at their own targets, goals, and strategies. I would also always consult with a finance professional before making investment decisions such as this.

Remember, I’m All About:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company isn’t cheap or has an upside high enough to qualify as a “BUY” here.

Be the first to comment